|

市場調查報告書

商品編碼

1994827

乾癬治療藥市場:2025-2035年Psoriasis Drugs Market, 2025 - 2035: Opportunities, Challenges, Strategies & Forecasts |

||||||

概要:

乾癬是一種慢性發炎性皮膚病,全球有超過1.25億人受其影響,其中包括美國超過800萬人。其特徵是出現增厚、發紅、鱗屑狀的斑塊,引起搔癢和疼痛,無論病情輕重,都會給患者帶來巨大的生理、心理和社會經濟負擔。隨著大眾對皮膚、頭髮和指甲外觀的關注度和期望值不斷提高,越來越多的患者尋求更有效、更持久的治療方法。

這種疾病的管理需要終身進行,其重點在於透過抑制過度皮膚細胞更新和減輕發炎來達到緩解。治療方法的選擇取決於疾病類型、受累體表面積以及整體嚴重程度。輕症通常採用局部治療,而中重度乾癬通常需要口服全身性治療、生物製藥或聯合治療。過去十年,乾癬的治療已從廣泛的免疫抑制療法轉向高度選擇性的療法。除了已有的生物製藥(TNF、IL-12/23、IL-17 和 IL-23 抑制劑)外,口服小分子藥物(特別是 TYK2 抑制劑)和新一代生物製藥也相繼問世。這些創新治療方法帶來了前所未有的皮膚症狀完全清除率(PASI 100)、更長的緩解持續時間以及更高的便利性和安全性。因此,市場成長加速,符合治療條件的患者群體擴大,保險公司和醫生對乾癬長期緩解疾病效果的期望也顯著提高。

根據SNS Research估計,到2025年底,乾癬治療市場銷售額預計將達到約200億美元。儘管面臨藥物穩定性問題和競爭對手之間的專利糾紛等挑戰,但在幾款處於後期研發階段的新藥的推動下,該市場預計將在預測期內實現顯著成長。

《乾癬治療藥市場:2025-2035 - 機會、挑戰、策略與預測》的報告,對乾癬治療生態系統進行了詳細評估,內容涵蓋疾病本身、治療方法類型、給藥技術、關鍵趨勢、市場促進因素、挑戰、投資潛力、主要治療方法、藥物開發平臺、機會、未來發展藍圖、價值鏈以及生態系統參與者的概況。報告也提供了2025年至2035年乾癬治療市場規模的預測。這些預測進一步細分為四個治療類別、三種給藥途徑、四個通路、五個地區和26個主要國家。

涵蓋的主題:

本報告涵蓋以下主題:

- 乾癬治療的生態系統

- 市場促進因素與障礙

- 乾癬:疾病及主要趨勢

- 主要藥物類別和主要乾癬治療方法的分析

- 未來藥物開發平臺

- 乾癬藥物傳遞技術

- 產業藍圖與價值鏈

- 概述和策略 66 家領先的生態系統參與企業,包括乾癬治療開發公司。

- 為參與企業提供的策略建議

- 2025年至2035年市場分析及預測

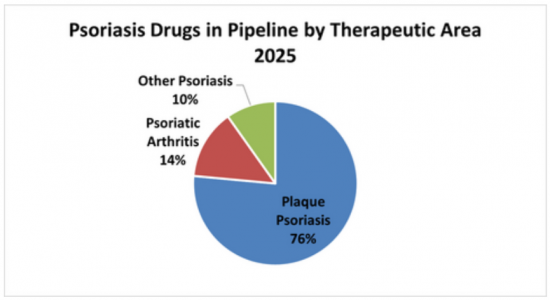

例:依治療領域分類的乾癬藥物開發平臺細分(%)

本報告包含一套完整的Excel 資料表,其中包含報告中所有數值預測的定量資料,以及一個涵蓋乾癬治療市場臨床開發平臺並介紹 51 種有前景的候選藥物的Excel 表格。

主要發現:

本報告的主要結論如下:

