|

市場調查報告書

商品編碼

1813196

塑膠市場:產業趨勢·全球預測 (~2035年):產品類型·添加劑·環境影響·樹脂·加工技術·用途·終端用戶·企業規模·經營模式·各主要地區Plastics Market, Till 2035: Distribution by Type of Product, Additive, Environmental Impact, Resin, Processing Technique, Application, End User, Company Size, Business Model, and Key Geographical Regions: Industry Trends and Global Forecasts |

||||||

塑膠市場概覽

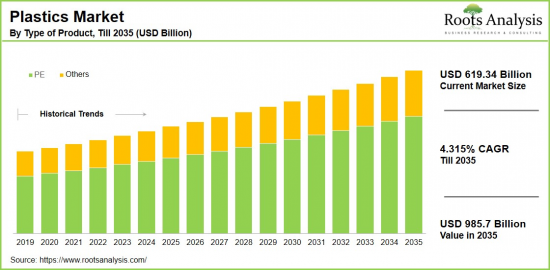

預計到 2035 年,全球塑膠市場規模將從目前的 6,193.4 億美元增長至 9,857 億美元,預測期內複合年增長率為 4.315%。

塑膠市場機會:分類

產品類型

- 丙烯睛-丁二烯-苯乙烯塑膠(ABS)

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚氨酯(PU)

- 聚氯乙烯(PVC)

- 聚酯(PET)

- 聚苯乙烯(PS)

- 其他

添加劑

- 著色劑

- 填充劑

- 阻燃劑

- 塑化劑

- 穩定劑

環境影響的種類

- 生物為基礎塑膠

- 可分解塑膠

- 非回收塑膠

- 回收塑膠

市場結構

- 售後市場

- OEM

樹脂

- 生質塑膠

- 熱塑性塑膠

- 熱硬化性塑膠

加工技術

- 樹脂的種類

- 生質塑膠

- 熱塑性塑膠

- 熱硬化性塑膠

用途

- 吹塑成型

- 壓縮成型

- 押出成型

- 射出成型

- 樂敦成型

- 熱成型

- 鑄造

- 其他

終端用戶

- 汽車·運輸

- 建築·建設

- 消費品·生活方式

- 電器及電子

- 醫療保健&製藥

- 基礎設施·建設

- 包裝

- 纖維

- 其他

企業規模

- 大企業

- 中小企業

經營模式

- B2B

- B2C

- B2B2C

地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 其他的北美各國

- 歐洲

- 奧地利

- 比利時

- 丹麥

- 法國

- 德國

- 愛爾蘭

- 義大利

- 荷蘭

- 挪威

- 俄羅斯

- 西班牙

- 瑞典

- 瑞士

- 英國

- 其他歐洲各國

- 亞洲

- 中國

- 印度

- 日本

- 新加坡

- 韓國

- 其他亞洲各國

- 南美

- 巴西

- 智利

- 哥倫比亞

- 委內瑞拉

- 其他的南美各國

- 中東·北非

- 埃及

- 伊朗

- 伊拉克

- 以色列

- 科威特

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他的中東·北非各國

- 全球其他地區

- 澳洲

- 紐西蘭

- 其他的國家

塑膠市場:成長和趨勢

塑膠產業蓬勃發展,瞬息萬變,透過先進技術重塑傳統製造工藝。該行業涵蓋從包裝到汽車零件等各種產品和應用,對於提高各行各業的營運效率和降低成本至關重要。對輕質耐用材料日益增長的需求,正在推動從傳統工藝向創新塑膠替代品的轉變,從而提高生產效率並減少浪費。

隨著企業努力滿足嚴格的品質標準和環境法規,採用新的加工技術和永續實踐變得越來越重要。對高品質產品的需求正推動企業投資先進的製造方法,以確保產品的一致性和合規性。然而,原材料價格波動、環境問題以及供應鏈中斷等挑戰可能會阻礙成長。此外,中小企業 (SME) 可能難以承擔實施先進技術所需的巨額初始投資。

