|

市場調查報告書

商品編碼

1684713

雙人自行車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Tandem Bike Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

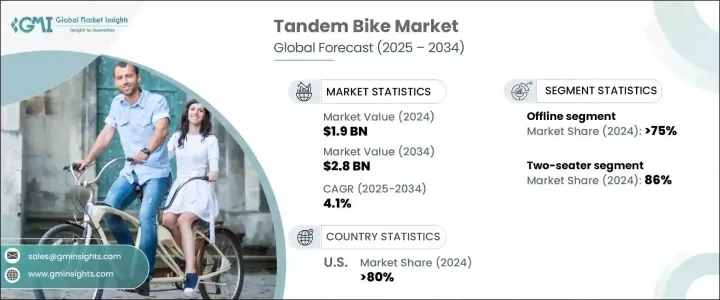

2024 年全球雙人自行車市場價值為 19 億美元,預計 2025 年至 2034 年期間的複合年成長率為 4.1%。這些自行車為不同技術水平的騎乘者提供獨特、愉快的體驗,成為家庭、情侶和團體的熱門選擇。隨著越來越多的人尋求在城市公園、風景小徑和旅遊目的地享受令人興奮的戶外體驗,雙人自行車的普及率持續上升。

此外,人們越來越注重健康生活方式和對休閒騎行的日益偏好也促進了市場擴張。越來越多的人選擇騎自行車來增強體質,同時與親人共度美好時光,因此雙人自行車成為共享戶外探險的有吸引力的選擇。這一成長背後的另一個驅動力是環保型交通替代品的興起。隨著世界各地的城市加大對自行車基礎設施和永續發展計畫的投資,雙人自行車正成為可行且環保的選擇。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 19億美元 |

| 預測值 | 28億美元 |

| 複合年成長率 | 4.1% |

雙人自行車市場按分銷管道分類,到 2024 年,線下銷售將佔總市場佔有率的 75%。由於雙人自行車需要仔細考慮適合度、重量和舒適度,因此買家通常選擇在店內購買以確保選擇正確的型號。購買前的試騎親身體驗,讓消費者對產品品質更有信心,有利於線下銷售的主導地位。雖然由於便利性和可近性,線上銷售正在穩步成長,但實體店購物仍然是雙人自行車買家的首選。

按騎乘者配置分類,雙座雙人自行車佔據最大佔有率,到 2024 年將佔據 86% 的市場佔有率。其輕巧的設計和方便用戶使用的特性使其適合休閒騎行、通勤和休閒探險。製造商不斷在這一領域進行創新,推出採用改良材料、增強懸吊和先進齒輪系統的雙人自行車,以滿足各種騎乘需求。對於輕型和高效雙座車型的持續需求預計將使該類別車型繼續佔據市場領先地位。

2024 年,美國將主導全球雙人自行車市場,佔有 80% 的佔有率。該國擁有完善的自行車文化,有廣泛的自行車道、風景路線和國家公園支撐,推動了這個令人印象深刻的市場佔有率。在美國,越來越多的人選擇騎雙人自行車來健身、休閒和進行環保交通。政府旨在擴大自行車基礎設施和促進永續交通的措施進一步促進了市場成長。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 原物料供應商

- 零件供應商

- 製造商

- 技術提供者

- 經銷商

- 最終用戶

- 供應商概況

- 利潤率分析

- 定價分析

- 成本明細分析

- 技術與創新格局

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 娛樂和健身活動日益流行

- 對環保交通方式的需求不斷成長

- 探險旅遊和休閒旅遊的成長

- 高度青睞家庭和團體騎行活動

- 產業陷阱與挑戰

- 自行車道或小徑有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:自行車市場估計與預測,2021 - 2034 年

- 主要趨勢

- 路

- 山

- 折疊式的

- 電的

第 6 章:市場估計與預測:按乘客配置,2021 - 2034 年

- 主要趨勢

- 雙座

- 多座位

第 7 章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 線上

- 離線

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 休閒騎手

- 職業自行車手

- 家庭/團體騎行

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Bike Friday

- Burley Design

- Calfee Design

- Cannondale

- Co-Motion Cycles

- da Vinci Designs

- Dawes Cycles

- Hase Bikes

- Hokitika

- KHS Bicycles

- Kinethic

- Koga

- Lapierre

- MTBT Tandems (Fandango)

- Órbita Bicycles

- Rivendell Bicycle Works

- Santana Cycles

- Schwinn Bicycle Company

- Thorn Bicycles

- Trek Bicycles

The Global Tandem Bike Market was valued at USD 1.9 billion in 2024 and is projected to grow at a CAGR of 4.1% between 2025 and 2034. The increasing enthusiasm for outdoor family activities and group adventures has significantly fueled the demand for tandem bikes. These bicycles offer a unique, enjoyable experience for riders of varying skill levels, making them a popular choice for families, couples, and groups. With more individuals seeking exciting outdoor experiences in urban parks, scenic trails, and tourist destinations, the adoption of tandem bikes continues to rise.

