|

市場調查報告書

商品編碼

2037814

下一代RNA療法市場(第二版):按治療方法、分子類型、標靶疾病、給藥途徑、地區和主要參與者分類-至2035年的趨勢與預測至2035年Next Generation RNA Therapeutics Market (2nd Edition) by Type of Modality, Type of Molecule, Target Indication, Route of Administration, Geographical Regions and Leading Players-Trends and Forecast Till 2035 |

||||||

下一代RNA治療藥物市場概覽

預計下一代 RNA 療法的市場規模將從2029年的1億美元成長到2035年的27億美元,在預測期內(到2035年)的年複合成長率將達到 63.1%。

下一代RNA治療藥物市場 - 成長與趨勢

隨著時間的推移,基於RNA的治療方法已成為現代醫學中最重要的治療方法之一。 RNA療法在調節蛋白質表現和基因活性方面發揮著非常重要的作用。此外,與傳統治療方法相比,它們具有更高的療效和安全性。然而,這些分子極不穩定,難以達到足夠的給藥濃度,這帶來了許多挑戰。

全球產業領導者正積極推動下一代RNA療法和疫苗的研發,以克服上述挑戰。此外,許多公司也提供尖端技術平台,用於創新RNA療法和疫苗的研發、生產和製造。

環狀RNA(circRNA)、無限循環RNA(eRNA)、自擴增RNA(saRNA)和轉移RNA(tRNA)代表了一種新型治療方法,具有更高的結構穩定性、表達特異性、標靶遞送能力和非免疫抗原性原性。這些特性使其可用於多種治療應用,包括乳癌和流感。鑑於RNA療法和疫苗行業的當前趨勢和未來潛力,預計該市場在不久的將來將以強勁的年複合成長率成長。

成長要素 - 市場擴張的策略促進因素

RNA療法和RNA疫苗市場受多種因素驅動,這些因素不僅對現代醫學產生了變革性影響,也支撐著其快速成長的動力。其中一個關鍵成長要素是基於mRNA的COVID-19疫苗在現實世界中的強大應用。這些疫苗展現出快速研發、測試和部署的能力,同時也能對不斷變異的病原體保持高效率。這項成功顯著提升了人們對該平台的信心,並促使創業投資、策略聯盟以及在腫瘤、罕見遺傳疾病、慢性病和個人化疫苗等治療領域拓展產品線等形式進行了大量投資。

這一發展動力因持續的技術進步而進一步增強,例如先進的脂質奈米顆粒和外泌體遞送系統的開發,這些系統解決了穩定性和靶向遞送方面的傳統難題。此外,諸如自擴增RNA平台等創新技術能夠最佳化劑量和成本,而人工智慧工具的整合則加速了序列設計、最佳化和候選藥物篩選過程。同時,日益加重的全球疾病負擔,包括感染疾病、癌症和遺傳性疾病,以及簡審類和孤兒藥核准不斷增加等支持性法規結構,持續推動市場需求。同時,生物技術公司、合約研發生產機構(CDMO)和研究機構之間高度協作的生態系統促進精準醫療方法的創新和投資,使基於RNA的治療方法能夠選擇性地誘導蛋白質表達或定序疾病相關基因。

市場挑戰 - 阻礙進展的主要障礙

儘管RNA療法和RNA疫苗市場具有上述優勢,但仍面臨許多挑戰,這些挑戰可能會減緩轉型步伐,並增加其廣泛應用的難度。生產製造仍然高度複雜且資本密集,需要專用的無塵室設施、嚴格的品管以及勞動密集的純化過程,顯著增加成本。這些挑戰也造成了原料供應和熟練人員短缺的瓶頸,往往限制了產量,並增加了因意外安全訊號或不一致而召回的風險。

此外,RNA分子脆弱易損,極易被核糖核酸酶(RNase)快速分解,因此遞送仍面臨許多挑戰。另一方面,脂質載體也經常面臨一些問題,例如難以從核內體中逃逸、脫靶效應,尤其是在肝臟外發生免疫活化,這些都可能降低療效或引發毒性擔憂。嚴格的低溫儲存和配送要求也帶來了物流的挑戰,這大大限制了資源匱乏地區的應用。不斷變化的區域法規結構、與兩用技術相關的地緣政治風險以及公眾因錯誤訊息而持續存在的疑慮,都進一步加劇了這些問題的複雜性,導致研發週期延長,中小創新者面臨更大的財務風險,並凸顯了持續創新以實現主流實用化的重要性。

下一代RNA療法市場 - 關鍵洞察

本報告詳細分析了下一代療法市場的現狀,並指出了該行業潛在的成長機會。報告的主要發現包括:

- 在各行業參與者開發的下一代治療方法中,73%仍處於藥物發現和臨床前階段。這些治療方法大多主要用於治療感染疾病。

- 目前,80%的下一代治療方法處於臨床試驗的I期或I/II期階段。尤其值得注意的是,約60%的下一代治療方法/疫苗是為肌肉注射而設計的。

- 儘管環狀RNA療法尚處於發展初期,但它正迅速成為一個新興的治療領域。這種高度穩定且高效的治療方法有望在不久的將來引起廣泛關注。

- 約 40%的治療方法開發後期進行評估,凸顯了下一代 RNA 技術在治療方法開發方面的巨大潛力。

- 2024年,大多數臨床試驗(21%)已啟動。特別是,RNA 療法和疫苗領域已完成的大多數臨床試驗(約 60%)都集中在感染疾病。

- 近年來,針對各種疾病的RNA 療法和疫苗的研究取得了長足發展,因此,許多行業相關人員正致力於在該領域開展進一步的臨床試驗。

- 2024年,與 RNA 療法和疫苗相關的專利約有 30%將被公佈,這反映了基於 RNA 的治療方法和技術領域的許多進步。

- 在該市場達成的交易中,53%集中在saRNA療法/疫苗的臨床試驗中。其中,50%的夥伴關係著重於評估針對腫瘤疾病的治療方法。

- 據報道,2021年該領域的投資約佔 40%,創業投資成為最主要的資金籌措模式,A 輪融資佔交易總數的64%。

- 預計到2029年,市場規模約為1億美元。預計在預測期內(至2035年),該數字將以63.1%的年複合成長率成長,到2035年達到約27億美元。

下一代RNA療法市場

市場規模和機會分析是根據以下參數進行細分的:

治療方法

- 治療方法

- 疫苗

分子類型

- circRNA

- sacRNA

- saRNA

目標疾病

- 進行性固體癌

- 肝細胞癌

- 遺傳性骨髓衰竭綜合症

- 放射線引起的口乾和唾液分泌減少

- 季節性流感

給藥途徑

- 導管內給藥

- 肌肉內注射

- 瘤內給藥

- 靜脈注射

地區

- 北美洲

- 美國

歐洲

- 法國

- 德國

- 義大利

- 西班牙

- 英國

- 其他

亞太地區

- 新加坡

下一代RNA治療藥物市場 - 關鍵細分市場

在RNA療法領域,哪種治療方法佔最大的市場佔有率?

下一代RNA療法市場細分為多種形式,包括疫苗和治療藥物。據預測,到2035年,治療藥物細分市場預計將佔據更大的市場佔有率(超過80%)。此外,預計該細分市場在預測期內將以顯著的速度成長。這主要是因為治療藥物的應用潛力比疫苗更廣泛。治療藥物可以治療急性和慢性疾病,擴大了市場潛力。相較之下,疫苗主要用於預防,針對感染疾病。

在下一代RNA療法領域,哪種分子類型有望最快成長?

產業預測顯示,到2035年,saRNA分子將佔據約60%的市場。此外,saRNA分子的市場佔有率預計將顯著成長,在預測期內以73.6%的年複合成長率成長。這是因為,與其他RNA治療方法(例如siRNA)相比,saRNA的雙鏈結構能夠增強轉錄層面的基因表現。這確保了能夠產生更多可用於治療疾病的蛋白質。

哪些適應症將佔據RNA療法的最大市場佔有率?

對下一代RNA療法市場的分析預測,到2035年,進行性固體癌細分市場將佔據最大的市場佔有率(約35%)。這一趨勢歸因於全球癌症發生率的不斷上升,癌症仍然是一項重大的健康挑戰。此外,遺傳性骨髓衰竭症候群細分市場預計在短期內將維持較高的年複合成長率。該成長歸因於遺傳性骨髓衰竭症候群的罕見性、其主要為單基因疾病的特性以及目前缺乏有效的治療方案。

北美:市場佔有率最大,引領市場。

預計北美將在下一代RNA療法市場佔據最大的市場佔有率(超過65%)。這主要歸功於北美對RNA生物學的大量公共資金投入,推動了該領域臨床研究的日益活躍。

下一代RNA療法市場主要公司範例

- AlphaVax

- Arcturus Therapeutics

- BioNTech

- HDT Bio

- MiNA Therapeutics

- VLP Therapeutics

下一代RNA治療藥物市場 - 研究範圍

- 市場規模和機會分析:本報告詳細分析了下一代 RNA 療法市場,重點關注關鍵市場細分,例如 [A]治療方法類型、[B] 分子類型、[C] 治療領域、[D] 給藥途徑以及 [E] 和 [F] 主要地區。

- 市場概覽:本章對已通過核准或評估中的新一代RNA療法和RNA疫苗進行全面評估,評估涵蓋多個參數,例如[A] 治療模式類型、[B] 分子類型、[C] 遞送載體類型、[D] 研發階段、[E] 治療領域以及[F] 關鍵細分市場(環狀RNA和saRNA)。此外,本章也分析了多家新一代RNA療法和RNA疫苗研發公司,分析指標包括[G] 成立年份、[H] 公司規模、[I] 總部所在地以及[J] 最活躍的公司(基於治療方法數量)。

