|

市場調查報告書

商品編碼

1706272

DevSecOps、OTA 和可觀察性:實現安全且可擴展的物聯網DevSecOps, OTA & Observability: Enabling Secure, Scalable IoT |

||||||

軟體 DevSecOps、部署、可觀察性和 OTA 解決方案正在不斷發展,以跟上物聯網設備和系統不斷變化的軟體開發和發布方法。隨著物聯網市場競爭的加劇,開發組織需要更快地將軟體從開發轉移到部署,這需要盡可能實現流程自動化,以縮短上市時間。此外,越來越多的標準和法規將設備安全和健康的責任轉移到製造商身上,推動了對能夠持續監控設備群並提供持續軟體維護和更新的強大商業解決方案的需求。

本報告研究了物聯網軟體 DevSecOps、部署、可觀察性和 OTA 解決方案市場,研究了市場規模趨勢、關鍵趨勢、新興市場、區域市場和主要供應商,並為嵌入式設備工程師和研究人員提供了精選見解。

您回答了哪些問題?

- 物聯網軟體 DevSecOps、部署、可觀察性和 OTA 解決方案市場規模?到 2029 年將成長多少?

- 哪些產業和地理市場成長最快?

- 主要合作夥伴關係、收購、標準化和監管對這個市場有何影響?

- 哪些市場適合廣泛採用 OTA 解決方案?

- 如何使用 AI 和 ML(機器學習)來實現軟體開發和部署的自動化?

- 哪些供應商在物聯網系統的軟體 DevSecOps、部署、可觀察性和 OTA 解決方案方面處於市場領先地位?

主要發現:

- 各行各業的設備製造商和營運商越來越多地選擇 OTA 作為部署增強功能和修補程式的主要方法,這一趨勢正在引起政府和標準機構加強監管和審查。

- 19.3% 的開發組織正在考慮使用容器技術作為向物聯網設備和嵌入式系統部署軟體和無線更新的一種手段。

- 軟體 DevSecOps、部署、可觀察性和 OTA 解決方案市場正在經歷越來越多的併購活動,主要參與者正在進行整合。這種工具和功能的融合極大地提高了整個平台的性能和功能。

- 歐洲網路彈性法案 (CRA) 等法規正在推動對物聯網系統的軟體 DevSecOps、部署、可觀察性和 OTA 解決方案的巨大需求。

目錄

本報告的內容

怎樣的問題能拿起?

應該讀本報告人是誰?

在本報告被刊登的組織

摘要整理

- 主要調查結果

簡介

- 有許多不同的實作方法

- 成功實施可建立強大的軟體開發生命週期

- 可觀察性

- 生命週期管理注意事項

全球市場概要

垂直市場

- 航太及防衛

- 汽車汽車

- CE產品

- 工業自動化

- 醫療設備

- 運輸

地區市場

- 南北美洲

- 歐洲·中東·非洲

- 亞太地區

最近的市場趨勢

- 人工智慧驅動的更新活動管理

- 成熟的方法簡化了流程

- 設備群的使用壽命越來越長

- 應用程式可擴展性:推動物聯網市場關注容器技術

- 收購、合作與市場轉型

- 組織

- 架構和框架

- 相關標準

- 鼓勵採用 OTA 的法規

競爭情形

- 主要供應商的洞察

- Aeris

- Balena

- CloudBees

- Elektrobit (Continental)

- Excelfore

- GitLab

- HARMAN

- JFrog

- Memfault

- Sibros

- Telit Cinterion

- Vector Informatik

- Wind River

終端用戶的洞察

- 遠端物聯網應用的採用持續成長

- 安全性問題推動 OTA 購買決策

- SDLC 集成

關於作者

Inside this Report

Software DevSecOps, deployment, observability, and over-the-air (OTA) solutions are evolving to keep pace with the changing methods of building and releasing software for IoT devices and systems. As competition in IoT markets intensifies, developer organizations must accelerate the transition of software from development to deployment, automating as many processes as possible to achieve rapid time-to-market. Rising standards and regulations have shifted the responsibility for device security and health to manufacturers, creating a demand for robust commercial solutions that continuously monitor device fleets and provide ongoing software maintenance and updates.

This report explores and sizes the IoT market for software DevSecOps, deployment, observability, and OTA solutions. It discusses trends, vertical and regional markets, leading vendors, and provides selected insights from VDC Research's survey of embedded device engineers and developers.

What Questions are Addressed?

- What is the size of the IoT market for software DevSecOps, deployment, observability, and OTA solutions and how fast will it grow through 2029?

- Which vertical and regional markets are growing the fastest?

- How are key partnerships, acquisitions, standards, and regulations shaping the market?

- Which markets are primed for widespread adoption of OTA solutions?

- How are Artificial Intelligence and Machine Learning used to automate software development and deployment?

- Which vendors are leading the software DevSecOps, deployment, observability, and OTA solutions for IoT systems market?

Who Should Read this Report?

