|

市場調查報告書

商品編碼

1950748

全球LED照明市場(2026年趨勢) - 資料庫及主要參與者策略2026 Global LED Lighting Market Trend- Database and Player Strategies |

||||||

根據TrendForce最新發布的報告《全球LED照明市場(2026年趨勢) - 資料庫及主要參與者策略(2026年上半年)》,全球LED照明市場預計將在2026年迎來關鍵轉折點,在宏觀經濟波動和需求調整的背景下,市場將從萎縮轉向穩定。隨著分銷通路庫存恢復到健康水準,預計年降幅將顯著收窄,整體需求預計將逐步恢復到以基本替換需求為主導的成長軌跡。更重要的是,競爭格局經歷結構性轉變,從價格競爭轉向以應用驅動的價值創造和系統整合能力為主導的競爭。

以下是2026年全球LED照明市場的五大策略考察:

1. 通用照明市場:工業和戶外領域是關鍵驅動因素

儘管2026年通用照明市場仍將處於調整階段,但某些細分市場展現出強勁的成長潛力。

預計工業照明將成為2026年的核心成長引擎,這得益於國防、航空航太、核電、液化天然氣(LNG)和戰略資源領域的投資。同時,人工智慧資料中心的加速建設推動了對專為液冷系統和伺服器機架設計的基礎設施照明的需求。在戶外領域,老舊基礎設施的更換和隧道照明標準的升級將繼續推動改造需求。此外,體育和娛樂場所的照明以及智慧節能解決方案推動市場顯著成長。

依地區劃分,歐洲仍是市場領導者,其次是北美和亞太地區。預計2025年至2030年,歐洲LED照明市場將以2.3%的年複合成長率成長。該成長主要得益於為遏制不斷上漲的能源成本而加速採用節能照明改造解決方案。亞太市場保持成長動力,其中東南亞預計在同一預測期內將以3.6%的年複合成長率成長。

2.智慧照明市場:從技術規格之爭轉向基於場景、以人為本的價值

根據TrendForce的分析,到2025年,全球照明產業將進入以 "情感照明" 和 "以人為本的照明(HCL)" 為中心的新階段。競爭焦點正從傳統的表現指標(例如發光效率和通訊協定)轉向以晝夜節律調節和體驗場景為核心的價值主張。

基於人工智慧的調光、全光譜控制和軟體定義照明(SDL)推動照明產品從靜態硬體設備轉變為能夠感知和自適應學習的智慧系統節點。根據 TrendForce 的資料,智慧照明市場預計到2030年將達到 217.85億美元,2025年至2030年的年複合成長率(CAGR)為 13.6%。預計大部分成長將來自人工智慧應用和系統升級帶來的價值提升,主要體現在三大應用場景:住宅照明、戶外照明和工業照明。

人工智慧、軟體定義照明和物聯網技術的融合將照明從基本的照明設備轉變為智慧生活環境、城市治理系統和工業數位化框架中的關鍵感知和互動節點。具備軟硬體整合能力、生態系統協作能力以及場景感知洞察力的供應商,將在未來智慧照明市場中獲得競爭優勢。

3.農業照明:區域差異化加劇,歐洲蘊藏成長機會

特種作物更新周期進展不如預期,預算限制持續對終端產品價格構成下行壓力。同時,全球新建溫室和垂直農場計畫在2025年被推遲。

然而,由於能源效率法規和高光合有效輻射(PPF/W,PPE)解決方案的採用,歐洲市場依然保持相對強勁,有效抵消了北美和其他地區的疲軟態勢。2025年,全球LED園藝照明市場規模達到13.65億美元(年增4%)。

展望2026年,歐洲高壓鈉燈(HPS)系統加速被LED取代的趨勢將持續推動市場需求,尤其是在溫室應用領域。同時,北美、亞洲和中東地區將進入新一輪擴張週期,這主要得益於糧食安全政策和出口導向農業投資。預計市場對高光效、光譜可調和智慧LED照明系統的需求將會增加。 TrendForce預測,2030年,市場規模將達到10.41億美元,2025年至2030年的年複合成長率(CAGR)為4%。

在LED封裝領域,預計2026年多通道光譜技術的應用將加速。許多新註冊的產品都具備動態調光功能和高精度控制要求,這將推動對高品質解決方案的需求成長,並促進LED出貨量的成長。經過過去的庫存調整和產業整合,預計2026年農業照明LED的平均售價將趨於穩定。