- 預計到2025年底,全球乾癬治療市場規模將達到196億美元,主要促進因素包括疾病盛行率上升、診斷率提高以及先進治療方法的普及。鑑於乾癬具有慢性復發的特點,長期治療需求預計將保持穩定,支撐市場在2030年後的穩定成長。

- 生物製藥仍然是乾癬治療市場的基石,IL-17 和 IL-23 抑制劑,特別是 Skyrizi(risankizumab)和 Tremfya(Guselkumab),由於其卓越的療效和持續的反應特性,繼續得到越來越多的應用。

- 在美國,生物相似藥的市場滲透率仍然有限。互通性障礙、曠日持久的訴訟以及合約策略等因素延緩了多種已獲FDA已通過核准的生物類似藥的實用化,導致生物製劑價格居高不下,並阻礙了成本競爭的加劇。

- 研發管線正日益聚焦於下一代免疫調節療法,策略重點也從傳統的TNF和IL-12/23計畫轉向更新、更具獲利潛力的機制。研發工作主要集中在下一代IL-23製劑、選擇性IL-17通路調變器,尤其是口服TYK2抑制劑。由於患者對非注射療法的強烈需求,這些仍然是重要的商業性重點。雖然TNF抑制劑在乾癬性關節炎和長期病情穩定的患者中仍具有臨床效用,但它們已不再是研發的主要成長動力。

- 除了生物製劑之外,口服和外用製劑領域的創新也加速發展。進行的計畫包括TYK2抑制劑、選擇性JAK通路調變器、第二代PDE4抑制劑、維生素D相關或合併外用製劑平台,以及目的是提高用藥依從性和維持緩解的新型多重機制療法。

- 免疫學產品組合具有很高的策略價值,因此產業整合加劇。併購和平台合作仍然是建立競爭優勢的核心,加速了領先的免疫學相關企業產品線的重組和多元化。

本報告主要解答以下問題:

本報告解答了以下關鍵問題:

- 乾癬治療藥物的市場規模有多大?

- 哪些趨勢、挑戰和障礙影響該成長?

- 各個細分市場和地區的生態系統是如何演變的?

- 到2030年,市場規模將達到多少?成長率將是多少?

- 預計哪個國家或細分市場將擁有最高的成長率?

- 生物相似藥在治療乾癬的前景如何?

- 乾癬治療藥物的市場規模有多大?

- 主要市場參與企業有哪些?他們的策略是什麼?

- 原廠藥專利到期會對市場產生什麼影響?

- 乾癬藥物生產商應採取哪些策略來避免競爭?

圖示範例:乾癬治療候選藥物依研發階段分佈(%)

預測性分割:

提供了以下各個子市場及其子類別的市場預測:

治療領域

- TNF抑制劑

- 白細胞介素

- 維生素D類似物和外用類固醇

- 其他

給藥途徑

- 外用

- 口服

- 腸外

通路

- 臨床環境/診所

- 零售藥房

- 數位藥房

- 直接面對消費者(D2C)

當地市場

- 亞太地區

- 歐洲

- 中東和非洲

- 北美洲

- 拉丁美洲和中美洲

國家/地區

- 澳洲

- 巴西

- 加拿大

- 中國

- 埃及

- 法國

- 德國

- 希臘

- 印度

- 以色列

- 義大利

- 日本

- 墨西哥

- 荷蘭

- 波蘭

- 葡萄牙

- 俄羅斯

- 沙烏地阿拉伯

- 南非

- 韓國

- 西班牙

- 瑞士

- 台灣

- 土耳其

- 英國

- 美國

公司和組織清單:

本報告中提及的所有公司和組織如下:

- Abbott Laboratories

- AbbVie

- AbGenomics International

- Acelyrin

- Aclaris Therapeutics

- Actelion Pharmaceuticals

- Akeso Biopharma

- Akros Pharma

- Akzo Nobel Group

- Almirall

- AltruBio

- Alumis(前身為 Esker Therapeutics)

