|

市場調查報告書

商品編碼

1858534

洲際導彈的全球市場:2025年~2035年Global Intercontinental Ballistic Missiles Market 2025-2035 |

||||||

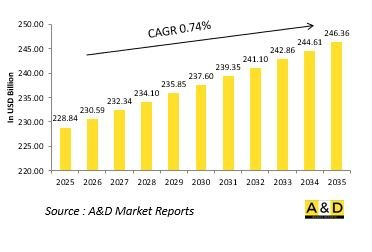

據估計,2025年全球洲際彈道飛彈市場規模為2,288.4億美元,預計到2035年將成長至2,463.6億美元,2025年至2035年的複合年增長率(CAGR)為0.74%。

洲際導彈市場簡介

洲際彈道飛彈(ICBM)市場是戰略威懾的核心,支撐著全球安全架構和主要大國之間的軍事平衡。洲際彈道飛彈是遠程運載系統,能夠攜帶常規彈頭或核彈頭,旨在確保在遭受侵略時進行可信的報復和威懾。其速度、射程和精準度是國家防禦戰略和核子三邊態勢的關鍵要素。該市場的特點是持續進行現代化改造,旨在提高可靠性、精度和應對新興飛彈防禦系統的生存能力。隨著各國致力於維持可信賴的威懾態勢,對先進推進、導引和再入飛行器技術的投資正在加速。移動發射平台和加固發射井的開發進一步增強了戰略戰備能力。總而言之,洲際彈道飛彈市場仍然是全球防禦戰略的基石,維持著力量投射和威懾之間的穩定平衡。

洲際導彈市場上技術的影響

技術進步顯著提升了洲際彈道飛彈的性能和效能。推進系統的改進,特別是固體燃料技術的改進,使得飛彈能夠更快地做好發射準備並延長使用壽命。改進的導引和導航系統,包括慣性導航、衛星修正和基於人工智慧的彈道優化,顯著提高了目標定位精度。再入飛行器技術的進步,包括多彈頭分導式再入飛行器(MIRV),使得單枚飛彈能夠同時攻擊多個目標。隱身塗層、誘餌和可控彈頭的引入,旨在突破先進的飛彈防禦系統。數位化指揮控制整合確保了戰略單位與防禦網路之間安全快速的通訊。此外,現代化專案擴大採用網路彈性架構來抵禦電子乾擾。總而言之,這些技術創新正在將洲際彈道飛彈轉變為更精確、生存能力更強、戰略靈活性更高的威懾系統。

洲際彈道飛彈市場的主要驅動因素

洲際彈道飛彈市場的主要驅動因素源自於不斷演變的安全威脅、戰略威懾需求以及現代化需求。地緣政治緊張局勢加劇以及對核威懾的重新重視,正促使主要國家加強和擴充其飛彈武庫。為了維持二次打擊能力,並確保對擁有類似戰略資產的對手構成可信的威懾,各國不斷推動技術進步。升級舊導彈系統以提高可靠性並對抗現代導彈防禦網路也是主要驅動因素。國防機構也優先發展移動式和隱蔽式發射平台,以增強生存能力和作戰靈活性。發射系統中數位技術和自動化的整合提高了戰備水平並減少了人為錯誤。總而言之,這些因素正在強化洲際彈道飛彈作為戰略防禦態勢和威懾框架重要組成部分的作用。

洲際彈道飛彈市場區域趨勢:

洲際彈道飛彈市場的區域發展反映了不同的戰略目標和國防理念。在北美,現代化計畫的重點是提高精度、確保通訊安全以及延長現有飛彈系統的使用壽命。歐洲的國防戰略仍然與基於聯盟的威懾框架緊密相連,強調與更廣泛的戰略防禦網絡相融合。在亞太地區,區域大國正日益發展或升級洲際彈道飛彈能力,以增強其戰略自主性並對抗競爭對手。在中東,人們對遠程導彈技術的興趣日益濃厚,但地緣政治和監管方面的限制限制了其發展。其他地區的新興國防工業正密切關注事態發展,並尋求潛在的合作和技術轉移機會。在所有地區,洲際彈道飛彈計畫繼續象徵著技術實力和戰略獨立性,增強了國家防禦能力和全球力量格局。

主要國防洲際彈道飛彈計畫:

美國核三位一體的陸基部分目前由400枚民兵III型洲際彈道飛彈組成,這些飛彈部署在蒙大拿州、北達科他州、懷俄明州、內布拉斯加州和科羅拉多州的地下發射井中,並由馬爾姆斯特羅姆空軍基地、邁諾特空軍基地和沃倫空軍基地負責操作。每枚飛彈攜帶一枚W87或W78型核彈頭,理論上可以攜帶兩枚或三枚。

