|

市場調查報告書

商品編碼

1883723

以人工智慧為基礎的數位病理市場:產業趨勢及全球預測(至 2035 年)—依神經網路類型、偵測類型、終端使用者類型、應用領域、目標疾病和主要地區劃分AI-based Digital Pathology Market: Industry Trends and Global Forecasts, Till 2035 - Distribution by Type of Neural Network, Type of Assay, Type of End-User, Area of Application, Target Disease Indication and Key Geographies |

||||||

基於人工智慧的數位病理市場—概述

根據 Roots Analysis 的研究,全球基於人工智慧的數位病理市場預計將從目前的 10.1 億美元增長到 2035 年的 23.2 億美元,預測期內(至 2035 年)的複合年增長率 (CAGR) 為 8.7%。

神經網路類型

- 人工神經網絡

- 卷積神經網絡

- 全卷積網絡

- 循環神經網絡

- 其他

檢測類型

- ER 檢測

- HER2 檢測

- Ki-67、PR 檢測

- 其他

最終使用者類型

- 學術機構

- 醫院/醫療機構

- 實驗室/診斷機構

- 研究機構

- 其他

應用領域

- 診斷

- 研究

- 其他

標靶疾病

- 乳癌

- 大腸直腸癌

- 子宮頸癌

- 胃腸道癌

- 肺癌

- 前列腺癌

- 其他

主要地區

- 北美

- 歐洲

- 亞太地區

- 中東和北非

- 拉丁美洲

基於人工智慧的數位病理市場 - 成長與趨勢

近年來,技術的進步和對精準醫療日益增長的關注推動了人工智慧 (AI) 的發展,並促進了用於樣本定量和定性評估的數位病理技術的應用。這項技術進步使得透過電腦顯示來檢查切片成為可能,取代了傳統的顯微鏡方法。此外,將玻璃切片轉換為影像顯著加快了樣本從診斷中心到病理學家的轉移速度。尤其值得注意的是,人工智慧的整合顯著加深了對組織微環境的理解。人工智慧在診斷中的應用使得確定針對每位患者個體情況的最佳治療策略成為可能,並且數位化方法正被用於對患者進行分類,篩選出符合診斷評估條件的患者。

鑑於病理學領域產生的數據量龐大,人工智慧有望為病理學所有子領域的創新提供機遇,並在影像和非影像診斷領域實現變革性的醫療服務模式。由於其優於傳統病理學方法的優勢,基於人工智慧的數位病理學領域近年來經歷了顯著增長,這些解決方案在研究、開發和臨床環境中變得越來越普遍。

基於人工智慧的數位病理學市場—主要發現

本報告深入分析了基於人工智慧的數位病理學市場的現狀,並指出了該行業潛在的成長機會。報告的主要發現包括:

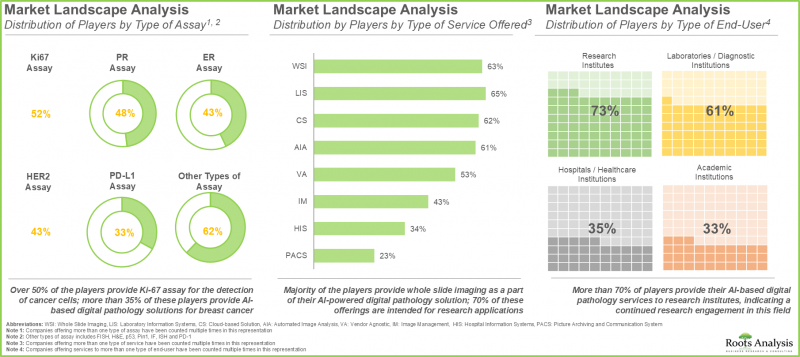

- 目前,約有 80 家公司聲稱向多個地理位置分散的終端用戶提供基於人工智慧的數位病理服務。

- 利害關係人正在利用其專業知識提供各種基於人工智慧的病理服務,這些解決方案主要被研究機構和診斷實驗室採用。

- 該領域的公司透過針對研究和診斷應用的專有產品提供一系列功能。

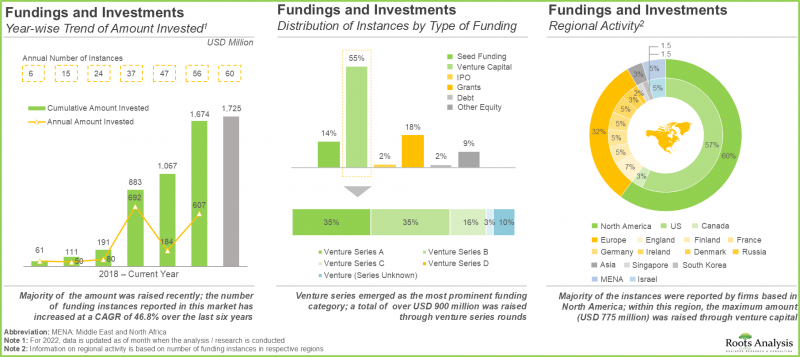

- 投資人意識到該領域的商機,已透過 60 輪融資累計投資約 20 億美元。

- 包括調查部署和人工智慧在臨床工作流程中的整合在內的多種因素,正在推動全球範圍內基於人工智慧的數位病理工具的普及。

- 在對基於人工智慧的數位病理解決方案的需求不斷增長以及對更便捷的醫療保健服務日益增長的偏好推動下,預計到2035年,該市場將以每年8.70%的速度增長。

基於人工智慧的數位病理市場 - 主要區隔市場

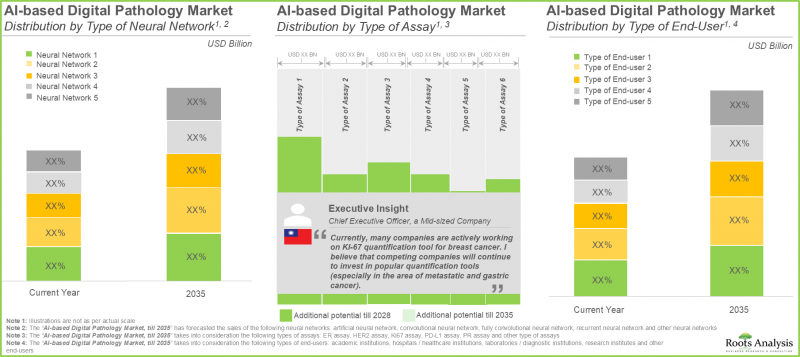

預計在預測期內,卷積神經網路將主導基於人工智慧的數位病理市場。

此市場依神經網路類型區隔為人工神經網路、卷積神經網路、全捲積網路、循環神經網路和其他神經網路。卷積神經網路在基於人工智慧的數位病理市場中佔最大佔有率。值得注意的是,基於人工智慧的神經網路數位病理市場預計將以更高的複合年增長率成長。

目前,Ki67 檢測在基於人工智慧的數位病理市場中佔最大佔有率。

依檢測類型劃分,市場可分為 ER 檢測、HER2 檢測、Ki67 檢測、PR 檢測和其他檢測。 Ki67 檢測佔了基於人工智慧的數位病理市場的大部分佔有率。這是因為 Ki67 表達與細胞增殖密切相關,並且經常被用作增殖標誌物,用於在常規病理檢測中量化人類惡性腫瘤的細胞增殖率。