- Alvotech

- Amgen

- Anacor Pharmaceuticals

- AnaptysBio

- Arcutis Biotherapeutics

- Artax Biopharma

- Artelo Biosciences

- AstraZeneca

- Azora Therapeutics

- Bausch & Lomb

- Bausch Health

- Bausch Health Ireland Limited

- Bayer

- Biocad

- Biocon Biologics

- Biofrontera AG

- Biogen

- BioMimetix

- Biosintez

- Bio-Thera Solutions

- BMS(Bristol-Myers Squibb)

- Boehringer Ingelheim

- Boston Pharmaceuticals

- Botanix Pharmaceuticals

- Cadila Healthcare

- Cadila Pharmaceuticals

- Can-Fite BioPharma

- Cantargia

- Celgene Corporation

- Celltrion Healthcare

- Cerbios-Pharma

- Cipher Pharmaceuticals

- Coherus BioSciences

- Dermata Therapeutics

- DICE Therapeutics(Eli Lilly收購)

- Dr. Reddy's Laboratories

- Dusa Pharmaceuticals

- Eli Lilly and Company

- Enavate Sciences

- Encore Dermatology

- EPI Health

- European Medicines Agency(EMA)

- FDA

- Galderma

- Galectin Therapeutics

- Glenmark Pharmaceuticals

- GSK(GlaxoSmithKline)

- Hanwha Pharmaceutical

- Immutep

- Innovent Biologics

- InSite Vision

- Issar Pharma

- Janssen Biotech

- Janssen Pharmaceutical

- Janssen Research & Development

- Japan Tobacco(JT)

- Jiangsu Hengrui Pharmaceuticals Co.

- Johnson & Johnson

- Kyongbo Pharm

- Kyowa Kirin

- LEO Pharma

- Lipidor AB

- Mabpharm

- Maruho

- Mayne Pharma Group

- MC2 Therapeutics

- Meiji Seika Pharma

- Merck

- Merck & Co.

- MIT

- MoonLake Immunotherapeutics

- Mylan

- Nestle Skin Health

- Novartis

- Ono Pharmaceutical

- Ortho Dermatologics

- Pelthos Therapeutics(Ligand Pharmaceuticals 的子公司)

- Pfizer

- Pharmalucence

- Photogen Technologies Inc.

- Pierre Fabre Laboratories

- Pola Pharma

- Portal Instruments

- Promius Pharma

- Protagonist Therapeutics

- Provectus Biopharmaceuticals

- Rani Therapeutics

- Samsung

- Samsung Bioepis

- Sandoz

- Sanofi

- SFA Therapeutics

- Shire

- Sudo Biosciences

- Sun Pharma

- Suzhou Zelgen Biopharmaceuticals

- Takeda

- Taro Pharmaceutical Industries

- Teva

- Theravance Biopharma

- US Department of Justice

- US Federal Trade Commission

- UCB

- UNION Therapeutics

- URL Pharma

- Vanda Pharmaceuticals

- Viatris

- Vyne Therapeutics

- XBiotech

- Xbrane Biopharma

- Yangji Pharmaceutical

- Zydus Group

Synopsis:

Psoriasis is a chronic inflammatory skin disorder affecting more than 125 million people globally, including over 8 million in the United States. Characterized by thick, reddened, scaly plaques that cause itching and pain, the disease imposes substantial physical, psychosocial, and economic burdens across all severity levels. Growing public awareness and rising expectations around skin, hair, and nail appearance have increased the number of patients seeking more effective and durable treatment options.

Disease management is lifelong and focuses on achieving remission by slowing excessive skin-cell turnover and reducing inflammation. Treatment selection depends on disease type, body-surface involvement, and overall severity. Mild disease is typically managed with topical therapies, whereas moderate-to-severe psoriasis often requires oral systemics, biologics, or combination approaches. Over the past decade, psoriasis treatment has shifted from broad immunosuppression to highly selective therapies. Established biologics (TNF, IL-12/23, IL-17, and IL-23 inhibitors) have been complemented by oral small molecules (notably TYK2 inhibitors) and next-generation biologics. These innovations are achieving unprecedented complete skin clearance rates (PASI 100), extended duration of response, and improved convenience and safety profiles. As a result, they are driving stronger market growth, expanding the treatable patient population, and significantly increasing payer and physician expectations for long-term disease modification in psoriasis.