美國空軍已將民兵III型飛彈的服役壽命延長至至少2030年,完成了一項耗資70億美元、歷時數十年的現代化改造計畫。升級後,空軍將改良後的飛彈描述為 "除了外殼之外,本質上是一個全新的系統" 。

目錄

洲際導彈市場- 目錄

洲際導彈市場報告定義

洲際導彈市場區隔

各地區

各推動因素

各範圍

洲際彈道飛彈市場技術展望

本部分討論了預計將影響該市場的十大技術,以及這些技術可能對整體市場產生的影響。

全球洲際彈道飛彈市場預測

以上各部分詳細涵蓋了該市場未來十年的洲際彈道飛彈市場預測。

全球洲際導彈市場預測

這個市場10年的洲際導彈市場預測,以上述的市場區隔全體被詳細內容填補。

各區域洲際彈道飛彈市場趨勢及預測

本部分涵蓋了各區域洲際彈道飛彈市場的趨勢、驅動因素、限制因素和挑戰,以及政治、經濟、社會和技術因素。此外,本部分也提供了詳細的區域市場預測和情境分析。區域分析最後包括主要公司概況、供應商格局和公司基準分析。目前市場規模是基於 "一切照舊" 情境估算的。

北美

促進因素,阻礙因素,課題

PEST

市場預測與情境分析

主要企業

供應商階層的形勢

企業基準

歐洲

中東

亞太地區

南美

洲際彈道飛彈市場國家分析

本章涵蓋該市場的主要國防項目以及最新的新聞和專利申請。此外,本章也提供未來十年各國的市場預測和情境分析。

美國

防衛計劃

最新消息

專利

這個市場上目前技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

洲際彈道飛彈市場機會矩陣

機會矩陣幫助讀者了解該市場中高機會細分領域。

專家對洲際彈道飛彈市場報告的意見

我們提供專家對該市場分析潛力的意見。

結論

關於航空·國防市場報告

The Global Intercontinental Ballistic Missiles market is estimated at USD 228.84 billion in 2025, projected to grow to USD 246.36 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 0.74% over the forecast period 2025-2035.

Introduction to Intercontinental Ballistic Missiles Market:

The defense Intercontinental Ballistic Missiles (ICBM) market represents the core of strategic deterrence capabilities, underpinning global security architectures and military balance among major powers. ICBMs are long-range delivery systems capable of carrying conventional or nuclear warheads, designed to ensure credible retaliation and deterrence in the event of aggression. Their speed, reach, and precision make them critical elements of national defense strategies and nuclear triads. The market is characterized by ongoing modernization efforts aimed at improving reliability, accuracy, and survivability against emerging missile defense systems. As nations focus on maintaining credible deterrent postures, investments in advanced propulsion, guidance, and reentry vehicle technologies are accelerating. The development of mobile launch platforms and hardened silos further strengthens strategic readiness. Overall, the ICBM market remains a cornerstone of global defense strategy, balancing power projection with deterrence stability.

Technology Impact in Intercontinental Ballistic Missiles Market:

Technological advancements have profoundly shaped the capabilities and effectiveness of intercontinental ballistic missiles. Improvements in propulsion systems, particularly solid-fuel technology, have enabled faster launch readiness and longer operational life. Enhanced guidance and navigation systems, integrating inertial navigation, satellite-based correction, and AI-assisted trajectory optimization, have greatly improved targeting precision. Developments in reentry vehicle technology, including multiple independently targetable reentry vehicles (MIRVs), allow a single missile to strike multiple targets simultaneously. Stealth coatings, decoys, and maneuverable warheads are being introduced to overcome advanced missile defense systems. Digital command and control integration ensures secure and rapid communication between strategic units and national defense networks. Furthermore, modernization programs increasingly incorporate cyber-resilient architectures to safeguard against electronic interference. Collectively, these innovations are transforming ICBMs into more accurate, survivable, and strategically flexible deterrent systems.

Key Drivers in Intercontinental Ballistic Missiles Market:

The key forces driving the ICBM market stem from evolving security threats, strategic deterrence needs, and modernization imperatives. Rising geopolitical tensions and renewed emphasis on nuclear deterrence have led major powers to enhance or expand their missile arsenals. The need to maintain second-strike capability and ensure credible deterrence against adversaries with comparable strategic assets fuels continuous technological advancement. Upgrading aging missile systems to enhance reliability and counter modern missile defense networks is another major driver. Defense organizations are also prioritizing mobile and concealed launch platforms to enhance survivability and operational flexibility. The integration of digital technologies and automation in launch systems improves readiness and reduces human error. Collectively, these factors are reinforcing the role of ICBMs as essential components of strategic defense postures and deterrence frameworks.