儘管如此,塑膠市場仍提供了巨大的成長機會,這得益於對環保和可回收材料日益增長的需求。生物塑膠、智慧聚合物和自動化技術的進步有望提高營運效率並減少環境影響。隨著該行業不斷適應不斷變化的消費者偏好和監管要求,預計將繼續擴張。預計這些因素將在預測期內推動塑膠市場的顯著成長。

本報告研究了全球塑膠市場,並提供了市場概況、背景、市場影響因素分析、市場規模趨勢和預測、按細分市場和地區進行的詳細分析、競爭格局以及主要公司概況。

目錄

第1章 序文

第2章 調查手法

第3章 經濟及其他專案特定考量

第4章 宏觀經濟指標

第5章 摘要整理

第6章 簡介

第7章 競爭情形

第8章 企業簡介

- 章概要

- Arkema

- BASF SE

- Borouge

- Borealis

- Braskem

- Celanese

- Phillips

- Dow

- DuPont

- Eni

- Evonik

- Exxon

- Formosa

第9章 價值鏈分析

第10章 SWOT分析

第11章 全球塑膠市場

第12章 各產品類型的市場機會

第13章 添加劑的市場機會

第14章 各環境影響類型的市場機會

第15章 市場結構的市場機會

第16章 樹脂的市場機會

第17章 加工各技術的市場機會

第18章 各用途的市場機會

第19章 各終端用戶的市場機會

第20章 不同企業規模的市場機會

第21章 不同商業模式的市場機會

第22章 北美塑膠的市場機會

第23章 歐洲的塑膠的市場機會

第24章 亞洲的塑膠的市場機會

第25章 中東·北非的塑膠的市場機會

第26章 南美的塑膠的市場機會

第27章 全球其他地區的塑膠的市場機會

第28章 表格形式資料

第29章 企業·團體一覽

第30章 客制化的機會

第31章 ROOTS的訂閱服務

第32章 著者詳細內容

Plastics Market Overview

As per Roots Analysis, the global plastics market size is estimated to grow from USD 619.34 billion in the current year to USD 985.7 billion by 2035, at a CAGR of 4.315% during the forecast period, till 2035.

The opportunity for plastics market has been distributed across the following segments:

Type of Product

- Acrylonitrile Butadiene Styrene (ABS)

- Polyethylene (PE)

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Polyester (PET)

- Polystyrene (PS)

- Others

Type of Additive

- Colorants

- Fillers

- Flame retardants

- Plasticizers

- Stabilizers

Type of Environmental Impact

- Bio-based Plastics

- Degradable Plastics

- Non-recyclable Plastics

- Recyclable Plastics

Type of Market Structure

- Aftermarket

- OEM (Original Equipment Manufacturer)

Type of Resin

- Bioplastics

- Thermoplastics

- Thermosetting plastics

Type of Processing Technique

- Type of Resin

- Bioplastics

- Thermoplastics

- Thermosetting plastics

Area of Application

- Blow Molding

- Compression Molding

- Extrusion Molding

- Injection Molding

- Roto Molding

- Thermoforming

- Casting

- Others

End User

- Automotive & Transportation

- Building & Construction

- Consumer Goods/Lifestyle

- Electrical & Electronics

- Healthcare & Pharmaceutical

- Infrastructure & Construction

- Packaging

- Textile

- Others

Company Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

Business Model

- B2B

- B2C

- B2B2C

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Plastics Market: Growth and Trends

The plastics industry is a vibrant and quickly changing field that is reshaping conventional manufacturing methods through cutting-edge technologies. This sector is essential for boosting operational efficiency and cost savings across a variety of industries, covering a diverse array of products and uses, from packaging to automotive parts. The increasing need for lightweight and resilient materials has fueled the transition from traditional techniques to innovative plastic alternatives, which enhance production efficiency and reduce waste.

