|

市場調查報告書

商品編碼

1848187

全球和中國的AI資料中心市場(2025年):展開及預測2025 Global and China AI Data Centers: Deployment and Outlook |

|||||||

價格

簡介目錄

本報告重點關注美國和中國通訊服務供應商 (CSP) 的人工智慧資料中心擴張。美國公司在全球擴張並增加國內投資,而中國公司則透過自主研發晶片進行擴張,雙方都將未來的能源安全放在首位。

主要亮點:

- 美國通訊服務供應商正透過整合運算和能源來加速其全球人工智慧資料中心的部署,而中國通訊服務供應商則奉行由BBAT和三大營運商主導的雙軌發展模式。

- 能源可用性、電網穩定性以及政策環境是選址的關鍵因素,因為能源成本和監管政策的調整決定了投資的速度和部署規模。

- 美國通訊服務供應商正在單一專案上投資數百億至數千億美元,並將容量擴展到吉瓦級,以滿足人工智慧和高效能運算 (HPC) 的需求。

- 在國家政策的推動下,中國通訊服務供應商(CSP)正致力於自主研發晶片和建構自主雲端策略,在維護國內核心基礎設施的同時,積極拓展海外市場。

- 高壓直流(HVDC)供電架構正逐步取代傳統模式,成為支撐千兆瓦級運算和降低能耗的關鍵。

樣品

目錄

第1章 簡介

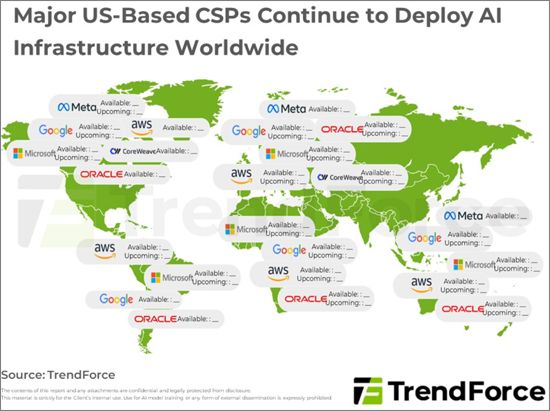

- 總部位於美國的大型通訊服務供應商(CSP)持續在全球部署人工智慧基礎設施,力求在運算能力方面取得競爭優勢。

第二章:北美主要雲端服務供應商正積極向千兆位元組級人工智慧資料中心轉型,因此能源相關因素在選擇未來選址時至關重要。

- Google的北美策略主要集中在美國各地建立多個資料中心,但其位於德國米滕瓦爾德的專案因能源供應問題而被取消。

- 為了回應美國政府的需求,Meta公司的Hyperion超級運算計畫大幅提高了投資目標,達到500億美元。

第三章:甲骨文公司正在推進美國首個自主人工智慧項目,該項目的基礎設施建設大量依賴NVIDIA GPU。

- 未來三年,Starget的目標是實現7吉瓦的發電容量,而甲骨文公司計劃提供超過5.5吉瓦的發電容量。

第四章:NVIDIA宣布投資OpenAI,以增強其在雲端AI市場GPU伺服器領域的影響力。

第五章:受地緣政治與國家政策的引導,中國雲端服務供應商同步在新興市場擴張資料中心。

- 中國雲端服務供應商積極建置國內外資料中心。

第六章:受自主雲端需求和公共建設的驅動,中國三大電信業者推出本土化伺服器和資料中心,成為國家政策的關鍵驅動力。

- 中國電信業者作為中國伺服器和人工智慧市場的關鍵參與者,正在啟動國家級項目

第七章:持續參與中美CSP專用人工智慧資料中心項目,為電力基礎設施(高壓直流輸電等)發展創造機會

簡介目錄

Product Code: TRi-0092

The report highlights AI data center expansion by U.S. and Chinese CSPs. U.S. firms scale globally and invest more at home, while Chinese firms expand with self-developed chips, but both prioritize energy stability going forward.

Key Highlights:

- U.S. CSPs are accelerating global AI data center deployments with a trend toward integrated compute and energy, while Chinese CSPs pursue a dual-track model led by BBAT and the three major telecoms.

- Energy availability, grid stability, and policy environments have become critical in site selection, with power costs and regulatory collaboration shaping investment pace and deployment.

- U.S. CSPs commit single-project investments ranging from tens to hundreds of billions of dollars, scaling to gigawatt-level capacity to support AI and HPC demand.

- Chinese CSPs, backed by national policies, are advancing self-developed chips and sovereign cloud strategies, maintaining core domestic builds while expanding overseas.

