|

市場調查報告書

商品編碼

2005200

中東和非洲醫療美容設備市場-按產品類型、手術、最終用戶、主要地區、產業趨勢和預測(至2035年)Middle East & Africa Medical Aesthetics Devices Market - Distribution by Type of Product and / or Device Offered, Procedure, End User, and Key Geographical Regions: Industry Trends and Global Forecasts, till 2035 |

||||||

中東和非洲醫療美容設備市場概覽

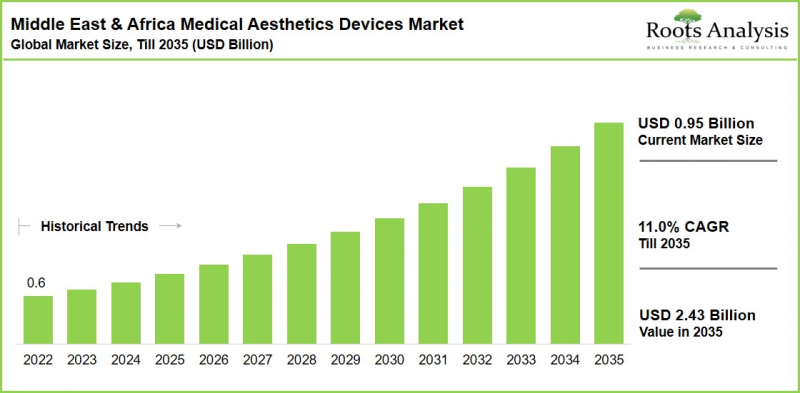

預計到2035年,中東和非洲醫療美容設備市場規模將從目前的9.5億美元成長至 24.3億美元,在預測期內(至2035年)的年複合成長率將達到 11.0%。

中東和非洲醫療美容設備市場:成長與趨勢

醫學美容是現代醫學的一個成熟分支,目的是改善個人外觀,主要透過非手術方式實現。這些療法主要用於抗衰老、減少細紋和皺紋、緊緻鬆弛的皮膚以及煥活肌膚。此外,醫學美容還可以幫助減少多餘脂肪、橘皮組織、去除體毛和蜘蛛網狀靜脈曲張。值得注意的是,該行業近90%的客戶是女性,但這些美容療法也越來越受到男性的歡迎。

值得一提的是,許多醫療問題擴大採用原本用於美容目的的治療方法、手術或器械進行管理。這種擴展拓寬了皮膚科醫師可選擇的治療方案範圍,使其能夠應對超出美容皮膚科範疇的各種適應症。

中東和非洲的醫療美容設備市場也呈現顯著成長,這主要得益於人們對微創治療日益成長的偏好、醫療程序的普及以及美容診所數量的增加。由於經濟變革、文化因素和醫學進步,中東和北非地區對醫療美容設備的需求迅速成長。值得注意的是,在中東和北非地區,尤其是在阿拉伯聯合大公國和沙烏地阿拉伯,非手術美容療法十分盛行,這些療法強調注射療法,具有恢復期短、皮膚修復和體型雕塑優點。肉毒桿菌和皮膚填充劑因其能夠立即減少皺紋和增加臉部容量而備受青睞,隨後人們還會選擇雷射治療和皮膚緊緻療法。基於這些因素,預計中東和北非的醫療美容設備市場在預測期內將顯著成長。

成長促進因素:市場擴張的策略推動因素

中東和北非的醫療美容設備市場正受到技術、人口和社會經濟因素的共同推動,這些因素共同創造了有利於市場成長的環境。在沙烏地阿拉伯和波灣合作理事會等石油資源豐富的海灣合作理事會(GCC)國家,可支配收入的增加和快速的城市化發展,使得不斷壯大的中產階級和上層階級能夠投資於高品質的非侵入性美容療程,消費習慣也從「奢侈品消費」轉向「日常自我護理」。社群媒體的廣泛影響力提高了人們對美的標準,Instagram和TikTok等平台向年輕用戶推廣肉毒桿菌、填充劑和雷射治療等熱門療程。此外,醫療旅遊中心,尤其是杜拜和利雅得,憑藉先進的診所和極具吸引力的價格,吸引著眾多國際患者,而政府數十億美元的醫療基礎設施投資也進一步推動了這一趨勢。

