|

市場調查報告書

商品編碼

1685145

發泡聚丙烯 (EPP) 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Expanded Polypropylene (EPP) Foam Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

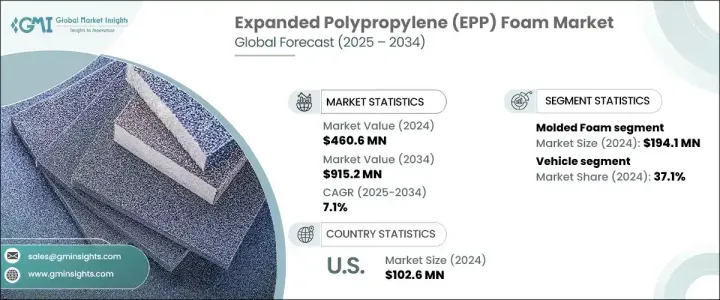

2024 年全球發泡聚丙烯市場規模達到 4.606 億美元,預計 2025 年至 2034 年期間的複合年成長率為 7.1%。這一成長主要受到汽車、包裝、航太和消費品等主要產業需求不斷成長的推動。隨著企業不斷尋求輕質和高性能材料,EPP 泡棉因其出色的緩衝、抗衝擊和能量吸收能力而脫穎而出。這些特性使其成為多個領域不可或缺的材料,尤其是在減輕重量和耐用性至關重要的行業。

EPP 泡沫越來越受歡迎,是因為與傳統泡沫材料相比,它具有多功能性和優異的性能。它因其高強度重量比、隔熱性和可回收性而廣受認可,符合全球永續發展的趨勢。隨著嚴格的法規鼓勵使用環保材料,製造商正在將 EPP 泡沫融入其產品中以滿足不斷發展的行業標準。此外,製造技術的進步正在提高產品品質、客製化選項和成本效率,進一步推動其採用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4.606 億美元 |

| 預測值 | 9.152億美元 |

| 複合年成長率 | 7.1% |

按類型細分的市場包括珠狀泡棉、模製泡棉、加工泡棉、汽車泡棉等。其中,模塑泡沫在2024年佔據主導地位,價值為1.941億美元。珠狀泡棉廣泛用於汽車、包裝和電子產品,因其減震和絕緣性能而受到重視。人造泡棉以其客製化能力而聞名,可用於需要客製化解決方案的行業,例如醫療設備和保護包裝。 EPP 泡沫類型的多樣性確保了市場的穩定擴張,滿足了行業特定的需求,同時支援向輕質、高性能材料的轉變。

市場也按應用程式細分,類別包括車輛、包裝、消費品、航太、建築、體育和休閒等。 2024 年,汽車佔據了 37.1% 的市場佔有率,隨著汽車製造商繼續優先考慮節能和抗衝擊材料,需求預計會增加。在包裝方面,EPP泡棉為電子產品、電器和易腐物品等易碎商品提供卓越的保護。電子商務產業的快速擴張進一步加速了其對保護性包裝解決方案的需求。航太製造商越來越依賴 EPP 泡沫的抗衝擊和隔熱性能,而其在消費品中的適應性凸顯了其在各個行業中的重要性。

2024 年,美國發泡聚丙烯市場產值達到 1.026 億美元,未來幾年將大幅成長。強大的汽車產業優先考慮輕量化和吸能材料,仍然是這一成長的主要驅動力。此外,蓬勃發展的電子商務產業也推動了對先進保護性包裝的需求,以適應消費者購買行為的轉變。美國擁有先進的製造設施並且注重創新,進一步鞏固了該國在全球 EPP 泡沫市場的領先地位。隨著對高性能和永續材料的需求不斷成長,EPP 泡沫預計將在多個行業中發揮更大的作用,推動長期市場擴張。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 珠狀泡沫

- 模塑泡沫

- 人造泡沫

- 汽車泡棉

- 其他

第 6 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 車輛

- 包裝

- 消費品

- 航太

- 建築與施工

- 運動與休閒

- 其他

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 汽車

- 電子產品

- 醫療的

- 包裝

- 航太

- 建造

- 其他

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- JSP Corporation

- BASF SE

- Kaneka Corporation

- Furukawa Electric Co.

- DS Smith PLC

- Hanwha Corporation

- Sonoco Products Company

- The Woodbridge Group

- Knauf Industries GmbH

- Greiner Holding AG

- Recticel NV

- Armacell International GmbH

- Zotefoams plc

- Swedfoam AB

- FoamPartner AG

The Global Expanded Polypropylene Foam Market reached USD 460.6 million in 2024 and is projected to expand at a CAGR of 7.1% between 2025 and 2034. This growth is largely driven by increasing demand from key industries such as automotive, packaging, aerospace, and consumer goods. As businesses continue to seek lightweight and high-performance materials, EPP foam stands out for its exceptional cushioning, impact resistance, and energy absorption capabilities. These properties make it an indispensable material across multiple sectors, especially in industries where weight reduction and durability are critical.