- 技術趨勢:本章對開發和實施的、用於支持下一代RNA療法和RNA疫苗研發的技術進行了全面評估,評估考慮了多種參數,例如[A]分子分類、[B]分子類型、[C]技術能力、[D]治療領域和[E]最先進的研發階段。此外,本章還基於[F]成立年份、[G]公司規模、[H]總部所在地和[I]商業模式,對多家下一代RNA療法和RNA疫苗技術研發公司進行了分析。

- 藥物概況:對於處於最後開發階段的候選藥物,提供詳細的概況,重點關注[A]開發公司詳情、[B]藥物概述、[C]臨床試驗資訊、[D]臨床試驗終點、[E]臨床試驗結果和[F]預計銷售額。

- 臨床試驗分析:根據以下參數審查已完成、進行和計劃中的各種下一代 RNA 療法和 RNA 疫苗的臨床試驗:[A]實驗狀況註冊年份,[B] 試驗狀態,[C] 試驗階段,[D] 入組患者人數,[E] 申辦方類型,[F] 治療領域,[G] 試驗檢驗,[H] 主要機構(基於試驗)

- 專利分析:針對與下一代 RNA 療法和 RNA 疫苗相關的各種已申請/已註冊專利,分析基於以下幾點:[A] 專利類型(已註冊專利、專利申請、其他),[B] 專利公開年份,[C] 專利管轄區,[D] CPC 分類代碼,[E] 新的重點領域,[C] 專利區經過的年限,/工業專利估值。

- 合作與聯合研究:根據幾個相關參數分析該領域建立的合作關係,包括[A] 合作年份,[B] 合作類型,[C] 分子類型,[D] 合作重點領域,[E] 合作目的,[F] 治療領域,[G] 最活躍的參與者(根據合作數量),以及[H] 該市場合作活動的區域分佈。

- 資金與投資分析:[A] 資金年份,[B] 資金形式,[C] 分子類型,[D] 投資金額,[E] 地區,[F] 資金用途,[G] 研發階段,[H] 治療領域,[I] 主要參與者(根據籌集資金數量和金額)以及 [J] 主要投資者(根據融資交易數量)等根據幾個相關參數對該領域的投資進行詳細評估。

- 大型製藥企業分析:基於幾個相關參數,包括[A]舉措數量,[B]舉措啟動年份,[C]舉措類型,[D]舉措目標,[E]舉措重點領域,以及[F] 總部所在地,全面檢驗了大型製藥企業實施的以下一代 RNA 療法和 RNA 疫苗為重點的各種舉措。

目錄

第1章 背景

第2章 調查方法

第3章 市場動態

第4章 宏觀經濟指標

第5章 執行摘要

第6章 引言

- 下一代RNA療法和疫苗概述

- 下一代RNA療法和疫苗的演進

- 下一代RNA分子類型

- 下一代RNA分子的關鍵方面

- 傳統RNA技術面臨的主要挑戰

- 使用下一代RNA技術的優勢

第7章 市場狀況:RNA療法與RNA疫苗

- RNA療法和RNA疫苗概述

- RNA療法與RNA疫苗:臨床治療方法概述

- RNA療法與RNA疫苗:藥物研發公司概覽

- RNA療法與RNA疫苗:自擴增RNA療法的現狀

- RNA療法與RNA疫苗:環狀RNA療法的現狀

第8章 技術概述

- RNA治療與RNA疫苗技術概述

- RNA療法與RNA疫苗:下一代RNA技術/平台開發商的現狀

第9章 藥物概況

- ARCT-154

- Gemcovac

- VLPCOV-01

- AVX901

- BNT161

- MTL-CEBPA +Sorafenib

第10章 臨床試驗分析

- 調查方法和關鍵參數

- RNA療法與RNA疫苗:臨床試驗分析

第11章 專利分析

第12章 夥伴關係與合作

第13章 資金籌措與投資分析

第14章 主要製藥公司的舉措

- 分析調查方法

- RNA療法和RNA疫苗:主要製藥公司的舉措

第15章 下一代RNA療法的全球市場

第16章 下一代RNA治療藥物市場(依治療方法)

第17章 下一代RNA治療藥物市場(依分子類型)

第18章 下一代RNA治療藥物市場(依目標疾病)

第19章 下一代RNA治療藥物市場(依給藥途徑)

第20章 下一代RNA治療藥物市場(依地區)

第21章 下一代RNA療法市場(依主要公司)

第22章 下一代RNA治療藥物市場及藥品銷售預測

- 下一代RNA療法:藥物銷售預測

- MTL-CEBPA

- BNT 161/PF-07926307

- STX-001

- RXRG001

- EXG-34217

第23章 市場機會分析:北美

第24章 市場機會分析:歐洲

第25章 市場機會分析:亞太地區

第26章 結論

第27章 附錄1:表格形式資料

第28章 附錄2:公司與組織列表

Next Generation RNA Therapeutics Market: Overview

As per Roots Analysis, the next generation therapeutics market is estimated to grow from USD 0.1 billion in 2029 to USD 2.7 billion by 2035, at a CAGR of 63.1% during the forecast period, till 2035.

Next Generation RNA Therapeutics Market: Growth and Trends

RNA-based treatments have become one of the most important therapeutic approaches in the contemporary healthcare sector over time. RNA therapeutics play a critical role in protein expression and the regulation of gene activity. Additionally, when compared to conventional treatment methods, they provide improved therapeutic and safety characteristics. The extremely unstable nature of these molecules and their distribution in sufficient concentrations, however, raise several issues.

Global industry leaders are pushing the development of next-generation RNA therapies and vaccines to get over the aforementioned obstacles. Further, several companies also provide cutting-edge technological platforms for the creation, development, and production of innovative RNA therapies and vaccines.

Circular RNA (circRNA), endless RNA (eRNA), self-amplifying RNA (saRNA), and transfer RNA (tRNA) are examples of emerging modalities that exhibit improved structural stability, expression specificity, targeted delivery, and non-immunogenic characteristics. These characteristics allow their utilization across various therapeutic applications including breast cancer and influenza. Given the current trends and anticipated potential of the RNA therapies and vaccines industry, the market is expected to grow at a healthy CAGR in the near future.

Growth Drivers: Strategic Enablers of Market Expansion

The RNA therapeutics and RNA vaccines market is driven by a numerous factors underscoring its transformative impact on modern medicine and supporting its accelerated growth trajectory. A key growth driver has been the strong real-world validation of mRNA-based COVID-19 vaccines, which demonstrated the ability for rapid development, testing, and deployment while maintaining high efficacy against evolving pathogens. This success has significantly strengthened confidence in the platform, triggering substantial investments in the form of venture capital, strategic partnerships, and pipeline expansion across therapeutic areas such as oncology, rare genetic disorders, chronic diseases, and personalized vaccines.

This momentum is further reinforced by ongoing technological advancements, including the development of advanced lipid nanoparticle and exosome-based delivery systems that address prior challenges related to stability and targeted delivery. Additionally, innovations such as self-amplifying RNA platforms have enabled dose and cost optimization, while the integration of AI-driven tools has accelerated sequence design, optimization, and candidate selection timelines. Moreover, the increasing global burden of diseases including infectious diseases, cancer, and genetic disorders combined with supportive regulatory frameworks, such as fast-track designations for orphan drugs and a growing number of product approvals, continues to drive market demand. At the same time, a highly collaborative ecosystem involving biotechnology companies, contract development and manufacturing organizations (CDMOs), and research institutions is fostering innovation and investment in precision medicine approaches, enabling RNA-based therapies to selectively direct protein expression or silence disease-associated genes.

Market Challenges: Critical Barriers Impeding Progress

Despite the abovementioned advantages, the RNA therapeutics and RNA vaccines market faces significant hurdles, that can slow the pace of transition and raise barriers for widespread implementation. Manufacturing remains exceptionally complex and capital-intensive, requiring specialized cleanroom facilities, rigorous quality oversight, and labor-intensive purification steps that significantly increase costs. These challenges also create bottlenecks in raw material supply and skilled personnel availability, often limiting production volumes and increasing vulnerability to recalls due to unexpected safety signals or inconsistencies.

In addition, delivery hurdles persist as RNA molecules are fragile and prone to rapid degradation by RNases, while lipid carriers frequently struggle with inefficient endosomal escape, off-target effects, or immune activation that can diminish potency or raise toxicity concerns, particularly outside the liver. Logistical challenges stem from stringent ultra-cold storage and distribution requirements, which significantly limit reach in low-resource settings. These issues are further compounded by evolving regional regulatory frameworks, geopolitical risks associated with dual-use technologies, and persistent public hesitancy driven by misinformation, collectively extending timelines, increasing financial risks for smaller innovators, and underscoring the need for continued innovation to achieve mainstream viability.

Next Generation RNA Therapeutics Market: Key Insights

The report delves into the current state of the next generation therapeutics market and identifies potential growth opportunities within industry. Some key findings from the report include:

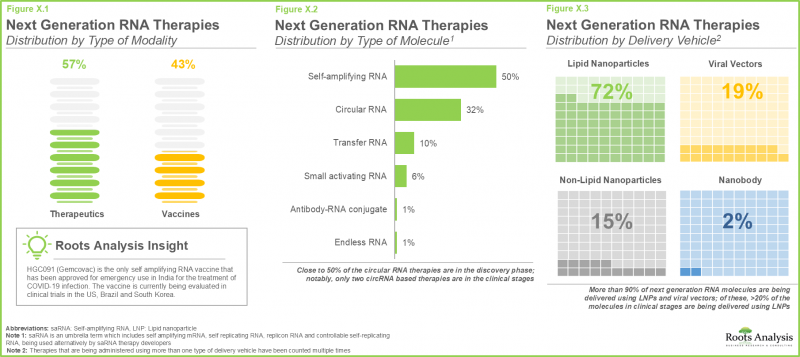

- 73% of the next generation therapies being developed by various industry players are in discovery and preclinical stages; most of these therapies primarily focus on the treatment of infectious diseases.

