|

市場調查報告書

商品編碼

2027686

全球國防慣性測量設備市場Global Defense Inertial Measurement Unit Market |

||||||

全球國防慣性測量單元(IMU)

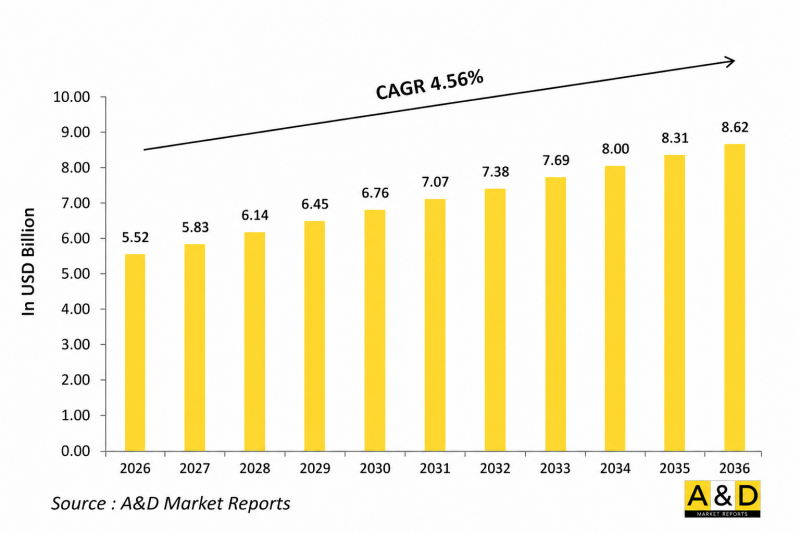

2026 年全球國防慣性測量設備 (IMU) 市場規模估計為 55.2 億美元,預計在 2026 年至 2036 年的預測期內將以 4.56% 的複合年成長率成長,到 2036 年達到 86.2 億美元。

1. 引言

慣性測量單元(IMU)在全球國防市場中扮演著至關重要的角色,是現代軍事導航、導引和穩定系統的基礎。 IMU 結合了加速計、陀螺儀,有時還包含磁力計,能夠獨立於外部訊號測量運動、姿態和速度。在 GPS 訊號不可用或通訊受到干擾的環境中,這些系統至關重要,因此對於飛彈、無人系統、飛機、艦艇和裝甲車輛等國防平台而言必不可少。

隨著精確性、自主性和生存能力在軍事行動中日益重要,慣性測量單元(IMU)正成為導航和目標捕獲解決方案的基礎。 IMU 能夠提供連續的位置信息,即使在電子戰環境下也能確保作戰可靠性。此外,IMU 與下一代作戰系統(包括高超音速武器和自主平台)的整合正在對市場產生影響。

全球地緣政治緊張局勢加劇以及各國軍隊的現代化計畫持續推動對高性能慣性系統的需求。推動國內生產和建立安全供應鏈的努力,進一步塑造了該市場的競爭格局。

2. 技術對國防慣性測量單元市場的影響

技術進步,特別是感測器技術的演進和小型化,大大改變了國防慣性測量單元(IMU)市場。微機電系統(MEMS)的發展使得製造緊湊、輕巧且經濟高效的IMU成為可能,同時也能保持高精度和高可靠性。這些進步支持將IMU整合到各種國防平台,從小型無人機到大型戰略系統。

光纖和環形雷射陀螺儀技術進一步提高了精度和穩定性,尤其是在需要抗電磁干擾和惡劣工作條件的高階軍事應用中。

感測器融合技術將慣性測量單元(IMU)與衛星導航系統和其他感測器結合,提高了導航精度和冗餘度。這在GPS訊號受干擾或被阻擋的環境中尤其重要。此外,人工智慧和嵌入式處理技術的進步使IMU能夠支援即時決策和自主運作。

