|

市場調查報告書

商品編碼

1343611

鋰離子電池電解液:技術趨勢與市場預測(至2030年)<2023> Lithium-Ion Battery Electrolyte Technology Trends and Market Forecast (~2030) |

||||||

近年來,二次電池市場已從小型IT應用擴展到ESS和電動車。 Panasonic等研發充電電池並引領該行業的日本企業正在輸給LGES等韓國巨頭,而CATL、BYD、CALB等中國企業則在中國政府的支持和無限的國內市場中苦苦掙扎。在此背景下進一步擴大M/S。 韓國、中國和日本的 "三邊體系" 預計將暫時持續,但隨著電動車市場的擴大,北美和歐洲也對大型製造和材料市場表現出持續的興趣。容量二次電池。馬蘇。 特別是,由於每個國家的市場狀況以及法規和政策,二次電池市場的性質預計將發生重大變化。

電解液主要由溶劑、鋰鹽和添加劑組成。 根據產品的性質,電解質是與鋰離子二次電池製造商合作開發的。 小型IT類產品的開發週期短至3至4個月,但xEV電解液的開發和評估需要一年以上的時間。 需要卓越的研發能力來開發和應對各種滿足客戶需求的產品。

電解液市場曾經由日本和韓國佔據主導地位,但由於近年來中國企業的快速成長,前三名的份額已經輸給了中國企業。 在韓國,Donghwa Electrolyte、Soulbrain和Enchem與三大鋰離子二次電池公司(Samsung SDI、LG Energy Solution和SK energy)一起成長為電解液供應商。 在日本,Mitsubishi Chemical正在使其客戶組合多元化,生產 IT 小型電池、xEV 中型電池和大型電池。 在中國,Tinci、Guotai-Huarong、Capchem佔據市場主導地位。

電解液的主要成分鋰鹽(LiPF6)先前主要由日本企業供應,但隨著中國企業擴大產能,情況發生了變化。 在韓國,Foosung 量產通用鋰鹽(LiPF6),Chunbo 量產特殊鋰鹽(LiFSI、LiPO2F2、LiDFOP、LiBOB)。 在電解液製造過程中添加添加劑以提高鋰離子二次電池的壽命和穩定性,包括SEI保護、防過充劑和導電性。 添加劑市場由日本公司主導,但在韓國,Chunbo和Chemtros是主要供應商。

電解質是構成二次電池的四種主要材料之一。 在典型的鋰離子二次電池的製造成本結構中,重要性按以下順序排列:陽極材料>隔膜>陰極材料>電解質。 為了提高單位電池的能量密度,二次電池製造商正在增加陽極和陰極材料的用量並減少電解液的用量。 不過,從2022年到2030年,電池市場預計將以每年平均約23%(容量比)的速度成長。 電解液市場預計將相應成長。

在用於電動車和ESS的大型二次電池中,每個單元電池的電解液用量約為IT的200至4,000倍,因此確保穩定性是一個特別重要的問題。 除了目前已實用化的液態電解質和凝膠狀聚合物電解質(聚合物)外,正在研究開發提高高溫穩定性優異的固態聚合物電解質和全固態陶瓷電解質的穩定性。

這份報告提供了鋰離子二次電池所用電解液的成品和成分的詳細技術信息,還根據我們的各種預測對粘合劑的需求和市場進行了預測,現在可以了解整體規模。

最後,本報告的目的是總結主要電池製造商的電解液需求以及電解液製造商的供應現狀和前景,為該領域的研究人員和相關各方提供廣泛的技術知識市場。

此報告的特點

- 1.電解質成品和組件的總體概述和技術訊息

- 2. 應用於傳統LiB以外的下一代電池的固態電解質和聚合物電解質概述

- 3.根據我們的預測數據提供電解液市場前景的客觀數據

- 4.韓國、中國、日本主要電解液生產商產品及生產狀況詳細介紹

目錄

報告摘要

第一章電解質概述

- 什麼是電解質?

- 電解質的發展趨勢及主要問題

第二章液體電解質發展趨勢

- 液體電解質的成分

- 液體電解質的特性

- 阻燃材料

第三章聚合物電解質發展趨勢

- 聚合物電解質的類型

- 聚合物電解質的特性

- 聚合物電解質的生產方法

第 4 章固體電解質

- 需要開發固體電解質

- 固體電解質的種類及技術特點

- 固態電解質的發展趨勢

第五章電解質最新發展趨勢

- 高壓電解液溶劑

- 鋰鹽

- 添加劑

- 聚電解質

第六章電解質溶劑

- 環狀碳酸酯

- 直鏈碳酸鹽

- 在電極表面形成保護膜的添加劑產生氣體的機制

第七章電解質添加劑

- 用於高鎳陰極界面穩定性的電解質添加劑

- 改善輸出特性的電解質添加劑

- 使用LiFSI鹽的電解液

- 提高熱穩定性的阻燃添加劑

- 用於高容量陽極界面穩定的添加劑

第8-1章電解液市場趨勢與展望

- 電解質需求:依國家劃分

- 電解液的用量:依用途

- 市場狀況:依供應商分類

- 電解液需求:依 LiB 公司劃分

- (SDI/LGES/SKon/Panasonic/CATL/ATL/比亞迪/力神/國軒/AESC)