- 80% of the clinical stage next generation therapies are in phase I and phase I / II; notably, around 60% clinical stage next generation therapies / vaccines are designed for intramuscular administration.

- Despite being in early stages of development, circular RNA therapies form a rapidly advancing therapy segment; this highly stable and efficient therapeutic modality is anticipated to gain significant popularity in the coming future.

- ~40% therapies are being evaluated in late-stages of development, highlighting the significant potential of next generation RNA technologies in therapy development.

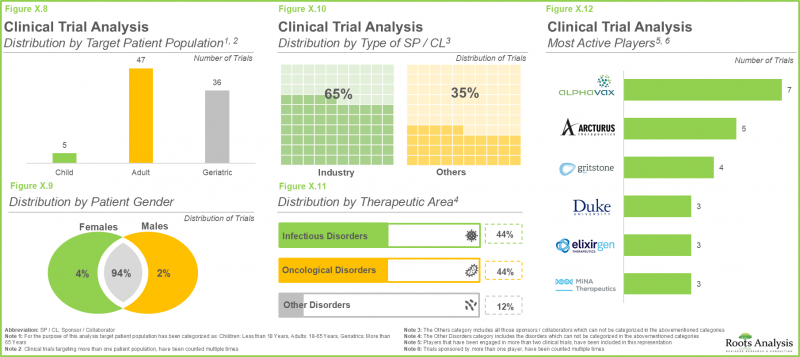

- Majority of the clinical trials (21%) were registered in 2024; notably, most of the (~60%) clinical trials completed in the RNA therapeutics and vaccines domain were focused on infectious diseases.

- Recently, the exploration of RNA therapeutics and vaccines in targeting various disorders has gained momentum, consequently drawing attention from several industry players to conduct more trials in this domain.

- Around 30% of the patents related to RNA therapeutics and vaccines have been published in 2024, reflecting numerous advancements in the field of RNA-based therapies and technologies.

- 53% of the deals inked in this market are focused on clinical research of saRNA therapeutics / vaccines; of these, 50% partnerships focus on the evaluation of therapies targeting oncological disorders.

- Around 40% of the investments made in this domain were reported in the year 2021; notably venture capital emerged as the most prominent funding model, with Series A rounds accounting for 64% of transactions.

- In 2029, the market size is estimated to be around USD 0.1 billion; this value is further projected to reach about USD 2.7 billion in 2035, growing at an annualized CAGR of 63.1%, during the forecast period till 2035.

Next Generation RNA Therapeutics Market

The market sizing and opportunity analysis has been segmented across the following parameters:

Type of Modality

- Therapeutics

- Vaccines

Type of Molecule

- circRNA

- sacRNA

- saRNA

Target Indication

- Advanced Solid Tumors

- Hepatocellular Carcinoma

- Inherited Bone Marrow Failure Syndrome

- Radiation-Induced Xerostomia and Hyposalivation

- Seasonal Influenza

Route of Administration

- Intraductal Route

- Intramuscular Route

- Intratumoral Route

- Intravenous Route

Geographical Regions

- North America

- US

Europe

- France

- Germany

- Italy

- Spain

- UK

- Rest of Europe

Asia-Pacific

- Singapore

Next Generation RNA Therapeutics Market: Key Segments

Which Modality Holds the Biggest Market Share for RNA Therapeutics?

The market for next-generation RNA treatments is segmented across various modalities, including vaccines and therapeutics. According to the next generation RNA therapeutics market forecast, the therapeutics sub-segment is expected to hold a larger proportion (>80%) in 2035. Furthermore, during the forecast period, this sub-segment is anticipated to increase at a notable rate. This is mainly because medicines have a wider range of possible applications than vaccinations. Therapeutics can treat both acute and chronic illnesses, increasing their market potential, in contrast to vaccines, which are mostly preventive and target infectious diseases.

Which molecule type exhibits the fastest growth in the next-generation RNA therapeutics sector?

According to the industry prediction, saRNA molecules are expected to have around 60% of the total market share by 2035. Additionally, the market is anticipated to see a significant rise in the proportion of saRNA molecules, expanding at a CAGR of 73.6% over the course of the projected period. This is because, in contrast to other RNA therapies like siRNAs, its double-stranded structure allows for enhanced gene expression at the transcriptional level. This guarantees the development of larger amounts of proteins that can be used to treat illnesses.

Which Target Indication Has the Biggest Market Share for RNA Therapeutics?

The advanced solid tumors subsegment is anticipated to hold the largest (~35%) market share in 2035, according to the next generation RNA therapies market analysis. This trend can be attributed to the rising global prevalence of oncological diseases, which continue to pose significant health challenges. Furthermore, the hereditary bone marrow failure syndrome sub-segment is anticipated to register a comparatively higher CAGR in the near term. This growth is driven by the rarity and predominantly monogenic nature of inherited bone marrow failure disorders, coupled with the current lack of effective therapeutic options.

North America: Taking the Lead in the Market with the Highest Share

North America is expected to have the largest market share (more than 65%) for next-generation RNA therapies. This is due to significant public funding in RNA biology, which has driven increased clinical activity within the field.

Example Players in Next Generation RNA Therapeutics Market

- AlphaVax

- Arcturus Therapeutics

- BioNTech

- HDT Bio

- MiNA Therapeutics

- VLP Therapeutics

Next Generation RNA Therapeutics Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the next generation RNA therapeutics market , focusing on key market segments, including [A] type of modality, [B] type of molecule, [C] therapeutic areas, [D] route of administration [E] and [F] key geographical regions.

- Market Landscape: A comprehensive evaluation of next generation RNA therapeutics and RNA vaccines that are either approved or being evaluated in different stages of development, considering various parameters, such as [A] type of modality, [B] type of molecule, [C] type of delivery vehicle, [D] phase of development [E] therapeutic area and [F] key niche market segments (circRNA and saRNA). Additionally, the chapter includes analysis of various next generation RNA therapeutic and RNA vaccine developers, based on their [G] year of establishment, [H] company size, [I] location of headquarters and [J] most active players (in terms of number of therapies).

- Technology Landscape: A comprehensive evaluation of technologies that are being developed / deployed to support the development of next generation RNA therapeutics and RNA vaccines, considering various parameters, such as [A] class of molecule, [B] type of molecule, [C] capabilities of the technology, [D] therapeutic area and [E] highest phase of development. Additionally, the chapter features analysis of various next generation RNA therapeutic and RNA vaccine technology developers, based on their [F] year of establishment, [G] company size, [H] location of headquarters and [I] operational model.

- Drug Profiles: In-depth profiles of drug candidates that are in advanced stages of development, focusing on [A] details on its developer, [B] drug overview, [C] clinical trial information, [D] clinical trial endpoints, [E] clinical trial results and [F] estimated sales.

- Clinical Trial Analysis: Examination of completed, ongoing, and planned clinical studies of various next generation RNA therapeutics and RNA vaccines, based on parameters like [A] trial registration year, [B] trial status, [C] trial phase, [D] patients enrolled, [E] type of sponsor, [F] therapeutic area, [G] study design, [H] leading organizations (in terms of number of trials), [I] focus area and [J] geography.

- Patent Analysis: Detailed analysis of various patents filed / granted related to next generation RNA therapeutics and RNA vaccines based on [A] type of patent (granted patents, patent applications and others), [B] patent publication year, [C] patent jurisdiction, [D] CPC symbols, [E] emerging focus areas, [F] patent age, [G] leading industry / non-industry players (in terms of number of patents filed / granted) and [H] patent valuation.

- Partnerships and Collaborations: An analysis of partnerships established in this sector based on several relevant parameters, such as the [A] year of partnership, [B] type of partnership, [C] type of molecule, [D] focus of partnership, [E] purpose of partnership, [F] therapeutic area, [G] most active players (in terms of number of partnerships) and [H] the regional distribution of partnership activity in this market.

- Funding and Investment Analysis: A detailed evaluation of the investments made in this domain based on several relevant parameters, such as [A] year of funding, [B] type of funding, [C] type of molecule, [D] amount invested, [E] geography, [F] purpose of funding, [G] stage of development, [H] therapeutic area, [I] most active players (in terms of number and amount of funding instances) and [J] leading investors (in terms of number of funding instances).

- Big Pharma Analysis: A comprehensive examination of various initiatives focused on next generation RNA therapeutics and RNA vaccines undertaken by major pharmaceutical companies based on several relevant parameters, such as [A] number of initiatives, [B] year of initiative, [C] type of initiative, [D] purpose of initiative, [E] focus of initiative and [F] location of headquarters.

Key Questions Answered in this Report

- Which are the leading companies in the next generation RNA therapeutics market?

- Which region dominates the next generation RNA therapeutics market?

