|

市場調查報告書

商品編碼

2028469

全球層析法市場(第二版):產業趨勢及2035年全球預測-依層析法產品類型、層析法設備、液相層析法、層析法組件、最終用戶及地區分類Chromatography Market (2nd Edition): Industry Trends and Global Forecasts, till 2035 - Distribution by Type of Chromatography Product, Chromatography Instrument, Liquid Chromatography, Chromatography Component, End User and Geographical Regions |

||||||

層析法市場概覽

預計到2035年,全球層析法市場將以 6.53%的年複合成長率成長,達到 223.5億美元,高於目前的126.5億美元。

層析法市場:成長與趨勢

層析法是一種廣泛用於分離、鑑定和純化複雜混合物的分析技術。自20世紀初Mikhail Zvett發明以來,該技術取得了顯著進步,其準確性、效率和適用性均已顯著提高。層析法的基本原理是利用分析物在流動相(液體或氣體)和固定相(固體或液體)之間分配的差異,實現組分的有效分離。

目前,層析法已廣泛應用於包括製藥、生物技術、化學、食品和石油化學公司在內的眾多產業。尤其是在製藥業,對用於複雜樣品定性和定量分析的層析法系統的需求顯著成長。該成長主要源於層析法在諸如大規模轉化研究、精準腫瘤學、病毒學和疫苗研發等領域的日益廣泛的應用。

此外,層析法可望在法醫學、臨床診斷和新藥研發等新興領域發揮日益重要的作用。持續的技術進步可望進一步拓展層析法系統和儀器的應用範圍和效能,以促進創新,加速各行各業的研發進程。

成長要素:市場擴張的策略促進因素

層析法市場的發展主要得益於層析法技術的不斷進步,包括先進檢測系統、人工智慧和小型化平台的整合。這些技術顯著拓展了層析法產業在科研和工業領域的應用範圍。連續層析法系統的出現實現了自動化、高通量分離,進一步提高了操作效率,提高了製程生產率並降低了整體成本。此外,隨著傳統層析法方法帶來的環境問題日益突出,綠色溶劑和超臨界流體等永續替代技術的應用加速推進。這些創新正成為推動市場成長要素。

市場挑戰:阻礙進展的主要障礙

儘管層析法具有諸多優勢,但它也面臨著可能阻礙其廣泛應用的重大挑戰。其中一個主要問題是,其他分離技術,例如結晶、超過濾超濾和高壓複性等,由於處理速度更快、通量更高,對色譜法的競爭日益激烈。

液相層析法質譜聯用(LC-MS)和氣相層析法質譜聯用(GC-MS)等先進層析法技術以及混合技術,都需要專業的知識與技能。此外,現場支援對於方法開發、樣品製備和資料分析等關鍵任務非常重要。熟練人員和技術基礎設施的匱乏是這些先進系統運作和維護所必需的,也是其進一步拓展市場的主要障礙。

層析法市場:關鍵洞察

本報告詳細分析了層析法市場的現狀,並指出了該行業的潛在成長機會。報告的主要發現包括:

- 目前,約有 90 家公司聲稱提供層析法設備,用於檢測、分離和純化各種應用領域的各種分析物。

- 70%的公司提供液相層析法設備,用於分離各種化合物,從小型有機分子到大型生物大分子。

- 目前,約有 95 家公司向各行各業供應各種層析法耗材,包括層析法樹脂、色譜柱、色譜介質和色譜膜。

- 層析法領域的相關人員提供各種用於複雜物質定性和定量分析的耗材,其中超過 75%的公司提供固相膜。

- 層析法領域公佈的專利中約有 60%是專利申請,其中大部分(33%)是在過去一年中公佈的。

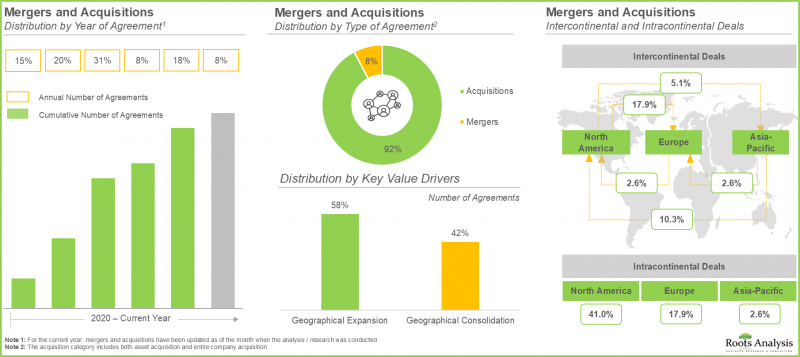

- 為了滿足日益成長的需求,層析法耗材和設備供應商正積極拓展產品系列。尤其值得一提的是,自2020年以來,該產業併購已顯著增加。

- 層析法技術的不斷進步已證明有助於滿足各行各業的分析需求,並預計未來層析法市場將穩步成長。

- 受對複雜分子高效檢測、分離和純化需求不斷成長的推動,層析法設備和耗材市場預計在未來十年將以 6.53%的年複合成長率成長。

- 預計市場機會將均勻分佈在各個細分市場,其中預注管柱市場預計將在預測期內經歷快速成長。

- 受主要企業在層析法設備和耗材方面快速技術進步的推動,層析法市場預計將以 5.70%的年複合成長率成長。

層析法市場

市場規模和機會分析是根據以下參數進行細分的:

依層析法產品類型

- 裝置

- 消耗品

- 其他產品

依層析法設備類型

- 液相層析法儀

- 氣相層析法儀

- 其他層析法設備

依液相層析法類型

- 高效液相層析(HPLC)

- 超高效液相層析(UHPLC)

- 尺寸排阻層析法

- 快速層析法

- 其他方法

依層析法組件類型

- 固定相

- 流動相

依固定相類型

- 預注管柱

- 瓶子/散裝樹脂

- 其他型式

最終用戶

- 製藥和生物技術產業

- 學術和研究機構

- 其他

依地區

- 北美洲

- 北美洲

- 亞太地區

- 拉丁美洲

- 中東和北非

層析法市場:主要細分市場

依產品類型分類的層析法市場佔有率分析 - 設備細分市場驅動層析法市場

全球層析法市場分為儀器、耗材和其他產品三大類。目前,儀器類產品約佔整個市場的70%,這主要歸功於層析法系統在複雜混合物的分離、純化和鑑定方面的廣泛應用。分析研究的不斷進步以及對能夠提供定性和定量分析結果的高性能儀器的需求日益成長,進一步鞏固了儀器類產品的市場主導地位。