- High-voltage direct current (HVDC) power architectures are gradually replacing traditional models, becoming essential to support gigawatt-scale compute and reduce energy consumption.

SAMPLE VIEW

Table of Contents

1. Introduction

- Major US-Based CSPs Continue to Deploy AI Infrastructure Worldwide, Aiming to Gain a Competitive Edge in Computing Power

2. Leading North American CSPs Are Actively Transitioning to GW-Scale AI Data Centers, with Energy-Related Considerations Becoming Critical for Future Site Selection

- Google's Strategy for North America Primarily Involves Establishing Numerous Sites Across the Country, While Its Mittenwald Project in Germany Is Canceled Due to Energy Supply Issues

- Investment Target of Meta's Hyperion Supercomputing Project Has Been Raised Significantly to US$50 Billion in Response to US Government's Needs

3. Oracle Pushes Forward with the First Sovereign AI Project in the US and Relies Heavily on NVIDIA's GPUs for Infrastructure Build-Out

- In Next Three Years, Starget Is Targeted to Reach 7GW, with Oracle Providing Over 5.5GW of Capacity

4. NVIDIA Has Announced Investment in OpenAI to Strengthen Its GPU Server Influence in the Cloud AI Market

5. Chinese CSPs Expand Data Centers in Emerging Markets Simultaneously under Geopolitics and Guidance of National Policies

- Aggressive Construction of Domestic and Overseas Data Centers by Chinese CSPs BBAT

6. Three Major Chinese Telecom Operators Actuate Localized Servers and Data Centers as Key Advocators for National Policies under Demand for Sovereign Cloud and Public Construction

- Chinese Telecom Operators Responsible for Establishment of National Projects as Key Actuators of China's Server and AI Market

7. Ongoing Involvement in AI Data Centers among US and Chinese CSPs to Generate Development Opportunities for Power Infrastructures (e.g. HVDC)

02-2729-4219

+886-2-2729-4219

全球人工智慧資料中心市場:按產品/服務、資料中心類型、部署方式、應用領域、最終用戶和地區分類-預測至2032年

全球人工智慧資料中心市場:按產品/服務、資料中心類型、部署方式、應用領域、最終用戶和地區分類-預測至2032年 全球人工智慧資料中心市場:市場規模、佔有率和趨勢分析(按組件、資料中心類型、部署方式、人工智慧應用領域、產業和地區分類),細分市場預測(2026-2033 年)

全球人工智慧資料中心市場:市場規模、佔有率和趨勢分析(按組件、資料中心類型、部署方式、人工智慧應用領域、產業和地區分類),細分市場預測(2026-2033 年) 人工智慧資料中心市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

人工智慧資料中心市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 全球人工智慧資料中心基礎設施市場:預測(至2034年)-按組件、部署方式、人工智慧工作負載、技術、電力和冷卻基礎設施、最終用戶和地區進行分析全球人工智慧資料中心風險管理市場:預測(至 2034 年)—按解決方案類型、風險管理類型、部署方式、資料中心類型、人工智慧技術、最終用戶和地區進行分析全球人工智慧驅動型資料中心永續性最佳化市場:預測(至 2034 年)—按組件、部署方式、資料中心類別、人工智慧技術類型、永續性最佳化重點領域、最終用戶和地區進行分析全球人工智慧驅動資料中心營運市場預測(至2034年):按部署類型、資料中心類型、應用程式和地區分類全球資料中心人工智慧最佳化網路基礎設施市場:預測(至2034年)-按產品、網路、部署方式、資料中心類別、人工智慧應用、最終使用者和地區進行分析

全球人工智慧資料中心基礎設施市場:預測(至2034年)-按組件、部署方式、人工智慧工作負載、技術、電力和冷卻基礎設施、最終用戶和地區進行分析全球人工智慧資料中心風險管理市場:預測(至 2034 年)—按解決方案類型、風險管理類型、部署方式、資料中心類型、人工智慧技術、最終用戶和地區進行分析全球人工智慧驅動型資料中心永續性最佳化市場:預測(至 2034 年)—按組件、部署方式、資料中心類別、人工智慧技術類型、永續性最佳化重點領域、最終用戶和地區進行分析全球人工智慧驅動資料中心營運市場預測(至2034年):按部署類型、資料中心類型、應用程式和地區分類全球資料中心人工智慧最佳化網路基礎設施市場:預測(至2034年)-按產品、網路、部署方式、資料中心類別、人工智慧應用、最終使用者和地區進行分析 人工智慧互聯的轉折點:物理層面的生態系統轉型與價值創造。

人工智慧互聯的轉折點:物理層面的生態系統轉型與價值創造。 人工智慧資料中心市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

人工智慧資料中心市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

▼