- What are the key trends observed in the next generation RNA therapeutics market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by next generation RNA therapeutics developers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. BACKGROUND

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Executive Summary: Market Landscape

- 5.2. Executive Summary: Market Trends

- 5.3. Executive Summary: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Overview of Next Generation RNA Therapeutics and Vaccines

- 6.2. Evolution of Next Generation RNA Therapeutics and Vaccines

- 6.3. Types of Next Generation RNA Molecules

- 6.4. Key Aspects of Next Generation RNA Molecules

- 6.5. Key Challenges Associated with Traditional RNA Modalities

- 6.6. Advantages of Using Next Generation RNA Modalities

7. MARKET LANDSCAPE: RNA THERAPEUTICS AND RNA VACCINES

- 7.1. Overview of RNA Therapeutics and RNA Vaccines Therapies

- 7.1.1. Analysis by Type of Modality

- 7.1.2. Analysis by Type of Molecule

- 7.1.3. Analysis by Delivery Vehicle

- 7.1.4. Analysis by Stage of Development

- 7.1.5. Analysis by Therapeutic Area

- 7.1.6. Most Active Players: Analysis by Number of Therapies

- 7.2. RNA Therapeutics and RNA Vaccines: Clinical Stage Therapies Landscape

- 7.2.1. Analysis by Phase of Development

- 7.2.2. Analysis by Route of Administration

- 7.2.3. Analysis by Therapeutic Area

- 7.3. RNA Therapeutics and RNA Vaccines: Therapy Developers Landscape

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.4. RNA Therapeutics and RNA Vaccines: Self-amplifying RNA Therapies Landscape

- 7.4.1. Analysis by Phase of Development

- 7.4.2. Analysis by Therapeutic Area

- 7.4.3. Most Active Players: Analysis by Number of Therapies

- 7.5. RNA Therapeutics and RNA Vaccines: Circular RNA Therapies Landscape

- 7.5.1. Analysis by Phase of Development

- 7.5.2. Analysis by Therapeutic Area

- 7.5.3. Most Active Players: Analysis by Number of Therapies

8. TECHNOLOGY LANDSCAPE

- 8.1. Overview of RNA Therapeutics and RNA Vaccines Technologies

- 8.1.1. Analysis by Class of Molecule

- 8.1.2. Analysis by Type of Molecule

- 8.1.3. Analysis by Capabilities of the Technology

- 8.1.4. Analysis by Therapeutic Area

- 8.1.5. Analysis by Highest Stage of Development

- 8.1.6. Analysis by Class of Molecule and Therapeutic Area

- 8.1.7. Analysis by Class of Molecule and Highest Stage of Development

- 8.1.8. Analysis by Type of Molecule and Capabilities of the Technology

- 8.2. RNA Therapeutics and RNA Vaccines: Next Generation RNA Technology / Platform Developers Landscape

- 8.2.1. Analysis by Year of Establishment

- 8.2.2. Analysis by Company Size

- 8.2.3. Analysis by Location of Headquarters

- 8.2.4. Analysis by Operational Model

9. DRUG PROFILES

- 9.1. ARCT-154

- 9.1.1. Company Overview

- 9.1.2. Drug Overview

- 9.1.3. Clinical Trial Information

- 9.1.4. Clinical Trial Endpoints

- 9.1.5. Clinical Trial Results

- 9.2. Gemcovac

- 9.3. VLPCOV-01

- 9.4. AVX901

- 9.5. BNT161

- 9.6. MTL-CEBPA + Sorafenib

10. CLINICAL TRIAL ANALYSIS

- 10.1. Methodology and Key Parameters

- 10.2. RNA Therapeutics and RNA Vaccines: Clinical Trial Analysis

- 10.2.1. Analysis by Trial Registration Year

- 10.2.2. Analysis by Trial Status

- 10.2.3. Analysis by Trial Registration Year and Trial Status

- 10.2.4. Analysis by Trial Phase

- 10.2.5. Analysis of Patients Enrolled by Trial Phase

- 10.2.6. Analysis of Patients Enrolled by Trial Registration Year

- 10.2.7. Analysis by Study Design

- 10.2.8. Analysis by Target Patient Population

- 10.2.9. Analysis by Patient Gender

- 10.2.10. Analysis by Type of Sponsor / Collaborator

- 10.2.11. Analysis by Therapeutic Area

- 10.2.12. Most Active Players: Analysis by Number of Trials

- 10.2.13. Analysis by Geography

11. PATENT ANALYSIS

- 11.1. Methodology and Key Parameters

- 11.2. RNA Therapeutics and RNA Vaccines: Patent Analysis

- 11.2.1. Analysis by Publication Year

- 11.2.2. Analysis by Type of Patent

- 11.2.3. Analysis of Granted Patents and Patent Applications by Publication Year

- 11.2.4. Analysis by Type of Applicant

- 11.2.5. Analysis by Application Year

- 11.2.6. Analysis by Patent Jurisdiction (Region)

- 11.2.7. Analysis by Patent Jurisdiction (Country)

- 11.2.8. Analysis by Patent Age

- 11.2.9. Leading Industry Players: Analysis by Number of Patents

- 11.2.10. Leading Non-Industry Players: Analysis by Number of Patents

- 11.2.11. Leading Individual Assignees: Analysis by Number of Patents

- 11.2.12. Analysis by CPC Symbols

- 11.3. Patent Benchmarking Analysis

- 11.4. Patent Valuation Analysis

12. PARTNERSHIPS AND COLLABORATIONS

- 12.1. Partnership Models

- 12.2. RNA Therapeutics and RNA Vaccines: Partnerships and Collaborations

- 12.2.1. Analysis by Year of Partnership

- 12.2.2. Analysis by Type of Partnership

- 12.2.3. Analysis by Year and Type of Partnership

- 12.2.4. Analysis by Year of Partnership and Type of Molecule

- 12.2.5. Analysis by Purpose of Partnership

- 12.2.6. Analysis by Focus Area of Partnership

- 12.2.7. Analysis by Therapeutic Area

- 12.2.8. Most Active Players: Analysis by Number of Partnerships

- 12.2.9. Analysis by Geography

- 12.2.9.1. Local and International Deals

- 12.2.9.2. Intracontinental and Intercontinental Deals

13. FUNDING AND INVESTMENT ANALYSIS

- 13.1. Funding Models

- 13.2. Funding Lifecycle Analysis

- 13.3. Investment Case: Risk and Return

- 13.4. RNA Therapeutics and RNA Vaccines: Funding and Investment Analysis

- 13.4.1. Analysis by Year of Funding

- 13.4.2. Analysis by Type of Funding

- 13.4.3. Analysis by Year and Type of Funding

- 13.4.4. Analysis of Amount Invested by Year of Funding

- 13.4.5. Analysis of Amount Invested by Type of Funding

- 13.4.6. Analysis by Geography

- 13.4.7. Analysis by Type of Molecule

- 13.4.8. Analysis by Purpose of Funding

- 13.4.9. Analysis by Stage of Development

- 13.4.10. Analysis by Therapeutic Area

- 13.4.11. Most Active Players: Analysis by Number of Funding Instances

- 13.4.12. Most Active Players: Analysis by Amount Invested

- 13.4.13. Most Active Investors: Analysis by Number of Funding Instances

- 13.5. Evolution and Relative Assessment of Funding Models

- 13.6. Summary of Funding and Investment Opportunities

14. BIG PHARMA INITIATIVES

- 14.1. Analysis Methodology

- 14.2. RNA Therapeutics and RNA Vaccines: Big Pharma Initiatives

- 14.2.1. Most Active Players: Analysis by Number of Big Pharma Initiatives

- 14.2.2. Analysis by Year of Initiative

- 14.2.3. Analysis by Type of Initiative

- 14.2.4. Analysis by Focus Area of Initiative

- 14.2.5. Analysis by Purpose of Initiative

- 14.2.6. Analysis by Type of Molecule

- 14.2.7. Analysis by Therapeutic Area

- 14.2.8. Analysis by Location of Headquarters

15. GLOBAL NEXT GENERATION RNA THERAPEUTICS MARKET

- 15.1. Forecast Model

- 15.2. Key Assumptions

- 15.3. Forecast Methodology

- 15.4. Global Next Generation RNA Therapeutics Market: Forecasted Estimates (till 2035)

- 15.4.1. Scenario Analysis

- 15.4.1.1. Conservative Scenario

- 15.4.1.2. Optimistic Scenario

- 15.4.1. Scenario Analysis

- 15.5. Key Market Segmentations

16. NEXT GENERATION RNA THERAPEUTICS MARKET, BY TYPE OF MODALITY

- 16.1. Next Generation RNA Therapeutics Market: Distribution by Type of Modality

- 16.1.1. Next Generation RNA Therapeutics Market for Therapeutics: Forecasted Estimates (till 2035)

- 16.1.2. Next Generation RNA Therapeutics Market for Vaccines: Forecasted Estimates (till 2035)

17. NEXT GENERATION RNA THERAPEUTICS MARKET, BY TYPE OF MOLECULE

- 17.1. Next Generation RNA Therapeutics Market: Distribution by Type of Molecule

- 17.1.1. Next Generation RNA Therapeutics Market for sacRNA: Forecasted Estimates (till 2035)

- 17.1.2. Next Generation RNA Therapeutics Market for saRNA: Forecasted Estimates (till 2035)

- 17.1.3. Next Generation RNA Therapeutics Market for circRNA: Forecasted Estimates (till 2035)

18. NEXT GENERATION RNA THERAPEUTICS MARKET, BY TARGET INDICATION

- 18.1. Next Generation RNA Therapeutics Market: Distribution by Target Indication

- 18.1.1. Next Generation RNA Therapeutics Market for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 18.1.2. Next Generation RNA Therapeutics Market for Seasonal Influenza: Forecasted Estimates (till 2035)

- 18.1.3. Next Generation RNA Therapeutics Market for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 18.1.4. Next Generation RNA Therapeutics Market for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 18.1.5. Next Generation RNA Therapeutics Market for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

19. NEXT GENERATION RNA THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION

- 19.1. Next Generation RNA Therapeutics Market: Distribution by Route of Administration

- 19.1.1. Next Generation RNA Therapeutics Market for Intravenous Route: Forecasted Estimates (till 2035)

- 19.1.2. Next Generation RNA Therapeutics Market for Intramuscular Route: Forecasted Estimates (till 2035)

- 19.1.3. Next Generation RNA Therapeutics Market for Intratumoral Route: Forecasted Estimates (till 2035)

