|

市場調查報告書

商品編碼

1684567

絞肉機市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Meat Grinder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

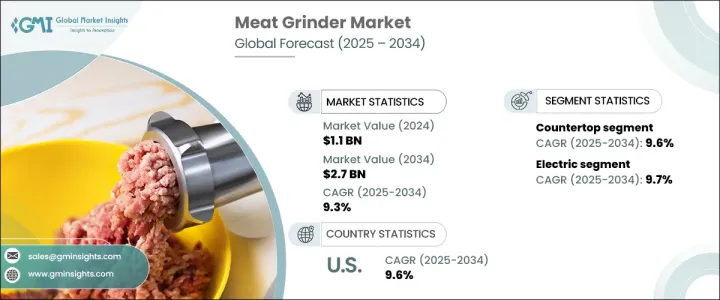

2024 年全球絞肉機市場規模達到 11 億美元,預計 2025 年至 2034 年期間的複合年成長率為 9.3%。該市場是食品加工設備產業的重要組成部分,在全球供應鏈中發揮重要作用。消費者對食品安全和肉質意識的不斷增強以及自製食品的流行趨勢推動了家庭和工業用途對絞肉機的需求。大型商業肉類加工商也在投資大容量研磨機以滿足日益成長的需求。此外,對永續生產實踐的關注和強大食品零售網路的發展進一步推動了該行業的成長。

市場分為手動和電動絞肉機。 2024 年,電動絞肉機市場佔據主導地位,估值達 9 億美元,預計 2025 年至 2034 年期間的複合年成長率為 9.7%。電動絞肉機因其效率高、使用方便而受到青睞,無論是在商業或住宅環境中都不可或缺。這些研磨機操作起來只需要很少的力氣,非常適合肉店、餐廳、餐飲準備中心和繁忙的家庭。手動部分雖然規模較小,但仍繼續迎合以可負擔性和簡單性為關鍵因素的利基市場。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 11億美元 |

| 預測值 | 27億美元 |

| 複合年成長率 | 9.3% |

市場的進一步細分包括檯面式和壁掛式絞肉機。 2024 年,桌上型絞肉機佔了 74% 的市場佔有率,預計 2025 年至 2034 年期間的複合年成長率為 9.6%。桌上型絞肉機因其便攜性、價格實惠和多功能性而廣受歡迎。它們特別受到需要中等程度絞肉能力的小型企業、屋主和餐廳的青睞。另一方面,在穩定性和耐用性至關重要的工業和大批量環境中,安裝式磨床是首選。

從地區來看,美國絞肉機市場規模在 2024 年達到 2.6 億美元,預計在 2025 年至 2034 年的預測期內複合年成長率為 9.6%。憑藉在食品加工和家電行業的領導地位,美國在北美絞肉機市場佔據主導地位。美國是世界上最大的人均肉類消費國,尤其是牛肉、豬肉和雞肉,這推動了對絞肉機的需求。這些設備廣泛用於準備香腸、漢堡和其他碎肉製品,滿足商業和住宅需求。

全球絞肉機市場也見證了技術的進步,例如智慧功能和節能設計的整合。製造商正專注於創新以增強產品功能並滿足不斷變化的消費者偏好。電子商務平台的日益普及進一步提高了市場可及性,使消費者能夠探索各種各樣的產品並做出明智的購買決定。這些因素共同表明,預測期內絞肉機市場將呈現良好的成長軌跡。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測參數

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 技術格局

- 衝擊力

- 成長動力

- 全球肉類消費量不斷增加

- 家庭肉品加工越來越受歡迎

- 肉類加工設備的技術進步

- 產業陷阱與挑戰

- 工業研磨機的初始成本高

- 嚴格的食品安全法規

- 成長動力

- 消費者購買行為分析

- 人口趨勢

- 影響購買決策的因素

- 消費者產品採用

- 首選配銷通路

- 偏好價格範圍

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品類型,2021 年至 2034 年

- 主要趨勢

- 手動絞肉機

- 電動絞肉機

第 6 章:市場估計與預測:按材料類型,2021 年至 2034 年

- 主要趨勢

- 鋁

- 鑄鐵

- 不銹鋼

- 其他(碳鋼等)

