|

市場調查報告書

商品編碼

2009455

全球國防飛機機翼結構市場(2026-2036 年)Global Defense Aircraft Wings Structure Market 2026-2036 |

||||||

全球國防飛機機翼結構市場

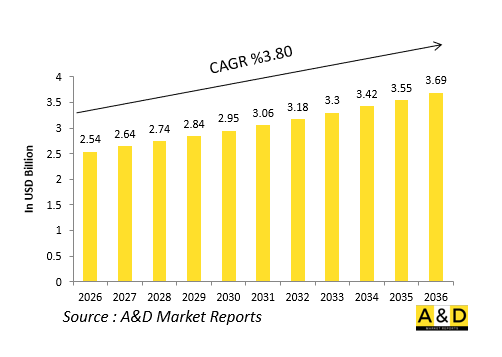

2026 年全球國防飛機機翼結構市場規模估計為 25.4 億美元,預計到 2036 年將達到 36.9 億美元,在 2026 年至 2036 年的預測期內,複合年成長率為 3.80%。

介紹

全球防務飛機機翼結構市場專注於高性能機翼的設計和製造,這些機翼對軍事航空至關重要。這些結構提供升力、機動性和穩定性,並透過整合主翼梁、蒙皮、翼肋和控制面,使其能夠承受氣動載荷、過載和武器後座力。碳複合材料、鈦合金等尖端材料以及變形技術的應用,使得機翼能夠採用更纖細的外形,從而實現隱身、更高的速度和更遠的航程。供應商涵蓋了從一級系統整合商到可變翼機構和航空母艦作業折疊式設計專家等各類企業。第五/六代戰鬥機、無人系統和旋翼飛機升級的採購需求,是推動市場發展的動力。對燃油效率、有效載荷多功能性和感測器整合的重視,正在推動創新。該領域是空中優勢策略的基礎,機翼正在發展成為多功能平台,在現代戰場上承載燃料箱、電子設備和共形天線。

科技對國防飛機機翼結構市場的影響

技術正在變革國防飛機機翼結構市場,提升性能和適應性。碳纖維複合材料具有卓越的剛性和抗疲勞性,能夠製造出更薄、更輕的機翼,在不犧牲強度的前提下增強機動性。利用智慧致動器和形狀記憶合金主動變形機翼表面,可以即時調整,從而在所有飛行狀態下實現最佳升力。積層製造技術能夠製造複雜的內部晶格結構,實現輕量化和快速原型製作。嵌入式光纖和壓電感測器能夠監測結構完整性,預測戰鬥應力引起的裂縫。混合翼設計整合了推進和隱身功能,同時最大限度地降低了阻力。基於計算流體力學的AI最佳化氣動分析能夠改進翼型,從而實現高超音速和超音速巡航能力。積層製造和固化製程的自動化實現了適合大規模生產的專案規模。這些突破性技術解決了顫振抑制和結冰等挑戰,將機翼轉變為動態系統,從而提高作戰效能和飛機使用壽命。

國防飛機機翼結構市場的關鍵促進因素

隨著威脅的演變,關鍵促進因素正在加速國防飛機機翼結構市場的發展。老舊機隊的現代化需要性能更優、升力更強的機翼,以承載更重的武器裝備並長途飛行。地緣政治衝突促使企業投資研發高機動性多用途平台,並採用可變後掠翼以適應多樣化的作戰任務。永續性目標推動了可回收複合材料的應用和空氣動力效率的提升,從而減少全生命週期排放。供應鏈的脆弱性促使企業轉向本地化生產和彈性材料採購。皇家僚機無人機的普及催生了對可整合到艦載機上的緊湊型折疊式機翼的需求。對低可視性的需求推動了雷達吸波結構和鋸齒狀邊緣的發展。數位化工程工具實現了虛擬測試,縮短了研發週期。國際夥伴關係促進了聯合研發,並在聯盟之間共用機翼技術。經濟因素凸顯了模組化設計的經濟性和擴充性。所有這些因素共同推動了市場的發展,該市場優先考慮在衝突地區實現生存能力、多功能性和快速部署的能力。

