|

市場調查報告書

商品編碼

2038703

高速鋼切削刀具市場商機、成長要素、產業趨勢分析及2026-2035年預測。High-Speed Steel Metal Cutting Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

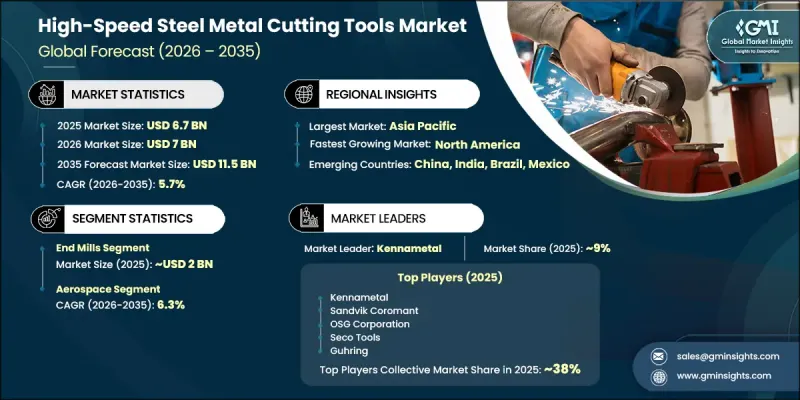

2025年全球高速鋼切削刀具市場價值為67億美元,預計到2035年將以5.7%的複合年成長率成長至115億美元。

在全球製造業成長、工業自動化以及汽車和航太等關鍵終端用戶產業需求不斷成長的推動下,該市場正在擴張。包括印度、中國和東南亞在內的新興經濟體的快速工業化進一步刺激了市場需求,因為這些地區在汽車、航太、國防和建築等行業的產量不斷成長,而這些行業都高度依賴高精度金屬切削解決方案。高速鋼成分的不斷進步,包括氮化鈦塗層技術和改進的冶金加工工藝,顯著提高了刀具的耐久性、耐磨性和切削性能,使其更適用於精密加工應用。此外,汽車製造中輕量材料的日益普及以及航太生產中先進高強度合金的廣泛應用,推動了對即使在高應力條件下也能保持精度的可靠切削刀具的需求。由於其成本效益、韌性和在各種加工過程中的通用性,高速鋼刀具在製造業中繼續廣泛應用。這些工具包括鑽頭、銑刀、絲錐、鉸刀以及其他各種工業生產必不可少的精密切削工具。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 67億美元 |

| 預測金額 | 115億美元 |

| 複合年成長率 | 5.7% |

預計到2025年,端銑刀市場規模將達到約20億美元,並在2026年至2035年間以6.3%的複合年成長率成長。此細分市場的成長主要得益於其在各製造業銑削加工中的廣泛應用。高速鋼端銑刀廣泛用於加工金屬零件上的槽、型腔、輪廓和複雜形狀。在航太製造業,這些刀具對於加工鋁合金、鈦合金和其他需要高精度加工的特殊材料至關重要。在汽車生產車間,端銑刀用於製造引擎零件、變速箱零件和結構件。其兼具粗加工和精加工功能的多功能性,提高了工作效率並減少了換刀次數。

預計到2025年,航太領域將佔據28.7%的市場佔有率,並在2035年之前以6.3%的複合年成長率成長。這一主導地位歸功於嚴格的精度標準和航太部件的複雜性。飛機結構件、引擎系統和起落架組件需要先進的加工工藝,並輔以高耐久性切削刀具。高速鋼(HSS)刀具因其韌性和抗崩刃性,在某些航太應用中備受青睞。此外,民航機、國防飛機和太空船零件的生產也推動了該領域的成長,這些生產都涉及加工鈦合金、不銹鋼和耐熱金屬等難加工材料。

美國高速鋼切削刀具市場預計到2025年將達到12億美元,並在2026年至2035年間以7%的複合年成長率成長。該國市場成長的主要驅動力是活躍的航太製造業、汽車製造業以及先進工業機械的研發。國防領域對軍用裝備和系統精密加工的需求也顯著推動了市場成長。醫療設備業透過專業製造手術器械和植入也支撐了市場需求。廣泛的工業製造活動進一步保障了切削刀具在多種應用領域的穩定消費。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 擴大航太和汽車製造

- 工業製造和機械生產的擴張

- 精密設計的醫療設備的需求日益成長

- 產業潛在風險與挑戰

- 與硬質合金和陶瓷切削刀具的競爭

- 原料成本波動與供應鏈問題

- 機會

- 拓展線上零售與電子商務平台

- 新興市場的擴張和年輕人的加入

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 交易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- HS編碼分類及貿易流量分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和形式(現代發行與傳統發行)分類的頻道覆蓋率(基於初步調查)