- 電解液需求預測

- 電解液產能及供需展望

- 電解液價格趨勢

- 電解液市場規模預測

第8-2章電解質材料現況

- 通用鋰鹽(LiPF6)

- 非LiPF6鋰鹽

- 功能性添加劑

第九章電解液生產企業現況

- 韓國電解液公司

- Dongwha Electrolyte/Soulbrain/Enchem/Foosung/Chunbo/Chemtros

- 日本電解質公司

- Mitsubishi/Ube/Centralglass/Tomiyama/MUIS/Nippon Shokubai

- 中國電解液企業

- Tinci/Capchem/Guotai Huarong/Shanshan/Jinniu/DFD/Shinghwa

Recently, the secondary battery market has expanded from small IT applications to ESS and electric vehicles. Japanese companies such as Panasonic, which developed secondary batteries and pioneered the industry, are losing out to Korean powerhouses such as LGES, while Chinese companies such as CATL, BYD, and CALB are further expanding their M/S with the support of the Chinese government and an unlimited domestic market. Although the Korean, Chinese, and Japanese "trilateral system" is expected to continue for the foreseeable future, North America and Europe are also showing continued interest in the large-capacity secondary battery manufacturing and materials market due to the expansion of the electric vehicle market. In particular, the policies and regulations of each country, such as the IRA, are expected to significantly change the landscape of the secondary battery market.

The electrolyte is mainly composed of solvents, lithium salts, and additives. Depending on the nature of the product, the electrolyte will be developed in collaboration with lithium-ion secondary battery manufacturers. For small IT-type products, the development period is as short as three to four months, while electrolytes for xEVs are developed and evaluated for more than a year. Excellent R&D capabilities are required to develop and respond to various products according to customer needs.

In the past, the electrolyte market was dominated by Japan and South Korea, but with the recent rapid growth of Chinese companies, the top three market shares have been taken over by Chinese companies. In Korea, Donghwa Electrolyte, Soulbrain, and Enchem have been able to grow together as electrolyte suppliers with the three major lithium-ion secondary battery companies (Samsung SDI, LG Energy Solution, and SK energy). In Japan, Mitsubishi Chemical has diversified its portfolio of customers producing IT small, xEV medium and large cells. In China, Tinci, Guotai-Huarong, and Capchem dominate the market.

Lithium salts (LiPF6), the main ingredient of electrolyte, have been mostly supplied by Japanese companies in the past, but the game has changed as Chinese companies have increased their CAPA. In South Korea, Foosung provides general-purpose lithium salts (LiPF6), while Chunbo mass-produces specialized lithium salts (LiFSI, LiPO2F2, LiDFOP, LiBOB). Additives are added during the electrolyte manufacturing process to improve the lifespan and stability of Li-ion secondary batteries, such as SEI protection, overcharge prevention agents, and conductive properties. While Japanese companies dominate the additives market, in Korea Chunbo and Chemtros are among the main suppliers.

Electrolyte is one of the four key materials that make up a secondary battery. In the manufacturing cost composition of a typical Li-ion battery, the order of importance is anode material > separator > cathode material > electrolyte. To increase the energy density per unit cell, secondary battery manufacturers are increasing the input of anode and cathode materials, while reducing the input of electrolyte. However, from 2022 to 2030, the battery market is expected to grow at an average annual rate of around 23% (by capacity). The electrolyte market is expected to grow accordingly.

For large-scale rechargeable batteries for electric vehicles and ESS, the amount of electrolyte used is about 200 times to 4,000 times higher on a unit cell basis than for IT, so securing stability is becoming a particularly important issue. In addition to liquid electrolytes and gel polymer electrolytes (polymers) that are currently commercialized, research and development is underway to improve the stability of solid polymer electrolytes and all-solid ceramic electrolytes with excellent high temperature stability.

This report provides detailed technical information on finished electrolyte products and their components for application in lithium-ion secondary batteries and forecasts the demand and market for binders based on our various forecasts to help readers understand the overall scale.

Finally, by summarizing the electrolyte demand of major battery manufacturers and the supply status and outlook of electrolyte companies, the report aims to provide researchers and interested parties in this field with a wide range of insights from technology to market.