As businesses aim to satisfy stringent quality and environmental regulations, the implementation of new processing technologies and sustainable practices has become increasingly crucial. The demand for high-quality goods compels companies to invest in advanced manufacturing methods that guarantee product uniformity and compliance with regulations. Nevertheless, challenges such as variable raw material prices, environmental issues, and supply chain interruptions can impede growth. Furthermore, small and medium enterprises (SMEs) might find it difficult to cope with the significant upfront investment necessary for advanced technologies.

Despite these obstacles, the plastics market presents considerable growth opportunities, fueled by a rising demand for eco-friendly and recyclable materials. Developments in bioplastics, smart polymers, and automation are expected to improve operational efficiency and lessen environmental consequences. As the industry responds to changing consumer preferences and regulatory requirements, it is set for ongoing expansion in the future. Owing to the above-mentioned factors, the plastics market is anticipated to experience significant growth during this forecast period.

Plastics Market: Key Segments

Market Share by Type of Product

Based on type of product, the global plastics market is segmented into acrylonitrile butadiene styrene (ABS), polyethylene (PE), polypropylene (PP), polyurethane (PU), polyvinyl chloride (PVC), polyester (PET), polystyrene (PS), and others.

According to our estimates, currently, the polyethylene (PE) segment captures the majority of the market share. This growth can be attributed to its extensive application in packaging, construction, and automotive sectors. Additionally, this growth can be linked to its versatility, strength, and recyclability.

Market Share by Type of Additive

Based on type of additive, the plastics market is segmented into colorants, fillers, flame retardants, plasticizers, stabilizers, and others. According to our estimates, currently, colorants segment captures the majority of the market. This can be attributed to its crucial role in enhancing the visual attractiveness of plastic products and in marketing initiatives.

As consumers look for unique and appealing products, the demand for colorants continues to be strong. Furthermore, advancements in colorant technologies facilitate customization and differentiation within the market.

Market Share by Type of Environmental Impact

Based on type of environmental impact, the plastics market is segmented bio-based plastics, degradable plastics, non-recyclable plastics, and recyclable plastics. According to our estimates, currently, recyclable plastics segment captures the majority share of the market. This can be attributed to the rising environmental awareness and regulatory demands to minimize plastic waste. Recyclable plastics present an eco-friendly solution by supporting circular economy practices and lessening environmental harm.

Market Share by Type of Market Structure

Based on type of market structure, the plastics market is segmented into aftermarket and OEM (Original Equipment Manufacturer). According to our estimates, currently, OEM segment captures the majority share of the market. This can be attributed to greater demand for plastic parts in the manufacturing processes of original equipment across several sectors such as automotive, electronics, and consumer products. OEMs depend on plastics to produce robust and lightweight components, which contributes to this segment's substantial market share.

Market Share by Type of Resin

Based on type of resin, the plastics market is segmented into bioplastics, thermoplastics, and thermosetting plastics. According to our estimates, currently, thermoplastics segment captures the majority share of the market, driven by their adaptability and ability to be recycled. They are extensively employed across various sectors such as automotive, packaging, and electronics due to their capacity to be melted and reshaped multiple times.

Market Share by Type of Processing Technique

Based on type of processing technique, the plastics market is segmented into 3D printing, compression molding, extrusion blow molding, injection blow molding, and multi-layer molding. According to our estimates, currently, injection blow molding segment captures the majority share of the market, due to its extensive use in producing plastic items such as bottles, containers, and parts for automobiles. Its popularity stems from high production efficiencies and the capability to fabricate intricate shapes with accuracy.

Market Share by Area of Application

Based on area of application, the plastics market is segmented into roto molding, thermoforming, casting, and others. According to our estimates, currently, OEM segment captures the majority share of the market. This can be attributed to its ability to manufacture a diverse array of plastic products, including automotive parts, packaging items, and consumer goods.

