|

市場調查報告書

商品編碼

1665219

空間 DC-DC 轉換器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Space DC-DC Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

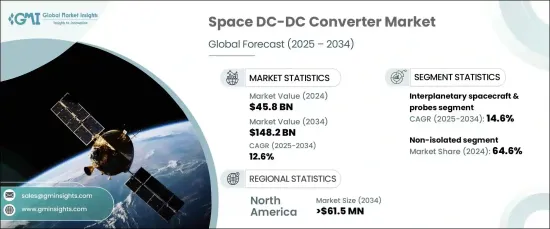

2024 年全球太空 DC-DC 轉換器市場規模達到 458 億美元,預計 2025 年至 2034 年期間將以 12.6% 的強勁複合成長率成長。小型衛星的不斷擴大部署和行星際探索的突破進一步推動了對可靠的能源轉換、分配和儲存解決方案的需求。這些尖端技術不僅最佳化了性能,而且還延長了任務壽命並降低了營運成本,使其成為未來太空探索不可或缺的一部分。

市場按類型分為非隔離式和隔離式轉換器,其中非隔離式部分將在 2024 年成為明顯的領先者,佔據 64.6% 的市場佔有率。非隔離轉換器以其高效率和緊湊尺寸而聞名,具有快速響應時間且設計簡單且具有成本效益。它們重量輕,非常適合要求最高效率和最小重量的應用,為需要高功率密度和可靠性能的系統提供完美的平衡。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 458億美元 |

| 預測值 | 1482億美元 |

| 複合年成長率 | 12.6% |

依平台細分,市場包括衛星、太空艙、行星際探測器、探測車和運載火箭。其中,行星際飛船和探測器將經歷最快的成長,到 2034 年複合年成長率將達到驚人的 14.6%。高可靠性 DC-DC 轉換器在為科學儀器、通訊系統和推進技術供電方面發揮著至關重要的作用,確保在最苛刻的條件下完成任務。

北美預計航太主導全球太空 DC-DC 轉換器市場,預計到 2034 年該地區的市場規模將達到 6,150 萬美元。北美完善的研發基礎設施推動著持續創新,而先進的製造能力和優質材料的取得確保了生產符合太空任務嚴格要求的耐用、可靠的電力系統。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 太空高效率電源管理需求日益成長

- 衛星技術的進步和小型化要求

- 太空探索和衛星部署的投資不斷增加

- 開發可靠、高效、耐輻射的組件

- 擴大太空太陽能發電系統的使用

- 產業陷阱與挑戰

- 太空系統的開發和生產成本高昂

- 確保極端條件下的可靠性的技術挑戰

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 非隔離

- 孤立

第6章:市場估計與預測:按輸出功率,2021-2034 年

- 主要趨勢

- <10瓦

- 10-29瓦

- 30-99瓦

- 100-250瓦

- 251-500瓦

- 501-1000瓦

- >1000瓦

第 7 章:市場估計與預測:依外形尺寸,2021 年至 2034 年

- 主要趨勢

- 底盤安裝

- 封閉式

- 磚

- 離散的

第 8 章:市場估計與預測:按平台,2021-2034 年

- 主要趨勢

- 衛星

- 小型衛星(< 500 公斤)

- 中型衛星(501-1000 公斤)

- 大型衛星(> 1000 公斤)

- 膠囊/貨物

- 行星際太空船和探測器

- 探測車/太空船著陸器

- 運載火箭

第 9 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 高度和軌道控制系統

- 地面機動和導航系統

- 命令和資料處理系統

- 環境監測系統

- 衛星熱電箱

- 電力子系統

- 其他

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Advanced Energy Industries Inc.

- Airbus Group SE

- Astronics Corporation

- Crane Co.

- EPC Space

- Infineon Technologies AG

- Microsemi Corporation

- Modular Devices Inc.

- Renesas Electronics Corporation

- STMicroelectronics

- SynQor Inc.

- Texas Instruments Incorporated

- Thales Group

- Vicor Corporation

- VPT

The Global Space DC-DC Converter Market reached USD 45.8 billion in 2024 and is projected to grow at a robust CAGR of 12.6% between 2025 and 2034. This remarkable growth is fueled by the increasing demand for efficient power management systems, driven by the rising complexity and frequency of space missions. Expanding deployments of small satellites and breakthroughs in interplanetary exploration are further propelling the need for reliable energy conversion, distribution, and storage solutions. These cutting-edge technologies not only optimize performance but also extend mission lifespans and reduce operational costs, making them indispensable to the future of space exploration.

The market is categorized by type into non-isolated and isolated converters, with the non-isolated segment emerging as the clear leader in 2024, holding 64.6% of the market share. Known for their high efficiency and compact size, non-isolated converters deliver fast response times and are designed for simplicity and cost-effectiveness. Their lightweight nature makes them ideal for applications demanding maximum efficiency and minimal weight, offering a perfect balance for systems requiring high power density and reliable performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.8 Billion |

| Forecast Value | $148.2 Billion |

| CAGR | 12.6% |

When segmented by platform, the market includes satellites, capsules, interplanetary probes, rovers, and launch vehicles. Among these, interplanetary spacecraft and probes are set to experience the fastest growth, with an impressive CAGR of 14.6% through 2034. These platforms require robust and resilient power systems capable of enduring extreme environmental conditions while delivering reliable energy distribution for mission-critical operations. High-reliability DC-DC converters play an essential role in powering scientific instruments, communication systems, and propulsion technologies, ensuring mission success in the most demanding conditions.