依類型分類的層析法設備市場佔有率:液相層析法佔據市場主導地位。

液相層析法設備佔據了整個市場超過65%的佔有率。其主導地位源自於其在分離複雜混合物方面的高效性,尤其擅長分離極性強、熱不穩定的化合物,而這些化合物難以使用氣相層析法等其他方法進行分析。同時,受其成本效益和易操作性的推動,預計氣相層析法產業在預測期內將以7.6%的較高年複合成長率成長。

依類型分類的液相層析法市場佔有率:UHPLC 呈現強勁成長。

在液相層析法領域,市場主要包括高效液相層析(HPLC)、超高效液相層析(UHPLC)、尺寸排除層析法、快速層析法等技術。其中,HPLC約佔66%的市場佔有率,這主要歸功於其在製藥和生物技術領域的關鍵作用,因為這些領域對高精度和法規遵從性要求極高。然而,UHPLC市場預計將以7.3%的較高複合層析法成長,這得益於其相比傳統色譜技術具有分析速度更快、解析度更高、靈敏度更高等優勢。

依層析法組分分類的市場佔有率:固定相組分是層析法市場的主要驅動力。

根據組成類型,層析法耗材市場可分為固定相和流動相。目前,固定相佔據市場主導地位,市場佔有率約為60%,在實現高效的分析物分離和純化方面發揮著非常重要的作用。其他促成因素包括高解析度、選擇性交互作用和成本效益。同時,流動相市場預計將以更高的年複合成長率(CAGR)成長,達到8.7%,這主要得益於溶劑配方方面的創新以及與液相色譜-質譜聯用(LC-MS)和氣相色譜-質譜聯用(GC-MS)等先進混合技術的整合。

依固定相形式分類的市場佔有率:預注管柱推動層析法市場發展。

預注管柱目前約佔市場佔有率的40%,預計在預測期內將以8.0%的年複合成長率成長。其廣泛應用主要得益於其高效的操作性能,無需人工裝填色譜柱,縮短了製備時間,提高了層析法工作流程的整體效率。

依終端用戶分類的市場佔有率:製藥和生物技術產業是層析法市場的主要驅動力。

製藥和生物技術產業在終端用戶領域佔據主導地位,約佔整個市場的75%。這主要是因為層析法在這些領域中對生物分子和化學物質的分離、鑑定和純化發揮非常重要的作用。

區域市場佔有率:亞太地區以更高的年複合成長率成長。

預計北美將繼續保持主導在層析法市場的領先地位,今年約佔全球市場佔有率的40%,並有望在可預見的未來保持這一主導地位。北美的主導地位得益於美國主要產業參與企業的強大實力,以及包括人工智慧驅動和小型化層析法系統在內的先進技術的快速應用。相較之下,亞太地區預計將呈現最高的成長率,在預測期內將達到6.8%的年複合成長率。該成長得益於經濟高效的層析法解決方案的普及,以及政府為加速生命科學領域分析技術創新所提供的支持。

層析法市場主要企業示例

- Agilent Technologies

- Bio-Rad Laboratories

- Gilson

- JASCO

- MilliporeSigma

- Revvity(Previously known as PerkinElmer)

- Sartorius

- Shimadzu Scientific Instruments

- Thermo Fisher Scientific

層析法市場:研究範圍

- 市場規模和機會分析 - 本報告詳細分析了醫療設備契約製造市場,重點關注以下關鍵市場細分:[A]層析法類型,[B]層析法設備類型,[C] 液相層析法類型,[D]層析法組件類型,[E] 固定相形式,[F] 最終用戶,以及 [G] 地區。

- 層析法設備供應商市場市場趨勢:除了對整個層析法設備供應商市場進行詳細評估外,本報告還包括有關幾個相關參數的資訊,例如 [A] 提供的層析法設備,[B] 提供的層析法耗材類型,[C] 應用領域,[D] 公司規模,[E] 成立年份,以及 [F] 總部所在地。

- 公司競爭分析 - 基於各種相關參數,對層析法耗材和層析法設備供應商進行詳細的競爭分析,包括 [A] 公司優勢和 [B] 產品組合優勢。

- 層析法耗材供應商市場趨勢:除了對層析法耗材供應商市場的市場趨勢進行詳細評估外,本報告還包括有關幾個相關參數的資訊,例如 [A] 提供的分離技術類型,[B] 提供的固相類型,[C] 分析物類型,[D] 公司規模,[E] 成立年份,以及 [F] 總部所在地。

- 公司簡介:詳細介紹總部位於北美、歐洲和亞太地區的主要企業。這些公司簡介基於多個參數,包括[A]成立年份、[B]總部所在地、[C]產品系列、[D]近期發展和[E]未來展望。

- 專利分析是根據以下關鍵參數進行的:[A] 專利類型,[B] 公開年份,[C] 申請年份,[D] 專利和專利申請數量,[E] 專利管轄區,[F] CPC 符號,[G] 專利年齡,[H] 申請人類型,以及 [I]個人專利持有人(就知識產權組合的規模而言)。

- 併購:根據相關參數對層析法行業的各種併購進行詳細分析,例如 [A] 合約年限,[B] 合約類型,[C] 地區,[D] 最活躍的參與者,[E] 所有權變更矩陣,[F] 關鍵價值促進因素,以及 [G] 交易倍數(銷售)。

- 市場影響分析 - 這是對可能影響市場成長的因素的詳細分析。它還包括對該行業關鍵促進因素、潛在限制、新興機會和現有挑戰的識別和分析。

目錄

第1章 序言

第2章 調查方法

第3章 經濟及其他專案特定考量因素

第4章 執行摘要

第5章 引言

- 章節概要

- 層析法概述

- 層析法原理

- 層析法類型

- 層析法的應用

- 未來展望

- 結論

第6章 層析法設備供應商市場趨勢

- 章節概要

- 層析法設備供應商:市場概況

第7章 層析法設備供應商:企業競爭力分析

- 章節概要

- 前提條件和關鍵參數

- 調查方法

- 層析法設備製造商:企業競爭力分析

第8章 層析法耗材供應商市場趨勢

- 章節概要

- 層析法耗材供應商:市場趨勢

第9章 公司簡介

- 章節概要

- Agilent Technologies

- Bio-Rad Laboratories

- PerkinElmer

- Sartorius

- Shimadzu

- Thermo Fisher Scientific

第10章 專利分析

- 章節概要

- 研究範圍和調查方法

- 層析法裝置及耗材:專利分析

- 層析法設備及耗材:專利基準分析

- 層析法裝置及耗材:專利評估

- 被引用次數最多的專利

第11章 併購

- 章節概要

- 併購模式

- 層析法設備及耗材:併購

第12章 市場影響分析 - 促進因素、阻礙因素、機會與挑戰

- 章節概要

- 市場促進因素

- 市場限制

- 市場機會

- 市場挑戰

- 結論

第13章 全球層析法市場

第14章 層析法市場:依產品類型分類

第16章 層析法市場:依耗材形式分類

第17章 層析法市場:依最終用戶分類

第18章 層析法市場:依地區分類

- 章節概要

- 關鍵假設和調查方法

- 北美:歷史趨勢(自2017年以來)和未來預測(至2035年)