SNS Research estimates that the psoriasis drugs market will account for nearly $20 Billion in revenue by the end of 2025. Despite challenges relating to drug stability and patent disputes amongst competition, the market is poised for significant growth over the forecast period, fueled by several novel agents advancing through late-stage development.

The "Psoriasis Drugs Market: 2025 - 2035 - Opportunities, Challenges, Strategies & Forecasts" report presents an in-depth assessment of the psoriasis drugs ecosystem including psoriasis disorders, types of treatment options, delivery technologies, key trends, market drivers, challenges, investment potential, leading therapies, drug development pipeline, opportunities, future roadmap, value chain, ecosystem player profiles and strategies. The report also presents market size forecasts for psoriasis drugs from 2025 through to 2035. The forecasts are further segmented by 4 therapeutic classes, 3 routes of administration, 4 distribution channels, 5 regions and 26 leading countries.

Topics Covered:

The report covers the following topics:

- Psoriasis drugs ecosystem

- Market drivers and barriers

- Psoriasis disorders and key trends

- Analysis of key drug classes and leading psoriasis drugs

- Future drug development pipeline

- Psoriasis drug delivery technologies

- Industry roadmap and value chain

- Profiles and strategies of 66 leading ecosystem players, including psoriasis drug developers

- Strategic recommendations for ecosystem players

- Market analysis and forecasts from 2025 till 2035

Sample Figure: Psoriasis Drugs Development Pipeline Breakdown by Therapeutic Area (%)

The report comes with an associated Excel datasheet suite covering quantitative data from all numeric forecasts presented in the report, as well as an Excel sheet covering clinical drug development pipeline for the psoriasis drugs market, profiling 51 future candidates.

Key Findings:

The report has the following key findings:

- Global psoriasis drug spending is projected to reach $19.6 billion by the end of 2025, driven by rising disease prevalence, increased diagnosis rates, and expanding access to advanced therapies. Given the chronic, relapsing nature of psoriasis, long-term treatment demand remains stable, supporting steady market growth through 2030 and beyond.

- Biologics remain the backbone of the psoriasis therapeutics market, with IL-17 and IL-23 inhibitors, particularly Skyrizi (risankizumab) and Tremfya (guselkumab), continuing to gain adoption due to superior efficacy and durable response profiles.

- In the U.S., biosimilar penetration remains limited. Interchangeability barriers, litigation timelines, and contracting strategies have slowed the real-world uptake of several FDA-approved biosimilars, sustaining premium biologic pricing and delaying broader cost competition.

- Pipeline activity is increasingly concentrated on next-generation immunomodulators, with strategic emphasis shifting away from legacy TNF and IL-12/23 programs and toward newer, higher-yield mechanisms. Development efforts center on next-generation IL-23 agents, selective IL-17 pathway modulators, and especially oral TYK2 inhibitors, which remain a major commercial focus due to strong patient preference for non-injectable therapies. TNF inhibitors retain clinical utility in psoriatic arthritis and long-term stable disease, but they are no longer a primary R&D growth engine.

- Beyond biologics, innovation is accelerating in oral and topical modalities. Active programs include TYK2 inhibitors, selective JAK pathway modulators, second-generation PDE4 inhibitors, vitamin-D-adjacent or combination-topical platforms, and emerging multi-mechanism regimens aimed at improving adherence and sustained clearance.

- Industry consolidation continues to intensify, reflecting the high strategic value of immunology portfolios. Mergers, acquisitions, and platform partnerships remain central to competitive positioning, reshaping pipelines and accelerating diversification among leading immunology players.