- 最後一公里基礎設施缺口和新興管道變化(基於初步研究)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 端銑刀

- 鑽頭

- 輕敲

- 擴孔器

- 胸針

- 其他(用於沉頭孔等)

第6章 市場估算與預測:依材料等級分類,2022-2035年

- T系列

- M系列

- 其他(例如鈷鋼)

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 轉彎

- 銑削

- 鑽孔

- 竊聽

- 其他(例如,切線等)

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 航太

- 醫療保健

- 車

- 工業製造

- 建造

- 其他(電子電氣設備等)

第9章 市場估價與預測:依銷售管道分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Top Global Player

- Sandvik Coromant

- Kennametal

- Sumitomo Electric Industries

- Seco Tools

- OSG Corporation

- Dormer Pramet

- Regional Player

- Emuge-Franken

- Niagara Cutter

- BIG Kaiser(BIG DAISHOWA Americas)

- Guhring

- Vargus

- 新興企業

- RTS Cutting Tools

- Hannibal Carbide Tool

- Toolmex Industrial Solutions

- GWS Tool Group

The Global High-Speed Steel Metal Cutting Tools Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 11.5 billion by 2035.

The market is expanding, supported by the growth of global manufacturing activities, industrial automation, and rising demand from major end-use industries such as automotive and aerospace. Rapid industrialization across emerging economies, including India, China, and Southeast Asia is further strengthening market demand as these regions experience increasing production in automotive, aerospace, defense, and construction sectors, all of which rely heavily on high-precision metal cutting solutions. Continuous advancements in high-speed steel compositions, including titanium nitride coating technologies and improved metallurgical processing techniques, have significantly enhanced tool durability, wear resistance, and cutting performance, making these tools more suitable for precision machining applications. In addition, increasing adoption of lightweight materials in automotive manufacturing and advanced high-strength alloys in aerospace production is boosting demand for reliable cutting tools capable of maintaining accuracy under high-stress conditions. High-speed steel tools continue to remain widely used in manufacturing operations due to their cost efficiency, toughness, and versatility across multiple machining processes. These tools include drills, milling cutters, taps, reamers, and various other precision cutting instruments essential for industrial production.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 5.7% |

The end mills segment accounted for around USD 2 billion in 2025 and is projected to grow at a CAGR of 6.3% between 2026 and 2035. This segment leads the market due to its extensive use in milling applications across diverse manufacturing industries. High-speed steel end mills are widely used for producing slots, cavities, profiles, and complex geometries in metal components. Aerospace manufacturing relies on these tools for machining aluminum alloys, titanium, and other specialized materials requiring high precision. Automotive production facilities utilize end mills for manufacturing engine parts, transmission components, and structural assemblies. Their adaptability for both roughing and finishing operations enhances operational efficiency and reduces tool change requirements.

The aerospace segment held a 28.7% share in 2025 and is expected to grow at a CAGR of 6.3% through 2035. This dominance is attributed to strict precision standards and the complexity of aerospace components. Aircraft structural parts, engine systems, and landing gear assemblies require advanced machining processes supported by durable cutting tools. High-speed steel tools are favored in certain aerospace applications due to their toughness and resistance to edge chipping. The segment is further supported by the production of commercial aircraft, defense aircraft, and spacecraft components, all of which involve machining of difficult materials such as titanium alloys, stainless steels, and high-temperature resistant metals.

U.S. High-Speed Steel Metal Cutting Tools Market reached USD 1.2 billion in 2025 and is forecast to grow at a CAGR of 7% from 2026 to 2035. Market growth in the country is driven by strong aerospace manufacturing activity, automotive production, and advanced industrial machinery development. The defense sector contributes significantly due to its requirement for precision machining in military equipment and systems. The medical device industry also supports demand through specialized manufacturing of surgical instruments and implants. Broad-based industrial manufacturing activities further sustain consistent consumption of cutting tools across multiple applications.