4.製造商收入:智慧照明及細分市場佔有率不斷擴大

根據TrendForce的最新統計資料,2025年全球20家領先照明製造商的總收入達到233.55億美元,較上年下降2%。前五的公司保持不變:Signify、Acuity Brands、Panasonic、LEDVANCE和Zumtobel。

在具體細分市場中,專業照明領域展現出規模經濟優勢。同時,受房地產市場低迷以及傳統住宅和商業照明市場價格競爭的影響,Signify和LEDVANCE等全球通用照明領導者2025年的收入出現下滑。相較之下,專注於高科技細分領域的公司則保持著強勁的業績。

專注於防爆和工業照明的Warrom公司預計,在2025年營收將成長5.8%,這主要得益於全球能源開採活動的復甦以及對工業安全需求的不斷成長。同樣,專注於船舶和海上能源照明的Grammox集團預計將維持3.2%的穩定成長率,這主要得益於歐盟海事碳排放政策的影響,推動了升級版船舶照明的需求。

TrendForce認為,在通用照明市場規模經濟效益下降的情況下,高科技細分領域將是製造商維持獲利能力和成長的關鍵。

5.LED封裝市場:從價格競爭到穩定與品質提升

根據TrendForce分析,由於西方國際品牌積極採取成本最佳化策略並大力推廣高性價比解決方案,2025年照明LED市場將面臨價格持續下跌和訂單前景疲軟的局面。

經過長期的利潤率壓縮,LED封裝市場預計將在2026年擺脫下行週期。隨著上游材料成本的上升,LED封裝價格預計將趨於穩定,標誌著市場將從持續的價格下跌過渡到銷售收縮與價格穩定並存的局面。

在永續發展政策、減碳目標和綠建築標準不斷提高的推動下,產業結構經歷質的轉變。LED照明產業預計將於2026年觸底反彈,並於2027年開始復甦。 TrendForce保持謹慎樂觀的態度,預測2030年,全球LED照明市場規模將達到37.34億美元,2025年至2030年的年複合成長率(CAGR)為2.5%。

TrendForce透過對通用照明、智慧照明和園藝照明三大細分市場的市場規模、價格趨勢和區域分佈分析,以及對LED封裝產業趨勢的分析,深入剖析了全球LED照明產業。本報告追蹤了前20大製造商的收入和策略,分析了Signify、Acquity、Panasonic、LEDVANCE和Oppel等主要廠商的競爭地位,並基於月度細分市場分析,概述了七大主要照明燈具類別的趨勢和價格。

目錄

第一部分:引言

- 市場研究方法

- 全球經濟(GDP)

- 匯率

第二部分:一般照明市場預測(2026-2030)

- 通用LED照明市場規模 - 需求、市場價值、數量和平均售價 - 依產品分類

- 通用LED照明市場規模、需求、市場價值 - 依類別(燈具和照明設備)分類

- 通用LED照明市場規模、需求、市場價值 - 依地區分類

- 通用LED照明市場規模 - 需求、市場價值和數量 - 依產品和地區分類

- 通用LED照明市場規模、需求、市場價值 - 依應用分類

- 通用LED照明普及率(安裝量)

- 通用LED照明市場 - 價值與數量 - 依應用分類

- 通用LED照明市場 - 價值、數量和平均售價(依電力)

- 通用LED照明市場 - 價值、數量和平均售價 - 依封裝類型分類

- 通用LED照明市場價值 - 色溫(CCT)

- 通用LED照明市場價值與數量 - 顯色指數(CRI)

- 通用LED照明價格

第三部分:智慧照明市場預測(2026-2030年)

- 智慧 LED 照明市場規模、需求、市場價值與應用

- 智慧 LED 照明市場規模、需求、市場價值與區域

第四部分:農業照明市場預測(2026-2030年)

- 園藝LED照明市場規模、需求、市場價值,依應用領域

- 園藝LED照明市場規模、需求、市場價值,依區域

- 農業LED照明市場 - 依晶片類型劃分的價值和數量

- 農業LED照明市場 - 依電力劃分的價值和數量

- 農業LED照明價格

- 園藝LED照明廠商收入排名(2023-2025年預測)

第五部分:照明產業收入排名及預測

- 照明設備製造商收入排名前20(2023-2025年預測)

- 照明設備製造商收入排名前10,依應用領域劃分(2023-2025年預測)

- LED照明廠商收入排名(2023-2025年預測)

