|

市場調查報告書

商品編碼

2009454

全球國防飛機機身結構市場(2026-2036 年)Global Defense Aircraft Fuselage Structures Market 2026-2036 |

||||||

全球國防飛機機身結構市場

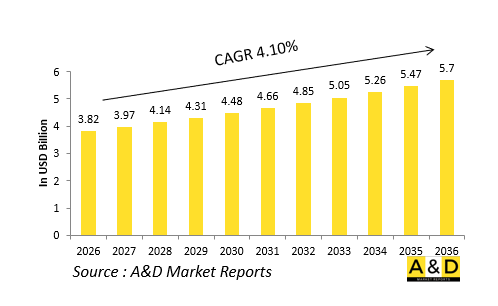

2026 年全球國防飛機機身結構市場規模估計為 38.2 億美元,預計到 2036 年將達到 57 億美元,在 2026 年至 2036 年的預測期內,複合年成長率為 4.10%。

介紹

國防飛機機身結構市場涵蓋軍用飛機所需的堅固機身的設計、製造和整合。這些結構構成飛機的核心骨架,支撐著機翼、引擎、航空電子設備和武器系統,同時承受高速機動、空戰和惡劣環境等極端運作負荷。複合材料、合金和混合層壓板等材料的進步使得更輕更強的設計成為可能,從而提高了燃油效率、有效載荷能力和隱身性能。主要企業包括領先的航太公司和專注於戰鬥機、轟炸機、運輸機和無人系統模組化機身的專業供應商。市場成長的驅動力來自日益加劇的地緣政治緊張局勢、現代化計劃以及對具有卓越生存能力的下一代平台的需求。積層製造和智慧感測器的創新進一步最佳化了生產和維護。該產業在國家國防戰略中繼續發揮關鍵作用,平衡世界各國軍隊對性能、成本和快速部署的需求。

技術對國防飛機機身結構市場的影響。

技術進步正對國防飛機機身結構市場產生重大影響,徹底革新材料科學和生產方法。碳纖維增強聚合物等複合材料具有卓越的強度重量比,在減輕結構重量的同時,還能提高耐腐蝕性和雷達吸波性能,這對隱身作戰至關重要。積層製造技術能夠實現複雜形狀的成型、快速原型製作和按需維修,從而大幅縮短前置作業時間並降低成本。數位雙胞胎和人工智慧驅動的模擬技術能夠整合健康監測系統,用於疲勞預測、載荷路徑最佳化和即時結構完整性評估。金屬與複合材料結合的混合結構兼具耐久性和柔軟性,使其成為高應力區域的理想選擇。包括機器人積層製造和雷射焊接在內的組裝流程自動化提高了精度和擴充性。這些創新解決了高超音速設計中的熱膨脹和戰鬥機防彈等挑戰。總而言之,這些技術增強了飛機的機動性、使用壽命和作戰能力,推動市場朝向永續且適應未來戰爭場景的機身結構發展。

國防飛機機身結構市場的主要促進因素

推動國防飛機機身結構市場發展的因素很多。地緣政治不穩定和日益嚴峻的全球威脅使得空軍現代化勢在必行,從而刺激了新型戰鬥機項目和升級改造對先進機身的需求。預算重新分配給高性能平台,優先考慮輕量化結構,以在不影響裝甲性能的前提下延長航程和續航時間。永續性要求採用可回收複合材料和高效製造程序,以符合環境法規。國內生產和戰略材料多樣化受到重視,以確保後疫情時代供應鏈的韌性。無人機系統(UAS)的日益普及需要能夠執行集群戰術和長途飛行作戰的緊湊型模組化機身。定向能量武器和感測器的整合需要更強大的安裝和電磁屏蔽能力。國際合作計畫促進了技術轉移並加速了創新。經濟壓力推動了透過數位化工程實現成本效益設計,而先進複合材料領域的勞動力技能提升也為市場成長提供了支持。這些因素正在推動一個充滿活力的市場,該市場優先考慮更高的殺傷力和生存能力。