目前,研究機構在基於人工智慧的數位病理市場中佔最大佔有率。

依最終使用者類型劃分,市場區隔包括學術機構、醫院/醫療機構、檢測/診斷機構、研究機構和其他最終使用者。目前,研究機構在人工智慧數位病理市場中佔最大佔有率,預計未來幾年這一趨勢將保持不變。

在預測期內,診斷領域將成為人工智慧數位病理市場中成長最快的領域。

依應用領域劃分,該市場可分為診斷、研究和其他應用。值得注意的是,研究領域目前在人工智慧數位病理市場中佔有較大佔有率。然而,診斷領域預計將以更高的複合年增長率成長。

預計在預測期內,乳癌將成為推動人工智慧數位病理市場成長的主要因素。

依目標疾病劃分,該市場可分為乳癌、大腸癌、子宮頸癌、胃腸道癌、肺癌、攝護腺癌和其他適應症。值得注意的是,乳癌目前佔人工智慧數位病理市場的大部分佔有率。預計這一趨勢將在未來十年持續。

北美將佔最大的市場佔有率。

依主要地區劃分,市場分為北美、歐洲、亞太、拉丁美洲、中東和北非以及世界其他地區。總部位於北美的公司預計將佔大部分市場佔有率。值得注意的是,預計未來幾年歐洲市場的複合年增長率將更高。

人工智慧數位病理市場代表性公司

- Aiforia Technologies

- Akoya Biosciences

- Ibex Medical Analytics

- Indica Labs

- Paige

- PathAI

- PROSCIA

- Roche Tissue Diagnostics

- Visiopharm

主要研究概述

本研究提出的觀點和見解是基於與多位利害關係人的討論。本報告包含對以下行業專業人士的詳細訪談:

- A公司董事長兼首席執行官

- B公司實驗室主任兼首席病理學家

- C公司副總裁(研發與科技)

- D公司銷售與行銷副總裁

基於人工智慧的數位病理市場 - 研究範圍

- 市場規模和機會分析:本報告對基於人工智慧的數位病理市場進行了詳細分析,重點關注以下關鍵市場區隔:[A] 神經網路類型,[B] 檢測類型,[C] 終端用戶類型,[D] 應用領域,[E] 目標疾病,以及 [F] 主要地區。

- 市場概況:對基於人工智慧的數位病理公司進行全面評估,評估內容包括:[A] 地理覆蓋範圍,[B] 成立年份,[C] 公司規模(員工人數),[D] 總部所在地,[E] 產品類型,[F] 服務類型,[G] 終端功能類型,[H] 附加功能,[E] 應用疾病可用軟體數量。

- 主要發現:深入分析,重點闡述當前市場趨勢,包括:[A] 依服務類型和應用領域劃分的分佈,[B] 依功能類型和應用領域劃分的分佈,[C] 依產品類型和應用領域劃分的分佈,[D] 依產品類型和總部所在地劃分的分佈,以及基於 [E] 公司規模和 [F] 總部的基於分析人工智慧的數位病理公司的綜合公司所在地的綜合分析。

- 公司簡介:提供基於人工智慧的數位病理服務主要公司的詳細簡介,重點關注[A]公司概況、[B]近期發展和[C]未來展望。

- 公司競爭分析:對基於人工智慧的數位病理公司進行全面的競爭分析。我們考察了投資組合實力和融資活動等因素。

- 融資與投資分析:我們基於相關參數對數位病理市場的投資進行詳細評估,例如[A]投資案例數、[B]投資金額、[C]融資類型、[D]應用領域、[E]地區和[F]基於人工智慧的數位病理領域最活躍的企業。

- 需求分析:我們基於相關參數估算基於人工智慧的數位病理的年度需求,例如[A]地區(北美、歐洲、亞洲、拉丁美洲、中東和北非以及世界其他地區)和[B]最終用戶(醫院、研究機構和其他最終用戶)。

目錄

第一章:引言

第二章:摘要整理

第三章:導論

- 章節概述

- 人工智慧在數位病理學的應用

- 基於人工智慧的數位病理學工作流程

- 基於人工智慧的數位病理學解決方案的應用

- 針對基於人工智慧的數位病理學的監管要求

- 人工智慧在數位病理學應用中面臨的挑戰

- 未來展望

第四章:基於人工智慧的數位病理學:市場概況

- 章節概述

- 基於人工智慧的數位病理學提供者:開發者視角

- 基於人工智慧的數位病理學提供者:市場概況

第五章:基於人工智慧的數位病理學市場 - 主要洞察

第六章:公司簡介

- 章節概述

- PathAI

- Paige

- Akoya Biosciences

- PROSCIA

- Visiopharm

- Roche Tissue Diagnostics

- Aiforia Technologies

- Indica Labs

- Ibex Medical Analytics

第七章:競爭分析

第八章:融資與投資

- 章節概述

- 融資類型

- 基於人工智慧的數位病理學:融資與投資列表

- 結論

第九章:需求分析

- 章節概述

- 研究範圍與方法

- 2035 年前全球對基於人工智慧的數位病理學的需求

- 基於人工智慧的數位病理學需求:區域分析

- 北美地區對基於人工智慧的數位病理學的需求

- 歐洲地區對基於人工智慧的數位病理學的需求

- 亞洲地區對以人工智慧為基礎的數位病理學的需求

- 拉丁美洲地區對基於人工智慧的數位病理學的需求

- 中東和北非地區對基於人工智慧的數位病理學的需求

- 世界其他地區對基於人工智慧的數位病理學的需求

- 基於人工智慧的數位病理學需求:依最終用戶類型分析

- 醫院對基於人工智慧的數位病理學的需求

- 科學研究機構對以人工智慧為基礎的數位病理學的需求機構

- 全球其他地區對基於人工智慧的數位病理學的需求

- 結論

第十章 市場規模評估與機會分析

- 章節概述

- 預測研究方法與關鍵假設

- 全球基於人工智慧的數位病理學市場至2035年

- 基於人工智慧的數位病理學市場 - 依神經網路類型劃分的分析(當前及2035年)

- 基於人工智慧的數位病理學市場 - 依檢測類型劃分的分析(當前及2035年)

- 基於人工智慧的數位病理學市場 - 依最終用戶類型劃分的分析(當前及2035年)

- 基於人工智慧的數位病理學市場 - 依應用領域劃分的分析(當前及2035年)

- 基於人工智慧的數位病理學市場 - 依目標疾病劃分的分析(當前及2035年)

- 以人工智慧為基礎的數位病理學市場-主要地區分析(現況及2035年展望)

第十一章:結論

第十二章:高階主管洞察

第十三章:附錄一:表格資料

第十四章:附錄二:公司及機構名單

AI-based Digital Pathology Market: Overview

As per Roots Analysis, the global AI-based digital pathology market is estimated to grow from USD 1.01 billion in the current year to USD 2.32 billion by 2035, at a CAGR of 8.7% during the forecast period, till 2035.