- 19.1.4. Next Generation RNA Therapeutics Market for Intraductal Route: Forecasted Estimates (till 2035)

20. NEXT GENERATION RNA THERAPEUTICS MARKET, BY GEOGRAPHICAL REGIONS

- 20.1. Next Generation RNA Therapeutics Market: Distribution by Geographical Regions

- 20.1.1. Next Generation RNA Therapeutics Market in North America: Forecasted Estimates (till 2035)

- 20.1.1.1. Next Generation RNA Therapeutics Market in the US: Forecasted Estimates (till 2035)

- 20.1.2. Next Generation RNA Therapeutics Market in Europe: Forecasted Estimates (till 2035)

- 20.1.2.1. Next Generation RNA Therapeutics Market in the UK: Forecasted Estimates (till 2035)

- 20.1.2.2. Next Generation RNA Therapeutics Market in Germany: Forecasted Estimates (till 2035)

- 20.1.2.3. Next Generation RNA Therapeutics Market in France: Forecasted Estimates (till 2035)

- 20.1.2.4. Next Generation RNA Therapeutics Market in Italy: Forecasted Estimates (till 2035)

- 20.1.2.5. Next Generation RNA Therapeutics Market in Spain: Forecasted Estimates (till 2035)

- 20.1.2.6. Next Generation RNA Therapeutics Market in Rest of Europe: Forecasted Estimates (till 2035)

- 20.1.3. Next Generation RNA Therapeutics Market in Asia-Pacific: Forecasted Estimates (till 2035)

- 20.1.3.1. Next Generation RNA Therapeutics Market in Singapore: Forecasted Estimates (till 2035)

- 20.1.1. Next Generation RNA Therapeutics Market in North America: Forecasted Estimates (till 2035)

21. NEXT GENERATION RNA THERAPEUTICS MARKET, BY LEADING PLAYERS

22. NEXT GENERATION RNA THERAPEUTICS MARKET, SALES FORECAST OF DRUGS

- 22.1. Next Generation RNA Therapeutics: Drug Sales Forecast

- 22.1.1. MTL-CEBPA

- 22.1.2. BNT 161 / PF-07926307

- 22.1.3. STX-001

- 22.1.4. RXRG001

- 22.1.5. EXG-34217

23. MARKET OPPORTUNITY ANALYSIS: NORTH AMERICA

- 23.1. Next Generation RNA Therapeutics Market in North America: Distribution by Type of Modality

- 23.1.1. Next Generation RNA Therapeutics Market in North America for Therapeutics: Forecasted Estimates (till 2035)

- 23.1.2. Next Generation RNA Therapeutics Market in North America for Vaccines: Forecasted Estimates (till 2035)

- 23.2. Next Generation RNA Therapeutics Market in North America: Distribution by Type of Molecule

- 23.2.1. Next Generation RNA Therapeutics Market in North America for sacRNA: Forecasted Estimates (till 2035)

- 23.2.2. Next Generation RNA Therapeutics Market in North America for saRNA: Forecasted Estimates (till 2035)

- 23.2.3. Next Generation RNA Therapeutics Market in North America for circRNA: Forecasted Estimates (till 2035)

- 23.3. Next Generation RNA Therapeutics Market in North America: Distribution by Target Indication

- 23.3.1. Next Generation RNA Therapeutics Market in North America for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 23.3.2. Next Generation RNA Therapeutics Market in North America for Seasonal Influenza: Forecasted Estimates (till 2035)

- 23.3.3. Next Generation RNA Therapeutics Market in North America for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 23.3.4. Next Generation RNA Therapeutics Market in North America for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 23.3.5. Next Generation RNA Therapeutics Market in North America for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

- 23.4. Next Generation RNA Therapeutics Market in North America: Distribution by Route of Administration

- 23.4.1. Next Generation RNA Therapeutics Market in North America for Intravenous Route: Forecasted Estimates (till 2035)

- 23.4.2. Next Generation RNA Therapeutics Market in North America for Intramuscular Route: Forecasted Estimates (till 2035)

- 23.4.3. Next Generation RNA Therapeutics Market in North America for Intratumoral Route: Forecasted Estimates (till 2035)

- 23.4.4. Next Generation RNA Therapeutics Market in North America for Intraductal Route: Forecasted Estimates (till 2035)

24. MARKET OPPORTUNITY ANALYSIS: EUROPE

- 24.1. Next Generation RNA Therapeutics Market in Europe: Distribution by Type of Modality

- 24.1.1. Next Generation RNA Therapeutics Market in Europe for Therapeutics: Forecasted Estimates (till 2035)

- 24.1.2. Next Generation RNA Therapeutics Market in Europe for Vaccines: Forecasted Estimates (till 2035)

- 24.2. Next Generation RNA Therapeutics Market in Europe: Distribution by Type of Molecule

- 24.2.1. Next Generation RNA Therapeutics Market in Europe for sacRNA: Forecasted Estimates (till 2035)

- 24.2.2. Next Generation RNA Therapeutics Market in Europe for saRNA: Forecasted Estimates (till 2035)

- 24.2.3. Next Generation RNA Therapeutics Market in Europe for circRNA: Forecasted Estimates (till 2035)

- 24.3. Next Generation RNA Therapeutics Market in Europe: Distribution by Target Indication

- 24.3.1. Next Generation RNA Therapeutics Market in Europe for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 24.3.2. Next Generation RNA Therapeutics Market in Europe for Seasonal Influenza: Forecasted Estimates (till 2035)

- 24.3.3. Next Generation RNA Therapeutics Market in Europe for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 24.3.4. Next Generation RNA Therapeutics Market in Europe for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 24.3.5. Next Generation RNA Therapeutics Market in Europe for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

- 24.4. Next Generation RNA Therapeutics Market in Europe: Distribution by Route of Administration

- 24.4.1. Next Generation RNA Therapeutics Market in Europe for Intravenous Route: Forecasted Estimates (till 2035)

- 24.4.2. Next Generation RNA Therapeutics Market in Europe for Intramuscular Route: Forecasted Estimates (till 2035)

- 24.4.3. Next Generation RNA Therapeutics Market in Europe for Intratumoral Route: Forecasted Estimates (till 2035)

- 24.4.4. Next Generation RNA Therapeutics Market in Europe for Intraductal Route: Forecasted Estimates (till 2035)

25. MARKET OPPORTUNITY ANALYSIS: ASIA-PACIFIC

- 25.1. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Type of Modality

- 25.1.1. Next Generation RNA Therapeutics Market in Asia-Pacific for Therapeutics: Forecasted Estimates (till 2035)

- 25.1.2. Next Generation RNA Therapeutics Market in Asia-Pacific for Vaccines: Forecasted Estimates (till 2035)

- 25.2. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Type of Molecule

- 25.2.1. Next Generation RNA Therapeutics Market in Asia-Pacific for sacRNA: Forecasted Estimates (till 2035)

- 25.2.2. Next Generation RNA Therapeutics Market in Asia-Pacific for saRNA: Forecasted Estimates (till 2035)

- 25.2.3. Next Generation RNA Therapeutics Market in Asia-Pacific for circRNA: Forecasted Estimates (till 2035)

- 25.3. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Target Indication

- 25.3.1. Next Generation RNA Therapeutics Market in Asia-Pacific for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 25.3.2. Next Generation RNA Therapeutics Market in Asia-Pacific for Seasonal Influenza: Forecasted Estimates (till 2035)

- 25.3.3. Next Generation RNA Therapeutics Market in Asia-Pacific for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 25.3.4. Next Generation RNA Therapeutics Market in Asia-Pacific for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 25.3.5. Next Generation RNA Therapeutics Market in Asia-Pacific for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

- 25.4. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Route of Administration

- 25.4.1. Next Generation RNA Therapeutics Market in Asia-Pacific for Intravenous Route: Forecasted Estimates (till 2035)

- 25.4.2. Next Generation RNA Therapeutics Market in Asia-Pacific for Intramuscular Route: Forecasted Estimates (till 2035)

- 25.4.3. Next Generation RNA Therapeutics Market in Asia-Pacific for Intratumoral Route: Forecasted Estimates (till 2035)

- 25.4.4. Next Generation RNA Therapeutics Market in Asia-Pacific for Intraductal Route: Forecasted Estimates (till 2035)

26. CONCLUDING INSIGHTS

27. APPENDIX I: TABULATED DATA

28. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 6.1 List of Next Generation RNA Therapeutics and RNA Vaccines

- Table 6.2 List of Clinical Stage Next Generation RNA Therapeutics and RNA Vaccines

