|

市場調查報告書

商品編碼

1666909

汽車預測技術市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Automotive Predictive Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

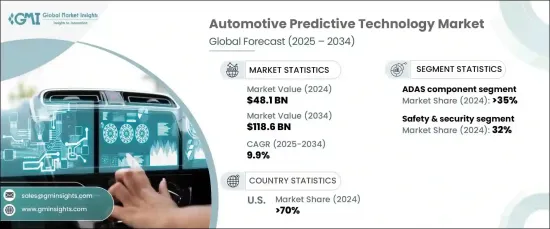

2024 年全球汽車預測技術市場價值為 481 億美元,預計 2025 年至 2034 年期間將以 9.9% 的複合年成長率強勁成長。汽車製造商正在加速採用預測技術,透過分析交通模式、駕駛員行為和車輛性能等即時資料來提高車輛安全性、防止事故並改善整體駕駛體驗。預測性維護也獲得了顯著的關注,可以提前發現潛在問題,防止意外故障,確保車輛的可靠性。

推動市場擴張的關鍵因素是電動車(EV)普及率的上升。隨著汽車產業走向永續發展,預測技術對於最佳化電動車性能和延長電池壽命變得至關重要。這些技術使用先進的分析技術來預測電池磨損、監控充電習慣並提高能源效率,確保電動車的最佳性能和使用壽命。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 481億美元 |

| 預測值 | 1186億美元 |

| 複合年成長率 | 9.9% |

市場的硬體部分包括 ADAS 組件、OBD 設備和遠端資訊處理系統。 2024 年,ADAS 組件佔據了 35% 的市場佔有率,預計到 2034 年將創造 480 億美元的市場價值。透過利用感測器、攝影機、雷達和人工智慧,這些技術使車輛能夠即時預測和降低風險,從而顯著提高道路安全。

市場也根據應用進行細分,包括預測性維護、車輛健康監測、安全保障以及駕駛模式分析。 2024 年,在全球重點關注減少交通事故死亡人數的推動下,安全和安保領域將佔據 32% 的市場佔有率。由於人為錯誤是造成道路事故的主要因素,預測技術對於預測危險和提高整體道路安全至關重要。

2024 年,美國汽車預測技術市場佔據全球 70% 的佔有率,領先全球。預測技術對於自動駕駛汽車至關重要,它使它們能夠處理來自感測器和攝影機的資料,以便在複雜的環境中導航、避免碰撞並做出快速、準確的決策。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 汽車原廠設備製造商

- 技術提供者

- 數據分析和雲端服務供應商

- 最終用途

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞及舉措

- 監管格局

- 案例研究

- 衝擊力

- 成長動力

- 對車輛安全性和效率的需求不斷增加

- 對個人化和互聯體驗的需求

- 人工智慧(AI)與機器學習(ML)的快速融合

- 連網汽車的普及率不斷提高

- 產業陷阱與挑戰

- 資料隱私和安全問題

- 實施成本高

- 成長動力

3.10 成長潛力分析

3.11 波特分析

3.12 PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 預測性維護

- 車輛健康監測

- 安全與保障

- 駕駛模式分析

- 其他

第6章:市場估計與預測:按部署,2021 - 2034 年

- 主要趨勢

- 本地

- 雲

第 7 章:市場估計與預測:按硬體,2021 - 2034 年

- 主要趨勢

- ADAS 元件

- 車載診斷系統 (OBD)

- 遠端資訊處理

第 8 章:市場估計與預測:按車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車

- 輕型商用車 (LCV)

- 重型商用車 (HCV)

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Aisin

- Aptiv

- Bosch

- Continental

- Garrett Motion

- HARMAN

- Honeywell

- Infineon

- Intel

- Lear

- Magna

- Mobileye

- NVIDIA

- NXP

- Qualcomm

- Renesas

- Siemens

- Valeo

- Visteon

- ZF Friedrichshafen

The Global Automotive Predictive Technology Market, valued at USD 48.1 billion in 2024, is expected to experience robust growth at a CAGR of 9.9% from 2025 to 2034. This growth is driven by the increasing demand for advanced safety features and driver assistance systems. Automakers are adopting predictive technologies at an accelerating pace to enhance vehicle safety, prevent accidents, and improve overall driving experiences by analyzing real-time data such as traffic patterns, driver behavior, and vehicle performance. Predictive maintenance has also gained significant traction, allowing for early detection of potential issues to prevent unexpected breakdowns and ensure greater vehicle reliability.