North America is poised to dominate the global space DC-DC converter market, with the region projected to reach USD 61.5 million by 2034. This leadership is fueled by significant investments in aerospace, defense, and space exploration. North America's well-established research and development infrastructure drives continuous innovation, while advanced manufacturing capabilities and access to premium-quality materials ensure the production of durable and dependable power systems tailored to the rigorous demands of space missions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for efficient power management in space

- 3.6.1.2 Advancements in satellite technology and miniaturization requirements

- 3.6.1.3 Rising investments in space exploration and satellite deployments

- 3.6.1.4 Development of reliable, high-efficiency, radiation-tolerant components

- 3.6.1.5 Expanding use of space-based solar power generation systems

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of development and production for space systems

- 3.6.2.2 Technical challenges in ensuring reliability under extreme conditions

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Non-isolated

- 5.3 Isolated

Chapter 6 Market Estimates & Forecast, By Output Power, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 <10W

- 6.3 10-29W

- 6.4 30-99W

- 6.5 100-250W

- 6.6 251-500W

- 6.7 501-1000W

- 6.8 >1000W

Chapter 7 Market Estimates & Forecast, By Form Factor, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Chassis mount

- 7.3 Enclosed

- 7.4 Brick

- 7.5 Discrete

Chapter 8 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Satellites

- 8.2.1 Small satellites (< 500 Kg)

- 8.2.2 Medium satellites (501-1000 Kg)

- 8.2.3 Large satellites (> 1000 Kg)

- 8.3 Capsules/Cargos

- 8.4 Interplanetary spacecraft & probes

- 8.5 Rovers/Spacecraft landers

- 8.6 Launch vehicles

Chapter 9 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Altitude & orbital control systems

- 9.3 Surface mobility and navigation systems

- 9.4 Command & data handling systems

- 9.5 Environmental monitoring systems

- 9.6 Satellite thermal power box

- 9.7 Electric power subsystems

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Advanced Energy Industries Inc.

- 11.2 Airbus Group SE

- 11.3 Astronics Corporation

- 11.4 Crane Co.

- 11.5 EPC Space

- 11.6 Infineon Technologies AG

- 11.7 Microsemi Corporation

- 11.8 Modular Devices Inc.

- 11.9 Renesas Electronics Corporation

- 11.10 STMicroelectronics

- 11.11 SynQor Inc.

- 11.12 Texas Instruments Incorporated

- 11.13 Thales Group

- 11.14 Vicor Corporation

- 11.15 VPT

全球直流-直流轉換器市場,依拓樸結構、架構、最終用途、輸出功率範圍、輸入電壓範圍、安裝類型和開關頻率分類-2025-2032年預測空間直流-直流轉換器市場按產品類型、轉換器類型、元件、輸入電壓範圍、輸出功率容量、平台、外形規格、最終用戶產業和應用分類-2025-2032年預測飛機直流-直流轉換器市場:按應用、最終用途、類型、功率等級、結構和分銷管道分類 - 全球預測 2025-2032

全球直流-直流轉換器市場,依拓樸結構、架構、最終用途、輸出功率範圍、輸入電壓範圍、安裝類型和開關頻率分類-2025-2032年預測空間直流-直流轉換器市場按產品類型、轉換器類型、元件、輸入電壓範圍、輸出功率容量、平台、外形規格、最終用戶產業和應用分類-2025-2032年預測飛機直流-直流轉換器市場:按應用、最終用途、類型、功率等級、結構和分銷管道分類 - 全球預測 2025-2032 2025年DC-DC轉換器全球市場報告

2025年DC-DC轉換器全球市場報告 全球 DC-DC 轉換器 IC 市場:未來預測(至 2032 年)- 按產品類型、輸入電壓、輸出電壓、輸出數量、安裝類型、應用、最終用戶和地區進行分析

全球 DC-DC 轉換器 IC 市場:未來預測(至 2032 年)- 按產品類型、輸入電壓、輸出電壓、輸出數量、安裝類型、應用、最終用戶和地區進行分析 全球航太DC-DC轉換器市場全球低壓與中壓直流系統市場

全球航太DC-DC轉換器市場全球低壓與中壓直流系統市場 全球隔離式 DC-DC 轉換器市場規模(按類型、輸入電壓、輸出電壓、最終用戶、區域範圍和預測)2032 年 DC-DC 轉換器市場預測:按產品、輸入電壓、輸出電壓、輸出功率、外形規格、應用和地區進行的全球分析

全球隔離式 DC-DC 轉換器市場規模(按類型、輸入電壓、輸出電壓、最終用戶、區域範圍和預測)2032 年 DC-DC 轉換器市場預測:按產品、輸入電壓、輸出電壓、輸出功率、外形規格、應用和地區進行的全球分析 2025 年至 2033 年 DC-DC 轉換器市場報告(按安裝方式、輸入電壓、輸出電壓、應用和地區分類)

2025 年至 2033 年 DC-DC 轉換器市場報告(按安裝方式、輸入電壓、輸出電壓、應用和地區分類)