- Table 6.3 List of Next Generation RNA Therapeutic and RNA Vaccine Developers

- Table 7.1 List of Next Generation RNA Technologies

- Table 7.2 List of Next Generation RNA Technology / Platform Developers

- Table 8.1 Gemcovac(R): Developer Overview

- Table 8.2 Gemcovac(R): Drug Overview

- Table 8.3 Gemcovac(R): Clinical Trial Information

- Table 8.4 Gemcovac(R): Clinical Trial Endpoints

- Table 8.5 Gemcovac(R): Clinical Trial Results

- Table 8.6 ATYR1923: Developer Overview

- Table 8.7 ATYR1923: Drug Overview

- Table 8.8 ATYR1923: Clinical Trial Information

- Table 8.9 ATYR1923: Clinical Trial Endpoints

- Table 8.10 ATYR1923: Clinical Trial Results

- Table 8.11 ARCT-154: Developer Overview

- Table 8.12 ARCT-154: Drug Overview

- Table 8.13 ARCT-154: Clinical Trial Information

- Table 8.14 ARCT-154: Clinical Trial Endpoints

- Table 8.15 ARCT-154: Clinical Trial Results

- Table 8.16 GRT-C901: Developer Overview

- Table 8.17 GRT-C901: Drug Overview

- Table 8.18 GRT-C901: Clinical Trial Information

- Table 8.19 GRT-C901: Clinical Trial Endpoints

- Table 8.20 GRT-C901: Clinical Trial Results

- Table 8.21 VLPCOV-01: Developer Overview

- Table 8.22 VLPCOV-01: Drug Overview

- Table 8.23 AVX-901: Developer Overview

- Table 8.24 AVX-901: Drug Overview

- Table 8.25 AVX-901: Clinical Trial Information

- Table 8.26 AVX-901: Clinical Trial Endpoints

- Table 8.27 AVX-901: Clinical Trial Results

- Table 8.28 MTL-CEBPA + Sorafenib: Developer Overview

- Table 8.29 MTL-CEBPA + Sorafenib: Drug Overview

- Table 8.30 MTL-CEBPA + Sorafenib: Clinical Trial Information

- Table 8.31 MTL-CEBPA + Sorafenib: Clinical Trial Endpoints

- Table 8.32 MTL-CEBPA + Sorafenib: Clinical Trial Results

- Table 8.33 SLATE: Developer Overview

- Table 8.34 SLATE: Drug Overview

- Table 8.35 SLATE: Clinical Trial Information

- Table 8.36 SLATE: Clinical Trial Endpoints

- Table 8.37 SLATE: Clinical Trial Results

- Table 9.1 RNA Therapeutics and RNA Vaccines: List of Clinical Trials

- Table 10.1 RNA Therapeutics and RNA Vaccines: List of Filed / Granted Patents, since 2019

- Table 11.1 RNA Therapeutics and RNA Vaccines: List of Partnerships and Collaborations, since 2019

- Table 12.1 RNA Therapeutics and RNA Vaccines: List of Funding and Investments, since 2019

- Table 13.1 RNA Therapeutics and RNA Vaccines: List of Big Pharma Initiatives, since 2019

- Table 14.1 Next Generation RNA Therapeutics Market :Expected Launch Year of Forecasted Drug Candidates

- Table 22.1 Next Generation RNA Therapies: Distribution by Type of Modality

- Table 22.2 Next Generation RNA Therapies: Distribution by Type of Molecule

- Table 22.3 Next Generation RNA Therapies: Distribution by Delivery Vehicle

- Table 22.4 Next Generation RNA Therapies: Distribution by Phase of Development

- Table 22.5 Next Generation RNA Therapies: Distribution by Therapeutic Area

- Table 22.6 Most Active Players: Distribution by Number of Therapies

- Table 22.7 Clinical Stage Therapies: Distribution by Phase of Development

- Table 22.8 Clinical Stage Therapies: Distribution by Route of Administration

- Table 22.9 Clinical Stage Therapies: Distribution by Therapeutic Area

- Table 22.10 Therapy Developer Landscape: Distribution by Year of Establishment

- Table 22.11 Therapy Developer Landscape: Distribution by Company Size

- Table 22.12 Therapy Developer Landscape: Distribution by Location of Headquarters

- Table 22.13 circRNA Therapies: Distribution by Phase of Development

- Table 22.14 circRNA Therapies: Distribution by Therapeutic Area

- Table 22.15 Most Active Players: Distribution by Number of circRNA Therapies

- Table 22.16 saRNA Therapies: Distribution by Phase of Development

- Table 22.17 saRNA Therapies: Distribution by Therapeutic Area

- Table 22.18 Most Active Players: Distribution by Number of saRNA Therapies

- Table 22.19 Next Generation RNA Technologies: Distribution by Class of Molecule

- Table 22.20 Next Generation RNA Technologies: Distribution by Type of Molecule

- Table 22.21 Next Generation RNA Technologies: Distribution by Capabilities of the Technology

- Table 22.22 Next Generation RNA Technologies: Distribution by Therapeutic Area

- Table 22.23 Next Generation RNA Technologies: Distribution by Highest Phase of Development

- Table 22.24 Technology Developer Landscape: Distribution by Year of Establishment

- Table 22.25 Technology Developer Landscape: Distribution by Company Size

- Table 22.26 Technology Developer Landscape: Distribution by Location of Headquarters

- Table 22.27 Technology Developer Landscape: Distribution by Operational Model

- Table 22.28 Gemcovac(R): Estimated Sales

- Table 22.29 ATYR1923: Estimated Sales

- Table 22.30 ARCT-154: Estimated Sales

- Table 22.31 GRT-C901: Estimated Sales

- Table 22.32 VLPCOV-01: Estimated Sales

- Table 22.33 AVX901: Estimated Sales

- Table 22.34 MTL-CEBPA + Sorafenib: Estimated Sales

- Table 22.35 SLATE: Estimated Sales

- Table 22.36 Clinical Trial Analysis: Cumulative Year-wise Trend

- Table 22.37 Clinical Trial Analysis: Distribution by Trial Status

- Table 22.38 Clinical Trial Analysis: Distribution by Trial Registration Year and Trial Status

- Table 22.39 Clinical Trial Analysis: Distribution by Trial Phase

- Table 22.40 Clinical Trial Analysis: Distribution by Patients Enrolled

- Table 22.41 Clinical Trial Analysis: Distribution by Type of Sponsor

- Table 22.42 Clinical Trial Analysis: Distribution by Therapeutic Area

- Table 22.43 Clinical Trial Analysis: Distribution by Study Design

- Table 22.44 Leading Organizations: Distribution by Number of Trials

- Table 22.45 Clinical Trial Analysis: Distribution by Focus Area

- Table 22.46 Clinical Trial Analysis: Distribution by Geography

- Table 22.47 Patent Analysis: Distribution by Type of Patent

- Table 22.48 Patent Analysis: Cumulative Year-wise Trend, since 2019

- Table 22.49 Patent Analysis: Distribution by Patent Jurisdiction

- Table 22.50 Patent Jurisdiction: North American Scenario

- Table 22.51 Patent Jurisdiction: European Scenario

- Table 22.52 Patent Jurisdiction: Asia-Pacific Scenario

- Table 22.53 Patent Analysis: Distribution by Patent Age

- Table 22.54 Patent Analysis: Distribution by CPC Symbols

- Table 22.55 Leading Industry Players: Distribution by Number of Patents

- Table 22.56 Leading Non-Industry Players: Distribution by Number of Patents

- Table 22.57 Patent Analysis: Distribution by Patent Characteristics

- Table 22.58 RNA Therapeutics and RNA Vaccines: Patent Valuation Analysis

- Table 22.59 Partnerships and Collaborations: Cumulative Year-wise Trend, since 2019

- Table 22.60 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 22.61 Partnerships and Collaborations: Distribution by Year and Type of Partnership, since 2019

- Table 22.62 Partnerships and Collaborations: Distribution by Year and Type of Molecule, since 2019

- Table 22.63 Partnerships and Collaborations: Distribution by Focus of Partnership

- Table 22.64 Partnerships and Collaborations: Distribution by Purpose of Partnership

- Table 22.65 Partnerships and Collaborations: Distribution by Therapeutic Area

- Table 22.66 Most Active Players: Distribution by Number of Partnerships

- Table 22.67 Partnerships and Collaborations: Local and International Deals

- Table 22.68 Partnerships and Collaborations: Intercontinental and Intracontinental Deals

- Table 22.69 Funding and Investment Analysis: Cumulative Year-wise Trend, since 2019

- Table 22.70 Funding and Investment Analysis: Distribution by Type of Funding

- Table 22.71 Funding and Investment Analysis: Distribution by Type of Molecule

- Table 22.72 Funding and Investment Analysis: Cumulative Amount Invested by Year, since 2019 (USD Million)

- Table 22.73 Funding and Investment Analysis: Distribution of Amount Invested by Type of Funding (USD Million)

- Table 22.74 Funding and Investment Analysis: Distribution of Amount Invested by Geography (USD Million)

- Table 22.75 Funding and Investment Analysis: Distribution by Year and Type of Funding, since 2019

- Table 22.76 Funding and Investment Analysis: Distribution by Purpose of Funding

- Table 22.77 Funding and Investment Analysis: Distribution by Stage of Development

- Table 22.78 Funding and Investment Analysis: Distribution by Therapeutic Area

- Table 22.79 Most Active Players: Distribution by Number of Funding Instances

- Table 22.80 Most Active Players: Distribution by Amount Invested (USD Million)

- Table 22.81 Leading Investors: Distribution by Number of Funding Instances

- Table 22.82 Big Pharma Initiatives: Distribution by Number of Initiatives

- Table 22.83 Big Pharma Initiatives: Cumulative Distribution by Year of Initiative, since 2019

- Table 22.84 Big Pharma Initiatives: Distribution by Type of Initiative

- Table 22.85 Big Pharma Initiatives: Cumulative Distribution by Purpose of Initiative

- Table 22.86 Big Pharma Initiatives: Cumulative Year-wise Trend, since 2019

- Table 22.87 Big Pharma Initiatives: Distribution by Focus of Initiative

- Table 22.88 Big Pharma Initiatives: Distribution by Location of Headquarters of Big Pharma Players

- Table 22.89 Global Next Generation RNA Therapeutics Market, Forecasted Estimates (till 2035), Base Scenario (USD Million)

- Table 22.90 Global Next Generation RNA Therapeutics Market, Forecasted Estimates (till 2035), Conservative Scenario (USD Million)

- Table 22.91 Global Next Generation RNA Therapeutics Market, Forecasted Estimates (till 2035), Optimistic Scenario (USD Million)

- Table 22.92 Global Next Generation RNA Therapeutics Market: Distribution by Type of Modality, 2023, 2028 and 2035 (USD Million)