- 歐洲:過去趨勢(自2017年以來)和未來預測(至2035年)

- 亞太地區:歷史趨勢(2017年至今)與未來預測(至2035年)

- 其他地區:歷史趨勢(自2017年以來)和未來預測(至2035年)

第19章 結論

第20章 高階主管洞見

第21章 附錄1:表格形式資料

第22章 附錄2:公司與組織列表

Chromatography Market: Overview

As per Roots Analysis, the global chromatography market is estimated to grow from USD 12.65 billion in the current year to USD 22.35 billion by 2035, at a CAGR of 6.53% during the forecast period, till 2035.

Chromatography Market: Growth and Trends

Chromatography is a widely adopted analytical technique used for the separation, identification, and purification of complex mixtures. Since its introduction by Mikhail Tsvet in the early 20th century, technology has undergone substantial advancements, enhancing its precision, efficiency, and applicability. The fundamental principle of chromatography is based on the differential distribution of analytes between a mobile phase (liquid or gas) and a stationary phase (solid or liquid), enabling effective component separation.

Currently, chromatography is extensively utilized across a broad spectrum of industries, including pharmaceuticals, biotechnology, chemicals, food, and petrochemicals. Notably, the pharmaceutical sector has witnessed a marked increase in demand for chromatography systems to support both qualitative and quantitative analysis of complex samples. This growth is primarily driven by the expanding application of chromatography in areas such as large-scale translational research, precision oncology, virology, and vaccine development.

Further, chromatography is expected to play an increasingly critical role in emerging domains such as forensic science, clinical diagnostics, and novel drug discovery. Continuous technological advancements are anticipated to further broaden the scope and capabilities of chromatography systems and instruments, thereby fostering innovation and accelerating research and development across multiple industries.

Growth Drivers: Strategic Enablers of Market Expansion

The chromatography market is propelled by ongoing advancements in chromatography technologies such as the integration of advanced detection systems, artificial intelligence, and miniaturized platforms. These technologies have significantly broadened the scope of applications across research and industrial domains within chromatography industry. The advent of continuous chromatography systems has further enhanced operational efficiency by enabling automated, high-throughput separations, thereby improving process productivity while reducing overall costs. Further, the increasing environmental concerns associated with conventional chromatography practices have accelerated the adoption of sustainable alternatives, including green solvents and supercritical fluids. These innovations are emerging as key growth drivers for the market.

Market Challenges: Critical Barriers Impeding Progress

Despite its numerous advantages, chromatography faces notable challenges that may hinder its widespread adoption. A primary concern is the growing competition from alternative separation technologies, including crystallization, high-resolution ultrafiltration, and high-pressure refolding which offer faster processing times and higher throughput capabilities.

Advanced and hyphenated chromatography techniques, including liquid chromatography-mass spectrometry (LC-MS) and gas chromatography-mass spectrometry (GC-MS), require specialized expertise. These methods also necessitate on-site support for key activities such as method development, sample preparation, and data interpretation. Furthermore, the limited availability of skilled personnel and technical infrastructure for the operation and maintenance of these advanced systems represents a key barrier to broader market penetration.

Chromatography Market: Key Insights

The report delves into the current state of the chromatography market and identifies potential growth opportunities within industry. Some key findings from the report include:

- Presently, close to 90 companies claim to offer chromatography instruments for the purpose of detection, separation and purification of different types of analytes across various application areas.

- 70% of the companies provide liquid chromatography instruments for the separation of a diverse range of compounds from small organic compounds to large biomacromolecules.

- Currently, around 95 companies offer different types of chromatography consumables, including chromatography resins, columns, media and membranes for a wide range of industries.

- Stakeholders engaged in the chromatography domain offer different types of consumables for qualitative and quantitative analysis of complex entities; more than 75% of the companies provide membranes as solid phases.

- Around 60% of the patents published in the chromatography domain are patent applications; notably, majority (33%) of the patents were published in the last year.

- To keep pace with the growing demand, chromatography consumables and instruments providers are actively expanding their product portfolio; notably the domain has witnessed notable mergers / acquisitions, since 2020.

- Ongoing advancements in chromatography techniques have proven useful in meeting the analytical demands across several industries; these are anticipated to drive the chromatography market at a steady pace in future.

- With growing demand for efficient detection, separation and purification of complex molecules, the market for chromatography instruments and consumables is likely to grow at a CAGR of 6.53% over the next decade.

- The projected opportunity is anticipated to be well distributed across different segments; prepacked columns segment is likely to grow at a faster pace during the forecasted period.

- Driven by the rapid technological advancements within chromatography instruments and consumables by prominent players in the US, the chromatography market is expected to grow at CAGR of 5.70%.

Chromatography Market

The market sizing and opportunity analysis has been segmented across the following parameters:

By Type of Chromatography Product

- Instruments

- Consumables

- Other Products

By Type of Chromatography Instrument

- Liquid Chromatography Instruments

- Gas Chromatography Instruments

- Other Chromatography Instruments

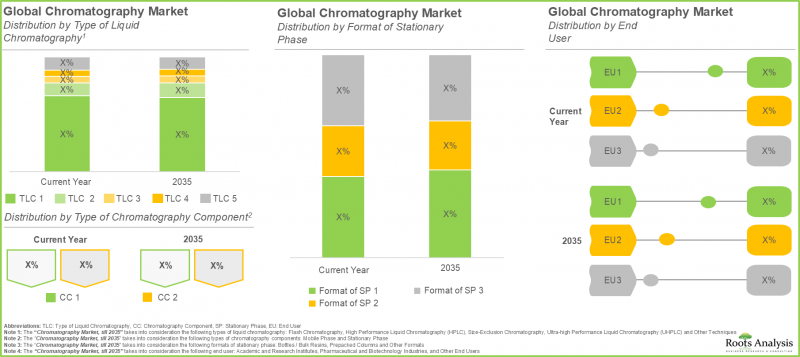

By Type of Liquid Chromatography

- High Performance Liquid Chromatography (HPLC)