Market Share by End User

Based on end user, the plastics market is segmented into automotive & transportation, building & construction, consumer goods/lifestyle, electrical & electronics, healthcare & pharmaceutical, infrastructure & construction, packaging, textile and others. According to our estimates, currently, packaging segment captures the majority share of the market.

This can be attributed to the common usage of plastic materials in various packaging forms, including bottles, containers, and films. The need for convenient and eco-friendly packaging options has resulted in the widespread adoption of plastics in this sector. Furthermore, the adaptability and cost-effectiveness of plastic materials contribute to their popularity for packaging uses in comparison to other industries such as automotive or construction, which have more specific requirements.

Market Share by Company Size

Based on company size, the plastics market is segmented into large size companies and small and mid-size companies. According to our estimates, currently, large companies captures the majority share of the market. This can be attributed to the fact that large companies possess the resources and capabilities to make significant investments in research and development, manufacturing facilities, and marketing, allowing them to produce plastics at a lower cost per unit compared to their smaller rivals.

Additionally, the plastics offered by medium and small businesses are cost-effective alternatives that maintain good quality. This segment is anticipated to expand by 2035 due to increasing demand and improved availability of plastics in the market.

Market Share by Business Model

Based on business model, the plastics market is segmented into B2B, B2C and B2B2C. According to our estimates, currently, B2B segment captures the majority share of the market. This can be attributed to the growing adoption of plastics technology across various industries, including aerospace, manufacturing, healthcare, finance, and more.

Additionally, the B2C model is projected to experience significant growth during the forecast period, as plastics technologies become increasingly user-friendly, with consumers embracing plastics for customized applications, smartphone integration, and an enhanced user experience.

Market Share by Geographical Regions

Based on geographical regions, the plastics market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently North America captures the majority share of the market.

This can be attributed to its sophisticated technological infrastructure, innovative businesses, and a vast and varied consumer base across multiple industries. Additionally, this region has many top plastic manufacturers and suppliers who utilize state-of-the-art technology, research initiatives, and well-established marketing and distribution networks to connect with a broader global audience.

Example Players in Plastics Market

- Arkema

- BASF SE

- Borouge

- Borealis

- Braskem

- Celanese Corporation

- Chevron Phillips Chemical

- China National Petroleum

- China Petroleum & Chemical

- Dow

- DuPont

- Eni

- Evonik

- Exxon Mobil

- Formosa Plastics

- Huntsman

- INEOS Group

- LANXESS

- LG Chem

- Lotte Chemical

- LyondellBasell

- Mitsui & Co.

- Repsol

- RTP

- SABIC

- Sumitomo

- TEIJIN

- Toray

Plastics Market: Research Coverage

The report on the plastics market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the plastics market, focusing on key market segments, including [A] type of product, [B] type of additive, [C] type of environmental impact, [D] type of market structure, [E] type of resin, [F] type of processing technique, [G] area of application, [H] end user, [I] company size, [J] business model, and [K] key geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the plastics market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the plastics market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] plastics portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the plastics market

Key Questions Answered in this Report

- How many companies are currently engaged in plastics market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Plastics Market

- 6.2.1. Key Characteristics of Plastics Market

- 6.2.2. Type of Product

- 6.2.3. Type of Additive

- 6.2.4. Type of Environmental Impact

- 6.2.5. Type of Market Structure

- 6.2.6. Stage of Resin

- 6.2.7. Type of Processing Technique

- 6.2.8. Area of Application

- 6.2.9. Type of End User

- 6.3. Future Perspective

7. COMPETITIVE LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Plastics: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Ownership Structure

8. COMPANY PROFILES

- 8.1. Chapter Overview

- 8.2. Arkema*

- 8.2.1. Company Overview

- 8.2.2. Company Mission

- 8.2.3. Company Footprint

- 8.2.4. Management Team

- 8.2.5. Contact Details

- 8.2.6. Financial Performance

- 8.2.7. Operating Business Segments

- 8.2.8. Service / Product Portfolio (project specific)