市場挑戰:阻礙進展的重大障礙

儘管中東和北非的醫療美容設備市場持續成長,但挑戰仍然存在,阻礙了其加速普及。這些挑戰包括監管不一致、文化因素和基礎設施問題,這些都可能阻礙市場成長。美容服務業熟練專業人員的短缺嚴重限制了服務的擴張。美容療程通常需要特定的專業知識和理解,因此需要熟悉最新技術、方法和安全標準的熟練人員。缺乏合格的專業人員限制了服務的提供,危及病人安全,並可能導致併發症和對治療效果的不滿。這形成了一個惡性循環,消費者對使用醫療美容產品猶豫不決,進一步阻礙了市場擴張。

本報告調查中東和非洲的醫療美容設備市場,提供了市場規模估算、機會分析、競爭格局和公司簡介等資訊。

目錄

第1章 序言

第2章 調查方法

第3章 市場動態

第4章 宏觀經濟指標

第5章 執行摘要

第6章 引言

第7章 市場狀況

第8章 企業競爭力分析

第9章 公司概況:中東和非洲醫療美容設備市場

- 章節概要

- Allergan(part of AbbVie)

- Galderma

- Cutera

- Alma Lasers

- Cynosure

- Lumenis

- Merz Pharma

- Johnson & Johnson

- Bausch Health

- Hologic

第10章 市場影響分析

第11章 中東和非洲的醫療和美容設備市場

第12章 中東和非洲醫療美容設備市場:依產品/設備類型分類

第13章 中東和非洲醫療美容設備市場:依手術類型分類

第14章 中東和非洲醫療美容設備市場:依最終用戶分類

第15章 中東和非洲醫療美容設備市場:依通路分類

第16章 中東和非洲的醫療美容設備市場:性別

第17章 結論

第18章 附錄1:表格形式資料

第19章 附錄2:公司與組織列表

Middle East and Africa Medical Aesthetics Devices Market: Overview

As per Roots Analysis, the Middle East and Africa medical aesthetics devices market is estimated to grow from USD 0.95 billion in the current year to USD 2.43 billion by 2035 at a CAGR of 11.0% during the forecast period, till 2035.

Middle East and Africa Medical Aesthetics Devices Market: Growth and Trends

Medical aesthetics is a recognized field of contemporary medicine that primarily aims to improve an individual's cosmetic appearance without undergoing surgical procedures. Such solutions are primarily employed for anti-aging reasons by minimizing fine lines and wrinkles, tightening loose skin, and revitalizing the skin. Moreover, medical aesthetic treatments can assist in diminishing excess fat and cellulite, unwanted hair, and spider veins. It is worth highlighting that almost 90% of the industry's clients are women; however, these cosmetic treatments are also becoming increasingly popular with men.

It is also worth mentioning that numerous medical issues are increasingly being managed with treatments, procedures, or devices mostly used for aesthetic purposes. This expansion has broadened the range of treatment options available for dermatologists to address diverse indications that extend beyond aesthetic dermatology.

The market for medical aesthetics devices in the Middle East & Africa (MEA) is also experiencing significant growth, fueled by a growing preference for minimally invasive treatments, the popularity of medical procedures, and a rise in the number of aesthetic clinics. The demand for medical aesthetics equipment in the MENA region is rapidly increasing, driven by a combination of economic changes, cultural factors, and improvements in healthcare. It is worth highlighting that the leading non-surgical cosmetic treatments in MENA, especially in the UAE and Saudi Arabia, focus on injectables, skin renewal, and body contouring with little recovery time. Botox and dermal fillers are favored for their rapid effects on wrinkles and volume increase, followed by laser therapies and skin firming. Owing to the abovementioned factors, the MENA medical aesthetics devices market is poised for notable growth during the forecast period.