第六部分:LED照明產品規格及定價

- 產品及價格 - 燈絲燈 - 依地區劃分

- 產品及價格 - 路燈 - 依地區劃分

- 產品及價格 - 面板燈 - 依地區劃分

- 產品及價格 - 槽型燈 - 依地區劃分

- 產品及價格 - 高/低棚燈 - 依地區劃分

- 產品及價格 - 防爆燈 - 依地區劃分

- 產品及價格園藝照明 - 依應用領域劃分

(PDF)1.2025年全球 LED 照明市場趨勢 - 市場參與者策略

第1章 全球智慧 LED 照明市場趨勢

- 全球智慧 LED 照明市場規模分析(2026-2030年)

- 全球智慧 LED 照明市場規模分析:住宅(2026-2030年)

- 智慧家庭照明產品(2025-2026年)

- 全球智慧 LED 照明市場規模分析:戶外(2026-2030年)

- 全球智慧 LED 照明市場規模分析:工業(2026-2030年)

- 全球智慧 LED 照明市場規模分析:依地區劃分(2026-2030年)

- 智慧照明控制協定 - Bluetooth

- 智慧照明控制協定 - Zhaga

第2章 照明產業收入及市場策略分析

- 照明設備製造商收入排名前20:照明產品(2023-2025)

- 照明製造商收入排名前20:LED照明(2023-2025)

- 照明產業收入及產品策略

- Signify

- Zumtobel

- Fagerhult

- Acuity

- Current

- Panasonic

- Endo Lighting

- 中國照明製造商的收入及產品策略

- LEDVANCE/MLS

- Opple Lighting

- NVC Lighting

- Foshan Lighting

- Yankon Group

(PDF)2.LED照明市場每月報告 - 依細分市場進行應用和產品分析

- 引言

- 趨勢展望

- 市場概覽及特質分析

- 產品類型及應用情境分析

- 主流產品規格及LED需求分析

- 製造商趨勢及競爭格局分析

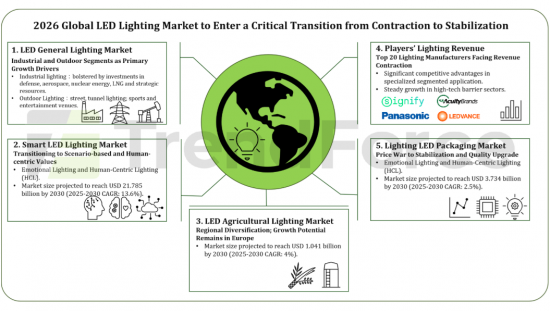

According to the latest TrendForce report, 2026 Global LED Lighting Market Trend- Database and Player Strategies (1H26), the global LED lighting market, after undergoing macroeconomic volatility and demand corrections, is expected to enter a critical transition phase in 2026, shifting from contraction to stabilization. As channel inventories return to healthier levels, the annual decline is projected to narrow significantly, with overall demand gradually reverting to fundamental replacement-driven growth. More importantly, the competitive landscape is undergoing a structural transformation - from price-based competition toward application-driven value creation and system integration capabilities.

Below are 5 strategic observations for the global LED lighting market in 2026:

1. General Lighting Market: Industrial and Outdoor Segments as Primary Growth Drivers

Although general lighting remains in an adjustment phase in 2026, selected subsegments demonstrate resilient growth potential.

Industrial lighting is set to become the core growth engine in 2026, bolstered by investments in defense, aerospace, nuclear energy, liquefied natural gas (LNG), and strategic resources. Simultaneously, the accelerated construction of AI data centers is driving demand for infrastructure lighting tailored for liquid cooling systems and server racks. In the outdoor segment, the renewal of aging infrastructure and upgrades to tunnel lighting standards continue to fuel retrofit demand. Furthermore, lighting for sports and entertainment venues, alongside smart and energy-saving solutions, are providing significant incremental growth to the market.

By region, Europe still dominates the market, followed by the North America and Asia-Pacific regions. The European LED lighting market is projected to expand at a CAGR of 2.3% from 2025 to 2030. This growth is mainly supported by the accelerating enforced adoption of energy-saving lighting retrofit solutions to rein in the rising energy costs. The Asian-Pacific market keeps up its momentum on growth, especially in the Southeastern market, with a CAGR of 3.6% throughout the same forecast period.

2. Smart Lighting Market: Transitioning from Technical Spec Wars to Scenario-based and Human-centric Values

TrendForce indicates that in 2025, the global lighting industry entered a new phase centered on Emotional Lighting and Human-Centric Lighting (HCL). Competitive dynamics are shifting away from traditional performance metrics such as luminous efficacy and communication protocols toward value propositions focused on circadian rhythm regulation and experiential scenarios.