- Ultra-high Performance Liquid Chromatography (UHPLC)

- Size-Exclusion Chromatography

- Flash Chromatography

- Other Techniques

By Type of Chromatography Component

- Stationary Phase

- Mobile Phase

By Format of Stationary Phase

- Prepacked Columns

- Bottles / Bulk Resins

- Other Formats

By End User

- Pharmaceutical and Biotechnology Industries

- Academic and Research Institutes

- Other End Users

By Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and North Africa

Chromatography Market: Key Segments

Market Share Analysis by Type of Chromatography Product: Instruments Segment Dominates the Chromatography Market

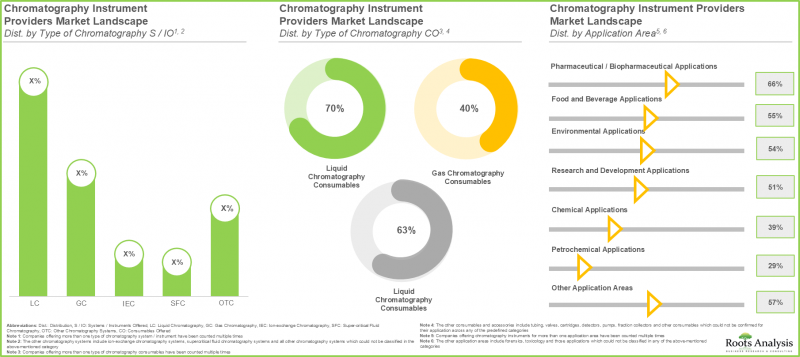

The global chromatography market is segmented into instruments, consumables, and other products. Currently, the instruments segment accounts for approximately 70% of the total market share, primarily driven by the extensive use of chromatography systems in the separation, purification, and identification of complex mixtures. This dominance is further supported by continuous advancements in analytical research and the growing demand for high-performance instrumentation capable of delivering both qualitative and quantitative insights.

Market Share by Type of Chromatography Instrument: Liquid Chromatography Leads the Market

Liquid chromatography instruments account for over 65% of the total market share. This dominance is driven by their effectiveness in separating complex mixtures, particularly polar and thermolabile compounds that are not easily analyzed using alternative methods such as gas chromatography. Meanwhile, the gas chromatography segment is anticipated to grow at a comparatively higher CAGR of 7.6% during the forecast period, driven by its cost-efficiency and ease of operation.

Market Share by Type of Liquid Chromatography: UHPLC to Exhibit Strong Growth

Within the liquid chromatography segment, the market comprises high-performance liquid chromatography (HPLC), ultra-high-performance liquid chromatography (UHPLC), size-exclusion chromatography, flash chromatography, and other techniques. Among these, HPLC holds the largest market share at approximately 66%, largely due to its critical role in pharmaceutical and biotechnology applications where high accuracy and regulatory compliance are essential. However, the UHPLC segment is expected to grow at a relatively higher CAGR of 7.3%, supported by its advantages in delivering faster analysis, enhanced resolution, and improved sensitivity compared to conventional chromatography techniques.

Market Share by Chromatography Component: Stationary Phase Segment Leads the Chromatography Market

Based on component type, the chromatography consumables market is categorized into stationary phase and mobile phase. The stationary phase segment currently dominates the market with a share of approximately 60%, owing to its pivotal role in achieving efficient analyte separation and purification. Additional contributing factors include high resolution, selective interactions, and cost-effectiveness. The mobile phase segment, however, is projected to grow at a higher CAGR of 8.7%, driven by innovations in solvent formulations and increasing integration with advanced hyphenated techniques such as LC-MS and GC-MS.

Market Share by Stationary Phase Format: Prepacked Columns at the Lead the Chromatography Market

Prepacked columns currently account for around 40% of the market share and are expected to grow at a CAGR of 8.0% over the forecast period. Their adoption is driven by operational efficiency, as they eliminate the need for manual column packing, thereby reducing preparation time and enhancing overall productivity in chromatographic workflows.

Market Share by End User: Pharmaceutical and Biotechnology Sectors Lead the Chromatography Market

The pharmaceutical and biotechnology industries dominate the end-user segment, contributing approximately 75% of the overall market share. This is primarily due to the critical role of chromatography in the separation, identification, and purification of biomolecules and chemical entities within these sectors.

Market Share by Geography: Asia-Pacific to Grow at a higher CAGR

North America is projected to maintain its leading position in the chromatography market, accounting for approximately 40% of the total share in the current year, with sustained dominance anticipated in the foreseeable future. This leadership is driven by the strong presence of key industry players in the United States, along with rapid adoption of advanced technologies, including AI-enabled and miniaturized chromatography systems. In contrast, the Asia-Pacific region is expected to register the highest growth rate, with a projected CAGR of 6.8% during the forecast period. This growth is supported by the availability of cost-effective chromatography solutions and favorable government initiatives aimed at promoting innovation in analytical technologies within the life sciences sector.

Example Players in Chromatography Market

- Agilent Technologies

- Bio-Rad Laboratories

- Gilson

- JASCO

- MilliporeSigma

- Revvity (Previously known as PerkinElmer)

- Sartorius

- Shimadzu Scientific Instruments

- Thermo Fisher Scientific

Chromatography Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the medical device contract manufacturing market, focusing on key market segments, including [A] type of chromatography [B] type of chromatography instrument, [C] type of liquid chromatography, [D] type of chromatography component, [E] format of stationary phase, [F] end user, and [G] geographical regions.

- Chromatography Instruments Providers Market Landscape: A detailed assessment of the overall chromatography instruments providers market landscape, along with information on several relevant parameters, such as [A] chromatography instruments offered, [B] type of chromatography consumables offered, [C] application area, [D] company size, [E] year of establishment and [F] location of headquarters.

- Company Competitiveness Analysis: An in-depth company competitiveness analysis of chromatography consumable and chromatography instrument providers based on various relevant parameters, such as [A] company strength, and [B] portfolio strength.

- Chromatography Consumables Providers Market Landscape: A detailed assessment of the overall chromatography consumables providers market landscape, along with information on several relevant parameters, such as [A] type of separation technique offered, [B] type of solid phase offered, [C] type of analyte, [D] company size, [E] year of establishment and [F] location of headquarters.