國防飛機機身結構市場區域趨勢

國防飛機機身結構市場的區域趨勢反映了各國不同的戰略重點和產業能力。北美憑藉強大的研發生態系統佔據領先地位,在先進複合材料和下一代戰鬥機隱身技術領域佔據主導地位。歐洲強調合作,將永續材料融入運輸機和多用途飛機的多國合作計畫中。亞太地區正透過專注於成本優勢合金和快速生產的自主研發,實現快速成長,以確保區域空中優勢。

本報告對全球國防飛機機身結構市場進行了深入分析,提供了影響該市場的技術資訊、未來 10 年的預測以及各區域市場的趨勢。

目錄

全球國防飛機機身結構市場報告定義

全球國防飛機機身結構市場區隔

按地區

按平台

依結構類型

按組件

按飛機類型

未來十年全球國防飛機機身結構市場分析

全球國防飛機機身結構市場技術

全球國防飛機機身結構市場預測

國防飛機機身結構的區域及全球市場趨勢及預測。

北美洲

促進因素、阻礙因素、挑戰

害蟲

市場預測與情境分析

主要企業

供應商等級

企業標竿管理

歐洲

中東

亞太地區

南美洲

全球國防飛機機身結構市場國別分析

我們

國防計劃

最新消息

專利

該市場目前的技術成熟度水平

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

全球國防飛機機身結構市場機會矩陣

全球國防飛機機身結構市場報告的專家意見

結論

關於航空航太和國防市場報告

Global Defense Aircraft Fuselage Structures Market

The Global Defense Aircraft Fuselage Structures Market is estimated at USD 3.82 billion in 2026, projected to grow to USD 5.7 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.10% over the forecast period 2026-2036.

Introduction:

The defense aircraft fuselage structures market encompasses the design, manufacturing, and integration of robust airframes essential for military aircraft. These structures form the core skeleton, supporting wings, engines, avionics, and weapon systems while enduring extreme operational stresses like high-speed maneuvers, aerial combat, and harsh environments. Advancements in materials such as composites, alloys, and hybrid laminates drive lighter, stronger designs that enhance fuel efficiency, payload capacity, and stealth capabilities. Key players include major aerospace primes and specialized suppliers focusing on modular fuselages for fighter jets, bombers, transport aircraft, and unmanned systems. Market growth stems from rising geopolitical tensions, modernization programs, and demands for next-generation platforms with superior survivability. Innovations in additive manufacturing and smart sensors further optimize production and maintenance. This sector remains pivotal for national defense strategies, balancing performance, cost, and rapid deployment needs across global militaries.

Technology Impact in Defense Aircraft Fuselage Structures Market

Technological advancements profoundly shape the defense aircraft fuselage structures market, revolutionizing material science and production methods. Composite materials like carbon fiber-reinforced polymers offer superior strength-to-weight ratios, reducing structural mass while improving corrosion resistance and radar absorbency for stealth operations. Additive manufacturing enables complex geometries, rapid prototyping, and on-demand repairs, slashing lead times and costs. Digital twins and AI-driven simulations predict fatigue, optimize load paths, and integrate health monitoring systems for real-time structural integrity assessments. Hybrid metal-composite fusions combine durability with flexibility, ideal for high-stress zones. Automation in assembly, including robotic layup and laser welding, boosts precision and scalability. These innovations address challenges like thermal expansion in hypersonic designs and ballistic protection in combat fuselages. Overall, technology enhances aircraft agility, longevity, and mission readiness, propelling market evolution toward sustainable, adaptable airframes for future warfare scenarios.

Key Drivers in Defense Aircraft Fuselage Structures Market

Several critical drivers propel the defense aircraft fuselage structures market forward. Geopolitical instability and escalating global threats necessitate fleet modernizations, spurring demand for advanced fuselages in new fighter programs and upgrades. Budget reallocations toward high-performance platforms prioritize lightweight structures that extend range and endurance without compromising armor. Sustainability mandates push for recyclable composites and efficient manufacturing to meet environmental regulations. Supply chain resilience, post-disruptions, emphasizes domestic production and diversified sourcing for strategic materials. Rising unmanned aerial systems (UAS) adoption requires compact, modular fuselages for swarming tactics and long-endurance missions. Integration of directed-energy weapons and sensors demands reinforced mounts and electromagnetic shielding. Collaborative international programs foster technology transfers, accelerating innovation. Economic pressures drive cost-effective designs via digital engineering, while workforce upskilling in advanced composites sustains growth. These factors collectively fuel a dynamic market focused on superior lethality and survivability.