Key players operating in the Global High-Speed Steel Metal Cutting Tools Market include Dormer Pramet, Sandvik Coromant, Kennametal, OSG Corporation, Seco Tools, Guhring, Sumitomo Electric Industries, Emuge-Franken, Vargus, BIG Kaiser (BIG DAISHOWA Americas), Niagara Cutter, Hannibal Carbide Tool, GWS Tool Group, Toolmex Industrial Solutions, and RTS Cutting Tools. Companies in the high-speed steel metal cutting tools market are focusing on continuous product innovation to enhance tool life, cutting precision, and heat resistance through advanced coatings and improved metallurgy. Manufacturers are expanding their production capabilities and investing in automated manufacturing technologies to improve efficiency and reduce production costs. Strategic partnerships with automotive, aerospace, and industrial OEMs are strengthening long-term supply agreements and ensuring stable demand. Firms are also emphasizing research and development to design tools compatible with advanced materials and high-speed machining applications. Geographic expansion into emerging manufacturing hubs is helping companies capture new demand centers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material Grade

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing aerospace and automotive manufacturing

- 3.2.1.2 Expansion of industrial manufacturing and machinery production

- 3.2.1.3 Rising demand for precision-engineered medical devices

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Competition from carbide and ceramic cutting tools

- 3.2.2.2 Fluctuating raw material costs and supply chain issues

- 3.2.3 Opportunities

- 3.2.3.1 Growing online retail and e-commerce platforms

- 3.2.3.2 Expansion in emerging markets and youth participation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 End mills

- 5.3 Drills

- 5.4 Taps

- 5.5 Reamers

- 5.6 Broaches

- 5.7 Others (countersinking etc.)

Chapter 6 Market Estimates & Forecast, By Material Grade, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 T series

- 6.3 M series

- 6.4 Others (cobalt steel etc.)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Turning

- 7.3 Milling

- 7.4 Drilling

- 7.5 Tapping

- 7.6 Others (threading etc.)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Aerospace

- 8.3 Medical

- 8.4 Automotive

- 8.5 Industrial manufacturing

- 8.6 Construction

- 8.7 Others (electronics & electrical etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Top Global Player

- 11.1.1 Sandvik Coromant

- 11.1.2 Kennametal

- 11.1.3 Sumitomo Electric Industries

- 11.1.4 Seco Tools

- 11.1.5 OSG Corporation

- 11.1.6 Dormer Pramet

- 11.2 Regional Player

- 11.2.1 Emuge-Franken

- 11.2.2 Niagara Cutter

- 11.2.3 BIG Kaiser (BIG DAISHOWA Americas)

- 11.2.4 Guhring

- 11.2.5 Vargus

- 11.3 Emerging Players

- 11.3.1 RTS Cutting Tools

- 11.3.2 Hannibal Carbide Tool

- 11.3.3 Toolmex Industrial Solutions

- 11.3.4 GWS Tool Group

數控金屬切削工具機市場-全球產業規模、佔有率、趨勢、機會、預測:依機器類型、技術、應用、地區和競爭格局分類,2021-2031年

數控金屬切削工具機市場-全球產業規模、佔有率、趨勢、機會、預測:依機器類型、技術、應用、地區和競爭格局分類,2021-2031年 金屬切削工具機市場報告:按產品、銷售管道、應用和地區分類(2026-2034 年)

金屬切削工具機市場報告:按產品、銷售管道、應用和地區分類(2026-2034 年) 機械剪切機市場:依產品類型、動力來源、應用及通路分類-2026年至2032年全球預測環線切割機市場:按類型、應用、最終用戶和分銷管道分類,全球預測,2026-2032年

機械剪切機市場:依產品類型、動力來源、應用及通路分類-2026年至2032年全球預測環線切割機市場:按類型、應用、最終用戶和分銷管道分類,全球預測,2026-2032年 全球金屬切削刀具市場規模、佔有率、趨勢及成長分析報告(2026-2034年)日本金屬切削刀具市場規模、佔有率、趨勢及預測(按刀具類型、產品類型、應用和地區分類),2026-2034年

全球金屬切削刀具市場規模、佔有率、趨勢及成長分析報告(2026-2034年)日本金屬切削刀具市場規模、佔有率、趨勢及預測(按刀具類型、產品類型、應用和地區分類),2026-2034年 2026年全球金屬切削刀具市場報告2026年全球金屬切削工具機市場報告全球金屬切削刀具市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034)金屬切削刀具市場-全球產業規模、佔有率、趨勢、機會、預測:依材料、製程、最終用途、地區和競爭格局分類,2021-2031年

2026年全球金屬切削刀具市場報告2026年全球金屬切削工具機市場報告全球金屬切削刀具市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034)金屬切削刀具市場-全球產業規模、佔有率、趨勢、機會、預測:依材料、製程、最終用途、地區和競爭格局分類,2021-2031年