Key Questions Answered:

The report provides answers to the following key questions:

- How big is the psoriasis drugs opportunity?

- What trends, challenges and barriers are influencing its growth?

- How is the ecosystem evolving by segment and region?

- What will the market size be in 2030 and at what rate will it grow?

- Which countries and submarkets will see the highest percentage of growth?

- What are the prospects of biosimilar drugs in psoriasis?

- How big is the market for psoriasis drugs?

- Who are the key market players and what are their strategies?

- How will patent expirations of innovator drugs impact the market?

- What strategies should psoriasis drug manufacturers adopt to remain competitive?

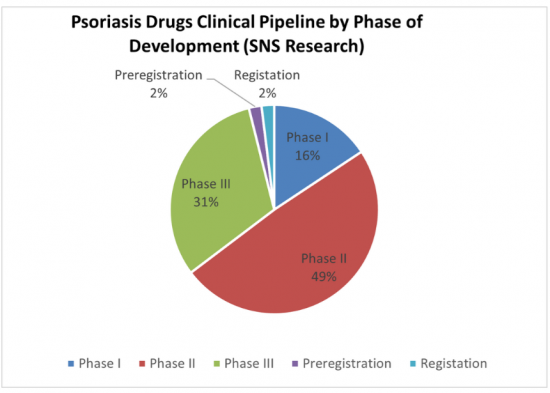

Sample Figure: Distribution of Psoriasis Pipeline Candidates by Developmental Phase (%)

Forecast Segmentation:

Market forecasts are provided for each of the following submarkets and their subcategories:

Therapeutic Class

- TNF Inhibitors

- Interleukins

- Vitamin D Analogues & Topical Steroids

- Others

Route of Administration

- Topical

- Oral

- Parenteral

Distribution Channel

- Point-of-Care / Clinic

- Retail Pharmacies

- Digital Pharmacies

- Direct to Consumer (D2C)

Regional Markets

- Asia Pacific

- Europe

- Middle East & Africa

- North America

- Latin & Central America

Country Markets

- Australia

- Brazil

- Canada

- China

- Egypt

- France

- Germany

- Greece

- India

- Israel

- Italy

- Japan

- Mexico

- Netherlands

- Poland

- Portugal

- Russia

- Saudi Arabia

- South Africa

- South Korea

- Spain

- Switzerland

- Taiwan

- Turkey

- UK

- USA

List of Companies & Organizations:

All the companies and organizations mentioned in the report are listed below:

- Abbott Laboratories

- AbbVie

- AbGenomics International

- Acelyrin

- Aclaris Therapeutics

- Actelion Pharmaceuticals

- Akeso Biopharma

- Akros Pharma

- Akzo Nobel Group

- Almirall

- AltruBio

- Alumis (Previously Esker Therapeutics)

- Alvotech

- Amgen

- Anacor Pharmaceuticals

- AnaptysBio

- Arcutis Biotherapeutics

- Artax Biopharma

- Artelo Biosciences

- AstraZeneca

- Azora Therapeutics

- Bausch & Lomb

- Bausch Health

- Bausch Health Ireland Limited

- Bayer

- Biocad

- Biocon Biologics

- Biofrontera AG

- Biogen

- BioMimetix

- Biosintez

- Bio-Thera Solutions

- BMS (Bristol-Myers Squibb)

- Boehringer Ingelheim

- Boston Pharmaceuticals

- Botanix Pharmaceuticals

- Cadila Healthcare

- Cadila Pharmaceuticals

- Can-Fite BioPharma

- Cantargia

- Celgene Corporation

- Celltrion Healthcare

- Cerbios-Pharma

- Cipher Pharmaceuticals

- Coherus BioSciences

- Dermata Therapeutics

- DICE Therapeutics (Acquired by Eli Lilly)

- Dr. Reddy's Laboratories

- Dusa Pharmaceuticals

- Eli Lilly and Company

- Enavate Sciences

- Encore Dermatology

- EPI Health

- European Medicines Agency (EMA)

- FDA

- Galderma

- Galectin Therapeutics

- Glenmark Pharmaceuticals

- GSK (GlaxoSmithKline)

- Hanwha Pharmaceutical

- Immutep

- Innovent Biologics

- InSite Vision

- Issar Pharma

- Janssen Biotech

- Janssen Pharmaceutical

- Janssen Research & Development

- Japan Tobacco (JT)

- Jiangsu Hengrui Pharmaceuticals Co.