Growth Drivers: Strategic Enablers of Market Expansion

The MENA market for medical aesthetics devices is driven by a mixture of technological, demographic, and socioeconomic factors that foster an environment conducive to growth. Increasing disposable incomes in oil-rich Gulf Cooperation Council (GCC) countries such as Saudi Arabia and the UAE, along with swift urban development, have enabled an expanding middle and upper class to invest in high-quality, non-invasive cosmetic procedures, transforming consumer habits from luxury purchases to regular self-care practices. The widespread impact of social media enhances beauty standards, as platforms such as Instagram and TikTok promote trending procedures like Botox, fillers, and laser treatments among a youthful audience. Further, medical tourism centers, especially Dubai and Riyadh, draw international patients with advanced clinics and attractive pricing, enhanced by government initiatives, investing billions into health infrastructure.

Market Challenges: Critical Barriers Impeding Progress

Challenges persist in the MENA medical aesthetics devices market despite the ongoing market growth, hindering faster adoption. These challenges include regulatory inconsistencies, cultural considerations, and infrastructure issues that may hinder growth. The shortage of skilled experts in the aesthetic services industry greatly hinders the expansion of these services. Aesthetic treatments, typically requiring specific expertise and understanding, demand a proficient workforce with most recent technologies, methods, and safety standards. The lack of certified professionals restricts service availability and threatens patient safety, resulting in possible complications and dissatisfaction with outcomes. This establishes a loop in which consumers are reluctant to interact with medical aesthetic products, thereby hindering market expansion. Further, the potential for side effects linked to aesthetic treatments serves as a major limitation for the medical aesthetic market, instilling fear in prospective clients. Numerous cosmetic treatments, whether they are surgical or non-surgical, have an inherent risk of complications like infections, scarring, or unsatisfactory outcomes. This anxiety regarding negative consequences can prevent people from pursuing these services, as users are more aware via social media and online platforms about others' experiences, encompassing unfavorable results. As a result, the possibility of side effects may foster the belief that these procedures are not worth the risk, resulting in decreased interest and involvement in the market.

Invasive Procedures: Leading Market Segment

At present, the invasive procedures segment holds almost 65% of the total market share in Middle East and Africa. This leading position is mainly due to deep-seated cultural inclinations towards dramatic, transformative outcomes instead of subtle improvements. In nations such as Saudi Arabia, Iran, and South Africa, treatments like liposuction, rhinoplasty (nose reshaping), and genioplasty (chin enhancement) lead in procedure numbers, typically making up 50-60% of overall surgeries. Patients seek bold facial restructuring and body contouring aligned with localized beauty ideals such as sharper noses, defined jaws, and slimmer silhouettes that signal status and youth in social circles.

Females: Dominating Market Segment

Currently, females lead the MENA medical aesthetics devices market, representing around 90% of procedure volumes and revenue share. This dominance arises from deep-rooted cultural and societal expectations that highly prioritize feminine beauty and physical perfection. Intense beauty standards, amplified by social media influencers and celebrity culture in urban hubs like Dubai and Riyadh, propel women, particularly those aged 25-45 to seek anti-aging fixes like fillers, Botox, and lasers to combat wrinkles, enhance facial contours, and achieve luminous skin suited to the harsh desert climate

Middle East and Africa Medical Aesthetics Devices Market: Key Segments

Type of Product and / or Device Offered

- Botulinum toxin

- Dermal Fillers

- Chemical Peels

- Body Contouring

- Gluteal Implants

- Hair Removal

- Breast Implants

- Other Products / Devices

By Type of Procedure

- Non Invasive

- Minimally Invasive

- Invasive

By End User

- Hospitals

- Clinics / Med Spas and Dermatology / Cosmetology Centers

- Other end users

By Gender

- Male

- Female

Distribution Channel

- Direct Distribution

- Indirect Distribution

Example Players in Middle East and Africa Medical Aesthetics Devices Market

- Allergan (part of AbbVie)

- Alma Lasers

- Bausch Health

- Candela Medical

- Cutera

- Cynosure

- Galderma

- Hologic

- Johnson & Johnson

- Lumenis

- Merz Pharma

Key Questions Answered in this Report

- How many Middle East and Africa medical aesthetics device developers are currently engaged in this market?