Enabled by AI-based dimming, full-spectrum control, and Software-Defined Lighting (SDL), lighting products evolve from static hardware devices into intelligent system nodes capable of perception and adaptive learning. According to TrendForce data, the smart lighting market is projected to reach USD 21.785 billion by 2030, representing a CAGR of 13.6% from 2025 to 2030. Growth will mostly come from value enhancement through AI enablement and system upgrades in three major application scenarios: residential, outdoor, and industrial lighting.

As AI, SDL, and IoT technologies converge, lighting is transitioning from basic illumination equipment to a critical sensing and interaction node within smart living environments, urban governance systems, and industrial digitalization frameworks. Suppliers with software-hardware integration capabilities, ecosystem collaboration and scenario-aware insights will be well-positioned to gain a competitive edge in the future smart lighting market.

3. Agricultural Lighting: Deepening Regional Differentiation with Upside Potential in Europe

Replacement cycles for specialty crops have not materialized as expected, while budget constraints have led to continued downward pressure on end-product pricing. Meanwhile, new greenhouse and vertical farm construction projects have been postponed globally in 2025.

However, Europe remains comparatively resilient, supported by energy-efficiency regulations and the adoption of high photosynthetic photon efficacy (PPF/W, PPE) solutions, effectively offsetting weakness in North America and other regions. In 2025, the global LED horticultural lighting market reached USD 1.365 billion (+4% YoY).

Looking ahead to 2026, with a specific focus on greenhouse applications, accelerated LED replacement of high-pressure sodium (HPS) systems in Europe will continue to drive demand. Meanwhile, North America, Asia, and the Middle East are entering a new expansion cycle, supported by food security policies and export-oriented agricultural investments. Demand for high-PPE, spectrum-tunable, and intelligent LED lighting systems is expected to increase. TrendForce projects the market to reach USD 1.041 billion by 2030, with a CAGR of 4% from 2025 to 2030.

In the LED packaging segment, 2026 is expected to mark accelerated adoption of multi-channel spectral technologies. Most newly registered products will feature dynamic dimming functionality and higher precision control requirements, driving demand for higher-quality solutions and increased LED shipment volumes. Following previous inventory adjustments and industry consolidation, agricultural lighting LED ASPs are expected to stabilize in 2026.

4. Manufacturer Revenue: Rising Share of Smart Lighting and Segmented Application Markets

According to TrendForce's latest statistics, total revenue of the global top 20 lighting companies is projected to decline 2% YoY to USD 23.355 billion in 2025. The top five players remain unchanged: Signify, Acuity Brands, Panasonic, LEDVANCE, and Zumtobel.

TrendForce observes that at specific segments, professional segmented lighting shows advantages in terms of economies of scale. While global general lighting leaders such as Signify and LEDVANCE face revenue contraction in 2025 due to sluggish real estate markets and price competition in the traditional residential and commercial general lighting markets. Conversely, companies focusing on high-tech niche areas show steady performance.

Warom, specializing in explosion-proof and industrial lighting, is expected to achieve a 5.8% revenue growth for 2025, as it has benefited from the recovery of global energy extraction activities and the rise in industrial safety demands. Similarly, Glamox Group, which focuses on marine and offshore energy lighting, is projected to maintain a steady growth rate of 3.2%, driven by the demand for ship lighting upgrades influenced by the EU's maritime carbon emission policies.

TrendForce believes that as the effect of economies of scale is diminishing in the general lighting market, high-tech niche segments have become the key for manufacturers to maintain profitability and growth.

5. LED Packaging Market: From Price War to Stabilization and Quality Upgrade

TrendForce analysis indicates that in 2025, the lighting LED market faced intensified price erosion and low order visibility due to aggressive cost optimization strategies by international brands from Europe and the USA and concentrated adoption of high cost-performance solutions.

After prolonged margin compression, the LED packaging market is expected to exit its downward cycle in 2026. With rising upstream material costs, LED packaging prices are likely to stabilize, marking a transition from continuous price decline to a volume contraction with price stabilization environment.

Supported by sustainability policies, carbon reduction targets, and strengthened green building standards, the industry structure is undergoing qualitative transformation. The LED lighting industry is expected to complete its cyclical bottoming phase in 2026 and begin recovery in 2027. TrendForce maintains a cautiously optimistic outlook, forecasting the global lighting LED market to reach USD 3.734 billion by 2030, representing a 2025-2030 CAGR of 2.5%.