- Table 22.93 Global RNA Therapeutics Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.94 Global RNA Vaccines Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.95 Global Next Generation RNA Therapeutics Market: Distribution by Type of Molecule, 2023, 2028 and 2035 (USD Million)

- Table 22.96 Global repRNA Therapeutics Vaccines Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.97 Global saRNA Therapeutics and Vaccines Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.98 Global sacRNA Therapeutics and Vaccines Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.99 Global sa-mRNA Therapeutics and Vaccines Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.100 Global tRNA Therapeutics and Vaccines Market, Forecasted Estimates (till 2035) (USD Million)

- Table 22.101 Global Next Generation RNA Therapeutics Market :Distribution by Therapeutic Area, 2023, 2028 and 2035 (USD Million)

- Table 22.102 Global Next Generation RNA Therapeutics Market for Infectious Diseases, Forecasted Estimates (till 2035) (USD Million)

- Table 22.103 Global Next Generation RNA Therapeutics Market for Oncological Disorders, Forecasted Estimates (till 2035) (USD Million)

- Table 22.104 Global Next Generation RNA Therapeutics Market for Pulmonary Disorders, Forecasted Estimates (till 2035) (USD Million)

- Table 22.105 Global Next Generation RNA Therapeutics Market: Distribution by Route of Administration, 2023, 2028 and 2035 (USD Million)

- Table 22.106 Global Next Generation RNA Therapeutics Market for Intradermal Therapeutics / Vaccines, Forecasted Estimates (till 2035) (USD Million)

- Table 22.107 Global Next Generation RNA Therapeutics Market forI ntramuscular Therapeutics / Vaccines, Forecasted Estimates (till 2035) (USD Million)

- Table 22.108 Global Next Generation RNA Therapeutics Market for Intravenous Therapeutics / Vaccines, Forecasted Estimates (till 2035) (USD Million)

- Table 22.109 Global Next Generation RNA Therapeutics Market: Distribution by Key Geographical Regions, 2023, 2028 and 2035 (USD Million)

- Table 22.110 Next Generation RNA Therapeutics Market in North America, Forecasted Estimates (till 2035) (USD Million)

- Table 22.111 Next Generation RNA Therapeutics Market in the US, Forecasted Estimates (till 2035) (USD Million)

- Table 22.112 Next Generation RNA Therapeutics Market in Europe, Forecasted Estimates (till 2035) (USD Million)

- Table 22.113 Next Generation RNA Therapeutics Market in France, Forecasted Estimates (till 2035) (USD Million)

- Table 22.114 Next Generation RNA Therapeutics Market in Italy, Forecasted Estimates (till 2035) (USD Million)

- Table 22.115 Next Generation RNA Therapeutics Market in Spain, Forecasted Estimates (till 2035) (USD Million)

- Table 22.116 Next Generation RNA Therapeutics Market in the UK, Forecasted Estimates (till 2035) (USD Million)

- Table 22.117 Next Generation RNA Therapeutics Market in the Netherlands, Forecasted Estimates (till 2035) (USD Million)

- Table 22.118 Next Generation RNA Therapeutics Market in Asia-Pacific, Forecasted Estimates (till 2035) (USD Million)

- Table 22.119 Next Generation RNA Therapeutics Market in India, Forecasted Estimates (till 2035) (USD Million)

- Table 22.120 Next Generation RNA Therapeutics Market in Japan, Forecasted Estimates (till 2035) (USD Million)

- Table 22.121 Next Generation RNA Therapeutics Market in Singapore, Forecasted Estimates (till 2035) (USD Million)

- Table 22.122 Global Next Generation RNA Therapeutics Market: Distribution by Leading Players (USD Million)

List of Figures

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Data Sources for Secondary Research

- Figure 2.3 Research Methodology: Robust Quality Control

- Figure 3.1 Market Dynamics: Forecast Methodology

- Figure 3.2 Market Dynamics: Market Assessment Framework

- Figure 4.1 Lessons Learnt from Past Recessions

- Figure 5.1 Executive Summary: Market Landscape

- Figure 5.2 Executive Summary: Market Trends

- Figure 5.3 Executive Summary: Market Forecast and Opportunity Analysis

- Figure 6.1 Evolution of Next Generation RNA Therapeutics and Vaccines

- Figure 6.2 Key Aspects of Next Generation RNA Molecules

- Figure 6.3 Key Challenges Associated with Traditional RNA Modalities

- Figure 6.4 Advantages of Using Next Generation RNA Modalities

- Figure 7.1 Next Generation RNA Therapies: Distribution by Type of Modality

- Figure 7.2 Next Generation RNA Therapies: Distribution by Type of Molecule

- Figure 7.3 Next Generation RNA Therapies: Distribution by Delivery Vehicle

- Figure 7.4 Next Generation RNA Therapies: Distribution by Stage of Development

- Figure 7.5 Next Generation RNA Therapies: Distribution by Therapeutic Area

- Figure 7.6 Most Active Players: Distribution by Number of Therapies

- Figure 7.7 Clinical Stage Therapies: Distribution by Phase of Development

- Figure 7.8 Clinical Stage Therapies: Distribution by Route of Administration

- Figure 7.9 Clinical Stage Therapies: Distribution by Therapeutic Area

- Figure 7.10 Therapy Developers Landscape: Distribution by Year of Establishment

- Figure 7.11 Therapy Developers Landscape: Distribution by Company Size

- Figure 7.12 Therapy Developers Landscape: Distribution by Location of Headquarters

- Figure 7.13 saRNA Therapies: Distribution by Phase of Development

- Figure 7.14 saRNA Therapies: Distribution by Therapeutic Area

- Figure 7.15 Most Active Players: Distribution by Number of saRNA Therapies

- Figure 7.16 circRNA Therapies: Distribution by Phase of Development

- Figure 7.17 circRNA Therapies: Distribution by Therapeutic Area

- Figure 7.18 Most Active Players: Distribution by Number of circRNA Therapies

- Figure 8.1 Next Generation RNA Technologies: Distribution by Class of Molecule

- Figure 8.2 Next Generation RNA Technologies: Distribution by Type of Molecule

- Figure 8.3 Next Generation RNA Technologies: Distribution by Capabilities of the Technology

- Figure 8.4 Next Generation RNA Technologies: Distribution by Therapeutic Area

- Figure 8.5 Next Generation RNA Technologies: Distribution by Highest Stage of Development

- Figure 8.6 Next Generation RNA Technologies: Distribution by Class of Molecule and Therapeutic Area

- Figure 8.7 Next Generation RNA Technologies: Distribution by Class of Molecule and Highest Stage of Development

- Figure 8.8 Next Generation RNA Technologies: Distribution by Type of Molecule and Capabilities of the Technology

- Figure 8.9 Technology Developer Landscape: Distribution by Year of Establishment

- Figure 8.10 Technology Developer Landscape: Distribution by Company Size

- Figure 8.11 Technology Developer Landscape: Distribution by Location of Headquarters

- Figure 8.12 Technology Developer Landscape: Distribution by Operational Model

- Figure 9.1 BNT161: Estimated Sales

- Figure 9.2 MTL-CEBPA: Estimated Sales

- Figure 10.1 Clinical Trial Analysis: Distribution by Trial Registration Year

- Figure 10.2 Clinical Trial Analysis: Distribution by Trial Status

- Figure 10.3 Clinical Trial Analysis: Distribution by Trial Registration Year and Trial Status

- Figure 10.4 Clinical Trial Analysis: Distribution by Trial Phase

- Figure 10.5 Clinical Trial Analysis: Distribution of Patients Enrolled by Trial Phase

- Figure 10.6 Clinical Trial Analysis: Distribution of Patients Enrolled by Trial Registration Year

- Figure 10.7 Clinical Trial Analysis: Distribution by Study Design

- Figure 10.8 Clinical Trial Analysis: Distribution by Target Patient Population

- Figure 10.9 Clinical Trial Analysis: Distribution by Patient Gender

- Figure 10.10 Clinical Trial Analysis: Distribution by Type of Sponsor / Collaborator

- Figure 10.11 Clinical Trial Analysis: Distribution by Therapeutic Area

- Figure 10.12 Clinical Trial Analysis: Most Active Players by Number of Trials

- Figure 10.13 Clinical Trial Analysis: Geographical Distribution of Trials and Number of Patients Enrolled

- Figure 10.14 Clinical Trial Analysis: North America: Key Insights

- Figure 10.15 Clinical Trial Analysis: Europe: Key Insights

- Figure 10.16 Clinical Trial Analysis: Asia-Pacific: Key Insights

- Figure 10.17 Clinical Trial Analysis: Rest of the World: Key Insights

- Figure 11.1 Patent Analysis: Distribution by Publication Year

- Figure 11.2 Patent Analysis: Distribution by Type of Patent

- Figure 11.3 Patent Analysis: Distribution of Granted Patents and Patent Applications by Publication Year

- Figure 11.4 Patent Analysis: Cumulative Year-wise Distribution by Type of Applicant

- Figure 11.5 Patent Analysis: Distribution by Application Year

- Figure 11.6 Patent Analysis: Distribution by Patent Jurisdiction (Region)

- Figure 11.7 Patent Analysis: Distribution by Patent Jurisdiction (Country)

- Figure 11.8 Patent Analysis: Distribution by Patent Age

- Figure 11.9 Leading Industry Players: Analysis by Number of Patents

- Figure 11.10 Leading Non-Industry Players: Analysis by Number of Patents

- Figure 11.11 Leading Individual Assignees: Analysis by Number of Patents

- Figure 11.12 Patent Analysis: Distribution by CPC Symbols

- Figure 11.13 Patent Benchmarking: Distribution of Patent Characteristics (CPC Codes) by Leading Industry Players

- Figure 11.14 Patent Benchmarking: Distribution of Leading Industry Players by Patent Characteristics (CPC Codes)