Regional Trends in Defense Aircraft Fuselage Structures Market

Regional dynamics in the defense aircraft fuselage structures market reflect diverse strategic priorities and industrial capabilities. North America leads with robust R&D ecosystems, dominating advanced composites and stealth technologies for next-gen fighters. Europe emphasizes collaborative frameworks, integrating sustainable materials across multinational programs for transport and multirole aircraft. Asia-Pacific surges through indigenous development, focusing on cost-competitive alloys and rapid production for regional air superiority. The Middle East invests heavily in upgrade kits and armored fuselages amid security concerns. Emerging markets in Latin America and Africa prioritize rugged, low-maintenance designs for patrol and training roles. Trends include technology localization to reduce import reliance, joint ventures for skill transfer, and adaptation to local climates like desert corrosion resistance. Supply chain shifts promote regional hubs, while export controls shape material flows. This landscape underscores a shift toward self-reliant, tailored solutions aligned with national defense postures.

Key Defense Aircraft Fuselage Structures Market Programs

Prominent programs define the defense aircraft fuselage structures market, showcasing cutting-edge engineering. Next-generation fighter initiatives feature all-composite airframes with integrated stealth shaping and sensor fusion for superior agility. Heavy bomber upgrades incorporate blast-resistant hybrids and modular sections for extended service life. Transport aircraft modernizations emphasize wide-body fuselages with reinforced cargo bays and rapid reconfigurable interiors. Unmanned combat aerial vehicles (UCAVs) pioneer lightweight, attritable designs using automated layup for swarm deployments. Hypersonic platform developments test thermal-protected structures blending ceramics and metals. Key collaborations involve fuselage sections for multirole jets, focusing on interoperability and quick-turn repairs. These programs drive material qualification, testing regimes, and supply chain innovations. Industry consortia advance digital threading from design to sustainment, ensuring scalability. Success hinges on balancing innovation with proven reliability, setting benchmarks for future military aviation structures.

Table of Contents

Global Defense Aircraft Fuselage Structures Market - Table of Contents

Global Defense Aircraft Fuselage Structures Market Report Definition

Global Defense Aircraft Fuselage Structures Market Segmentation

By Region

By Platform

By Structure Type

By Component

By Aircraft Type

Global Defense Aircraft Fuselage Structures Market Analysis for next 10 Years

The 10-year Global Defense Aircraft Fuselage Structures Market analysis would give a detailed overview of Global Defense Aircraft Fuselage Structures Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global Defense Aircraft Fuselage Structures Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Aircraft Fuselage Structures Market Forecast

The 10-year Global Defense Aircraft Fuselage Structures Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global Defense Aircraft Fuselage Structures Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global Defense Aircraft Fuselage Structures Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Defense Aircraft Fuselage Structures Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global Defense Aircraft Fuselage Structures Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Structure Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Structure Type, 2026-2036

List of Figures

- Figure 1: Global Defense Aircraft Fuselage Structures Market Forecast, 2026-2036

- Figure 2: Global Defense Aircraft Fuselage Structures Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Aircraft Fuselage Structures Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Aircraft Fuselage Structures Market Forecast, By Structure Type, 2026-2036

- Figure 5: North America, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 17: France, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 33: India, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 35: China, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Aircraft Fuselage Structures Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Aircraft Fuselage Structures Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Aircraft Fuselage Structures Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Aircraft Fuselage Structures Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Aircraft Fuselage Structures Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Aircraft Fuselage Structures Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Aircraft Fuselage Structures Market, By Structure Type(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Aircraft Fuselage Structures Market, By Structure Type(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Aircraft Fuselage Structures Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Aircraft Fuselage Structures Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Aircraft Fuselage Structures Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Aircraft Fuselage Structures Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Aircraft Fuselage Structures Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Aircraft Fuselage Structures Market, By Structure Type, 2026-2036

- Figure 60: Scenario 2, Defense Aircraft Fuselage Structures Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Aircraft Fuselage Structures Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Aircraft Fuselage Structures Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Aircraft Fuselage Structures Market, By Structure Type, 2026-2036

- Figure 64: Company Benchmark, Defense Aircraft Fuselage Structures Market, 2026-2036