- Company Profiles: In-depth profiles of key companies based in North America, Europe and Asia-Pacific based on several parameters such as [A] year of establishment, [B] location of headquarters, [C] product portfolio, [D] recent developments and [E] an informed future outlook.

- Patent Analysis: A detailed analysis of the patents that have been filed / granted based on important parameters such as, [A] type of patent, [B] publication year, [C] application year, [D] number of granted patents and patent applications, [E] patent jurisdiction, [F] CPC symbols, [G] patent age, [H] type of applicant, and [I] individual patent assignees (in terms of size of intellectual property portfolio).

- Mergers and Acquisitions: A detailed analysis of various mergers and acquisitions of chromatography companies, based on several relevant parameters, such as [A] year of agreement, [B] type of agreement, [C] geography, [D] most active players, [E] ownership change matrix and [F] key value drivers and [G] deal multiples (based on revenues).

- Market Impact Analysis: An in-depth analysis of the factors that can impact the growth of the market. It also features identification and analysis of key drivers, potential restraints, emerging opportunities, and existing challenges in this domain.

Key Questions Answered in this Report

- Which are the leading companies in the chromatography market?

- Which region dominates the chromatography market?

- What are the key trends observed in the chromatography market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by chromatography instrument and consumable providers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complementary PPT Insights Pack

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Project Objectives

- 1.3. Scope of the Report

- 1.4. Inclusions and Exclusions

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Developers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. EXECUTIVE SUMMARY

5. INTRODUCTION

- 5.1. Chapter Overview

- 5.2. Overview of Chromatography

- 5.3. Principle of Chromatography

- 5.4. Types of Chromatography

- 5.5. Applications of Chromatography

- 5.6. Future Perspectives

- 5.7. Concluding Remarks

6. CHROMATOGRAPHY INSTRUMENTS PROVIDERS MARKET LANDSCAPE

- 6.1. Chapter Overview

- 6.2. Chromatography Instrument Providers: Overall Market Landscape

- 6.2.1. Analysis by Year of Establishment

- 6.2.2. Analysis by Company Size

- 6.2.3. Analysis by Location of Headquarters

- 6.2.4. Analysis by Company Size and Location of Headquarters

- 6.2.5. Analysis by Chromatography Instrument Offered

- 6.2.6. Analysis by Type of Mobile Phase Used

- 6.2.7. Analysis by Type of Chromatography Consumables Offered

- 6.2.8. Analysis by Scale of Operation

- 6.2.9. Analysis by Type of Industry Served

7. CHROMATOGRAPHY INSTRUMENTS PROVIDERS: COMPANY COMPETITIVENESS ANALYSIS

- 7.1. Chapter Overview

- 7.2. Assumptions and Key Parameters

- 7.3. Methodology

- 7.4. Chromatography Instrument Providers: Company Competitiveness Analysis

- 7.4.1. Small Companies Providing Chromatography Instruments

- 7.4.2. Mid-sized Companies Providing Chromatography Instruments

- 7.4.3. Large Companies Providing Chromatography Instruments

- 7.4.4. Very Large Companies Providing Chromatography Instruments

8. CHROMATOGRAPHY CONSUMABLES PROVIDERS MARKET LANDSCAPE

- 8.1. Chapter Overview

- 8.2. Chromatography Consumables Providers: Overall Market Landscape

- 8.2.1. Analysis by Year of Establishment

- 8.2.2. Analysis by Company Size

- 8.2.3. Analysis by Location of Headquarters

- 8.2.4. Analysis by Company Size and Location of Headquarters

- 8.2.5. Analysis by Type of Separation Technique Used

- 8.2.6. Analysis by Type of Solid Phase Offered

- 8.2.7. Analysis by Type of Consumable Format Offered

- 8.2.8. Analysis by Type of Analyte

- 8.2.9. Analysis by Application Area of Chromatography Consumables

9. COMPANY PROFILES

- 9.1. Chapter Overview

- 9.2. Agilent Technologies

- 9.2.1. Company Overview

- 9.2.2. Chromatography Product Portfolio

- 9.2.3. Recent Developments and Future Outlook

- 9.3. Bio-Rad Laboratories

- 9.3.1. Company Overview

- 9.3.2. Chromatography Product Portfolio

- 9.3.3. Recent Developments and Future Outlook

- 9.4. PerkinElmer

- 9.4.1. Company Overview

- 9.4.2. Chromatography Product Portfolio

- 9.4.3. Recent Developments and Future Outlook

- 9.5. Sartorius

- 9.5.1. Company Overview

- 9.5.2. Chromatography Product Portfolio

- 9.5.3. Recent Developments and Future Outlook

- 9.6. Shimadzu

- 9.6.1. Company Overview

- 9.6.2. Chromatography Product Portfolio

- 9.6.3. Recent Developments and Future Outlook

- 9.7. Thermo Fisher Scientific

- 9.7.1. Company Overview

- 9.7.2. Chromatography Product Portfolio

- 9.7.3. Recent Developments and Future Outlook

10. PATENT ANALYSIS

- 10.1. Chapter Overview

- 10.2. Scope and Methodology

- 10.3. Chromatography Instruments and Consumables: Patent Analysis

- 10.3.1. Analysis by Patent Publication Year

- 10.3.2. Analysis by Patent Application Year

- 10.3.3. Analysis of Granted Patents and Patent Applications by Publication Year

- 10.3.4. Analysis by Patent Jurisdiction

- 10.3.5. Analysis by CPC Symbols

- 10.3.6. Analysis by Type of Applicant

- 10.3.7. Leading Industry Players: Analysis by Number of Patents

- 10.3.8. Leading Non-Industry Players: Analysis by Number of Patents

- 10.3.9. Leading Individual Patent Assignees: Analysis by Number of Patents

- 10.4. Chromatography Instruments and Consumables: Patent Benchmarking Analysis

- 10.4.1. Analysis by Patent Characteristics

- 10.5. Chromatography Instruments and Consumables: Patent Valuation

- 10.6. Leading Patents by Number of Citations

11. MERGERS AND ACQUISITIONS

- 11.1. Chapter Overview

- 11.2. Merger and Acquisition Models

- 11.3. Chromatography Instruments and Consumables: Mergers and Acquisitions

- 11.3.1. Analysis by Type of Deal

- 11.3.2. Analysis by Year of Deal

- 11.3.3. Analysis by Company Ownership

- 11.3.4. Analysis by Geography

- 11.3.4.1. Intercontinental and Intracontinental Deals

- 11.3.4.2. Local and International Deals

- 11.3.5. Most Active Players: Analysis by Number of Mergers and Acquisitions

- 11.3.6. Analysis by Key Value Drivers

- 11.3.7. Key Acquisitions: Deal Multiples

12. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. GLOBAL CHROMATOGRAPHY MARKET