TrendForce provides in-depth insights into global LED lighting industry trends, covering market size, pricing, and regional distribution across general, smart, and horticultural lighting segments, along with analysis of developments in the LED packaging sector. The report tracks revenue and strategies of the top 20 manufacturers, examines the competitive positioning of leading players such as Signify, Acuity, Panasonic, LEDVANCE, and Opple, and outlines trends and price movements in seven major luminaire categories, supported by monthly segmented markets analysis.

TABLE OF CONTENTS

PART 1 Introduction

- 1.1 Market Research Methodology

- 1.2 Global Economics (GDP)

- 1.3 Exchange Rates

PART 2 General Lighting Market Forecast (2026-2030)

- 2.1 General LED Lighting Market Scale-Demand Market Value & Volume & ASP-by Product

- 2.2 General LED Lighting Market Scale-Demand Market Value-by Category-Lamps & Luminaries

- 2.3 General LED Lighting Market Scale-Demand Market Value-by Region

- 2.4 General LED Lighting Market Scale-Demand Market Value & Volume-by Product & by Region

- 2.5 General LED Lighting Market Scale-Demand Market Value-by Application

- 2.6 General LED Lighting Penetration Rate (Installed Based Volume)

- 2.7 General Lighting LED Market-Value & Volume-by Application

- 2.8 General Lighting LED Market-Value & Volume & ASP-by Power

- 2.9 General Lighting LED Market-Value & Volume & ASP-by Package Type

- 2.10 General Lighting LED Market-Value-by CCT

- 2.11 General Lighting LED Market-Value & Volume-by CRI

- 2.12 General Lighting LED Price

PART 3 Smart Lighting Market Forecast (2026-2030)

- 3.1 Smart LED Lighting Market Scale-Demand Market Value-by Application

- 3.2 Smart LED Lighting Market Scale-Demand Market Value-by Region

PART 4 Agricultural Lighting Market Forecast (2026-2030)

- 4.1 Horticultural LED Lighting Market Scale-Demand Market Value-by Application

- 4.2 Horticultural LED Lighting Market Scale-Demand Market Value-by Region

- 4.3 Agricultural Lighting LED Market-Value & Volume-by Chip Type

- 4.4 Agricultural Lighting LED Market-Value & Volume-by Power

- 4.5 Agricultural Lighting LED Price

- 4.6 Horticultural Lighting LED Player Revenue Ranking (2023-2025E)

PART 5 Lighting Player Revenue Ranking and Estimated

- 5.1 Top 20 Lighting Player Revenue (2023-2025E)

- 5.2 Top 10 Lighting Player Revenue Ranking by Application (2023-2025E)

- 5.3 Lighting LED Player Revenue (2023-2025E)

PART 6 LED Lighting Product Specification and Price

- 6.1 Product & Price- Filament Lamp-by Region

- 6.2 Product & Price- Street Light-by Region

- 6.3 Product & Price- Panel Light-by Region

- 6.4 Product & Price- Troffer-by Region

- 6.5 Product & Price- High/Low Bay-by Region

- 6.6 Product & Price- Explosion Proof Light-by Region

- 6.7 Product & Price- Horticultural Light- by Application

(PDF)1. 2025 Global LED Lighting Market Trend- Player Strategies

Chapter 1 Global Smart LED Lighting Market Trend

- 2026-2030 Global Smart LED Lighting Market Size Analysis

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Residential

- 2025-2026 Smart Residential Lighting Products

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Outdoor

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Industrial

- 2026-2030 Global Smart LED Lighting Market Size Analysis: by Region

- Smart Lighting Control Protocol- Bluetooth

- Smart Lighting Control Protocol- Zhaga

Chapter 2 Lighting Player Revenue and Market Strategies Analysis

- 2023-2025(E) Top 20 Lighting Player Revenue Ranking: Total Lighting

- 2023-2025(E) Top 20 Lighting Player Revenue Ranking: LED Lighting

- Lighting Player Revenue and Product Strategies

- Signify

- Zumtobel

- Fagerhult

- Acuity

- Current

- Panasonic

- Endo Lighting

- Chinese Lighting Player Revenue and Product Strategies

- LEDVANCE / MLS

- Opple Lighting

- NVC Lighting

- Foshan Lighting

- Yankon Group

(PDF)2. LED Lighting Market Monthly Report-Segment Application and Product Analysis

- Foreword

- TrendForce's Perspective

- Market Overview and Feature Analysis

- Product Types and Application Scenario Analysis

- Mainstream Product Specifications and LED Requirement Analysis

- Manufacturer Dynamics and Competitive Landscape Analysis