在小型化、輕量化和低耗電量的同時提升效能的努力持續推動著創新。這些技術進步正在擴大其在更廣泛的軍事應用領域的部署,並提高防禦系統的整體效能。

3. 國防慣性測量單元市場的主要促進因素

國防慣性測量單元(IMU)市場的主要驅動力是衝突地區和GPS訊號無法涵蓋的環境中對可靠導航系統日益成長的需求。在現代戰爭中,干擾衛星導航的電子戰能力變得越來越重要,這使得慣性系統作為獨立的導航解決方案變得至關重要。

另一個主要驅動力是自主軍事系統的快速發展,包括無人機、地面機器人和海上平台。這些系統高度依賴慣性測量單元(IMU)進行導航、穩定和運動追蹤,從而確保在無需外部輸入的情況下持續作戰。

此外,精確導引飛彈部署的擴大推動了對高性能慣性感測器的需求。精確的目標捕獲和彈道控制需要精密的慣性測量單元(IMU),即使在惡劣條件下也能保持精度。此外,武器、監視系統和通訊設備對平台穩定性的要求也進一步推動了IMU的應用。

全球國防現代化計畫也是關鍵因素,各國政府都在投資升級老舊系統並研發下一代平台。重視國內生產和確保供應鏈安全也是推動國內慣性測量單元(IMU)發展的重要因素。

此外,感測器技術的進步和研發投入的增加提高了系統性能,使慣性測量單元更容易獲得,並能應用於更廣泛的軍事領域。

4. 國防慣性測量單元市場的區域趨勢

國防慣性測量單元(IMU)市場的區域趨勢與國防費用、技術能力和戰略重點密切相關。北美憑藉其強大的航太和國防生態系統、完善的研發基礎設施以及對先進軍事技術的持續投入,仍然是該市場的主導區域。

歐洲正著力研發高性能慣性技術,尤其是在航太和飛彈系統領域,這通常由涉及多個國家的聯合防禦項目所推動。精密工程和先進陀螺儀技術的創新在該地區備受重視。

亞太地區正經歷快速成長,這主要得益於國防預算的增加和國內製造業能力的提升。中國、印度、日本和韓國等國正大力投資發展完善的慣性導航系統,以減少對進口的依賴。

以色列已累積了豐富的專業技術,尤其是在用於精確導引飛彈和小型防禦系統的戰術慣性測量單元(IMU)方面。而俄羅斯則在維持其傳統慣性技術優勢的同時,正向現代固體系統轉型。

對先進慣性技術的出口限制進一步促進了區域自主性,並塑造了全球國防工業中植根於區域的創新和生產策略。

本報告檢視了全球國防應用慣性測量單元 (IMU) 市場,概述了市場背景、市場影響因素分析、市場規模趨勢和預測,並按各個細分市場和地區進行了詳細分析。

目錄

國防慣性測量單元(IMU)市場:目錄

報告定義

市場區隔

按平台

按地區

最終用戶

未來十年市場展望

市場成長、發展趨勢、技術應用概述和市場吸引力等方面的詳細資訊。

市場技術

預計將對市場產生影響的十大技術及其對整體市場的潛在影響。

全球市場預測

上述所有細分市場的未來十年市場預測均已詳細涵蓋。

區域市場趨勢和預測

本報告涵蓋市場趨勢、促進因素、阻礙因素、挑戰以及政治、經濟、社會和技術等因素。報告還包括詳細的區域市場預測和情境分析。區域分析最後對主要企業、供應商和公司基準進行了概述。目前市場規模是基於典型情境估算的。

北美洲

促進因素、限制因素與挑戰

PEST分析

市場預測與情境分析

主要企業

供應商層級狀態

企業標竿管理

歐洲

中東

亞太地區

南美洲

國別分析

我們

國防計劃

最新消息

專利

該市場目前的技術成熟度水平

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

機會矩陣

專家意見

結論

關於航空航太和國防市場報告

Global Defense Inertial Measurement Unit Market

The Global Defense Inertial Measurement Unit Market is estimated at USD 5.52 billion in 2026, projected to grow to USD 8.62 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.56% over the forecast period 2026-2036.