Type of Neural Network

- Artificial Neural Network

- Convolutional Neural Network

- Fully Convolutional Network,

- Recurrent Neural Network

- Other Neural Network

Type of Assay

- ER Assay

- HER2 Assay

- KI67, PR Assay

- Other Type of Assay

Type of End-User

- Academic Institutions

- Hospitals / Healthcare Institutions

- Laboratories / Diagnostic Institutions

- Research Institutes

- Other End-Users

Area of Application

- Diagnostics

- Research

- Other Areas of Application

Target Disease Indication

- Breast Cancer

- Colorectal Cancer

- Cervical Cancer

- Gastrointestinal Cancer

- Lung Cancer

- Prostate Cancer

- Other Indications

Key Geographical Regions

- North America

- Europe

- Asia-Pacific

- Middle East and North Africa

- Latin America

AI-based Digital Pathology Market: Growth and Trends

In recent years, advancements in technology and an emphasis on precision medicine have paved the way for the development of artificial intelligence (AI), which has spurred digital pathology techniques for both quantitative and qualitative assessment of samples. The improved technique allows for the examination of slides via computer displays, replacing conventional microscopic approaches. Additionally, converting glass slides into images allows for samples to be transmitted from diagnostic centers to pathologists much more quickly. It is essential to highlight that the integration of AI has significantly enhanced the understanding of tissue micro-environment. AI involvement in diagnosis enables the determination of optimal treatment strategies suited to patient profiles, utilizing digital methods for categorizing patients and selecting individuals for diagnostic evaluations.

Given the vast amount of data generated in pathology, AI is expected to offer an opportunity for innovation across all pathology subdomains, enabling a transformative model for care delivery in both imaging and non-imaging areas. As a result of the aforementioned advantages over conventional techniques in pathology, the AI-based digital pathology sector has seen significant growth in recent times, with these solutions becoming increasingly popular in research, development, and clinical settings.

AI-based Digital Pathology Market: Key Insights

The report delves into the current state of the AI-based digital pathology market and identifies potential growth opportunities within the industry. Some key findings from the report include:

- Presently, close to 80 players claim to provide AI-based digital pathology services to multiple end-users located across different geographical locations.

- Leveraging their expertise, stakeholders are offering a range of AI-based services for pathology applications; such solutions are primarily being employed by research institutes and laboratory / diagnostic institutions.

- Companies engaged in this domain are offering a range of features through their proprietary products, intended for both research and diagnostic applications.

- Having realized the opportunity associated with this segment, investors have collectively invested ~USD 2 billion, across 60 funding instances.

- A number of factors, such as inclusion of research, as well as the incorporation of AI in the clinical workflow, have led to a rise in the adoption of AI-based digital pathology tools, on a global scale.

- Driven by the rise in demand for AI-based digital pathology solutions and the growing preference for more accessible healthcare services, this market is anticipated to grow at an annualized rate of 8.70% till 2035.

AI-based Digital Pathology Market: Key Segments

Convolutional Neural Network is Likely to Dominate the AI-based Digital Pathology Market During the Forecast Period

In terms of the type of neural network, the market is segmented into artificial neural network, convolutional neural network, fully convolutional network, recurrent neural network and other neural network. The maximum share of the AI-based digital pathology market is captured by convolutional neural network. It is worth highlighting that the AI-based digital pathology market for artificial neural networks is likely to grow at a higher CAGR.

Currently, Ki67 Assays Occupy the Largest Share of the AI-based Digital Pathology Market

In terms of type of assay, the market is segmented into ER assay, HER2 assay, Ki67 assay, PR assay and other type of assay. The majority of the AI-based digital pathology market share is captured by Ki67 assay. This is due to the fact that the expression of Ki67 assays is highly related to cell proliferation and hence, is frequently employed in routine pathology, as a proliferation marker to quantify the growth fraction of cells in human malignancies.

Currently, Research Institutes Occupy the Largest Share of the AI-based Digital Pathology Market

In terms of type of end-user, the market is segmented into academic institutions, hospitals/ healthcare institutions, laboratories / diagnostic institutions, research institutes and other end-users. Currently, research institutes hold the maximum share of the AI-based digital pathology market and the trend will be similar in the coming years.

Diagnostics Segment is the Fastest Growing Segment of the AI-based Digital Pathology Market During the Forecast Period

In terms of area of application, the market is segmented into diagnostics, research and other areas of application. It is worth highlighting that, at present, the research segment holds a larger share of the AI-based digital pathology market. However, the AI-based digital pathology market for diagnostics is likely to grow at a higher CAGR.

Breast Cancer is Likely to Dominate the AI-based Digital Pathology Market During the Forecast Period

In terms of the target disease indication, the market is segmented into breast cancer, colorectal cancer, cervical cancer, gastrointestinal cancer, lung cancer, prostate cancer and other indications. It is worth highlighting that majority of the current AI-based digital pathology market is captured by breast cancer. This trend is likely to remain the same in the coming decade.

North America Accounts for the Largest Share of the Market

In terms of key geographical regions, the market is segmented into North America, Europe, Asia Pacific, Latin America, Middle East and North Africa, and the Rest of the World. The majority of the share is expected to be captured by players based in North America. It is worth highlighting that, over the years, the market in Europe is expected to grow at a higher CAGR.

Example Players in the AI-based Digital Pathology Market

- Aiforia Technologies

- Akoya Biosciences

- Ibex Medical Analytics

- Indica Labs

- Paige

- PathAI

- PROSCIA

- Roche Tissue Diagnostics

- Visiopharm

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

- Chief Executive Officer and Chairman, Company A

- Laboratory Director and Chief Pathologist, Company B

- Vice President (Research and Technology), Company C

- Vice President (Sales and Marketing), Company D

AI-based Digital Pathology Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the AI-based digital pathology market, focusing on key market segments, including [A] type of neural network, [B] type of assay, [C] type of end-user, [D] area of application, [E] target disease indication and [F] key geographical regions.

- Market Landscape: A comprehensive evaluation of AI-based digital pathology companies, considering various parameters, such as [A] geographical reach, [B] year of establishment, [C] company size (in terms of number of employees), [D] location of headquarters, [E] type of product, [F] type of service, [G] type of feature, [H] additional features, [I] area of application, [J] target disease indication, [K] type of assay, [L] type of end-user and [M] information on number of available software.

- Key Insights: An in-depth analysis, highlighting the contemporary market trends, including [A] distribution based on type of service and area of application, [B] distribution based on type of feature and area of application, [C] distribution based on type of product and area of application, [D] type of product and location of headquarters, as well as an insightful hybrid representation of AI-based digital pathology companies based on [E] company size and [F] location of headquarters.

- Company Profiles: In-depth profiles of key AI-based digital pathology companies offering AI-based digital pathology services, focusing on [A] company overviews, [B] recent developments and [C] an informed future outlook.

- Company Competitiveness Analysis: A comprehensive competitive analysis of AI-based digital pathology companies, examining factors, such as portfolio strength and funding activity.

- Funding and Investment Analysis: A detailed evaluation of the investments made in digital pathology market based on several relevant parameters, such as [A] number of instances, [B] amount invested, [C] type of funding, [D] area of application, [E] geography and [F] most active players engaged in the AI-based digital pathology domain.

- Demand Analysis: Informed estimates of the annual demand for AI-based digital pathology based on several relevant parameters, such as [A] geography (North America, Europe, Asia, Latin America, MENA and Rest of the World) and [B] end-users (hospitals, research and other end-users).

