|

市場調查報告書

商品編碼

1665047

電動車 EMC 電池濾波器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測EV EMC Battery Filter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

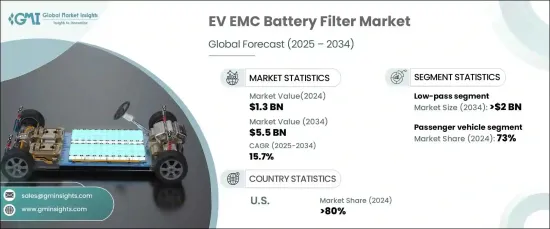

2024 年全球電動車 EMC 電池濾波器市場價值為 13 億美元,預計在 2025 年至 2034 年期間經歷顯著成長,複合年成長率為 15.7%。隨著對電動車的需求不斷成長,對先進的電磁相容性 (EMC) 電池濾波器解決方案的需求也大幅增加。

安全問題和嚴格的汽車監管標準進一步推動了市場的發展。電動車中先進電子元件的整合度不斷提高,因此符合 EMC 要求至關重要,以確保系統免受電磁干擾 (EMI)。國際電工委員會 (IEC) 和 ISO 等監管機構已經制定了嚴格的性能標準,以提高電動車系統的安全性和可靠性。這些監管要求正在推動 EMC 電池濾波器領域的創新和採用,從而促進強勁的市場前景。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 55億美元 |

| 複合年成長率 | 15.7% |

市場按濾波器類型細分,包括低通、高通、帶通和帶阻濾波器。 2024 年,低通濾波器佔據了 40% 的市場佔有率,預計到 2034 年將成長到 20 億美元。隨著電動車設計採用越來越複雜的電子設備(包括感測器、控制系統和通訊技術),對低通濾波器的需求持續上升。這些濾波器允許低頻訊號通過,同時阻止破壞性的高頻噪聲,從而提高系統性能和可靠性。

按車型分類,乘用車在 2024 年佔據市場主導地位,佔 73% 的佔有率。電動車在個人交通領域的快速普及是由於人們環保意識的增強和排放法規的嚴格。隨著消費者轉向電動車,對 EMC 電池濾波器的需求正在增加,以確保乘用車的最佳性能和安全性。

在美國,電動車 EMC 電池濾波器市場在 2024 年佔據了 80% 的區域佔有率。監管機構執行嚴格的排放和安全標準進一步推動了對先進 EMC 解決方案的需求,以確保電動車的合規性和無縫功能。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 原物料供應商

- 組件提供者

- 生產

- 經銷商

- 最終用戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞及舉措

- 監管格局

- 成本分析

- 衝擊力

- 成長動力

- 電動車需求不斷成長

- 嚴格的 EMC 監管標準

- 電動車電池技術的進步

- 更加重視電源效率與降噪

- 產業陷阱與挑戰

- 複雜的監理合規性

- 與現有電動車系統的整合挑戰

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按篩選條件,2021 - 2034 年

- 主要趨勢

- 低通

- 高通

- 帶通

- 帶阻

第 6 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 動力系統 EMC 濾波

- 電池管理系統

- 充電基礎設施

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車 (LCV)

- 重型商用車 (HCV)

第 8 章:市場估計與預測:按電池,2021 - 2034 年

- 主要趨勢

- 鉛酸電池

- 鋰離子電池

- 鎳氫電池

- 固態電池

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- AstrodyneTDI

- AVX

- Bourns

- Cooper

- Delta

- Eaton

- Epcos

- InTiCa

- KEMET

- Littelfuse

- MAHLE

- Molex

- Mouse

- Murata

- NXP

- STMicroelectronics

- TDK

- TE Connectivity

- Vishay

- Wurth Elektronik

The Global EV EMC Battery Filter Market, valued at USD 1.3 billion in 2024, is projected to experience remarkable growth with a CAGR of 15.7% from 2025 to 2034. This surge is driven by the rising adoption of electric vehicles (EVs) worldwide, supported by stricter environmental policies and government incentives designed to accelerate EV usage. As the demand for EVs continues to grow, the need for advanced electromagnetic compatibility (EMC) battery filter solutions is expanding significantly.

Safety concerns and stringent automotive regulatory standards are further propelling the market. The increasing integration of advanced electronic components in EVs makes compliance with EMC requirements essential to ensure systems remain protected from electromagnetic interference (EMI). Regulatory bodies like the International Electrotechnical Commission (IEC) and ISO have established rigorous performance standards to enhance the safety and reliability of EV systems. These regulatory demands are driving innovation and adoption in the EMC battery filter sector, fostering a robust market outlook.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 15.7% |

The market is segmented by filter type, including low-pass, high-pass, band-pass, and band-stop filters. In 2024, low-pass filters held a dominant 40% market share and are anticipated to grow to USD 2 billion by 2034. Low-pass filters are critical in mitigating high-frequency EMI, which can disrupt sensitive EV components such as battery management systems and powertrains. As EV designs incorporate increasingly sophisticated electronics-spanning sensors, control systems, and communication technologies-the demand for low-pass filters continues to rise. These filters improve system performance and reliability by letting low-frequency signals to pass through while blocking disruptive high-frequency noise.