- Figure 11.15 Patent Valuation

- Figure 12.1 Partnerships and Collaborations: Cumulative Year-wise Trend

- Figure 12.2 Partnerships and Collaborations: Distribution by Type of Partnership

- Figure 12.3 Partnerships and Collaborations: Distribution by Year and Type of Partnership

- Figure 12.4 Partnerships and Collaborations: Distribution by Year of Partnership and Type of Molecule

- Figure 12.5 Partnerships and Collaborations: Distribution by Purpose of Partnership

- Figure 12.6 Partnerships and Collaborations: Distribution by Focus Area of Partnership

- Figure 12.7 Partnerships and Collaborations: Distribution by Therapeutic Area

- Figure 12.8 Most Active Players: Distribution by Number of Partnerships

- Figure 12.9 Partnerships and Collaborations: Local and International Deals

- Figure 12.10 Partnerships and Collaborations: Intercontinental and Intracontinental Deals

- Figure 13.1 Funding and Investment Analysis: Cumulative Year-wise Trend

- Figure 13.2 Funding and Investment Analysis: Distribution by Type of Funding

- Figure 13.3 Funding and Investment Analysis: Distribution by Year and Type of Funding

- Figure 13.4 Funding and Investment Analysis: Distribution of Cumulative Amount Invested by Year (USD Million)

- Figure 13.5 Funding and Investment Analysis: Distribution of Amount Invested by Type of Funding (USD Million)

- Figure 13.6 Funding and Investment Analysis: Distribution by Geography

- Figure 13.7 Funding and Investment Analysis: Distribution by Type of Molecule

- Figure 13.8 Funding and Investment Analysis: Distribution by Purpose of Funding

- Figure 13.9 Funding and Investment Analysis: Distribution by Stage of Development

- Figure 13.10 Funding and Investment Analysis: Distribution by Therapeutic Area

- Figure 13.11 Most Active Players: Analysis by Number of Funding Instances

- Figure 13.12 Most Active Players: Analysis by Amount Invested (USD Million)

- Figure 13.13 Most Active Investors: Analysis by Number of Funding Instances

- Figure 14.1 Most Active Players by Number of Big Pharma Initiatives

- Figure 14.2 Big Player Initiatives: Distribution by Year of Initiative

- Figure 14.3 Big Player Initiatives: Distribution by Type of Initiative

- Figure 14.4 Big Player Initiatives: Distribution by Focus Area of Initiative

- Figure 14.5 Big Player Initiatives: Distribution by Purpose of Initiative

- Figure 14.6 Big Player Initiatives: Distribution by Type of Molecule

- Figure 14.7 Big Player Initiatives: Distribution by Therapeutic Area

- Figure 14.8 Big Player Initiatives: Distribution by Therapeutic Area

- Figure 14.9 Big Player Initiatives: Distribution by Location of Headquarters

- Figure 15.1 Global Next Generation RNA Therapeutics Market, Forecasted Estimates (till 2035): Base Scenario

- Figure 15.2 Global Next Generation RNA Therapeutics Market, Forecasted Estimates (till 2035): Conservative Scenario

- Figure 15.3 Global Next Generation RNA Therapeutics Market, Forecasted Estimates (till 2035): Optimistic Scenario

- Figure 16.1 Next Generation RNA Therapeutics Market: Distribution by Type of Modality

- Figure 16.2 Next Generation RNA Therapeutics Market for Therapeutics, Forecasted Estimates (till 2035)

- Figure 16.3 Next Generation RNA Therapeutics Market for Vaccines, Forecasted Estimates (till 2035)

- Figure 17.1 Next Generation RNA Therapeutics Market: Distribution by Type of Molecule

- Figure 17.2 Next Generation RNA Therapeutics Market for sacRNA, Forecasted Estimates (till 2035)

- Figure 17.3 Next Generation RNA Therapeutics Market for saRNA, Forecasted Estimates (till 2035)

- Figure 17.4 Next Generation RNA Therapeutics Market for circRNA, Forecasted Estimates (till 2035)

- Figure 18.1 Next Generation RNA Therapeutics Market: Distribution by Target Indication

- Figure 18.2 Next Generation RNA Therapeutics Market for Hepatocellular Carcinoma, Forecasted Estimates (till 2035)

- Figure 18.3 Next Generation RNA Therapeutics Market for Seasonal Influenza, Forecasted Estimates (till 2035)

- Figure 18.4 Next Generation RNA Therapeutics Market for Advanced Solid Tumors, Forecasted Estimates (till 2035)

- Figure 18.5 Next Generation RNA Therapeutics Market for Radiation-Induced Xerostomia and Hyposalivation, Forecasted Estimates (till 2035)

- Figure 18.6 Next Generation RNA Therapeutics Market for Inherited Bone Marrow Failure Syndromes, Forecasted Estimates (till 2035)

- Figure 19.1 Next Generation RNA Therapeutics Market: Distribution by Route of Administration

- Figure 19.2 Next Generation RNA Therapeutics Market for Intravenous Route, Forecasted Estimates (till 2035)

- Figure 19.3 Next Generation RNA Therapeutics Market for Intramuscular Route, Forecasted Estimates (till 2035)

- Figure 19.4 Next Generation RNA Therapeutics Market for Intratumoral Route, Forecasted Estimates (till 2035)

- Figure 19.5 Next Generation RNA Therapeutics Market for Intraductal Route, Forecasted Estimates (till 2035)

- Figure 20.1 Next Generation RNA Therapeutics Market: Distribution by Geographical Region

- Figure 20.2 Next Generation RNA Therapeutics Market in North America, Forecasted Estimates (till 2035)

- Figure 20.3 Next Generation RNA Therapeutics Market in the US, Forecasted Estimates (till 2035)

- Figure 20.4 Next Generation RNA Therapeutics Market in Europe, Forecasted Estimates (till 2035)

- Figure 20.5 Next Generation RNA Therapeutics Market in the UK, Forecasted Estimates (till 2035)

- Figure 20.6 Next Generation RNA Therapeutics Market in Germany, Forecasted Estimates (till 2035)

- Figure 20.7 Next Generation RNA Therapeutics Market in France, Forecasted Estimates (till 2035)

- Figure 20.8 Next Generation RNA Therapeutics Market in Italy, Forecasted Estimates (till 2035)

- Figure 20.9 Next Generation RNA Therapeutics Market in Spain, Forecasted Estimates (till 2035)

- Figure 20.10 Next Generation RNA Therapeutics Market in Rest of Europe, Forecasted Estimates (till 2035)

- Figure 20.11 Next Generation RNA Therapeutics Market in Asia-Pacific, Forecasted Estimates (till 2035)

- Figure 20.12 Next Generation RNA Therapeutics Market in Singapore, Forecasted Estimates (till 2035)

- Figure 21.1 Next Generation RNA Therapeutics Market: Distribution by Distribution by Leading Players, 2032 (based on revenues generated)

- Figure 21.2 Next Generation RNA Therapeutics Market: Distribution by Distribution by Leading Players, 2035 (based on revenues generated)

- Figure 22.1 Next Generation RNA Therapeutics Market: Sales Forecast for MTL-CEBPA, Forecasted Estimates (till 2035) (USD Million)

- Figure 22.2 Next Generation RNA Therapeutics Market: Sales Forecast for BNT 161, Forecasted Estimates (till 2035) (USD Million)

- Figure 22.3 Next Generation RNA Therapeutics Market: Sales Forecast for STX-001, Forecasted Estimates (till 2035) (USD Million)

- Figure 22.4 Next Generation RNA Therapeutics Market: Sales Forecast for RXRG001, Forecasted Estimates (till 2035) (USD Million)

- Figure 22.5 Next Generation RNA Therapeutics Market: Sales Forecast for EXG-34217, Forecasted Estimates (till 2035) (USD Million)

mRNA治療市場預測——全球按治療方法、mRNA構建體、遞送系統、應用、最終用戶、分銷管道和地區分類的分析——2034年

mRNA治療市場預測——全球按治療方法、mRNA構建體、遞送系統、應用、最終用戶、分銷管道和地區分類的分析——2034年 mRNA治療市場:依技術平台、遞送方式及治療應用分類-2026-2032年全球市場預測mRNA平台市場:依產品類型、治療領域、給藥途徑及最終用戶分類-2026-2032年全球市場預測

mRNA治療市場:依技術平台、遞送方式及治療應用分類-2026-2032年全球市場預測mRNA平台市場:依產品類型、治療領域、給藥途徑及最終用戶分類-2026-2032年全球市場預測 mRNA療法市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測全球mRNA治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

mRNA療法市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測全球mRNA治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年) mRNA平台市場 - 全球產業規模、佔有率、趨勢、機會及預測(按適應症、易用性、mRNA類型、最終用戶、地區和競爭格局分類,2021-2031年)mRNA治療藥物合約開發和生產市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、適應症、最終用戶、地區和競爭格局分類,2021-2031年)甲基假尿苷三磷酸溶液市場按技術、等級、應用、最終用戶和分銷管道分類-2026-2032年全球預測

mRNA平台市場 - 全球產業規模、佔有率、趨勢、機會及預測(按適應症、易用性、mRNA類型、最終用戶、地區和競爭格局分類,2021-2031年)mRNA治療藥物合約開發和生產市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、適應症、最終用戶、地區和競爭格局分類,2021-2031年)甲基假尿苷三磷酸溶液市場按技術、等級、應用、最終用戶和分銷管道分類-2026-2032年全球預測 mRNA療法市場規模、佔有率和成長分析(按類型、應用、最終用戶和地區分類)—2026-2033年產業預測

mRNA療法市場規模、佔有率和成長分析(按類型、應用、最終用戶和地區分類)—2026-2033年產業預測 mRNA療法市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

mRNA療法市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)