Additionally, the surge in health-conscious lifestyles and the growing preference for recreational cycling have contributed to market expansion. People are increasingly embracing cycling as a means to improve fitness while spending quality time with loved ones, making tandem bikes an appealing option for shared outdoor adventures. Another driving force behind this growth is the rise in eco-friendly transportation alternatives. As cities worldwide invest in cycling infrastructure and sustainability initiatives, tandem bikes are emerging as a viable, environmentally friendly option.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 4.1% |

The tandem bike market is categorized by distribution channels, with offline sales accounting for 75% of the total market share in 2024. Consumers overwhelmingly prefer purchasing tandem bikes from physical retail locations, such as local bike shops and specialty stores, where they can personally examine and test the bicycles before making a decision. Because tandem bikes require careful consideration of fit, weight, and comfort, buyers often opt for in-store purchases to ensure they select the right model. The hands-on experience of test riding before purchase provides confidence in the product's quality, contributing to the dominance of offline sales. While online sales are steadily increasing due to convenience and accessibility, in-person shopping remains the primary choice for tandem bike buyers.

By rider configuration, two-seater tandem bikes represent the largest segment, accounting for 86% of the market share in 2024. These models are widely favored for their ease of use, making them ideal for couples and families looking for a fun, interactive riding experience. Their lightweight design and user-friendly nature make them suitable for leisure rides, commuting, and casual adventures. Manufacturers are continuously innovating in this segment, introducing tandem bikes with improved materials, enhanced suspension, and advanced gear systems to cater to various riding needs. The ongoing demand for lightweight and efficient two-seater models is expected to keep this category at the forefront of the market.

In 2024, the United States dominated the global tandem bike market, holding an 80% share. The country's well-established cycling culture, supported by extensive bike paths, scenic routes, and national parks, has driven this impressive market share. More individuals in the U.S. are turning to tandem bikes for fitness, leisure, and eco-friendly transportation. Government initiatives aimed at expanding cycling infrastructure and promoting sustainable transportation have further contributed to market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 Distributors

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Cost breakdown analysis

- 3.6 Technology & innovation landscape

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing popularity of recreational and fitness activities

- 3.9.1.2 Rising demand for eco-friendly transportation options

- 3.9.1.3 Growth in adventure tourism and leisure travel

- 3.9.1.4 High preference for family and group cycling activities

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Limited availability of cycling tracks or trails

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Bike, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Road

- 5.3 Mountain

- 5.4 Folding

- 5.5 Electric

Chapter 6 Market Estimates & Forecast, By Rider Configuration, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Two-seater

- 6.3 Multi-seater

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Recreational riders

- 8.3 Professional cyclists

- 8.4 Family/group riders

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Bike Friday

- 10.2 Burley Design

- 10.3 Calfee Design

- 10.4 Cannondale

- 10.5 Co-Motion Cycles

- 10.6 da Vinci Designs

- 10.7 Dawes Cycles

- 10.8 Hase Bikes

- 10.9 Hokitika

- 10.10 KHS Bicycles

- 10.11 Kinethic

- 10.12 Koga

- 10.13 Lapierre

- 10.14 MTBT Tandems (Fandango)

- 10.15 Órbita Bicycles

- 10.16 Rivendell Bicycle Works

- 10.17 Santana Cycles

- 10.18 Schwinn Bicycle Company

- 10.19 Thorn Bicycles

- 10.20 Trek Bicycles

液壓模組化閥市場:按閥類型、驅動方式、壓力範圍、流量範圍和最終用戶分類,全球預測,2026-2032年

液壓模組化閥市場:按閥類型、驅動方式、壓力範圍、流量範圍和最終用戶分類,全球預測,2026-2032年 2026年全球多串聯閥市場報告2026年全球液壓閥市場報告微流體控裝置市場按產品類型、技術、應用和最終用戶分類,全球預測(2026-2032年)

2026年全球多串聯閥市場報告2026年全球液壓閥市場報告微流體控裝置市場按產品類型、技術、應用和最終用戶分類,全球預測(2026-2032年) 全球液壓閥市場-2025-2030年預測

全球液壓閥市場-2025-2030年預測 液壓閥遠端控制系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

液壓閥遠端控制系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 多聯閥:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)

多聯閥:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年) 液壓法蘭配件市場報告:2031 年趨勢、預測與競爭分析

液壓法蘭配件市場報告:2031 年趨勢、預測與競爭分析 2024-2028年全球液壓閥市場

2024-2028年全球液壓閥市場