EPP foam's growing popularity stems from its versatility and superior performance compared to conventional foam materials. It is widely recognized for its high strength-to-weight ratio, thermal insulation, and recyclability, aligning with the global push toward sustainability. With stringent regulations encouraging eco-friendly materials, manufacturers are integrating EPP foam into their products to meet evolving industry standards. Additionally, advancements in manufacturing techniques are enhancing product quality, customization options, and cost-efficiency, further fueling its adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $460.6 Million |

| Forecast Value | $915.2 Million |

| CAGR | 7.1% |

Market segmentation by type includes bead foam, molded foam, fabricated foam, automotive foam, and others. Among these, molded foam dominated in 2024, accounting for USD 194.1 million. Bead foam, widely used in automotive, packaging, and electronics, is valued for its shock-absorbing and insulating properties. Fabricated foam, known for its customization capabilities, serves industries requiring tailored solutions, such as medical devices and protective packaging. The diverse range of EPP foam types ensures a steady market expansion, catering to industry-specific demands while supporting the transition toward lightweight, high-performance materials.

The market is also segmented by application, with categories including vehicles, packaging, consumer goods, aerospace, building and construction, sports and leisure, and others. Vehicles accounted for a substantial 37.1% market share in 2024, with demand expected to rise as automakers continue prioritizing energy-efficient and impact-resistant materials. In packaging, EPP foam provides superior protection for fragile goods such as electronics, appliances, and perishables. The rapid expansion of the e-commerce industry has further accelerated its demand for protective packaging solutions. Aerospace manufacturers increasingly rely on EPP foam for impact resistance and thermal insulation, while its adaptability in consumer goods highlights its importance across various industries.

The U.S. expanded polypropylene foam market generated USD 102.6 million in 2024 and is poised for significant growth in the coming years. A strong automotive industry, prioritizing lightweight and energy-absorbing materials, remains a primary driver of this growth. Additionally, the booming e-commerce sector has fueled the need for advanced protective packaging, aligning with shifting consumer purchasing behaviors. The presence of advanced manufacturing facilities and a focus on innovation in the U.S. further solidify the country's leading position in the global EPP foam market. As demand for high-performance and sustainable materials continues to rise, EPP foam is expected to play an even greater role across multiple industries, driving long-term market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bead foam

- 5.3 Molded foam

- 5.4 Fabricated foam

- 5.5 Automotive foam

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Vehicle

- 6.3 Packaging

- 6.4 Consumer goods

- 6.5 Aerospace

- 6.6 Building & construction

- 6.7 Sports & leisure

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Electronics

- 7.4 Medical

- 7.5 Packaging

- 7.6 Aerospace

- 7.7 Construction

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 JSP Corporation

- 9.2 BASF SE

- 9.3 Kaneka Corporation

- 9.4 Furukawa Electric Co.

- 9.5 DS Smith PLC

- 9.6 Hanwha Corporation

- 9.7 Sonoco Products Company

- 9.8 The Woodbridge Group

- 9.9 Knauf Industries GmbH

- 9.10 Greiner Holding AG

- 9.11 Recticel NV

- 9.12 Armacell International GmbH

- 9.13 Zotefoams plc

- 9.14 Swedfoam AB

- 9.15 FoamPartner AG

聚丙烯硬質泡棉市場按產品類型、製造流程、密度、終端用途產業和應用分類-全球預測,2026-2032年

聚丙烯硬質泡棉市場按產品類型、製造流程、密度、終端用途產業和應用分類-全球預測,2026-2032年 2026年全球閉孔泡棉市場報告

2026年全球閉孔泡棉市場報告 發泡聚丙烯(EPP)泡沫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

發泡聚丙烯(EPP)泡沫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球閉孔聚氨酯泡棉市場規模、佔有率、趨勢與成長分析報告

2026-2034年全球閉孔聚氨酯泡棉市場規模、佔有率、趨勢與成長分析報告 發泡聚丙烯市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測

發泡聚丙烯市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測 發泡聚丙烯(EPP)市場規模、佔有率和成長分析(按類型、最終用途產業、應用和地區分類)-2026-2033年產業預測

發泡聚丙烯(EPP)市場規模、佔有率和成長分析(按類型、最終用途產業、應用和地區分類)-2026-2033年產業預測 全球EPP泡沫市場、市場規模及預測分析(2018-2034)

全球EPP泡沫市場、市場規模及預測分析(2018-2034) 全球 EPP 泡棉市場(按類型、應用和地區)預測(至 2030 年)按應用、產品類型、製程和密度分類的發泡聚丙烯市場—2025-2032 年全球預測

全球 EPP 泡棉市場(按類型、應用和地區)預測(至 2030 年)按應用、產品類型、製程和密度分類的發泡聚丙烯市場—2025-2032 年全球預測 發泡聚丙烯市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭細分,2020-2030 年)

發泡聚丙烯市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭細分,2020-2030 年)