1. Introduction

The Global Defense Inertial Measurement Unit Market plays a foundational role in modern military navigation, guidance, and stabilization systems. Inertial Measurement Units, commonly known as IMUs, combine accelerometers, gyroscopes, and sometimes magnetometers to determine motion, orientation, and velocity without relying on external signals. These systems are critical in GPS-denied or contested environments, making them indispensable for defense platforms such as missiles, unmanned systems, aircraft, naval vessels, and armored vehicles.

As military operations increasingly emphasize precision, autonomy, and survivability, IMUs serve as the backbone of navigation and targeting solutions. Their ability to provide continuous positional awareness ensures operational reliability even under electronic warfare conditions. The market is also influenced by the integration of IMUs into next-generation combat systems, including hypersonic weapons and autonomous platforms.

Growing geopolitical tensions and modernization programs across global armed forces continue to drive demand for high-performance inertial systems. The push toward indigenous manufacturing and secure supply chains further shapes the competitive landscape of this market.

2. Technology Impact in Defense Inertial Measurement Unit Market

Technological advancements have significantly transformed the Defense Inertial Measurement Unit Market, particularly through the evolution of sensor technologies and miniaturization. The development of micro-electromechanical systems has enabled compact, lightweight, and cost-effective IMUs while maintaining high levels of accuracy and reliability. These advancements support integration into a wide range of defense platforms, from small unmanned aerial vehicles to large strategic systems.

Fiber optic and ring laser gyroscope technologies have further enhanced precision and stability, especially in high-end military applications requiring resistance to electromagnetic interference and extreme operational conditions.

Sensor fusion, combining IMUs with satellite navigation and other sensors, has improved navigation accuracy and redundancy. This is particularly critical in environments where GPS signals are disrupted or denied. Additionally, advancements in artificial intelligence and embedded processing allow IMUs to support real-time decision-making and autonomous operations.

The focus on reducing size, weight, and power consumption while enhancing performance continues to drive innovation. These technological improvements are enabling broader deployment across diverse military applications and enhancing the overall effectiveness of defense systems.

3. Key Drivers in Defense Inertial Measurement Unit Market

The Defense Inertial Measurement Unit Market is primarily driven by the increasing demand for reliable navigation systems in contested and GPS-denied environments. Modern warfare increasingly involves electronic warfare capabilities that can disrupt satellite-based navigation, making inertial systems essential as independent navigation solutions.

Another major driver is the rapid expansion of autonomous military systems, including unmanned aerial vehicles, ground robots, and maritime platforms. These systems rely heavily on IMUs for navigation, stabilization, and motion tracking, ensuring operational continuity without external inputs.

The growing deployment of precision-guided munitions also fuels demand for high-performance inertial sensors. Accurate targeting and trajectory control require advanced IMUs capable of maintaining precision under extreme conditions. Additionally, platform stabilization requirements for weapons, surveillance systems, and communication equipment further boost adoption.

Defense modernization programs worldwide are another significant factor, as governments invest in upgrading legacy systems and developing next-generation platforms. The emphasis on indigenous production and secure supply chains also encourages domestic IMU development.

Finally, advancements in sensor technology and increasing investments in research and development are enhancing system capabilities, making IMUs more accessible and versatile across a wider range of military applications.

4. Regional Trends in Defense Inertial Measurement Unit Market

Regional dynamics in the Defense Inertial Measurement Unit Market are closely linked to defense spending, technological capabilities, and strategic priorities. North America remains a dominant region due to its strong aerospace and defense ecosystem, extensive research infrastructure, and continuous investment in advanced military technologies.

Europe focuses on high-performance inertial technologies, particularly in aerospace and missile systems, often driven by collaborative defense programs among multiple countries. The region emphasizes precision engineering and innovation in advanced gyroscope technologies.