Strong points of this report:

- 1. overall overview and technical information on electrolyte finished products and components

- 2. Introduction to solid and polymer electrolytes that will be applied to next-generation batteries other than conventional LIBs

- 3. Provides objective data on the electrolyte market outlook based on our forecast data

- 4. Detailed information on the product and production status of major electrolyte players in Korea, China, and Japan

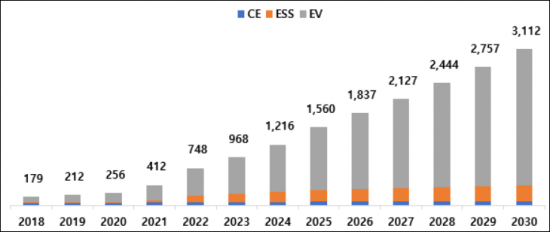

<Global Electrolytes Market Demand Forecas (~2030)>

*Based on SNE battery demand forecasts.

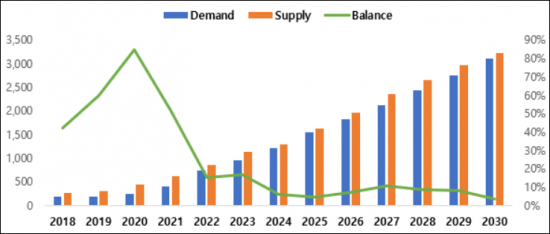

<Global Electrolyte Supply and Demand Outlook (2018~2030)>

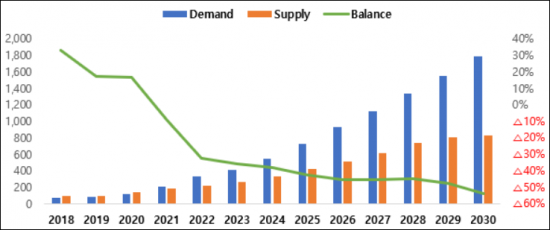

<Electrolyte Supply and Demand Outlook for Non-Chinese Markets (2018~2030)>

*Except for Chinese market supply and demand.

Table of Contents

Outline of Report

Chapter I. Electrolyte Overview

- 1.1. Understanding of electrolytes

- 1.2. Development trends and major issues of electrolytes

Chapter II. Development Trend of Liquid Electrolytes

- 2.1. Composition of liquid electrolytes

- 2.2. Characteristics of liquid electrolytes

- 2.3. Flame retardant material

Chapter III. Development Trend of Polymer Electrolyte

- 3.1. Types of polymer electrolytes

- 3.2. Characteristics of polymer electrolytes

- 3.3. Manufacturing method of polymer electrolytes

Chapter IV. Solid Electrolytes

- 4.1. Necessity for development of solid electrolytes

- 4.2. Types and technical characteristics of solid electrolytes

- 4.3. Development trends of solid electrolytes

Chapter V. Latest Development Trends of Electrolytes

- 5.1. High voltage electrolyte solvents

- 5.2. Lithium salts

- 5.3. Additives

- 5.4. Polyelectrolytes

Chapter VI. Electrolyte Solvents

- 6.1. Cyclic carbonate

- 6.2. Linear carbonate

- 6.3. Gas generation mechanism by additives for forming the protective film on the electrode surface

Chapter VII. Electrolyte Additives

- 7.1. Electrolyte additives for high-Ni cathode interface stabilization

- 7.2. Electrolyte additives for improved output characteristics

- 7.3. Electrolytes using LiFSI salts

- 7.4. Flame retardant additives for improved thermal stability

- 7.5. Additives for high-capacity anode interface stabilization

Chapter VIII-1. Electrolyte Market Trends and Outlook

- 8.1.1. Electrolyte demand by country

- 8.1.2. Electrolyte usage by application

- 8.1.3. Market status by suppliers

- 8.1.4. Electrolyte demand by LIB companies

- (SDI/LGES/SKon/Panasonic/CATL/ATL/BYD/Lishen/Guoxuan(Gotion)/AESC)

- 8.1.5. Electrolyte demand outlook

- 8.1.6. Electrolyte CAPA and supply & demand outlook

- 8.1.7. Electrolyte price trends

- 8.1.8. Electrolyte market size forecast

Chapter VIII-2. Electrolyte Material Status

- 8.2.1. General lithium salts (LiPF6)

- 8.2.2. Non-LiPF6 lithium salts

- 8.2.3. Functional additives

Chapter IX. Electrolyte Manufacturer Status

- 9.1. Korean electrolyte companies

- Dongwha Electrolyte / Soulbrain / Enchem / Foosung / Chunbo / Chemtros

- 9.2. Japanese electrolyte companies

- Mitsubishi / Ube / Centralglass / Tomiyama / MUIS / Nippon Shokubai

- 9.3. Chines electrolyte companies

- Tinci / Capchem / Guotai Huarong / Shanshan / Jinniu / DFD / Shinghwa