|

市場調查報告書

商品編碼

1708208

肱骨外上髁炎治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Lateral Epicondylitis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

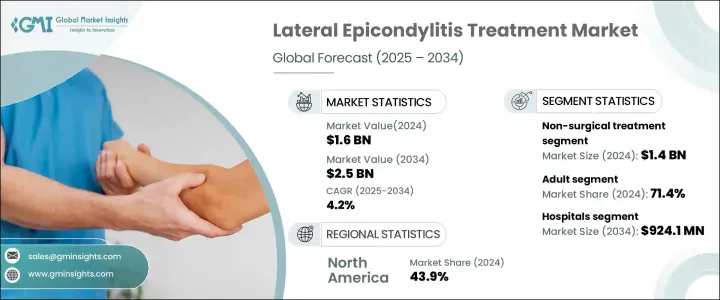

2024 年全球外上髁炎治療市場價值為 16 億美元,預計 2025 年至 2034 年期間的複合年成長率為 4.2%。外上髁炎(俗稱網球肘)盛行率的不斷上升主要是由於人們參與運動和其他體育活動的增加。隨著越來越多人參與高強度運動和重複性動作練習,罹患這種疾病的可能性也隨之上升。此外,人們對早期診斷和治療方案的認知不斷提高,導致對手術和非手術介入的需求也越來越高。市場也見證了治療方式的重大創新,包括生物療法和微創手術,為治療病情提供了更安全、更有效的解決方案。隨著醫療保健提供者優先考慮以患者為中心的方法並強調預防保健的重要性,對物理治療和皮質類固醇注射等非侵入性療法的需求激增,促進了整體市場的成長。

推動市場擴張的另一個主要因素是老年人口的增加,老年人更容易罹患外上髁炎等肌肉骨骼疾病。尤其是已開發經濟體的老齡人口擴大選擇非手術治療,因為與手術相比,非手術治療恢復時間更快、風險更低。富血小板血漿 (PRP) 和幹細胞治療等創新療法正在獲得關注,並在疼痛管理和組織再生方面顯示出良好的效果。這些進步不僅為傳統手術提供了有效的替代方案,而且也符合患者對微創手術日益成長的偏好,進一步推動了市場成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16億美元 |

| 預測值 | 25億美元 |

| 複合年成長率 | 4.2% |

外上髁炎治療市場大致分為非手術和手術治療兩類,其中非手術治療佔主導地位。 2024年,非手術治療領域創造了14億美元的收入。非手術療法,包括物理療法、藥物療法、支架療法和衝擊波療法,已被證明在控制疼痛和加速康復方面具有很高的療效。由於這些治療方法安全、停機時間短且經濟高效,患者越來越喜歡它們。隨著越來越多的人尋求保守方法來治療外上髁炎,對非手術治療的需求預計將繼續上升。

按年齡層分析市場時,成年人佔據主導地位,佔 2024 年 71.4% 的市佔率。成年人由於日常工作或娛樂活動中涉及重複的動作,更容易患上外上髁炎。體育比賽和健身趨勢的不斷成長進一步增加了這種疾病的盛行率,推動了對有效治療方案的需求。此外,對疼痛管理解決方案的需求推動了非手術方法的不斷進步,確保患者能夠獲得安全可靠的治療選擇。

2024 年,美國外上髁炎治療市場創收 6.56 億美元,鞏固了在全球市場中的重要地位。體育運動和體力勞動等體力活動的頻繁發生,導致該國外上髁炎病例數量增加。美國市場高度重視提供有效的疼痛管理解決方案,包括皮質類固醇注射和局部治療,因此持續蓬勃發展。生物治療和再生醫學領域的持續研發努力進一步鞏固了中國在全球外上髁炎治療領域的主導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 外上髁炎和運動相關傷害的發生率不斷上升

- 微創手術日益受到青睞

- 治療方式的進步

- 產業陷阱與挑戰

- 治療費用高

- 替代療法的可用性

- 成長動力

- 成長潛力分析

- 監管格局

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依治療類型,2021 年至 2034 年

- 主要趨勢

- 非手術治療

- 藥物

- 物理治療

- 矯正器和支架

- 其他非手術治療

- 手術治療

- 關節鏡手術

- 開放性手術

- 其他外科治療

第6章:市場估計與預測:依年齡層,2021 年至 2034 年

- 主要趨勢

- 兒科

- 成人

- 老年

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 骨科診所

- 居家照護環境

- 其他最終用途

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 3M Company

- BTL

- DJO Global (Enovis)

- Folsom Orthopaedics & Sports Medicine

- GlaxoSmithKline

- MedStar Health

- Merck & Co

- Novartis

- Ossur Corporate

- Pfizer

- Pharmascience

- ReLiva Physiotherapy & Rehab

- Scandinavian Physiotherapy Center

- Zimmer Biomet

The Global Lateral Epicondylitis Treatment Market was valued at USD 1.6 billion in 2024 and is projected to grow at a CAGR of 4.2% between 2025 and 2034. The growing prevalence of lateral epicondylitis, commonly known as tennis elbow, is primarily driven by increasing participation in sports and other physical activities. As more individuals engage in high-impact sports and repetitive motion exercises, the likelihood of developing this condition continues to rise. Additionally, heightened awareness about early diagnosis and treatment options has led to a higher demand for both surgical and non-surgical interventions. The market has also witnessed significant innovation in treatment modalities, including biological therapies and minimally invasive procedures, which offer safer and more effective solutions for managing the condition. As healthcare providers prioritize patient-centric approaches and emphasize the importance of preventive care, the demand for non-invasive therapies, such as physical therapy and corticosteroid injections, has surged, contributing to the overall market growth.