Key Questions Answered in this Report

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Chapter Overview

- 1.2. Market Segmentations

- 1.3. Research Methodology

- 1.4. Key Questions Answered

- 1.5. Chapter Outlines

2. EXECUTIVE SUMMARY

3. INTRODUCTION

- 3.1. Chapter Overview

- 3.2. Artificial Intelligence in Digital Pathology

- 3.3. Workflow of AI-based Digital Pathology

- 3.4. Applications of AI-based Digital Pathology Solutions

- 3.5. Regulatory Requirements Focused on AI-based Digital Pathology:

- 3.6. Challenges Associated with the Use of AI in Digital Pathology

- 3.7. Future Perspectives

4. AI-BASED DIGITAL PATHOLOGY: MARKET LANDSCAPE

- 4.1. Chapter Overview

- 4.2. AI-based Digital Pathology Providers: Developers Landscape

- 4.2.1. Analysis by Year of Establishment

- 4.2.2. Analysis by Company Size

- 4.2.3. Analysis by Location of Headquarters

- 4.2.4. Analysis by Geographical Reach

- 4.3. AI-based Digital Pathology Providers: Market Landscape

- 4.3.1. Analysis by Type of Product

- 4.3.2. Analysis by Type of Service Offered

- 4.3.3. Analysis by Type of Feature

- 4.3.4. Analysis by Additional Features

- 4.3.5. Analysis by Target Disease Indication

- 4.3.6. Analysis by Type of Assay

- 4.3.7. Analysis by Area of Application

- 4.3.8. Analysis by Type of End-user

- 4.3.9. Analysis by Number of Available Software

5. AI-BASED DIGITAL PATHOLOGY MARKET: KEY INSIGHTS

- 5.1. Chapter Overview

- 5.1.1. Analysis by Type of Service and Area of Application

- 5.1.2. Analysis by Type of Feature and Area of Application

- 5.1.3. Analysis by Type of Product and Area of Application

- 5.1.4. Analysis by Type of Product and Location of Headquarters

- 5.1.5. Analysis by Company Size and Location of Headquarters

6. COMPANY PROFILES

- 6.1. Chapter Overview

- 6.2. PathAI

- 6.2.1. Company Overview

- 6.2.2. Recent Developments and Future Outlook

- 6.3. Paige

- 6.3.1. Company Overview

- 6.3.2. Recent Developments and Future Outlook

- 6.4. Akoya Biosciences

- 6.4.1. Company Overview

- 6.4.2. Recent Developments and Future Outlook

- 6.5. PROSCIA

- 6.5.1. Company Overview

- 6.5.2. Recent Developments and Future Outlook

- 6.6. Visiopharm

- 6.6.1. Company Overview

- 6.6.2. Recent Developments and Future Outlook

- 6.7. Roche Tissue Diagnostics

- 6.7.1. Company Overview

- 6.7.2. Recent Developments and Future Outlook

- 6.8. Aiforia Technologies

- 6.8.1. Company Overview

- 6.8.2. Recent Developments and Future Outlook

- 6.9. Indica Labs

- 6.9.1. Company Overview

- 6.9.2. Recent Developments and Future Outlook

- 6.10. Ibex Medical Analytics

- 6.10.1. Company Overview

- 6.10.2. Recent Developments and Future Outlook

7. COMPANY COMPETITIVENESS ANALYSIS

- 7.1. Chapter Overview

- 7.2. Assumptions and Key Parameters

- 7.3. Methodology

- 7.4. Benchmarking of Portfolio Strength

- 7.5. Benchmarking of Funding Strength

- 7.6. Company Competitiveness Analysis: Small Players

- 7.7. Company Competitiveness Analysis: Mid-sized Players

- 7.8. Company Competitiveness Analysis: Large Players

8. FUNDING AND INVESTMENTS

- 8.1. Chapter Overview

- 8.2. Types of Funding

- 8.3. AI-based Digital Pathology: List of Funding and Investments

- 8.3.1. Cumulative Year-wise Trend by Number of Instances

- 8.3.2. Cumulative Year-wise Trend by Amount Invested

- 8.3.3. Analysis by Type of Funding

- 8.3.4. Analysis by Type of Funding and Amount Invested

- 8.3.5. Analysis by Area of Application

- 8.3.6. Analysis by Type of Funding and Area of Application

- 8.3.7. Analysis by Geography

- 8.3.8. Most Active Players: Analysis by Number of Funding Instances

- 8.3.9. Most Active Players: Analysis by Amount Raised

- 8.4. Concluding Remarks

9. DEMAND ANALYSIS

- 9.1. Chapter Overview

- 9.2. Scope and Methodology

- 9.3. Global Demand for AI-based Digital Pathology, till 2035

- 9.4. Demand for AI-based Digital Pathology: Analysis by Geography

- 9.4.1. Demand for AI-based Digital Pathology in North America

- 9.4.1.1 Demand for AI-based Digital Pathology in the US

- 9.4.1.2 Demand for AI-based Digital Pathology in Canada

- 9.4.2. Demand for AI-based Digital Pathology in Europe

- 9.4.2.1. Demand for AI-based Digital Pathology in UK

- 9.4.2.2. Demand for AI-based Digital Pathology in Germany

- 9.4.2.3. Demand for AI-based Digital Pathology in Spain

- 9.4.2.4. Demand for AI-based Digital Pathology in Italy

- 9.4.2.5. Demand for AI-based Digital Pathology in France

- 9.4.3. Demand for AI-based Digital Pathology in Asia

- 9.4.3.1. Demand for AI-based Digital Pathology in China

- 9.4.3.2. Demand for AI-based Digital Pathology in Japan

- 9.4.3.3. Demand for AI-based Digital Pathology in South Korea

- 9.4.4. Demand for AI-based Digital Pathology in Latin America

- 9.4.4.1. Demand for AI-based Digital Pathology in Brazil

- 9.4.5. Demand for AI-based Digital Pathology in MENA

- 9.4.5.1. Demand for AI-based Digital Pathology in Saudi Arabia

- 9.4.6. Demand for AI-based Digital Pathology in Rest of the World

- 9.4.6.1. Demand for AI-based Digital Pathology in Australia

- 9.4.1. Demand for AI-based Digital Pathology in North America

- 9.5. Demand for AI-based Digital Pathology: Analysis by Type of End-user

- 9.5.1 Demand for AI-based Digital Pathology in Hospitals

- 9.5.2. Demand for AI-based Digital Pathology in Research Institutes

- 9.5.3. Demand for AI-based Digital Pathology in Other End-users

- 9.6. Concluding Remarks

10. MARKET SIZING AND OPPORTUNITY ANALYSIS

- 10.1. Chapter Overview

- 10.2. Forecast Methodology and Key Assumptions

- 10.3. Global AI-based Digital Pathology Market, till 2035

- 10.4. AI-based Digital Pathology Market: Analysis by Type of Neural Network, Current Year and 2035

- 10.4.1. AI-based Digital Pathology Market for Artificial Neural Network, till 2035

- 10.4.2. AI-based Digital Pathology Market for Convolutional Neural Network, till 2035

- 10.4.3. AI-based Digital Pathology Market for Fully Convolutional Network, till 2035

- 10.4.4. AI-based Digital Pathology Market for Recurrent Neural Network, till 2035

- 10.4.5. AI-based Digital Pathology Market for Other Neural Networks, till 2035

- 10.5. AI-based Digital Pathology Market: Analysis by Type of Assay, Current Year and 2035