第7章:市場估計與預測:依結構,2021 – 2034 年

- 主要趨勢

- 桌上型絞肉機

- 掛裝絞肉機

- 落地式

- 桌面安裝

第 8 章:市場估計與預測:按產能,2021 年至 2034 年

- 主要趨勢

- 小型(最高 150 磅/小時)

- 中(150-500 磅/小時)

- 大型(500 磅/小時以上)

第 9 章:市場估計與預測:按營運,2021 – 2034 年

- 主要趨勢

- 輕型

- 中型

- 重負

第 10 章:市場估計與預測:按價格範圍,2021 年至 2034 年

- 主要趨勢

- 低(500 美元以下)

- 中型(500 美元 - 1000 美元)

- 高(1000 美元以上)

第 11 章:市場估計與預測:按飼料類型,2021 年至 2034 年

- 主要趨勢

- 托盤進料磨床

- 垂直進給

- 螺旋給料

- 手動推料

- 其他(真空進料等)

第 12 章:市場估計與預測:按最終用戶,2021 年至 2034 年

- 主要趨勢

- 住宅

- 商業的

- 飯店和餐廳

- 餐飲服務

- 肉店

- 其他

- 工業的

- 肉類加工廠

- 食品生產設施

第 13 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 線上

- 電子商務網站

- 公司網站

- 離線

- 大賣場和超市

- 專賣店

- 其他(百貨商場、個體店等)

第 14 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 15 章:公司簡介

- ABM Company

- ADE Germany

- AlexanderSolia GmbH

- Amisy

- Ari Makina

- ASGO

- Bizerba

- CRM srl

- Clearline

- Dadaux SAS

- Dito Sama

- Fatosa, SA

- Fimar Spa

- Hobart

- Nikai Group

- Roser Group

- Weston Brands

The Global Meat Grinder Market reached USD 1.1 billion in 2024 and is projected to grow at a CAGR of 9.3% between 2025 and 2034. This market forms a vital component of the food processing equipment sector, which plays a significant role in the global supply chain. Increasing consumer awareness about food safety and meat quality, and the rising trend of homemade food preparation have driven the demand for meat grinders for both residential and industrial purposes. Large-scale commercial meat processors are also investing in high-capacity grinders to meet the growing demand. Additionally, the focus on sustainable production practices and the development of strong food retail networks have further fueled the sector's growth.

The market is categorized into manual and electric meat grinders. In 2024, the electric meat grinder segment dominated the market with a valuation of USD 900 million and is expected to grow at a CAGR of 9.7% between 2025 and 2034. Electric grinders are preferred for their efficiency and ease of use, making them indispensable in both commercial and residential settings. These grinders require minimal effort to operate, making them ideal for butcher shops, restaurants, meal prep centers, and busy households. The manual segment, while smaller, continues to cater to niche markets where affordability and simplicity are key factors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 9.3% |

Further segmentation of the market includes countertops and mounted meat grinders. In 2024, countertop meat grinders held a 74% market share and are anticipated to grow at a CAGR of 9.6% between 2025 and 2034. Countertop grinders are popular due to their portability, affordability, and versatility. They are particularly favored by small businesses, homeowners, and restaurants that require moderate meat grinding capabilities. Mounted grinders, on the other hand, are preferred in industrial and high-volume settings where stability and durability are critical.

Regionally, the U.S. meat grinder market reached USD 260 million in 2024 and is projected to grow at a CAGR of 9.6% during the forecast period between 2025 and 2034. The country holds a dominant position in the North American market for meat grinders due to its leadership in the food processing and home appliance industries. The U.S. is the world's largest consumer of meat per capita, particularly beef, pork, and chicken, which has driven the demand for meat grinders. These devices are widely used for preparing sausages, burgers, and other ground meat products, catering to both commercial and residential needs.