國防飛機機翼結構市場區域趨勢

國防飛機機翼結構市場的區域趨勢凸顯了戰略差異。北美在隱形戰鬥機和戰略轟炸機的自適應機翼和複合材料方面處於創新主導。歐洲則利用合資企業在可變後掠翼運輸機和歐洲戰鬥機改進方面取得進展,強調互通性。亞太地區則透過為區域巡邏機和艦載機開發高機動性機翼來增強自身能力。

本報告對全球國防飛機機翼結構市場進行了深入分析,提供了影響該市場的技術資訊、未來 10 年的預測以及各區域市場的趨勢。

目錄

國防飛機機翼結構市場報告定義

國防飛機機翼結構市場的細分

按地區

按平台

材料

按組件

按翅膀類型

透過技術

未來十年國防飛機機翼結構市場分析

國防飛機機翼結構技術市場

全球國防飛機機翼結構市場預測

國防飛機機翼結構區域市場趨勢與預測

北美洲

促進因素、阻礙因素、挑戰

害蟲

市場預測與情境分析

主要企業

供應商等級

企業標竿管理

歐洲

中東

亞太地區

南美洲

國防飛機機翼結構市場國別分析

我們

國防計劃

最新消息

專利

該市場目前的技術成熟度水平

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防飛機機翼結構市場機會矩陣

專家對國防飛機機翼結構市場報告的意見

結論

關於航空航太和國防市場報告

Global Defense Aircraft Wings Structure Market

The Global Defense Aircraft Wings Structure Market is estimated at USD 2.54 billion in 2026, projected to grow to USD 3.69 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.80% over the forecast period 2026-2036.

Introduction:

The global defense aircraft wings structure market focuses on the engineering and production of high-performance wings critical for military aviation. These structures provide lift, maneuverability, and stability, integrating spars, skins, ribs, and control surfaces to withstand aerodynamic loads, g-forces, and weapon recoil. Advanced materials like carbon composites, titanium alloys, and morphing technologies enable slimmer profiles for stealth, higher speeds, and extended ranges. Suppliers range from tier-one integrators to specialists in variable-sweep mechanisms and foldable designs for carrier operations. Market momentum arises from procurement of fifth- and sixth-generation fighters, unmanned systems, and rotary-wing upgrades. Emphasis on fuel efficiency, payload versatility, and sensor embedding drives innovation. This sector underpins air dominance strategies, with wings evolving into multifunctional platforms housing fuel tanks, electronics, and conformal antennas for modern battlefields.

Technology Impact in Defense Aircraft Wings Structure Market

Technologies are transforming the defense aircraft wings structure market, enhancing performance and adaptability. Carbon fiber composites deliver exceptional stiffness and fatigue resistance, enabling thinner, lighter wings that boost agility without sacrificing strength. Active morphing surfaces, using smart actuators and shape-memory alloys, allow real-time adjustments for optimal lift across flight regimes. Additive manufacturing fabricates intricate internal lattices, reducing weight and enabling rapid iteration. Embedded fiber optics and piezoelectric sensors enable structural health monitoring, predicting cracks from combat stresses. Blended-wing designs integrate propulsion and stealth features, minimizing drag. AI-optimized aerodynamics via computational fluid dynamics refine airfoil shapes for hypersonic and supercruise capabilities. Automation in layup and curing processes scales production for high-volume programs. These breakthroughs address challenges like flutter suppression and ice accretion, positioning wings as dynamic systems that elevate mission effectiveness and aircraft longevity.