- 10.5.1. AI-based Digital Pathology Market for ER Assay, till 2035

- 10.5.2. AI-based Digital Pathology Market for HER2 Assay, till 2035

- 10.5.3. AI-based Digital Pathology Market for Ki67 Assay, till 2035

- 10.5.4. AI-based Digital Pathology Market for PD-L1 Assay, till 2035

- 10.5.5. AI-based Digital Pathology Market for PR Assay, till 2035

- 10.5.6. AI-based Digital Pathology Market for Other Type of Assays, till 2035

- 10.6. AI-based Digital Pathology Market: Analysis by Type of End-user, Current Year and 2035

- 10.6.1. AI-based Digital Pathology Market for Academic Institutions, till 2035

- 10.6.2. AI-based Digital Pathology Market for Hospitals / Healthcare Institutions, till 2035

- 10.6.3. AI-based Digital Pathology Market for Laboratories / Diagnostic Institutions, till 2035

- 10.6.4. AI-based Digital Pathology Market for Research Institutes, till 2035

- 10.6.5. AI-based Digital Pathology Market for Other End-users, till 2035

- 10.7. AI-based Digital Pathology Market: Analysis by Area of Application, Current Year and 2035

- 10.7.1. AI-based Digital Pathology Market for Diagnostics, till 2035

- 10.7.2. AI-based Digital Pathology Market for Research, till 2035

- 10.7.3. AI-based Digital Pathology Market for Other Areas of Application, till 2035

- 10.8. AI-based Digital Pathology Market: Analysis by Target Disease Indication, Current Year and 2035

- 10.8.1. AI-based Digital Pathology Market for Breast Cancer, till 2035

- 10.8.2. AI-based Digital Pathology Market for Colorectal Cancer, till 2035

- 10.8.3. AI-based Digital Pathology Market for Cervical Cancer, till 2035

- 10.8.4. AI-based Digital Pathology Market for Gastrointestinal Cancer, till 2035

- 10.8.5. AI-based Digital Pathology Market for Lung Cancer, till 2035

- 10.8.6. AI-based Digital Pathology Market for Prostate Cancer, till 2035

- 10.8.7. AI-based Digital Pathology Market for Other Indications, till 2035

- 10.9. AI-based Digital Pathology Market: Analysis by Key Geographies, Current Year and 2035

- 10.9.1. AI-based Digital Pathology Market in North America, till 2035

- 10.9.1.1. AI-based Digital Pathology Market in the US, till 2035

- 10.9.1.2. AI-based Digital Pathology Market in Canada, till 2035

- 10.9.2. AI-based Digital Pathology Market in Europe, till 2035

- 10.9.2.1. AI-based Digital Pathology Market in UK, till 2035

- 10.9.2.2. AI-based Digital Pathology Market in Germany, till 2035

- 10.9.2.3. AI-based Digital Pathology Market in Spain, till 2035

- 10.9.2.4. AI-based Digital Pathology Market in Italy, till 2035

- 10.9.2.5. AI-based Digital Pathology Market in France, till 2035

- 10.9.3. AI-based Digital Pathology Market in Asia, till 2035

- 10.9.3.1. AI-based Digital Pathology Market in China, till 2035

- 10.9.3.2. AI-based Digital Pathology Market in Japan, till 2035

- 10.9.3.3. AI-based Digital Pathology Market in South Korea, till 2035

- 10.9.4. AI-based Digital Pathology Market in Latin America, till 2035

- 10.9.4.1. AI-based Digital Pathology Market in Brazil, till 2035

- 10.9.5. AI-based Digital Pathology Market in MENA, till 2035

- 10.9.5.1. AI-based Digital Pathology Market in Saudi Arabia, till 2035

- 10.9.6. AI-based Digital Pathology Market in Rest of the World, till 2035

- 10.9.6.1. AI-based Digital Pathology Market in Australia, till 2035

- 10.9.1. AI-based Digital Pathology Market in North America, till 2035

11. CONCLUDING REMARKS

12. EXECUTIVE INSIGHTS

- 12.1. Chapter Overview

- 12.2. Company A

- 12.2.1. Company Snapshot

- 12.2.2. Interview Transcript: Chief Executive Officer and Chairman

- 12.3. Company B

- 12.3.1. Company Snapshot

- 12.3.2. Interview Transcript: Laboratory Director and Chief Pathologist

- 12.4. Company C

- 12.4.1. Company Snapshot

- 12.4.2. Interview Transcript: Vice President, Research and Technology

- 12.5. Company D

- 12.5.1. Company Snapshot

- 12.5.2. Interview Transcript: Vice President, Sales and Marketing

- 12.6. Company E

- 12.6.1. Company Snapshot

- 12.6.2. Interview Transcript: Vice President, Business Development and Strategic Partnerships

13. APPENDIX 1: TABULATED DATA

14. APPENDIX II: LIST OF COMPANIES AND ORGANIZATION

List of Tables

- Table 4.1 List of AI-based Digital Pathology Providers

- Table 4.2 AI-based Digital Pathology Providers: Information on Type of Product

- Table 4.3 AI-based Digital Pathology Providers: Information on Type of Service Offered

- Table 4.4 AI-based Digital Pathology Providers: Information on Type of Feature

- Table 4.5 AI-based Digital Pathology Providers: Information on Additional Features

- Table 4.6 AI-based Digital Pathology Providers: Information on Target Disease Indication

- Table 4.7 AI-based Digital Pathology Providers: Information on Type of Assay

- Table 4.8 AI-based Digital Pathology Providers: Information on Area of Application

- Table 4.9 AI-based Digital Pathology Providers: Information on Type of End-user

- Table 6.1 AI-based Digital Pathology Providers: List of Profiled Companies

- Table 6.2 PathAI: Company Snapshot

- Table 6.3 PathAI: Recent Developments and Future Outlook

- Table 6.4 Paige: Company Snapshot

- Table 6.5 Paige: Recent Developments and Future Outlook

- Table 6.6 Akoya Biosciences: Company Snapshot

- Table 6.7 Akoya Biosciences: Recent Developments and Future Outlook

- Table 6.8 PROSCIA: Company Snapshot

- Table 6.9 PROSCIA: Recent Developments and Future Outlook

- Table 6.10 Visiopharm: Company Snapshot

- Table 6.11 Visiopharm: Recent Developments and Future Outlook

- Table 6.12 Roche Tissue Diagnostics: Company Snapshot

- Table 6.13 Roche Tissue Diagnostics: Recent Developments and Future Outlook

- Table 6.14 Aiforia Technologies: Company Snapshot

- Table 6.15 Aiforia Technologies: Recent Developments and Future Outlook

- Table 6.16 Indica Labs: Company Snapshot

- Table 6.17 Indica Labs: Recent Developments and Future Outlook

- Table 6.18 Ibex Medical Analytics: Company Snapshot

- Table 6.19 Ibex Medical Analytics: Recent Developments and Future Outlook

- Table 8.1 AI-based Digital Pathology Providers: List of Funding and Investments

- Table 12.1 aetherAI: Company Snapshot

- Table 12.2 Clinitech Laboratory: Company Snapshot

- Table 12.3 Huron Digital Pathology: Company Snapshot

- Table 12.4 Mindpeak: Company Snapshot

- Table 12.5 Pramana: Company Snapshot

- Table 13.1 AI-based Digital Pathology Providers: Distribution by Type of Product