- 8.2.9. MOAT Analysis

- 8.2.10. Recent Developments and Future Outlook

- 8.3. BASF SE

- 8.4. Borouge

- 8.5. Borealis

- 8.6. Braskem

- 8.7. Celanese

- 8.8. Phillips

- 8.9. Dow

- 8.10. DuPont

- 8.11. Eni

- 8.12. Evonik

- 8.13. Exxon

- 8.14. Formosa

9. VALUE CHAIN ANALYSIS

10. SWOT ANALYSIS

11. GLOBAL PLASTICS MARKET

- 11.1. Chapter Overview

- 11.2. Key Assumptions and Methodology

- 11.3. Trends Disruption Impacting Market

- 11.4. Global Plastics Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 11.5. Multivariate Scenario Analysis

- 11.5.1. Conservative Scenario

- 11.5.2. Optimistic Scenario

- 11.6. Key Market Segmentations

12. MARKET OPPORTUNITIES BASED ON TYPE OF PRODUCT

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Revenue Shift Analysis

- 12.4. Market Movement Analysis

- 12.5. Penetration-Growth (P-G) Matrix

- 12.6. Plastics Market for Acrylonitrile Butadiene Styrene: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.7. Plastics Market for Polyethylene: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.8. Plastics Market for Polypropylene: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.9. Plastics Market for Polyurethane: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.10. Plastics Market for Polyvinyl Chloride: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.11. Plastics Market for Polyester: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.12. Plastics Market for Polystyrene: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.13. Plastics Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.14. Data Triangulation and Validation

13. MARKET OPPORTUNITIES BASED ON TYPE OF ADDITIVE

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Revenue Shift Analysis

- 13.4. Market Movement Analysis

- 13.5. Penetration-Growth (P-G) Matrix

- 13.6. Plastics Market for Colorants: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.7. Plastics Market for Fillers: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.8. Plastics Market for Flame Retardants: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.9. Plastics Market for Plasticizers: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.10. Plastics Market for Stabilizers: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.11. Data Triangulation and Validation

14. MARKET OPPORTUNITIES BASED ON TYPE OF ENVIRONMENTAL IMPACT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Revenue Shift Analysis

- 14.4. Market Movement Analysis

- 14.5. Penetration-Growth (P-G) Matrix

- 14.6. Plastics Market for Bio-based Plastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.7. Plastics Market for Degradable Plastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.8. Plastics Market for Non-recyclable Plastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.9. Plastics Market for Recyclable Plastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.10. Data Triangulation and Validation

15. MARKET OPPORTUNITIES BASED ON TYPE OF MARKET STRUCTURE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Revenue Shift Analysis

- 15.4. Market Movement Analysis

- 15.5. Penetration-Growth (P-G) Matrix

- 15.6. Plastics Market for Aftermarket: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7. Plastics Market for OEM: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.8. Data Triangulation and Validation

16. MARKET OPPORTUNITIES BASED ON TYPE OF RESIN

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Revenue Shift Analysis

- 16.4. Market Movement Analysis

- 16.5. Penetration-Growth (P-G) Matrix

- 16.6. Plastics Market for Bioplastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.7. Plastics Market for Thermoplastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.8. Plastics Market for Thermosetting Plastics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.9. Data Triangulation and Validation

17. MARKET OPPORTUNITIES BASED ON TYPE OF PROCESSING TECHNIQUE

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Revenue Shift Analysis

- 17.4. Market Movement Analysis

- 17.5. Penetration-Growth (P-G) Matrix

- 17.6. Plastics Market for 3D Printing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.7. Plastics Market for Compression Molding: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.8. Plastics Market for Extrusion Blow Molding: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.9. Plastics Market for Injection Blow Molding: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.10. Plastics Market for Multi-Layer Molding: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.11. Data Triangulation and Validation