- Which are the leading companies in this market?

- Which country dominates the Middle East and Africa medical aesthetics devices market?

- What are the key trends observed in the Middle East and Africa medical aesthetics devices market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by medical aesthetics device developers in Middle East and Africa?

- What is the current and future Middle East and Africa medical aesthetics devices market size?

- What is the CAGR of Middle East and Africa medical aesthetics devices market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Complementary Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1.PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Concept of Medical Aesthetics

- 6.3. Evolution of Medical Aesthetics

- 6.4. Types of Medical Aesthetic Procedures

- 6.5. Advantages of Medical Aesthetics

- 6.6. Side Effects of Medical Aesthetics

- 6.7. Key Growth Drivers

- 6.8. Emerging Technologies in Medical Aesthetics

- 6.8.1. Virtual Reality in Medical Aesthetics

- 6.8.2. Augmented Reality in Medical Aesthetics

- 6.8.3. Artificial Intelligence in Medical Aesthetics

- 6.8.4. Telemedicine in Medical Aesthetics

- 6.9. Key Challenges of Medical Aesthetics

- 6.10. Future Perspectives

7. MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Medical Aesthetic Companies: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters (Region)

- 7.2.4. Analysis by Location of Headquarters (Country)

- 7.2.5. Analysis by Type of Offering

- 7.2.6. Analysis by Type of Products and / or Devices Offered

- 7.2.7. Analysis by Type of Body Contouring Products and / or Devices Offered

- 7.2.8. Analysis by Type of Hair Removal Devices Offered

- 7.2.9. Analysis by Type of Breast Aesthetic Products and / or Devices Offered

- 7.2.10. Analysis by Application Area

- 7.2.11. Analysis by Type of Procedure

- 7.2.12. Analysis by End-user

8. COMPANY COMPETITIVENESS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Medical Aesthetic Devices: Company Competitiveness Analysis

- 8.4.1. Small Medical Aesthetic Device Developers (Peer Group I)

- 8.4.2. Mid-sized Medical Aesthetic Device Developers (Peer Group II)

- 8.4.3. Large Medical Aesthetic Device Developers (Peer Group III)

9. COMPANY PROFILES: MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET

- 9.1. Chapter Overview

- 9.2. Allergan (part of AbbVie)

- 9.2.1. Company Overview

- 9.2.2. Product Portfolio

- 9.2.3. Financial Information

- 9.2.4. Recent Developments and Future Outlook

- 9.3. Galderma

- 9.4. Cutera

- 9.5. Alma Lasers

- 9.6. Cynosure

- 9.7. Lumenis

- 9.8. Merz Pharma

- 9.9. Johnson & Johnson

- 9.10. Bausch Health

- 9.11. Hologic

10. MARKET IMPACT ANALYSIS

- 10.1. Chapter Overview

- 10.2. Market Drivers

- 10.3. Market Restraints

- 10.4. Market Opportunities

- 10.5. Market Challenges

- 10.6. Conclusion

11. MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET

- 11.1. Chapter Overview

- 11.2. Key Assumptions and Methodology

- 11.3. Global Middle East and Africa Medical Aesthetics Devices Market, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 11.4. Roots Analysis Perspective on Market Growth

- 11.5 Scenario Analysis

- 11.5.1. Conservative Scenario

- 11.5.2. Optimistic Scenario

- 11.6. Key Market Segmentations

12. MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET, BY TYPE OF PRODUCT AND / OR DEVICE OFFERED

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Middle East and Africa Medical Aesthetics Devices Market: Distribution by Type of Product and / or Device Offered