Another major factor propelling market expansion is the rising geriatric population, which is more susceptible to musculoskeletal conditions, such as lateral epicondylitis. The aging demographic, particularly in developed economies, is increasingly opting for non-surgical treatments that offer faster recovery times and lower risks compared to surgical procedures. Innovative therapies such as platelet-rich plasma (PRP) and stem cell treatments are gaining traction, offering promising outcomes in pain management and tissue regeneration. These advancements not only provide effective alternatives to traditional surgery but also align with the growing patient preference for minimally invasive options, further driving market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 4.2% |

The lateral epicondylitis treatment market is broadly segmented into non-surgical and surgical treatment categories, with non-surgical options leading the way. In 2024, the non-surgical treatment segment generated USD 1.4 billion in revenue. Non-surgical therapies, including physical therapy, medications, braces, and shockwave therapy, have demonstrated high efficacy in managing pain and accelerating recovery. Patients increasingly prefer these treatments due to their safety, reduced downtime, and cost-effectiveness. As more individuals seek conservative approaches to manage lateral epicondylitis, the demand for non-surgical therapies is expected to continue its upward trajectory.

When analyzing the market by age group, adults dominated the landscape, accounting for 71.4% of the market share in 2024. Adults are more prone to developing lateral epicondylitis due to repetitive movements involved in their daily work or recreational activities. The growing number of sports competitions and fitness trends has further increased the prevalence of this condition, driving the need for effective treatment options. Furthermore, the demand for pain management solutions has led to continuous advancements in non-surgical methods, ensuring that patients have access to safe and reliable treatment options.

The U.S. lateral epicondylitis treatment market generated USD 656 million in 2024, securing its position as a key player in the global landscape. The high incidence of physical activity, including sports and manual labor, has led to an increased number of lateral epicondylitis cases in the country. With a strong emphasis on providing effective pain management solutions, including corticosteroid injections and topical treatments, the U.S. market continues to thrive. Ongoing research and development efforts in biological therapies and regenerative medicine have further strengthened the country's dominance in the global lateral epicondylitis treatment sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of lateral epicondylitis and sports-related injuries

- 3.2.1.2 Growing preference for minimally invasive procedures

- 3.2.1.3 Advancement in treatment modalities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Availability of alternative therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Non-surgical treatment

- 5.2.1 Medications

- 5.2.2 Physical therapy

- 5.2.3 Orthotics and braces

- 5.2.4 Other non-surgical treatments

- 5.3 Surgical treatment

- 5.3.1 Arthroscopic surgery

- 5.3.2 Open surgery

- 5.3.3 Other surgical treatments

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric

- 6.3 Adult

- 6.4 Geriatric

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Orthopedic clinics

- 7.5 Homecare settings

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 BTL

- 9.3 DJO Global (Enovis)

- 9.4 Folsom Orthopaedics & Sports Medicine

- 9.5 GlaxoSmithKline

- 9.6 MedStar Health

- 9.7 Merck & Co

- 9.8 Novartis

- 9.9 Ossur Corporate

- 9.10 Pfizer

- 9.11 Pharmascience

- 9.12 ReLiva Physiotherapy & Rehab

- 9.13 Scandinavian Physiotherapy Center

- 9.14 Zimmer Biomet

2025年全球肱骨外上髁炎治療市場報告

2025年全球肱骨外上髁炎治療市場報告 全球先進整形外科技術市場

全球先進整形外科技術市場 歐洲脊椎導航市場:分析與預測(2023-2032)骨科支撐系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2025年全球足下垂治療設備市場報告2025年全球整形外科配件市場報告2025年全球顳顎關節植入市場報告

歐洲脊椎導航市場:分析與預測(2023-2032)骨科支撐系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2025年全球足下垂治療設備市場報告2025年全球整形外科配件市場報告2025年全球顳顎關節植入市場報告 膝關節腫脹治療市場規模、佔有率、成長分析(按類型、按藥物療法、按手術、按最終用戶、按地區)- 行業預測 2025-2032

膝關節腫脹治療市場規模、佔有率、成長分析(按類型、按藥物療法、按手術、按最終用戶、按地區)- 行業預測 2025-2032 整形外科支撐系統市場規模、佔有率及成長分析(按產品類型、材料、應用、分銷管道、病患細分及地區)-2025-2032 年產業預測

整形外科支撐系統市場規模、佔有率及成長分析(按產品類型、材料、應用、分銷管道、病患細分及地區)-2025-2032 年產業預測 2025-2029年全球整形外科製造外包市場

2025-2029年全球整形外科製造外包市場