The Asia-Pacific region is witnessing rapid growth, fueled by increasing defense budgets and the expansion of indigenous manufacturing capabilities. Countries such as China, India, Japan, and South Korea are investing heavily in developing complete inertial navigation ecosystems to reduce reliance on imports.

Israel has developed specialized expertise in tactical-grade IMUs, particularly for precision-guided munitions and compact defense systems. Meanwhile, Russia continues to maintain strengths in traditional inertial technologies while transitioning toward modern solid-state systems.

Export restrictions on advanced inertial technologies have further encouraged regional self-reliance, shaping localized innovation and production strategies across the global defense landscape.

5. Key Defense Inertial Measurement Unit Market Program

A notable program shaping the Defense Inertial Measurement Unit Market involves a strategic collaboration between Paras Defence and Space Technologies and an Israeli inertial solutions provider. This initiative focuses on the co-development and production of advanced IMUs, including fiber optic gyro-based systems and integrated navigation solutions.

The program is designed to support multiple defense platforms, including unmanned systems, missiles, and armored vehicles, enhancing navigation accuracy in complex operational environments. It emphasizes technology transfer and domestic manufacturing, aligning with national self-reliance initiatives and reducing dependence on foreign suppliers.

Such collaborations are becoming increasingly common as countries seek to strengthen their defense industrial base and secure critical technologies. The program also highlights the growing importance of partnerships between domestic firms and international technology providers in accelerating innovation and deployment.

By focusing on localization and advanced system integration, this initiative represents a broader trend in the market toward building resilient and self-sufficient defense supply chains.

Table of Contents

Defense Inertial Measurement Unit Market - Table of Contents

Market Definition

Market Segmentation

By Platform

By Region

By End - User

10 Year Market Outlook

The 10-year market outlook would give a detailed overview of changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Market Forecast

The 10-year market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Market Trends & Forecast

The regional market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions

Hear from our experts their opinion of the possible outlook for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, Apac

- Table 12: Restraints, Impact Analysis, Apac

- Table 13: Challenges, Impact Analysis, Apac

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform2026-2036

- Table 19: Scenario Analysis, Scenario 1, By End User, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform2026-2036

- Table 22: Scenario Analysis, Scenario 2, By End User, 2026-2036

List of Figures

- Figure 1: Global Defense Inertial Measurement Unit Market Forecast, 2026-2036

- Figure 2: Global Defense Inertial Measurement Unit Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Inertial Measurement Unit Market Forecast, By Platform 2026-2036

- Figure 4: Global Defense Inertial Measurement Unit Market Forecast, By End User, 2026-2036

- Figure 5: North America, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 8: Apac, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Inertial Measurement Unit Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Inertial Measurement Unit Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Inertial Measurement Unit Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Inertial Measurement Unit Market , By Region (Cagr), 2026-2036

- Figure 50: Opportunity Analysis, Defense Inertial Measurement Unit Market , By Platform Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Inertial Measurement Unit Market , By Platform(Cagr), 2026-2036

- Figure 52: Opportunity Analysis, Defense Inertial Measurement Unit Market , By End User(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Inertial Measurement Unit Market , By End User(Cagr), 2026-2036

- Figure 54: Scenario Analysis, Defense Inertial Measurement Unit Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Inertial Measurement Unit Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Inertial Measurement Unit Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Inertial Measurement Unit Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense Inertial Measurement Unit Market , By Platform 2026-2036

- Figure 59: Scenario 1, Defense Inertial Measurement Unit Market , By End User, 2026-2036

- Figure 60: Scenario 2, Defense Inertial Measurement Unit Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Inertial Measurement Unit Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense Inertial Measurement Unit Market , By Platform 2026-2036

- Figure 63: Scenario 2, Defense Inertial Measurement Unit Market , By End User, 2026-2036

- Figure 64: Company Benchmark, Defense Inertial Measurement Unit Market , 2026-2036