- 13.1. Chapter Overview

- 13.2. Assumptions and Methodology

- 13.3. Global Chromatography Market, Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 13.3.1. Scenario Analysis

- 13.4. Key Market Segmentations

- 13.5. Dynamic Dashboard

14. CHROMATOGRAPHY MARKET: DISTRIBUTION BY TYPE OF PRODUCT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Chromatography Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 14.4. Chromatography Consumables: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 14.5. Other Accessories: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 14.6. Data Triangulation

- 14.6.1. Insights from Primary Research

- 14.6.2. Insights from Secondary Research

- 14.6.3. Insights from In-house Repository

15. CHROMATOGRAPHY MARKET: DISTRIBUTION BY TYPE OF CHROMATOGRAPHY INSTRUMENT

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Liquid Chromatography Instrument: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 15.4. Gas Chromatography Instrument: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 15.5. Other Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 15.6. Data Triangulation

- 15.6.1. Insights based on Primary Research

- 15.6.2. Insights based on Secondary Research

- 15.6.3. Insights from In-house Repository

16. CHROMATOGRAPHY MARKET: DISTRIBUTION BY TYPE OF CONSUMABLE FORMAT OFFERED

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Pre-Packed Columns: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 16.4. Bottles / Bulk Resins: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 16.5. Other Formats: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 16.6. Data Triangulation

- 16.6.1. Insights based on Primary Research

- 16.6.2. Insights based on Secondary Research

- 16.6.3. Insights from In-house Repository

17. CHROMATOGRAPHY MARKET: DISTRIBUTION BY END USER

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Pharmaceutical and Biopharmaceutical Companies: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 17.4. Academic / Research Institutes: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 17.5. Other Industries: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 17.6. Data Triangulation

- 17.6.1. Insights based on Primary Research

- 17.6.2. Insights based on Secondary Research

- 17.6.3. Insights from In-house Repository

18. CHROMATOGRAPHY MARKET: DISTRIBUTION BY GEOGRAPHY

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. North America: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.3.1. Chromatography Market for Chromatography Instruments

- 18.3.2. Chromatography Market for Chromatography Consumables

- 18.3.3. Chromatography Market for Other Accessories

- 18.4. Europe: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.4.1. Chromatography Market for Chromatography Instruments

- 18.4.2. Chromatography Market for Chromatography Consumables

- 18.4.3. Chromatography Market for Other Accessories

- 18.5. Asia-Pacific: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.5.1. Chromatography Market for Chromatography Instruments

- 18.5.2. Chromatography Market for Chromatography Consumables

- 18.5.3. Chromatography Market for Other Accessories

- 18.6. Rest of the World: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.6.1. Chromatography Market for Chromatography Instruments

- 18.6.2. Chromatography Market for Chromatography Consumables

- 18.6.3. Chromatography Market for Other Accessories

- 18.7. Data Triangulation

- 18.7.1. Insights based on Primary Research

- 18.7.2. Insights based on Secondary Research

- 18.7.3. Insights from In-house Repository

19. CONCLUSION

20. EXECUTIVE INSIGHTS

21. APPENDIX 1: TABULATED DATA

22. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 6.1 Chromatography Instruments Providers: Information on Year of Establishment, Company Size, Location of Headquarters, Type of Chromatography Instrument Offered, Type of Mobile Phase Offered, and Type of Chromatography Consumable Offered

- Table 6.2 Chromatography Instruments Providers: Information on Scale of Operation and Type of Industry Served

- Table 8.1 Chromatography Consumables Providers: Information on Chromatography Consumables Providers and Type of Separation Technique Offered

- Table 8.2 Chromatography Consumables Providers: Information of Type of Separation Technique Offered, Type of Solid Phase Offered and Type of Format Offered

- Table 8.3 Chromatography Consumables Providers: Information of Type of Separation Technique Offered and Type of Analyte Separated

- Table 8.4 Chromatography Consumables Providers: Information of Type of Separation Technique Offered and Application Areas

- Table 9.1 Leading Chromatography Instruments and Consumables Providers

- Table 9.2 Agilent Technologies: Company Overview

- Table 9.3 Agilent Technologies: Chromatography Instruments Portfolio

- Table 9.4 Agilent Technologies: Chromatography Consumables Portfolio

- Table 9.5 Agilent Technologies: Recent Developments and Future Outlook

- Table 9.6 Bio-Rad Laboratories: Company Overview

- Table 9.7 Bio-Rad Laboratories: Chromatography Instruments Portfolio

- Table 9.8 Bio-Rad Laboratories: Chromatography Consumables Portfolio

- Table 9.9 PerkinElmer: Company Overview

- Table 9.10 PerkinElmer: Chromatography Instruments Portfolio

- Table 9.11 PerkinElmer: Chromatography Consumables Portfolio

- Table 9.12 PerkinElmer: Recent Developments and Future Outlook

- Table 9.13 Sartorius: Company Overview

- Table 9.14 Sartorius: Chromatography Instruments Portfolio

- Table 9.15 Sartorius: Chromatography Consumables Portfolio

- Table 9.16 Sartorius: Recent Developments and Future Outlook

- Table 9.17 Shimadzu: Company Overview

- Table 9.18 Shimadzu: Chromatography Instruments Portfolio

- Table 9.19 Shimadzu: Chromatography Consumables Portfolio

- Table 9.20 Shimadzu: Recent Developments and Future Outlook

- Table 9.21 Thermo Fisher Scientific: Company Overview

- Table 9.22 Thermo Fisher Scientific: Chromatography Instruments Portfolio

- Table 9.23 Thermo Fisher Scientific: Chromatography Consumables Portfolio

- Table 9.24 Thermo Fisher Scientific: Recent Developments and Future Outlook

- Table 10.1 Patent Analysis: Top CPC Symbols

- Table 10.2 Patent Analysis: Top CPC Codes

- Table 10.3 Patent Analysis: Summary of Benchmarking Analysis

- Table 10.4 Patent Analysis: Categorization based on Weighted Valuation Scores

- Table 10.5 Patent Portfolio: List of Leading Patents (by Highest Relative Valuation)

- Table 10.6 Patent Portfolio: List of Leading Patents (by Number of Citations)

- Table 11.1 Chromatography Instruments and Consumables: List of Mergers and Acquisitions