- CEO or other C-level executives

- Corporate development and M&A teams

- Marketing executives

- Business development and sales leaders

- Product development and strategy leaders

- Channel management and channel strategy leaders

Organizations Listed in this Report:

|

|

|

Executive Summary

As DevSecOps methodologies and continuous integration/continuous delivery (CI/CD) practices mature, developers integrate faster feedback loops into the earlier stages of the software and device development lifecycle, improving time to market, product quality, and software deployment in IoT. This blending of development processes is evident in the commercial market for deployment and maintenance solutions, where platforms now combine software testing with deployment features, offering developers a unified solution for automation across the design, build, test, and deploy phases.

DevSecOps observability enables teams to continuously monitor, measure, and analyze the health, performance, and security of applications and infrastructure throughout the software development lifecycle. It includes a combination of metrics, logs, and traces to provide insights into the system's operational and security aspects, allowing teams to detect issues early and respond quickly. The secure wireless distribution of software updates supports the continuous delivery aspect of the CI/CD pipeline.

OTA updates, initially introduced for mobile phones, expanded into the consumer electronics and automotive sectors. Vendors help fuel the wider adoption of updates by integrating OTA solutions across diverse IoT industries, offering both specialized solutions for specific applications and versatile platforms designed to serve multiple IoT market segments. The combination of regulations mandating the updatability of connected devices and the growing adoption of CI/CD and DevSecOps practices within development organizations is increasing the demand for commercial solutions to replace in-house developed alternatives.

Key Findings

- Device manufacturers and operators across multiple industries are choosing OTA updates as their primary means to deliver enhanced features and rollout patches, a trend which is bringing increased scrutiny and regulations from governments and standardization bodies.

- 19.3% of developer organizations are looking toward container technology as an emerging method of deploying software and delivering OTA updates to IoT devices and embedded systems.

- Merger and acquisition activity in the software DevSecOps, deployment, observability, and OTA solutions market has led to increased consolidation among key players. This convergence of tool domains and functionalities has significantly enhanced platform capabilities.

- Regulations like the European Cyber Resilience Act (CRA) are significantly driving the demand for software DevSecOps, deployment, observability, and OTA solutions for IoT systems.

Security Concerns Driving OTA Purchasing Decision

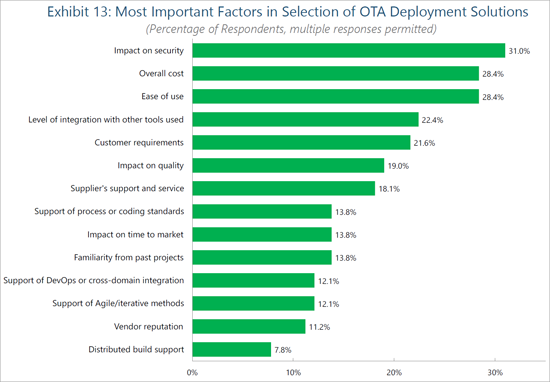

Tied with cost sensitivity, ease of use ranks as the second-most important factor influencing the selection of OTA deployment solutions [See Exhibit 13]. The deployment of OTA update campaigns is oftentimes a very manual task, requiring engineers to weigh multiple factors including rollout timing, device downtime, and potential versioning issues. This is one area where AI-driven OTA campaigns and the pairing of monitoring solutions can introduce increased ease of use to OTA solutions. By intelligently connecting update campaigns to real-time device status and analytics, device manufacturers/fleet managers can minimize the potentially costly consequences of failed update campaigns. Vendor reputation noticeably ranks amongst the lowest purchasing decision factors, suggesting a yet-to-be-determined competitive positioning of embedded OTA solution vendors. This consumer sentiment offers a considerate opportunity for new entrants seeking to deliver OTA capabilities to embedded markets. For those seeking to enter or increase their positioning within this segment of the IoT, focus should be dedicated towards enabling seamless yet confident deployment capabilities, bolstered by real-time capabilities and insights into campaign rollouts.

As with many areas of the IoT, the impact of integrating OTA solutions into toolchains and software stacks remains the topmost priority for development organizations. Failed software deployments can not only cause monetary and opportunity costs in the form of patches and downtime but also increase the attack surface for exploitation. Furthermore, an insecure OTA solution can enable threat actors to deploy malware alongside software packages to devices. Other opportunities for exploitation within the deployment process include hijacking and interrupting updates mid-deployment, leading to corrupted devices and systems. Partnerships with IoT security vendors (e.g., public key infrastructure (PKI) vendors) offer one avenue for OTA solution providers to bolster the security of their solutions (such as those between Excelfore/IIJ Global, Karma Automotive (Airbiquity)/QNX, and Telit Cinterion/Thales).

Table of Contents

Inside this Report

What Questions are Addressed?

Who Should Read this Report?