- Table 13.2 AI-based Digital Pathology Providers: Distribution by Type of Service Offered

- Table 13.3 AI-based Digital Pathology Providers: Distribution by Type of Feature

- Table 13.4 AI-based Digital Pathology Providers: Distribution by Additional Features

- Table 13.5 AI-based Digital Pathology Providers: Distribution by Target Disease Indication

- Table 13.6 AI-based Digital Pathology Providers: Distribution by Type of Assay

- Table 13.7 AI-based Digital Pathology Providers: Distribution by Area of Application

- Table 13.8 AI-based Digital Pathology Providers: Distribution by Type of End-User

- Table 13.9 AI-based Digital Pathology Providers: Distribution by Number of Available Software

- Table 13.10 AI-based Digital Pathology Providers: Distribution by Geographical Reach

- Table 13.11 AI-based Digital Pathology Providers: Distribution by Year of Establishment

- Table 13.12 AI-based Digital Pathology Providers: Distribution by Company Size

- Table 13.13 AI-based Digital Pathology Providers: Distribution by Location of Headquarters (Country-wise)

- Table 13.14 AI-based Digital Pathology Providers: Distribution by Location of Headquarters (Continent-wise)

- Table 13.15 Key Insights: Distribution by Type of Service and Area of Application

- Table 13.16 Key Insights: Distribution by Type of Feature and Area of Application

- Table 13.17 Key Insights: Distribution by Type of Product and Area of Application

- Table 13.18 Key Insights: Distribution by Type of Product and Location of Headquarters

- Table 13.19 Key Insights: Distribution by Company Size and Location of Headquarters

- Table 13.20 Funding and Investments: Cumulative Year-wise Trend by Number of Instances

- Table 13.21 Funding and Investments: Cumulative Year-wise Trend by Amount Invested

- Table 13.22 Funding and Investments: Distribution of Instances by Type of Funding

- Table 13.23 Funding and Investments: Distribution of Instances by Type of Funding and Amount Invested

- Table 13.24 Funding and Investments: Distribution of Instances by Area of Application

- Table 13.25 Funding and Investments: Distribution of Instances by Geography

- Table 13.26 Most Active Players: Distribution by Number of Funding Instances

- Table 13.27 Most Active Players: Distribution by Amount Raised

- Table 13.28 Funding and Investments: Concluding Remarks

- Table 13.29 Global Demand for AI-based Digital Pathology, till 2035 (Million Slides)

- Table 13.30 Demand for AI-based Digital Pathology: Distribution by Geography, Current Year and 2035

- Table 13.31 Demand for AI-based Digital Pathology in North America, till 2035 (Million Slides)

- Table 13.32 Demand for AI-based Digital Pathology in the US, till 2035 (Million Slides)

- Table 13.33 Demand for AI-based Digital Pathology in Canada, till 2035 (Million Slides)

- Table 13.34 Demand for AI-based Digital Pathology in Europe, till 2035 (Million Slides)

- Table 13.35 Demand for AI-based Digital Pathology in UK, till 2035 (Million Slides)

- Table 13.36 Demand for AI-based Digital Pathology in Germany, till 2035 (Million Slides)

- Table 13.37 Demand for AI-based Digital Pathology in Spain, till 2035 (Million Slides)

- Table 13.38 Demand for AI-based Digital Pathology in Italy, till 2035 (Million Slides)

- Table 13.39 Demand for AI-based Digital Pathology in France, till 2035 (Million Slides)

- Table 13.40 Demand for AI-based Digital Pathology in Asia, till 2035 (Million Slides)

- Table 13.41 Demand for AI-based Digital Pathology in China, till 2035 (Million Slides)

- Table 13.42 Demand for AI-based Digital Pathology in Japan, till 2035 (Million Slides)

- Table 13.43 Demand for AI-based Digital Pathology in South Korea, till 2035 (Million Slides)

- Table 13.44 Demand for AI-based Digital Pathology in Latin America, till 2035 (Million Slides)

- Table 13.45 Demand for AI-based Digital Pathology in Brazil, till 2035 (Million Slides)

- Table 13.46 Demand for AI-based Digital Pathology in MENA, till 2035 (Million Slides)

- Table 13.47 Demand for AI-based Digital Pathology in Saudi Arabia, till 2035 (Million Slides)

- Table 13.48 Demand for AI-based Digital Pathology in Rest of the World, till 2035 (Million Slides)

- Table 13.49 Demand for AI-based Digital Pathology in Australia, till 2035 (Million Slides)

- Table 13.50 Global Demand for AI-based Digital Pathology: Distribution by End-users, Current Year and 2035

- Table 13.51 Global Demand for AI-based Digital Pathology in Hospitals, till 2035 (Million Slides)

- Table 13.52 Global Demand for AI-based Digital Pathology in Research Institutes, till 2035 (Million Slides)

- Table 13.53 Global Demand for AI-based Digital Pathology in Other End-users, till 2035 (Million Slides)

- Table 13.54 Global AI-based Digital Pathology Market, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.55 AI-based Digital Pathology Market: Distribution by Type of Neural Network, Current Year and 2035

- Table 13.56 AI-based Digital Pathology Market for Artificial Neural Network, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.57 AI-based Digital Pathology Market for Convolutional Neural Network, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.58 AI-based Digital Pathology Market for Fully Convolutional Network, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.59 AI-based Digital Pathology Market for Recurrent Neural Network, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.60 AI-based Digital Pathology Market for Other Neural Networks, till 2035, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.61 AI-based Digital Pathology Market: Distribution by Type of Assay, Current Year and 2035

- Table 13.62 AI-based Digital Pathology Market for ER Assay, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.63 AI-based Digital Pathology Market for HER2 Assay, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.64 AI-based Digital Pathology Market for Ki67 Assay, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.65 AI-based Digital Pathology Market for PD-L1 Assay, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.66 AI-based Digital Pathology Market for PR Assay, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.67 AI-based Digital Pathology Market for Other Type of Assays, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.68 AI-based Digital Pathology Market: Distribution by Type of End-user, Current Year and 2035

- Table 13.69 AI-based Digital Pathology Market for Academic Institutions, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.70 AI-based Digital Pathology Market for Hospitals / Healthcare Institutions, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.71 AI-based Digital Pathology Market for Laboratories / Diagnostic Institutions, Conservative, Base and Optimistic Scenario, till 2035 SD Million)

- Table 13.72 AI-based Digital Pathology Market for Research Institutes, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.73 AI-based Digital Pathology Market for Other End-users, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.74 AI-based Digital Pathology Market: Distribution by Area of Application, Current Year and 2035

- Table 13.75 AI-based Digital Pathology Market for Diagnostics, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.76 AI-based Digital Pathology Market for Research, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.77 AI-based Digital Pathology Market for Other Areas of Application, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.78 AI-based Digital Pathology Market: Distribution by Target Disease Indication, Current Year and 2035

- Table 13.79 AI-based Digital Pathology Market for Breast Cancer, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.80 AI-based Digital Pathology Market for Colorectal Cancer, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.81 AI-based Digital Pathology Market for Cervical Cancer, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.82 AI-based Digital Pathology Market for Gastrointestinal Cancer, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.83 AI-based Digital Pathology Market for Lung Cancer, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.84 AI-based Digital Pathology Market for Prostate Cancer, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.85 AI-based Digital Pathology Market for Other Indications, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.86 AI-based Digital Pathology Market: Distribution by Key Geographies, Current Year and 2035