- Johnson & Johnson

- Kyongbo Pharm

- Kyowa Kirin

- LEO Pharma

- Lipidor AB

- Mabpharm

- Maruho

- Mayne Pharma Group

- MC2 Therapeutics

- Meiji Seika Pharma

- Merck

- Merck & Co.

- MIT

- MoonLake Immunotherapeutics

- Mylan

- Nestle Skin Health

- Novartis

- Ono Pharmaceutical

- Ortho Dermatologics

- Pelthos Therapeutics (Part of Ligand Pharmaceuticals)

- Pfizer

- Pharmalucence

- Photogen Technologies Inc.

- Pierre Fabre Laboratories

- Pola Pharma

- Portal Instruments

- Promius Pharma

- Protagonist Therapeutics

- Provectus Biopharmaceuticals

- Rani Therapeutics

- Samsung

- Samsung Bioepis

- Sandoz

- Sanofi

- SFA Therapeutics

- Shire

- Sudo Biosciences

- Sun Pharma

- Suzhou Zelgen Biopharmaceuticals

- Takeda

- Taro Pharmaceutical Industries

- Teva

- Theravance Biopharma

- U.S. Department of Justice

- U.S. Federal Trade Commission

- UCB

- UNION Therapeutics

- URL Pharma

- Vanda Pharmaceuticals

- Viatris

- Vyne Therapeutics

- XBiotech

- Xbrane Biopharma

- Yangji Pharmaceutical

- Zydus Group

全球慢性乾癬市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球慢性乾癬市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 銀屑病治療市場規模、佔有率和成長分析:按治療方法、照光治療、系統療法、替代療法和地區分類——2026-2033年行業預測

銀屑病治療市場規模、佔有率和成長分析:按治療方法、照光治療、系統療法、替代療法和地區分類——2026-2033年行業預測 乾癬治療市場-全球產業規模、佔有率、趨勢、機會和預測:按治療類型、作用機制、給藥途徑、地區和競爭格局分類,2021-2031年

乾癬治療市場-全球產業規模、佔有率、趨勢、機會和預測:按治療類型、作用機制、給藥途徑、地區和競爭格局分類,2021-2031年 銀屑病治療市場:2026-2032年全球市場預測(依治療分類、給藥途徑、疾病嚴重程度、病患年齡層、最終用戶和分銷管道分類)銀屑病治療市場:2026-2032年全球市場預測(按藥物類別、給藥途徑、銀屑病類型、患者人口統計特徵、分銷管道和治療環境分類)

銀屑病治療市場:2026-2032年全球市場預測(依治療分類、給藥途徑、疾病嚴重程度、病患年齡層、最終用戶和分銷管道分類)銀屑病治療市場:2026-2032年全球市場預測(按藥物類別、給藥途徑、銀屑病類型、患者人口統計特徵、分銷管道和治療環境分類) 比美珠單抗市場:依適應症、年齡層、性別、最終用戶、通路和地區分類全球銀屑病治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

比美珠單抗市場:依適應症、年齡層、性別、最終用戶、通路和地區分類全球銀屑病治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年) Tremfya市場分析及至2035年預測:按類型、產品、技術、應用、最終用戶、組件、部署、流程、功能和設備分類乾癬藥物市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、劑型、給藥途徑及研發階段分類

Tremfya市場分析及至2035年預測:按類型、產品、技術、應用、最終用戶、組件、部署、流程、功能和設備分類乾癬藥物市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、劑型、給藥途徑及研發階段分類 阿維A酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測

阿維A酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測