- 12.3.1. Middle East and Africa Medical Aesthetics Devices Market for Botulinum, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.2. Middle East and Africa Medical Aesthetics Devices Market for Dermal Fillers, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.3. Middle East and Africa Medical Aesthetics Devices Market for Chemical Peels, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.4. Middle East and Africa Medical Aesthetics Devices Market for Body Contouring, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.5. Middle East and Africa Medical Aesthetic Devices Market for Gluteal Implants, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.6. Middle East and Africa Medical Aesthetic Devices Market for Hair Removal, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.7. Middle East and Africa Medical Aesthetic Devices Market for Breast Implants, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.3.8. Middle East and Africa Medical Aesthetic Devices Market for Other Products / Devices, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 12.4. Data Triangulation and Validation

13. MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET, BY TYPE OF PROCEDURE

- 13.1. Chapter Overview

- 13.2. Assumptions and Methodology

- 13.3. Middle East and Africa Medical Aesthetics Devices Market: Distribution by Type of Procedure

- 13.3.1. Middle East and Africa Medical Aesthetics Devices Market for Non-invasive Procedures, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 13.3.2. Middle East and Africa Medical Aesthetics Devices Market for Minimally Invasive Procedures, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 13.3.3. Middle East and Africa Medical Aesthetics Devices Market for Invasive Procedures, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 13.4. Data Triangulation and Validation

14. MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET, BY END-USER

- 14.1. Chapter Overview

- 14.2. Assumptions and Methodology

- 14.3. Middle East and Africa Medical Aesthetics Devices Market: Distribution by End-user

- 14.3.1. Middle East and Africa Medical Aesthetics Devices Market for Hospitals, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 14.3.2. Middle East and Africa Medical Aesthetics Devices Market for Clinics / Med Spas and Dermatology / Cosmetology Centers, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 14.4. Data Triangulation and Validation

15. MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET, BY DISTRIBUTION CHANNEL

- 15.1. Chapter Overview

- 15.2. Assumptions and Methodology

- 15.3. Middle East and Africa Medical Aesthetics Devices Market: Distribution by Distribution Channel

- 15.3.1. Middle East and Africa Medical Aesthetics Devices Market for Direct Distribution, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 15.3.2. Middle East and Africa Medical Aesthetics Devices Market for Indirect Distribution, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 15.4. Data Triangulation and Validation

16. MIDDLE EAST AND AFRICA MEDICAL AESTHETICS DEVICES MARKET, BY GENDER

- 16.1. Chapter Overview

- 16.2. Assumptions and Methodology

- 16.3. Middle East and Africa Medical Aesthetics Devices Market: Distribution by Gender

- 16.3.1. Middle East and Africa Medical Aesthetics Devices Market for Females, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 16.3.2. Middle East and Africa Medical Aesthetics Devices Market for Males, Historical Trends (Since 2022) and Forecasted Estimates (till 2035)

- 16.4. Data Triangulation and Validation

17. CONCLUDING REMARKS

18. APPENDIX I: TABULATED DATA

19. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

皮膚分析系統市場規模、佔有率和成長分析:按技術、組件、模式、應用、最終用戶和地區分類-2026-2033年產業預測

皮膚分析系統市場規模、佔有率和成長分析:按技術、組件、模式、應用、最終用戶和地區分類-2026-2033年產業預測 2026年全球非醫療眼科器材市場報告

2026年全球非醫療眼科器材市場報告 全球美容科技市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球美容科技市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 美容設備市場:按產品類型、治療類型、最終用戶和地區分類。

美容設備市場:按產品類型、治療類型、最終用戶和地區分類。 美容醫療設備市場規模、佔有率和成長分析(按產品類型、應用、治療類型、最終用戶和地區分類):產業預測(2026-2033 年)2026年全球家用皮膚科設備市場報告2026年全球非醫療美容器材市場報告

美容醫療設備市場規模、佔有率和成長分析(按產品類型、應用、治療類型、最終用戶和地區分類):產業預測(2026-2033 年)2026年全球家用皮膚科設備市場報告2026年全球非醫療美容器材市場報告 美容設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年AI皮膚分析市場:按組件、部署模式、技術、應用、設備類型、最終用戶和地區分類全球美容市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

美容設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年AI皮膚分析市場:按組件、部署模式、技術、應用、設備類型、最終用戶和地區分類全球美容市場規模、佔有率、趨勢和成長分析報告(2026-2034年)