The global meat grinder market is also witnessing advancements in technology, such as the integration of smart features and energy-efficient designs. Manufacturers are focusing on innovation to enhance product functionality and cater to evolving consumer preferences. The increasing penetration of e-commerce platforms has further boosted market accessibility, enabling consumers to explore a wide range of products and make informed purchasing decisions. These factors collectively indicate a promising growth trajectory for the meat grinder market over the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Technological landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing meat consumption worldwide

- 3.7.1.2 Rising popularity of home meat processing

- 3.7.1.3 Technological advancements in meat processing equipment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs for industrial grinders

- 3.7.2.2 Stringent food safety regulations

- 3.7.1 Growth drivers

- 3.8 Consumer buying behavior analysis

- 3.8.1 Demographic trends

- 3.8.2 Factors affecting buying decision

- 3.8.3 Consumer product adoption

- 3.8.4 Preferred distribution channel

- 3.8.5 Preferred price range

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Manual meat grinder

- 5.3 Electric meat grinder

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Aluminum

- 6.3 Cast iron

- 6.4 Stainless steel

- 6.5 Others (carbon steel, etc.)

Chapter 7 Market Estimates and Forecast, By Structure, 2021 – 2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Countertop meat grinder

- 7.3 Mounted meat grinder

- 7.3.1 Floor mounted

- 7.3.2 Table mounted

Chapter 8 Market Estimates and Forecast, By Capacity, 2021 – 2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Small (Up to 150 lbs/hour)

- 8.3 Medium (150-500 lbs/hour)

- 8.4 Large (Above 500 lbs/hour)

Chapter 9 Market Estimates and Forecast, By Operation, 2021 – 2034 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Light-duty

- 9.3 Medium-duty

- 9.4 Heavy-duty

Chapter 10 Market Estimates and Forecast, By Price Range, 2021 – 2034 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Low (under USD 500)

- 10.3 Medium (USD 500 - USD 1000)

- 10.4 High (above USD 1000)

Chapter 11 Market Estimates and Forecast, By Feed Type, 2021 – 2034 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Tray feed grinder

- 11.3 Vertical feed

- 11.4 Auger feed

- 11.5 Manual push feed

- 11.6 Others (vacuum feed, etc.)

Chapter 12 Market Estimates and Forecast, By End User, 2021 – 2034 (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 Residential

- 12.3 Commercial

- 12.3.1 Hotels and restaurants

- 12.3.2 Catering services

- 12.3.3 Butcher shops

- 12.3.4 Others

- 12.4 Industrial

- 12.4.1 Meat processing plants

- 12.4.2 Food manufacturing facilities

Chapter 13 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Million Units)

- 13.1 Key trends

- 13.2 Online

- 13.2.1 E-commerce website

- 13.2.2 Company website

- 13.3 Offline

- 13.3.1 Hypermarkets and supermarkets

- 13.3.2 Specialty stores

- 13.3.3 Others (department stores, individual stores, etc.)

Chapter 14 Market Estimates & Forecast, By Region, 2021 – 2034 (USD Billion) (Million Units)

- 14.1 Key trends

- 14.2 North America

- 14.2.1 U.S.

- 14.2.2 Canada

- 14.3 Europe

- 14.3.1 UK

- 14.3.2 Germany

- 14.3.3 France

- 14.3.4 Italy

- 14.3.5 Spain

- 14.3.6 Russia

- 14.4 Asia Pacific

- 14.4.1 China

- 14.4.2 Japan

- 14.4.3 India

- 14.4.4 South Korea

- 14.4.5 Australia

- 14.5 Latin America

- 14.5.1 Brazil

- 14.5.2 Mexico

- 14.6 MEA

- 14.6.1 South Africa

- 14.6.2 Saudi Arabia

- 14.6.3 UAE

Chapter 15 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 15.1 ABM Company

- 15.2 ADE Germany

- 15.3 AlexanderSolia GmbH

- 15.4 Amisy

- 15.5 Ari Makina

- 15.6 ASGO

- 15.7 Bizerba

- 15.8 C.R.M. s.r.l.

- 15.9 Clearline

- 15.10 Dadaux SAS

- 15.11 Dito Sama

- 15.12 Fatosa, S.A.

- 15.13 Fimar S.p.a.

- 15.14 Hobart

- 15.15 Nikai Group

- 15.16 Roser Group

- 15.17 Weston Brands