Organizations Listed in this Report

Executive Summary

- Key Findings

Introduction

- Deployment Approaches Vary

- Successful Deployment Establishes a Robust Software Development Life Cycle

- Observability

- Lifecycle Management Considerations

Global Market Overview

Vertical Markets

- Aerospace and Defense

- Automotive In-Vehicle

- Consumer Electronics

- Industrial Automation

- Medical Devices

- Transportation

Regional Markets

- The Americas

- Europe, the Middle East & Africa (EMEA)

- Asia-Pacific (APAC)

Recent Market Developments

- AI-driven Update Campaign Management

- Maturing Practices Streamline Processes

- Device Fleet Longevity Increasing

- Application Scalability Driving Interest in Containers Within the IoT Market

- Acquisitions, Partnerships and Market Pivots

- Karma Automotive Acquires Airbiquity to Bring OTA In-house

- Aurora Labs Pivots Away From OTA

- Excelfore Partners With Microsoft to Deploy AI-driven Update Campaigns

- Qualcomm Acquires Foundries.io

- JFrog Acquires Qwak AI

- Sibros Partners with Harbinger Motors and ZM Trucks to Deploy OTA to Medium-Duty Vehicles

- CloudBees Acquires Launchable

- Organizations

- Cloud Native Computing Foundation

- Continuous Delivery Foundation

- eSync Alliance

- Architectures & Frameworks

- AUTOSAR

- SOAFEE

- Eclipse Kanto

- Pantavisor Linux

- Uptane

- Relevant Standards

- Regulations Driving OTA Adoption

- AUTOMOTIVE

- MEDICAL DEVICES

- OTHER IOT

Competitive Landscape

- Selected Vendor Insights

- Aeris

- Balena

- CloudBees

- Elektrobit (Continental)

- Excelfore

- GitLab

- HARMAN

- JFrog

- Memfault

- Sibros

- Telit Cinterion

- Vector Informatik

- Wind River

End-User Insights

- Sustained Increases in Remote IoT Application Deployments

- Security Concerns Driving OTA Purchasing Decision

- Unifying the SDLC

About the Authors

List of Exhibits

- Exhibit 1: Worldwide Revenue for Software DevSecOps, Deployment, Observability, and OTA Solutions for IoT Systems

- Exhibit 2: Worldwide Revenue for Software DevSecOps, Deployment, Observability, and OTA Solutions for IoT Systems 2024 & 2029, Share by Vertical Market

- Exhibit 3: Worldwide Revenue for Software DevSecOps, Deployment, Observability, and OTA Solutions for IoT Systems 2024 & 2029, Share by Geographic Region

- Exhibit 4: Software Design Methodologies Used and Expected to Be Used

- Exhibit 5: Software DevSecOps, Deployment, Observability, and OTA Solutions for IoT Systems Forecast Scope

- Exhibit 6: Estimated Number of Years of Useful Life for Product Once Deployed, 2022 & 2024

- Exhibit 7: Factors Driving Organization to Adopt Container Technology in Current Project

- Exhibit 8: Worldwide Revenue for Software DevSecOps, Deployment, Observability, and OTA Solutions for IoT Systems, Share by Vendor

- Exhibit 9: Over-the-air (OTA) Software/Firmware Deployment Solutions Used on Current Project

- Exhibit 10: Most Important Factors in Selection of OTA Deployment Solutions, by Solution Source

- Exhibit 11: Current & Expected Use of Remote Application Deployment & Management

- Exhibit 12: Current Use of Remote Deployment & Management by Vertical Market

- Exhibit 13: Most Important Factors in Selection of OTA Deployment Solutions

- Exhibit 14: Most Important Factors in Selection of Release Management/Continuous Deployment Tools

DevSecOps 市場預測 2034 – 按組件、部署模式、組織規模、安全類型、開發階段、工具類型、最終用戶和地區分類的全球分析

DevSecOps 市場預測 2034 – 按組件、部署模式、組織規模、安全類型、開發階段、工具類型、最終用戶和地區分類的全球分析 軟體材料清單(SBOM)管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

軟體材料清單(SBOM)管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) DevSecOps 市場:按組件、部署、最終用途和區域分類

DevSecOps 市場:按組件、部署、最終用途和區域分類 2026年全球DevSecOps市場報告

2026年全球DevSecOps市場報告 全球DevSecOps市場:按組件、組織規模、服務、部署方法、最終用途、國家和地區分類-產業分析、市場規模、佔有率和未來預測(2025-2032)

全球DevSecOps市場:按組件、組織規模、服務、部署方法、最終用途、國家和地區分類-產業分析、市場規模、佔有率和未來預測(2025-2032) DevSecOps全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球DevSecOps市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

DevSecOps全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球DevSecOps市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) DevSecOps市場規模、佔有率和成長分析(按組件、服務、部署類型、組織規模、垂直產業和地區分類)-2026-2033年產業預測

DevSecOps市場規模、佔有率和成長分析(按組件、服務、部署類型、組織規模、垂直產業和地區分類)-2026-2033年產業預測 DevSecOps 市場 - 全球產業規模、佔有率、趨勢、機會和預測(按組件、按部署、按組織規模、按最終用途、按地區、按競爭)2020-2030F全球 DevSecOps 市場規模(按組件、部署、組織、最終用戶產業、區域範圍和預測)

DevSecOps 市場 - 全球產業規模、佔有率、趨勢、機會和預測(按組件、按部署、按組織規模、按最終用途、按地區、按競爭)2020-2030F全球 DevSecOps 市場規模(按組件、部署、組織、最終用戶產業、區域範圍和預測)