- Table 11.2 Acquisitions: Information on Key Value Drivers

- Table 11.3 Key Acquisitions: Information on Deal Multiples

- Table 20.1 Hemochrom: Company Snapshot

- Table 20.2 SRI Instruments: Company Snapshot

- Table 21.1 Chromatography Instruments Providers: Distribution by Year of Establishment

- Table 21.2 Chromatography Instruments Providers: Distribution by Company Size

- Table 21.3 Chromatography Instruments Providers: Distribution by Location of Headquarters

- Table 21.4 Chromatography Instruments Providers: Distribution by Company Size and Location of Headquarters

- Table 21.5 Chromatography Instruments Providers: Distribution by Chromatography Instrument Offered

- Table 21.6 Chromatography Instruments Providers: Distribution by Type of Mobile Phase Used

- Table 21.7 Chromatography Instruments Providers: Distribution by Type of Consumables Offered

- Table 21.8 Chromatography Instruments Providers: Distribution by Scale of Operation

- Table 21.9 Chromatography Instruments Providers: Distribution by Type of Industry Served

- Table 21.10 Chromatography Consumables Providers: Distribution by Year of Establishment

- Table 21.11 Chromatography Consumables Providers: Distribution by Company Size

- Table 21.12 Chromatography Consumables Providers: Distribution by Location of Headquarters

- Table 21.13 Chromatography Consumables Providers: Distribution by Company Size and Location of Headquarters

- Table 21.14 Chromatography Consumables Providers: Distribution by Type of Separation Technique Used

- Table 21.15 Chromatography Consumables Providers: Distribution by Type of Solid Phase Used

- Table 21.16 Chromatography Consumables Providers: Distribution by Type of Consumable Formats Offered

- Table 21.17 Chromatography Consumables Providers: Distribution by Type of Analyte

- Table 21.18 Chromatography Consumables Providers: Distribution by Application Area

- Table 21.19 Patent Analysis: Distribution by Type of Patent

- Table 21.20 Patent Analysis: Distribution by Patent Publication Year

- Table 21.21 Patent Analysis: Distribution by Patent Application Year

- Table 21.22 Patent Analysis: Distribution of Granted Patents and Patent Applications by Publication Year

- Table 21.23 Patent Analysis: Distribution by Patent Jurisdiction (Region)

- Table 21.24 Patent Analysis: Distribution by Patent Jurisdiction (Country)

- Table 21.25 Patent Analysis: Cumulative Year-wise Distribution by Type of Applicant

- Table 21.26 Leading Industry Players: Distribution by Number of Patents

- Table 21.27 Leading Non-Industry Players: Distribution by Number of Patents

- Table 21.28 Leading Individual Patent Assignees: Distribution by Number of Patents

- Table 21.29 Patent Analysis: Distribution by Patent Age

- Table 21.30 Chromatography Instruments and Consumables: Patent Valuation

- Table 21.31 Mergers and Acquisitions: Cumulative Year-Wise Distribution

- Table 21.32 Mergers and Acquisitions: Distribution by Type of Deal

- Table 21.33 Acquisitions: Distribution by Company Ownership

- Table 21.34 Acquisitions and Mergers: Intercontinental and Intracontinental Deals

- Table 21.35 Mergers and Acquisitions: Distribution by Local and International Agreements

- Table 21.36 Most Active Players: Distribution by Number of Mergers and Acquisitions

- Table 21.37 Acquisitions: Key Value Drivers

- Table 21.38 Global Chromatography Market, Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.40 Global Chromatography Market, Till 2035: Conservative Scenario

- Table 21.41 Chromatography Market: Distribution by Type of Product (USD Billion)

- Table 21.42 Chromatography Market for Chromatography Instruments: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.43 Chromatography Market for Chromatography Consumables: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.44 Chromatography Market for Other Accessories: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.45 Chromatography Market: Distribution by Type of Instrument (USD Billion)

- Table 21.46 Chromatography Market for Liquid Chromatography Instruments: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.47 Chromatography Market for Gas Chromatography Instruments: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.48 Chromatography Market for Other Instruments: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.49 Chromatography Market: Distribution by Type of Consumable Formats (USD Billion)

- Table 21.50 Chromatography Market for Pre-packed columns: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.51 Chromatography Market for Bottles / Bulk Resins: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.52 Chromatography Market for Other Formats: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.53 Chromatography Market: Distribution by End User (USD Billion)

- Table 21.54 Chromatography Market for Pharmaceutical and Biotechnology Companies: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.55 Chromatography Market for Academic and Research Institutes: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.56 Chromatography Market for Other Industries: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.57 Chromatography Market: Distribution by Key Geographical Regions (USD Billion)

- Table 21.58 Chromatography Market in North America: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.59 Chromatography Market in Europe: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.60 Chromatography Market in Asia-Pacific: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

- Table 21.61 Chromatography Market in Rest of the World: Historical Trends (Since 2017) and Forecasted Estimates (Till 2035)

List of Figures

- Figure 2.1 Research Methodology: Research Assumptions

- Figure 2.2 Research Methodology: Project Methodology

- Figure 2.3 Research Methodology: Forecast Methodology

- Figure 2.4 Research Methodology: Robust Quality Control

- Figure 2.5 Research Methodology: Key Market Segmentations

- Figure 4.1 Executive Summary: Chromatography Instrument Providers Market Landscape

- Figure 4.2 Executive Summary: Chromatography Consumables Market Landscape

- Figure 4.3 Executive Summary: Patent Analysis

- Figure 4.4 Executive Summary: Mergers and Acquisitions

- Figure 4.5 Executive Summary: Market Sizing and Opportunity Analysis

- Figure 5.1 Components of Chromatography

- Figure 5.2 Types of Chromatography

- Figure 5.3 Applications of Chromatography

- Figure 6.1 Chromatography Instruments Providers: Distribution by Year of Establishment

- Figure 6.2 Chromatography Instruments Providers: Distribution by Company Size

- Figure 6.3 Chromatography Instruments Providers: Distribution by Location of Headquarters

- Figure 6.4 Chromatography Instruments Providers: Distribution by Company Size and Location of Headquarters

- Figure 6.5 Chromatography Instruments Providers: Distribution by Chromatography Instrument Offered

- Figure 6.6 Chromatography Instruments Providers: Distribution by Type of Mobile Phase Used

- Figure 6.7 Chromatography Instruments Providers: Distribution by Type of Consumables Offered

- Figure 6.8 Chromatography Instruments Providers: Distribution by Scale of Operation