By vehicle type, passenger vehicles led the market in 2024, capturing a commanding 73% share. The rapid adoption of EVs in personal transportation is driven by heightened environmental awareness and stringent emissions regulations. As consumers transition to electric mobility, the demand for EMC battery filters to ensure optimal performance and safety in passenger vehicles is increasing.

In the United States, the EV EMC battery filter market accounted for 80% of the regional share in 2024. This growth is attributed to robust government support for EV adoption, including tax credits, subsidies, and investments in EV infrastructure development. Regulatory agencies enforcing strict emissions and safety standards further boost the demand for advanced EMC solutions, ensuring compliance and seamless functionality in electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacture

- 3.1.4 Distributors

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing demand for electric vehicles

- 3.9.1.2 Stringent regulatory standards for EMC

- 3.9.1.3 Advancements in EV battery technology

- 3.9.1.4 Increased focus on power efficiency and noise reduction

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Complex regulatory compliance

- 3.9.2.2 Integration challenges with existing EV systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Filter, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Low-pass

- 5.3 High-pass

- 5.4 Band-pass

- 5.5 Band-stop

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Powertrain EMC filtering

- 6.3 Battery management system

- 6.4 Charging infrastructure

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicle

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light Commercial Vehicles (LCVs)

- 7.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lead acid battery

- 8.3 Lithium-ion battery

- 8.4 Nickel metal hydride battery

- 8.5 Solid-state battery

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AstrodyneTDI

- 10.2 AVX

- 10.3 Bourns

- 10.4 Cooper

- 10.5 Delta

- 10.6 Eaton

- 10.7 Epcos

- 10.8 InTiCa

- 10.9 KEMET

- 10.10 Littelfuse

- 10.11 MAHLE

- 10.12 Molex

- 10.13 Mouse

- 10.14 Murata

- 10.15 NXP

- 10.16 STMicroelectronics

- 10.17 TDK

- 10.18 TE Connectivity

- 10.19 Vishay

- 10.20 Wurth Elektronik

2026年全球電動車(EV)電池單體及電池組材料市場報告

2026年全球電動車(EV)電池單體及電池組材料市場報告 電動汽車電池市場:2026-2032年全球市場預測(按電池類型、充電容量、電池形狀、驅動系統、車輛類型和銷售管道)新能源汽車電池黏合劑市場:黏合劑類型、組件形式、應用階段、固化技術和銷售管道-全球預測,2026-2032年

電動汽車電池市場:2026-2032年全球市場預測(按電池類型、充電容量、電池形狀、驅動系統、車輛類型和銷售管道)新能源汽車電池黏合劑市場:黏合劑類型、組件形式、應用階段、固化技術和銷售管道-全球預測,2026-2032年 全球電動車電池市場:策略性洞察與預測(2026-2031)

全球電動車電池市場:策略性洞察與預測(2026-2031) 全球和中國電動汽車電池和材料:技術、趨勢和市場預測

全球和中國電動汽車電池和材料:技術、趨勢和市場預測 電動車 (EV) 用 EMC 電池濾波器市場規模、佔有率和成長分析:按濾波器類型、電池類型、電壓額定值、電流額定值、車輛類型、應用和地區分類—產業預測 (2026-2033)電動汽車電池市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區洞察,2026-2034年的預測

電動車 (EV) 用 EMC 電池濾波器市場規模、佔有率和成長分析:按濾波器類型、電池類型、電壓額定值、電流額定值、車輛類型、應用和地區分類—產業預測 (2026-2033)電動汽車電池市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區洞察,2026-2034年的預測 日本電動車電池市場規模、佔有率、趨勢及預測(按電池類型、驅動系統、車輛類型和地區分類,2026-2034年)2026年全球電動汽車電池市場報告

日本電動車電池市場規模、佔有率、趨勢及預測(按電池類型、驅動系統、車輛類型和地區分類,2026-2034年)2026年全球電動汽車電池市場報告 電動車電池市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按車輛類型、動力方式、電池類型、電池容量、需求類別、地區和競爭格局分類,2021-2031年)

電動車電池市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按車輛類型、動力方式、電池類型、電池容量、需求類別、地區和競爭格局分類,2021-2031年)