A key factor fueling market expansion is the rise in electric vehicle (EV) adoption. As the automotive industry moves toward greater sustainability, predictive technologies are becoming essential for optimizing EV performance and extending battery life. These technologies use advanced analytics to forecast battery wear, monitor charging habits, and enhance energy efficiency, ensuring optimal performance and longevity of EVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.1 Billion |

| Forecast Value | $118.6 Billion |

| CAGR | 9.9% |

The hardware segment of the market includes ADAS components, OBD devices, and telematics systems. In 2024, ADAS components accounted for 35% of the market share and are expected to generate USD 48 billion by 2034. The increasing demand for automation and safer driving solutions has led to the integration of ADAS features such as adaptive cruise control, lane assist, and collision detection. By leveraging sensors, cameras, radar, and artificial intelligence, these technologies enable vehicles to predict and mitigate risks in real-time, significantly enhancing road safety.

The market is also segmented by applications, including predictive maintenance, vehicle health monitoring, safety and security, and driving pattern analysis. In 2024, the safety and security segment held 32% of the market share, driven by the global focus on reducing traffic fatalities. With human error being a major factor in road accidents, predictive technologies have become crucial in anticipating hazards and improving overall road safety.

The U.S. automotive predictive technology market led the global market with a dominant 70% share in 2024. The country's leadership in developing autonomous vehicles (AVs) and advanced predictive systems has attracted significant investments from automakers and tech companies alike. Predictive technology is crucial for AVs, enabling them to process data from sensors and cameras to navigate complex environments, avoid collisions, and make quick, precise decisions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Technology providers

- 3.1.3 Data analytics & cloud service providers

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case study

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for vehicle safety & efficiency

- 3.9.1.2 Demand for personalized & connected experiences

- 3.9.1.3 Rapid integration of Artificial Intelligence (AI) and Machine Learning (ML)

- 3.9.1.4 Rising adoption of connected cars

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Data privacy & security concerns

- 3.9.2.2 High implementation costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

CHAPTER 4 : Competitive Landscape

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Predictive maintenance

- 5.3 Vehicle health monitoring

- 5.4 Safety & security

- 5.5 Driving pattern analysis

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Hardware, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 ADAS component

- 7.3 OBD

- 7.4 Telematics

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Passenger vehicle

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCVs)

- 8.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 94.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin

- 10.2 Aptiv

- 10.3 Bosch

- 10.4 Continental

- 10.5 Garrett Motion

- 10.6 HARMAN

- 10.7 Honeywell

- 10.8 Infineon

- 10.9 Intel

- 10.10 Lear

- 10.11 Magna

- 10.12 Mobileye

- 10.13 NVIDIA

- 10.14 NXP

- 10.15 Qualcomm

- 10.16 Renesas

- 10.17 Siemens

- 10.18 Valeo

- 10.19 Visteon

- 10.20 ZF Friedrichshafen

汽車預測性維護感測器市場機會、成長促進因素、產業趨勢分析及2025-2034年預測

汽車預測性維護感測器市場機會、成長促進因素、產業趨勢分析及2025-2034年預測 全球汽車預測分析市場規模、佔有率、行業分析報告(按組件、車輛類型、最終用戶、應用和地區分類)、展望和預測(2025-2032 年)

全球汽車預測分析市場規模、佔有率、行業分析報告(按組件、車輛類型、最終用戶、應用和地區分類)、展望和預測(2025-2032 年) 2032 年汽車技術市場預測:按組件、部署、車輛類型、技術、應用、最終用戶和地區進行的全球分析

2032 年汽車技術市場預測:按組件、部署、車輛類型、技術、應用、最終用戶和地區進行的全球分析 汽車預測性維護市場:2025-2032年全球預測(按組件、技術、車輛類型、部署類型、預測性維護軟體交付類型、服務類型和最終用戶分類)汽車預測分析市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車預測性維護市場:2025-2032年全球預測(按組件、技術、車輛類型、部署類型、預測性維護軟體交付類型、服務類型和最終用戶分類)汽車預測分析市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球汽車診斷市場全球汽車預測技術市場

全球汽車診斷市場全球汽車預測技術市場 全球汽車預測市場報告(2025年)

全球汽車預測市場報告(2025年) 汽車預測分析市場規模、佔有率和趨勢分析報告:按零件、應用、車輛類型、最終用途、地區和細分市場預測,2025 年至 2033 年

汽車預測分析市場規模、佔有率和趨勢分析報告:按零件、應用、車輛類型、最終用途、地區和細分市場預測,2025 年至 2033 年 汽車預後診斷市場(2025-2029)

汽車預後診斷市場(2025-2029)