Regional Trends in Intercontinental Ballistic Missiles Market:

Regional developments in the ICBM market reflect distinct strategic ambitions and defense doctrines. In North America, modernization programs emphasize enhanced accuracy, secure communication, and life extension of existing missile systems. European defense strategies remain closely tied to alliance-based deterrence frameworks, focusing on integration with broader strategic defense networks. The Asia-Pacific region is witnessing increased activity as regional powers develop or upgrade their ICBM capabilities to bolster strategic autonomy and counterbalance rival nations. In the Middle East, interest in long-range missile technology is growing, though development remains limited due to geopolitical and regulatory constraints. Emerging defense industries in other regions are monitoring advancements for potential collaboration or technology transfer opportunities. Across all regions, ICBM programs continue to symbolize technological strength and strategic independence, reinforcing national defense and global power dynamics.

Key Defense Intercontinental Ballistic Missiles Program:

The land-based component of the U.S. nuclear triad currently consists of 400 deployed Minuteman III Intercontinental Ballistic Missiles (ICBMs) housed in underground silos located across Montana, North Dakota, Wyoming, Nebraska, and Colorado, and operated from the Malmstrom, Minot, and Warren Air Force Bases. Each missile is equipped with a single nuclear warhead - either the W87 or W78 - though in theory, each could accommodate two or three warheads.

The U.S. Air Force concluded a $7 billion modernization effort that spanned several decades, extending the operational life of the Minuteman III fleet through at least 2030. Following the upgrades, the Air Force described the renewed missiles as "essentially new systems, apart from the outer shell."

Table of Contents

Intercontinental Ballistic Missiles Market - Table of Contents

Intercontinental Ballistic Missiles Market Report Definition

Intercontinental Ballistic Missiles Market Segmentation

By Region

By Propulsion

By Range

Intercontinental Ballistic Missiles Market Analysis for next 10 Years

The 10-year Intercontinental Ballistic Missiles Market analysis would give a detailed overview of Intercontinental Ballistic Missiles Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Intercontinental Ballistic Missiles Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Intercontinental Ballistic Missiles Market Forecast

The 10-year Intercontinental Ballistic Missiles Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Intercontinental Ballistic Missiles Market Trends & Forecast

The regional Intercontinental Ballistic Missiles Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Intercontinental Ballistic Missiles Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Intercontinental Ballistic Missiles Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Intercontinental Ballistic Missiles Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Propulsion, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Range, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Propulsion, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Range, 2025-2035

List of Figures

- Figure 1: Global Intercontinental Ballistic Missiles Market Forecast, 2025-2035

- Figure 2: Global Intercontinental Ballistic Missiles Market Forecast, By Region, 2025-2035

- Figure 3: Global Intercontinental Ballistic Missiles Market Forecast, By Propulsion, 2025-2035

- Figure 4: Global Intercontinental Ballistic Missiles Market Forecast, By Range, 2025-2035

- Figure 5: North America, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 6: Europe, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 8: APAC, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 9: South America, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 10: United States, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 11: United States, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 12: Canada, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 14: Italy, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 16: France, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 17: France, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 18: Germany, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 24: Spain, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 30: Australia, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 32: India, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 33: India, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 34: China, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 35: China, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 40: Japan, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Intercontinental Ballistic Missiles Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Intercontinental Ballistic Missiles Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Intercontinental Ballistic Missiles Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Intercontinental Ballistic Missiles Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Intercontinental Ballistic Missiles Market, By Propulsion (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Intercontinental Ballistic Missiles Market, By Propulsion (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Intercontinental Ballistic Missiles Market, By Range (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Intercontinental Ballistic Missiles Market, By Range (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Intercontinental Ballistic Missiles Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Intercontinental Ballistic Missiles Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Intercontinental Ballistic Missiles Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Intercontinental Ballistic Missiles Market, By Region, 2025-2035

- Figure 58: Scenario 1, Intercontinental Ballistic Missiles Market, By Propulsion, 2025-2035

- Figure 59: Scenario 1, Intercontinental Ballistic Missiles Market, By Range, 2025-2035

- Figure 60: Scenario 2, Intercontinental Ballistic Missiles Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Intercontinental Ballistic Missiles Market, By Region, 2025-2035

- Figure 62: Scenario 2, Intercontinental Ballistic Missiles Market, By Propulsion, 2025-2035

- Figure 63: Scenario 2, Intercontinental Ballistic Missiles Market, By Range, 2025-2035

- Figure 64: Company Benchmark, Intercontinental Ballistic Missiles Market, 2025-2035