- Table 13.87 AI-based Digital Pathology Market in North America, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.88 AI-based Digital Pathology Market in the US, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.89 AI-based Digital Pathology Market in Canada, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.90 AI-based Digital Pathology Market in the Europe, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.91 AI-based Digital Pathology Market in UK, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.92 AI-based Digital Pathology Market in the Germany, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.93 AI-based Digital Pathology Market in Spain, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.94 AI-based Digital Pathology Market in Italy, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.95 AI-based Digital Pathology Market in France, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.96 AI-based Digital Pathology Market in Asia, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.97 AI-based Digital Pathology Market in China, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.98 AI-based Digital Pathology Market in Japan, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.99 AI-based Digital Pathology Market in South Korea, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.100 AI-based Digital Pathology Market in Latin America, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.101 AI-based Digital Pathology Market in Brazil, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.102 AI-based Digital Pathology Market in MENA, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.103 AI-based Digital Pathology Market in Saudi Arabia, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.104 AI-based Digital Pathology Market in Rest of the World, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

- Table 13.105 AI-based Digital Pathology Market in Australia, Conservative, Base and Optimistic Scenario, till 2035 (USD Million)

List of Figures

- Figure 2.1 Executive Summary: Market Landscape

- Figure 2.2 Executive Summary: Key Insights

- Figure 2.3 Executive Summary: Funding and Investments

- Figure 2.4 Executive Summary: Demand Analysis

- Figure 2.5 Executive Summary: Market Sizing and Opportunity Analysis

- Figure 3.1 Workflow of AI-based Digital Pathology

- Figure 3.2 Applications of AI-based Digital Pathology Solutions

- Figure 4.1 AI-based Digital Pathology Providers: Distribution by Year of Establishment

- Figure 4.2 AI-based Digital Pathology Providers: Distribution by Company Size

- Figure 4.3 AI-based Digital Pathology Providers: Distribution by Location of Headquarters (Region-wise)

- Figure 4.4 AI-based Digital Pathology Providers: Distribution by Location of Headquarters (Country-wise)

- Figure 4.5 AI-based Digital Pathology Providers: Distribution by Geographical Reach

- Figure 4.6 AI-based Digital Pathology Providers: Distribution by Type of Product

- Figure 4.7 AI-based Digital Pathology Providers: Distribution by Type of Service Offered

- Figure 4.8 AI-based Digital Pathology Providers: Distribution by Type of Feature

- Figure 4.9 AI-based Digital Pathology Providers: Distribution by Additional Features

- Figure 4.10 AI-based Digital Pathology Providers: Distribution by Target Disease Indication

- Figure 4.11 AI-based Digital Pathology Providers: Distribution by Type of Assay

- Figure 4.12 AI-based Digital Pathology Providers: Distribution by Area of Application

- Figure 4.13 AI-based Digital Pathology Providers: Distribution by Type of End-user

- Figure 4.14 AI-based Digital Pathology Providers: Distribution by Number of Available Software

- Figure 5.1 Key Insights: Distribution by Type of Service and Area of Application

- Figure 5.2 Key Insights: Distribution by Type of Feature and Area of Application

- Figure 5.3 Key Insights: Distribution by Type of Product and Area of Application

- Figure 5.4 Key Insights: Distribution by Type of Product and Location of Headquarters

- Figure 5.5 Key Insights: Distribution by Company Size and Location of Headquarters

- Figure 7.1 Company Competitiveness Analysis: Benchmarking of Portfolio Strength

- Figure 7.2 Company Competitiveness Analysis: Benchmarking of Funding Strength

- Figure 7.3 Company Competitiveness Analysis: Small Players

- Figure 7.4 Company Competitiveness Analysis: Mid-sized Players

- Figure 7.5 Company Competitiveness Analysis: Large Players

- Figure 8.1 Funding and Investments: Cumulative Year-wise Trend by Number of Instances

- Figure 8.2 Funding and Investments: Cumulative Year-wise Trend by Amount Invested

- Figure 8.3 Funding and Investments: Distribution of Instances by Type of Funding

- Figure 8.4 Funding and Investments: Distribution of Instances by Type of Funding and Amount Invested

- Figure 8.5 Funding and Investments: Distribution of Instances by Area of Application

- Figure 8.6 Funding and Investments: Distribution of Instances by Geography

- Figure 8.7 Most Active Players: Distribution by Number of Funding Instances

- Figure 8.8 Most Active Players: Distribution by Amount Raised

- Figure 8.9 Funding and Investments: Concluding Remarks

- Figure 9.1 Global Demand for AI-based Digital Pathology, till 2035 (Million Slides)

- Figure 9.2 Demand for AI-based Digital Pathology: Distribution by Geography, Current Year and 2035

- Figure 9.3 Demand for AI-based Digital Pathology in North America, till 2035 (Million Slides)

- Figure 9.4 Demand for AI-based Digital Pathology in the US, till 2035 (Million Slides)

- Figure 9.5 Demand for AI-based Digital Pathology in Canada, till 2035 (Million Slides)

- Figure 9.6 Demand for AI-based Digital Pathology in Europe, till 2035 (Million Slides)

- Figure 9.7 Demand for AI-based Digital Pathology in UK, till 2035 (Million Slides)

- Figure 9.8 Demand for AI-based Digital Pathology in Germany, till 2035 (Million Slides)

- Figure 9.9 Demand for AI-based Digital Pathology in Spain, till 2035 (Million Slides)

- Figure 9.10 Demand for AI-based Digital Pathology in Italy, till 2035 (Million Slides)

- Figure 9.11 Demand for AI-based Digital Pathology in France, till 2035 (Million Slides)

- Figure 9.12 Demand for AI-based Digital Pathology in Asia, till 2035 (Million Slides)

- Figure 9.13 Demand for AI-based Digital Pathology in China, till 2035 (Million Slides)

- Figure 9.14 Demand for AI-based Digital Pathology in Japan, till 2035 (Million Slides)

- Figure 9.15 Demand for AI-based Digital Pathology in South Korea, till 2035 (Million Slides)

- Figure 9.16 Demand for AI-based Digital Pathology in Latin America, till 2035 (Million Slides)

- Figure 9.17 Demand for AI-based Digital Pathology in Brazil, till 2035 (Million Slides)

- Figure 9.18 Demand for AI-based Digital Pathology in MENA, till 2035 (Million Slides)

- Figure 9.19 Demand for AI-based Digital Pathology in Saudi Arabia, till 2035 (Million Slides)

- Figure 9.20 Demand for AI-based Digital Pathology in Rest of the World, till 2035 (Million Slides)

- Figure 9.21 Demand for AI-based Digital Pathology in Australia, till 2035 (Million Slides)

- Figure 9.22 Global Demand for AI-based Digital Pathology: Distribution by Type of End-user, Current Year and 2035

- Figure 9.23 Global Demand for AI-based Digital Pathology in Hospitals, till 2035 (Million Slides)

- Figure 9.24 Global Demand for AI-based Digital Pathology in Research Institutes, till 2035 (Million Slides)

- Figure 9.25 Global Demand for AI-based Digital Pathology in Other End-users, till 2035 (Million Slides)