- Figure 6.9 Chromatography Instruments Providers: Distribution by Type of Industry Served

- Figure 7.1 Small Companies Providing Chromatography Instruments

- Figure 7.2 Company Competitiveness Analysis: Leading Small Companies

- Figure 7.3 Mid-sized Companies Providing Chromatography Instruments

- Figure 7.4 Company Competitiveness Analysis: Leading Mid-sized Companies

- Figure 7.5 Large Companies Providing Chromatography Instruments

- Figure 7.6 Company Competitiveness Analysis: Leading Large Companies

- Figure 7.7 Very Large Companies Providing Chromatography Instruments

- Figure 7.8 Company Competitiveness Analysis: Leading Very Large Companies

- Figure 8.1 Chromatography Consumables Providers: Distribution by Year of Establishment

- Figure 8.2 Chromatography Consumable Providers: Distribution by Company Size

- Figure 8.3 Chromatography Consumable Providers: Distribution by Location of Headquarters

- Figure 8.4 Chromatography Consumable Providers: Distribution by Company Size and Location of Headquarters

- Figure 8.5 Chromatography Consumable Providers: Distribution by Type of Separation Technique Used

- Figure 8.6 Chromatography Consumable Providers: Distribution by Type of Solid Phase Used

- Figure 8.7 Chromatography Consumable Providers: Distribution by Type of Consumable Formats Offered

- Figure 8.8 Chromatography Consumable Providers: Distribution by Scale of Operation

- Figure 8.9 Chromatography Consumable Providers: Distribution by Application Area

- Figure 10.1 Patent Analysis: Distribution by Type of Patent

- Figure 10.2 Patent Analysis: Distribution by Patent Publication Year, Since 2020

- Figure 10.3 Patent Analysis: Distribution by Patent Application Year, Since Pre-2019

- Figure 10.4 Patent Analysis: Distribution of Granted Patents and Patent Applications by Publication Year, Since 2020

- Figure 10.5 Patent Analysis: Distribution by Patent Jurisdiction (Region-wise)

- Figure 10.6 Patent Analysis: Distribution by Patent Jurisdiction (Country-wise)

- Figure 10.7 Patent Analysis: Distribution by CPC Symbols

- Figure 10.8 Patent Analysis: Cumulative Year-wise Distribution by Type of Applicant, Since 2020

- Figure 10.9 Leading Industry Players: Distribution by Number of Patents

- Figure 10.10 Leading Non-Industry Players: Distribution by Number of Patents

- Figure 10.11 Leading Individual Patent Assignees: Distribution by Number of Patents

- Figure 10.12 Patent Benchmarking Analysis: Distribution of Leading Industry Player by Patent Characteristics (CPC Codes)

- Figure 10.13 Patent Analysis: Distribution by Patent Age

- Figure 10.14 Chromatography Instruments and Consumables: Patent Valuation

- Figure 11.1 Mergers and Acquisitions: Distribution by Type of Deal

- Figure 11.2 Mergers and Acquisitions: Cumulative Year-Wise Distribution, Since Pre-2017

- Figure 11.3 Acquisitions: Distribution by Company Ownership

- Figure 11.4 Acquisitions and Mergers: Intercontinental and Intracontinental Deals

- Figure 11.5 Mergers and Acquisitions: Distribution by Local and International Deals

- Figure 11.6 Most Active Players: Distribution by Number of Mergers and Acquisitions

- Figure 11.7 Acquisitions: Key Value Drivers

- Figure 13.1 Global Chromatography Market, Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 13.2 Global Chromatography Market, Till 2035: Optimistic Scenario

- Figure 13.3 Global Chromatography Market, Till 2035: Conservative Scenario

- Figure 14.1 Chromatography Market for Chromatography Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 14.2 Chromatography Market for Chromatography Consumables: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 14.3 Chromatography Market for Other Accessories: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 15.1 Chromatography Market for Liquid Chromatography Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 15.2 Chromatography Market for Gas Chromatography Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 15.3 Chromatography Market for Other Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 16.1 Chromatography Market for Pre-packed columns: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 16.2 Chromatography Market for Bottles / Bulk Resins: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 16.3 Chromatography Market for Other Formats: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 17.1 Chromatography Market for Pharmaceutical and Biotechnology Companies: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 17.2 Chromatography Market for Academic and Research Institutes: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 17.3 Chromatography Market for Other Industries: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 18.1 Chromatography Market in North America: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 18.2 Chromatography Market in Europe: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 18.3 Chromatography Market in Asia-Pacific: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 18.4 Chromatography Market in Rest of the World: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- Figure 19.1 Concluding Remarks: Chromatography Instrument Providers Market Landscape

- Figure 19.2 Concluding Remarks: Chromatography Consumables Providers Market Landscape

- Figure 19.3 Concluding Remarks: Patent Analysis

- Figure 19.4 Concluding Remarks: Mergers and Acquisitions

- Figure 19.5 Concluding Remarks: Market Sizing and Opportunity Analysis

超臨界流體市場:依產品、設備、製程、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

超臨界流體市場:依產品、設備、製程、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 層析法市場(2025-2030 年):市場概覽

層析法市場(2025-2030 年):市場概覽 層析法設備市場:按組件、儀器類型、分析方法、檢測器類型和應用分類-2026-2032年全球市場預測離子交換層析法市場:2026-2032年全球市場預測(依產品類型、材料類型、方法類型、生產規模、分析類型、結構類型、應用和最終用戶分類)

層析法設備市場:按組件、儀器類型、分析方法、檢測器類型和應用分類-2026-2032年全球市場預測離子交換層析法市場:2026-2032年全球市場預測(依產品類型、材料類型、方法類型、生產規模、分析類型、結構類型、應用和最終用戶分類) 層析法資料系統市場:按產品類型、最終用戶產業、部署模式和地區分類芹菜素市場:依純度、原料、型態、應用、地區分類

層析法資料系統市場:按產品類型、最終用戶產業、部署模式和地區分類芹菜素市場:依純度、原料、型態、應用、地區分類 全球層析法設備市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球層析法設備市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球一次性膜層析法系統市場報告氣相層析法系統市場:2026年至2032年全球市場預測,依應用、產品類型、技術、檢測器類型、色譜管柱類型和最終用戶分類2026年全球現場層析法數據系統市場報告

2026年全球一次性膜層析法系統市場報告氣相層析法系統市場:2026年至2032年全球市場預測,依應用、產品類型、技術、檢測器類型、色譜管柱類型和最終用戶分類2026年全球現場層析法數據系統市場報告