Key Drivers in Defense Aircraft Wings Structure Market

Key drivers accelerate the defense aircraft wings structure market amid evolving threats. Modernization of legacy fleets demands upgraded wings with enhanced lift for heavier armaments and extended loiter times. Geostrategic rivalries fuel investments in agile, multirole platforms with variable geometry for diverse missions. Sustainability goals promote recyclable composites and aerodynamic efficiencies to lower lifecycle emissions. Supply chain vulnerabilities spur localized manufacturing and resilient materials sourcing. Proliferation of loyal wingman drones requires compact, foldable wings for mothership integration. Demands for low-observability drive radar-absorbent structures and serrated edges. Digital engineering tools enable virtual testing, compressing development cycles. International partnerships facilitate co-development, sharing wing tech across alliances. Economic factors emphasize affordable scalability through modular designs. Collectively, these propel a market prioritizing survivability, versatility, and rapid deployment in contested airspace.

Regional Trends in Defense Aircraft Wings Structure Market

Regional trends in the defense aircraft wings structure market highlight strategic divergences. North America spearheads innovation in adaptive wings and composites for stealth fighters and strategic bombers. Europe leverages joint ventures for swing-wing transports and eurofighter enhancements, stressing interoperability. Asia-Pacific ramps up indigenous capabilities, developing high-maneuverability wings for regional patrols and carrier-based jets. Middle Eastern nations focus on desert-hardened structures with anti-icing and dust-resistant coatings. In Africa and Latin America, trends favor rugged, cost-effective wings for counter-insurgency and maritime surveillance. Localization efforts build domestic supply chains, reducing foreign dependency. Export-oriented production adapts designs to client specifications, like tropical corrosion resistance. Collaborative R&D hubs emerge, fostering tech transfer. These patterns reflect tailored responses to local threats, budgets, and industrial maturity, shaping a fragmented yet interconnected global ecosystem.

Key Defense Aircraft Wings Structure Market Programs

Landmark programs anchor the defense aircraft wings structure market, pioneering next-era capabilities. Sixth-generation fighter efforts feature folding, adaptive wings with embedded weapons bays for air superiority. Loyal wingman initiatives deploy semi-autonomous drones with lightweight composite spars for teaming with manned jets. Rotary-wing upgrades incorporate rigid rotor blades evolving into advanced wing-like structures for tiltrotor versatility. Hypersonic demonstrator projects test heat-resistant wings using ceramic matrix composites. Multirole bomber refreshes integrate conformal fuel tanks within blended wings for global reach. Carrier aviation programs emphasize reinforced, folding mechanisms for compact storage and high-g launches. These efforts validate morphing tech, digital twins, and automated assembly. Industry teams collaborate on qualification testing for extreme loads. Success metrics include seamless integration with avionics and propulsion, redefining wings as intelligent, mission-reconfigurable components for networked warfare.

Table of Contents

Defense Aircraft Wings Structure Market - Table of Contents

Defense Aircraft Wings Structure Market Report Definition

Defense Aircraft Wings Structure Market Segmentation

By Region

By Platform

By By Material

By Component

By Wing Type

By Technology

Defense Aircraft Wings Structure Market Analysis for next 10 Years

The 10-year Defense Aircraft Wings Structure Market analysis would give a detailed overview of Defense Aircraft Wings Structure Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Aircraft Wings Structure Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Aircraft Wings Structure Market Forecast

The 10-year Defense Aircraft Wings Structure Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Aircraft Wings Structure Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Aircraft Wings Structure Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Aircraft Wings Structure Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Aircraft Wings Structure Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Material, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Material, 2026-2036

List of Figures

- Figure 1: Global Defense Aircraft Wings Structure Market Forecast, 2026-2036

- Figure 2: Global Defense Aircraft Wings Structure Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Aircraft Wings Structure Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Aircraft Wings Structure Market Forecast, By Material, 2026-2036

- Figure 5: North America, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 17: France, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 33: India, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 35: China, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Material(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Material(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Aircraft Wings Structure Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Aircraft Wings Structure Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Aircraft Wings Structure Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Aircraft Wings Structure Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Aircraft Wings Structure Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Aircraft Wings Structure Market, By Material, 2026-2036

- Figure 60: Scenario 2, Defense Aircraft Wings Structure Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Aircraft Wings Structure Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Aircraft Wings Structure Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Aircraft Wings Structure Market, By Material, 2026-2036

- Figure 64: Company Benchmark, Defense Aircraft Wings Structure Market, 2026-2036