- Figure 10.1 Global AI-based Digital Pathology Market, till 2035 (USD Million)

- Figure 10.2 AI-based Digital Pathology Market: Distribution by Type of Neural Network, Current Year and 2035

- Figure 10.3 AI-based Digital Pathology Market for Artificial Neural Network, till 2035 (USD Million)

- Figure 10.4 AI-based Digital Pathology Market for Convolutional Neural Network, till 2035 (USD Million)

- Figure 10.5 AI-based Digital Pathology Market for Fully Convolutional Network, till 2035 (USD Million)

- Figure 10.6 AI-based Digital Pathology Market for Recurrent Neural Network, till 2035 (USD Million)

- Figure 10.7 AI-based Digital Pathology Market for Other Neural Networks, till 2035 (USD Million)

- Figure 10.8 AI-based Digital Pathology Market: Distribution by Type of Assay, Current Year and 2035

- Figure 10.9 AI-based Digital Pathology Market for ER Assay, till 2035 (USD Million)

- Figure 10.10 AI-based Digital Pathology Market for HER2 Assay, till 2035 (USD Million)

- Figure 10.11 AI-based Digital Pathology Market for Ki67 Assay, till 2035 (USD Million)

- Figure 10.12 AI-based Digital Pathology Market for PD-L1 Assay, till 2035 (USD Million)

- Figure 10.13 AI-based Digital Pathology Market for PR Assay, till 2035 (USD Million)

- Figure 10.14 AI-based Digital Pathology Market for Other Type of Assays, till 2035 (USD Million)

- Figure 10.15 AI-based Digital Pathology Market: Distribution by Type of End-user, Current Year and 2035

- Figure 10.16 AI-based Digital Pathology Market for Academic Institutions, till 2035 (USD Million)

- Figure 10.17 AI-based Digital Pathology Market for Hospitals / Healthcare Institutions, till 2035 (USD Million)

- Figure 10.18 AI-based Digital Pathology Market for Laboratories / Diagnostic Institutions, till 2035 (USD Million)

- Figure 10.19 AI-based Digital Pathology Market for Research Institutes, till 2035 (USD Million)

- Figure 10.20 AI-based Digital Pathology Market for Other End-users, till 2035 (USD Million)

- Figure 10.21 AI-based Digital Pathology Market: Distribution by Area of Application, Current Year and 2035

- Figure 10.22 AI-based Digital Pathology Market for Diagnostics, till 2035 (USD Million)

- Figure 10.23 AI-based Digital Pathology Market for Research, till 2035 (USD Million)

- Figure 10.24 AI-based Digital Pathology Market for Other Areas of Application, till 2035 (USD Million)

- Figure 10.25 AI-based Digital Pathology Market: Distribution by Target Disease Indication, Current Year and 2035

- Figure 10.26 AI-based Digital Pathology Market for Breast Cancer, till 2035 (USD Million)

- Figure 10.27 AI-based Digital Pathology Market for Colorectal Cancer, till 2035 (USD Million)

- Figure 10.28 AI-based Digital Pathology Market for Cervical Cancer, till 2035 (USD Million)

- Figure 10.29 AI-based Digital Pathology Market for Gastrointestinal Cancer, till 2035 (USD Million)

- Figure 10.30 AI-based Digital Pathology Market for Lung Cancer, till 2035 (USD Million)

- Figure 10.31 AI-based Digital Pathology Market for Prostate Cancer, till 2035 (USD Million)

- Figure 10.32 AI-based Digital Pathology Market for Other Indications, till 2035 (USD Million)

- Figure 10.33 AI-based Digital Pathology Market: Distribution by Geography, Current Year and 2035

- Figure 10.34 AI-based Digital Pathology Market in North America, till 2035 (USD Million)

- Figure 10.35 AI-based Digital Pathology Market in the US, till 2035 (USD Million)

- Figure 10.36 AI-based Digital Pathology Market in Canada, till 2035 (USD Million)

- Figure 10.37 AI-based Digital Pathology Market in Europe, till 2035 (USD Million)

- Figure 10.38 AI-based Digital Pathology Market in UK, till 2035 (USD Million)

- Figure 10.39 AI-based Digital Pathology Market in the Germany, till 2035 (USD Million)

- Figure 10.40 AI-based Digital Pathology Market in Spain, till 2035 (USD Million)

- Figure 10.41 AI-based Digital Pathology Market in Italy, till 2035 (USD Million)

- Figure 10.42 AI-based Digital Pathology Market in France, till 2035 (USD Million)

- Figure 10.43 AI-based Digital Pathology Market in Asia, till 2035 (USD Million)

- Figure 10.44 AI-based Digital Pathology Market in China, till 2035 (USD Million)

- Figure 10.45 AI-based Digital Pathology Market in Japan, till 2035 (USD Million)

- Figure 10.46 AI-based Digital Pathology Market in South Korea, till 2035 (USD Million)

- Figure 10.47 AI-based Digital Pathology Market in Latin America, till 2035 (USD Million)

- Figure 10.48 AI-based Digital Pathology Market in Brazil, till 2035 (USD Million)

- Figure 10.49 AI-based Digital Pathology Market in MENA, till 2035 (USD Million)

- Figure 10.50 AI-based Digital Pathology Market in Saudi Arabia, till 2035 (USD Million)

- Figure 10.51 AI-based Digital Pathology Market in Rest of the World, till 2035 (USD Million)

- Figure 10.52 AI-based Digital Pathology Market in Australia, till 2035 (USD Million)

- Figure 11.1 Concluding Remarks: Market Landscape

- Figure 11.2 Concluding Remarks: Key Insights

- Figure 11.3 Concluding Remarks: Funding and Investments

- Figure 11.4 Concluding Remarks: Demand Analysis

- Figure 11.5 Concluding Remarks: Market Sizing and Opportunity Analysis

數位病理全玻片掃描器市場:按產品類型、技術、應用和最終用戶分類,全球預測,2026-2032年

數位病理全玻片掃描器市場:按產品類型、技術、應用和最終用戶分類,全球預測,2026-2032年 2026年全球數位核型分析市場報告2026年全球數位病理市場報告2026年全球遠距病理切片掃描儀市場報告

2026年全球數位核型分析市場報告2026年全球數位病理市場報告2026年全球遠距病理切片掃描儀市場報告 數位病理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球幻燈片掃描影像分析系統市場(按技術、產品類型、最終用戶、應用和分銷管道分類)預測(2026-2032)整合數位病理掃描儀市場(按類型、影像技術、普及程度、應用和最終用戶分類),全球預測,2026-2032年數位病理切片掃描器市場:按產品、掃描器類型、技術、切片容量、安裝模式、應用和最終用戶分類,全球預測(2026-2032年)

數位病理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球幻燈片掃描影像分析系統市場(按技術、產品類型、最終用戶、應用和分銷管道分類)預測(2026-2032)整合數位病理掃描儀市場(按類型、影像技術、普及程度、應用和最終用戶分類),全球預測,2026-2032年數位病理切片掃描器市場:按產品、掃描器類型、技術、切片容量、安裝模式、應用和最終用戶分類,全球預測(2026-2032年) 數位病理市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,預測(2026-2034 年)全球遠距病理市場:市場規模、市場佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

數位病理市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,預測(2026-2034 年)全球遠距病理市場:市場規模、市場佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)