18. MARKET OPPORTUNITIES BASED ON AREA OF APPLICATION

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Revenue Shift Analysis

- 18.4. Market Movement Analysis

- 18.5. Penetration-Growth (P-G) Matrix

- 18.6. Plastics Market for Roto Molding: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. Plastics Market for Thermoforming: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.8. Plastics Market for Casting: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.9. Plastics Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.10. Data Triangulation and Validation

19. MARKET OPPORTUNITIES BASED ON END USER

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Plastics Market for Automotive & Transportation: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. Plastics Market for Building & Construction: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. Plastics Market for Consumer Goods/Lifestyle: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.9. Plastics Market for Electrical & Electronic: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.10. Plastics Market for Healthcare & Pharmaceutical: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.11. Plastics Market for Infrastructure & Construction: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.12. Plastics Market for Packaging: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.13. Plastics Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.14. Data Triangulation and Validation

20. MARKET OPPORTUNITIES BASED ON COMPANY SIZE

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Plastics Market for Large Enterprises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Plastics Market for Small and Medium-sized Enterprises (SMEs): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.8. Data Triangulation and Validation

21. MARKET OPPORTUNITIES BASED ON BUSINESS MODEL

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Plastics Market for B2B: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Plastics Market for B2C: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.8. Plastics Market for B2B2C: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.9. Data Triangulation and Validation

22. MARKET OPPORTUNITIES FOR PLASTICS IN NORTH AMERICA

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Plastics Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.1. Plastics Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.2. Plastics Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.3. Plastics Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.4. Plastics Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Data Triangulation and Validation

23. MARKET OPPORTUNITIES FOR PLASTICS IN EUROPE

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Plastics Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.1. Plastics Market in the Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.2. Plastics Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.3. Plastics Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.4. Plastics Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.5. Plastics Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.6. Plastics Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.7. Plastics Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.8. Plastics Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.9. Plastics Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.10. Plastics Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.11. Plastics Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.12. Plastics Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.13. Plastics Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.14. Plastics Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.15. Plastics Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR PLASTICS IN ASIA

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Plastics Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.1. Plastics Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.2. Plastics Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.3. Plastics Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.4. Plastics Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.5. Plastics Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.6. Plastics Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR PLASTICS IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Plastics Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. Plastics Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 25.6.2. Plastics Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. Plastics Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.4. Plastics Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.5. Plastics Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.6. Plastics Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.7. Plastics Market in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.8. Plastics Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR PLASTICS IN LATIN AMERICA

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Plastics Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.1. Plastics Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.2. Plastics Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.3. Plastics Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.4. Plastics Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.5. Plastics Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.6. Plastics Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR PLASTICS IN REST OF THE WORLD

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Plastics Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.1. Plastics Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.2. Plastics Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.3. Plastics Market in Other Countries

- 27.7. Data Triangulation and Validation

28. TABULATED DATA

29. LIST OF COMPANIES AND ORGANIZATIONS

30. CUSTOMIZATION OPPORTUNITIES

31. ROOTS SUBSCRIPTION SERVICES

32. AUTHOR DETAIL

塑膠市場分析及預測(至2035年):類型、產品、應用、材料類型、技術、最終用戶、製程、組件、安裝類型

塑膠市場分析及預測(至2035年):類型、產品、應用、材料類型、技術、最終用戶、製程、組件、安裝類型 東南亞塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東南亞塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球電氣設備塑膠市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球電氣設備塑膠市場規模、佔有率、趨勢和成長分析報告 2026年全球塑膠和橡膠製品市場報告2026年全球塑膠製品市場報告2026年全球熱塑性半成品市場報告2026年全球塑膠材料和樹脂市場報告

2026年全球塑膠和橡膠製品市場報告2026年全球塑膠製品市場報告2026年全球熱塑性半成品市場報告2026年全球塑膠材料和樹脂市場報告 塑膠市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測(2026-2033 年)

塑膠市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測(2026-2033 年)