|

市場調查報告書

商品編碼

1803897

類神經形態運算的全球市場(~2035年):各提供類型,各用途類型,各部署類型,各終端用戶類型,各地區,產業趨勢,預測Neuromorphic Computing Market, Till 2035: Distribution by Type of Offering, Type of Application, Type of Deployment, Type of End User, and Geographical Regions: Industry Trends and Global Forecasts |

||||||

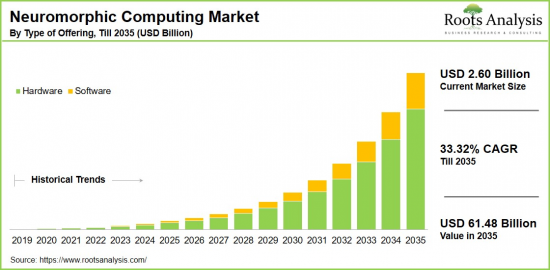

預計到 2035 年,全球神經形態計算市場規模將從目前的 26 億美元增長至 614.8 億美元,預測期內複合年增長率為 33.32%。

神經形態運算市場:成長與趨勢

神經形態計算是一種模擬人腦功能的計算範式。它通常包含旨在模擬大腦神經結構和突觸的硬體和軟體,從而實現更自然、更有效率的資訊處理。 1980年,米歇爾·馬霍瓦爾德(Miescher Mahowald)和卡弗·米德(Carver Mead)創造了第一個矽神經元和突觸,並由此建立了神經形態計算模型。這種方法基於生物學原理,即大腦透過相互連接的神經元和突觸網路並行處理訊息,傳遞化學和電訊號以促進神經元之間的通訊。

在這方面,脈衝神經網路 (SNN) 代表了神經形態計算的一個基本概念,它模擬了生物系統的通訊方式。 SNN 由脈衝突觸和人工神經元組成,不同於依賴連續同步訊號的傳統人工神經網路 (ANN)。 SNN 使用脈衝進行資料處理,從而提高了即時邊緣應用的能源效率。

在此框架內,神經形態運算硬體(包括旨在複製類腦處理過程的專用晶片)發揮關鍵作用。這些神經形態晶片基於神經形態原理運行,能夠比傳統的矽基架構更有效率地執行各種人工智慧任務,包括感知、學習和決策。這項先進的運算技術使各行各業能夠開發出能夠更有效率、更精確地執行複雜任務的機器。

神經形態系統旨在顯著降低功耗,使其成為行動裝置、邊緣運算解決方案和感測器網路等低功耗應用的理想選擇。此外,它們能夠並行處理資料、處理即時資訊並進行自適應學習和可擴展性,這凸顯了它們在人工智慧、機器人、醫療保健和節能計算等各個領域的重要性。隨著人工智慧和機器學習需求的不斷增長,以及神經形態系統在醫療保健領域的日益普及,預計神經形態運算市場在預測期內將大幅成長。

本報告探討並分析了全球神經形態運算市場,提供了市場規模估算、機會分析、競爭格局、公司概況和大趨勢。

目錄

章節1 報告概要

第1章 序文

第2章 調查手法

第3章 市場動態

第4章 宏觀經濟指標

章節2 定性知識見解

第5章 摘要整理

第6章 簡介

第7章 法規Scenario

章節3 市場概要

第8章 主要企業整體性資料庫

第9章 競爭情形

第10章 閒置頻段的分析

第11章 企業的競爭力的分析

第12章 類神經形態運算市場上Start-Ups生態系統

章節4 企業簡介

第13章 企業簡介

- 章概要

- Accenture

- BrainChip Holdings

- Cadence Design Systems

- CEA-Leti

- General Vision

- Gr AI Matter Labs

- Hewlett Packard

- HRL Laboratories

- IBM

- Innatera Nanosystems

- Instar Robotics

- Intel

- Known

- Koniku

- Numenta

- Qualcomm

- Samsung Electronics

- SK Hynix

- NVIDIA

- SynSense

- Vicarious

章節5 市場趨勢

第14章 大趨勢的分析

第15章 未滿足需求的分析

第16章 專利分析

第17章 近幾年的發展

章節6 市場機會分析

第18章 全球類神經形態運算市場

第19章 市場機會:各提供類型

第20章 市場機會:各用途類型

第21章 市場機會:各部署類型

第22章 市場機會:各終端用戶類型

第23章 北美的類神經形態運算市場機會

第24章 歐洲的類神經形態運算市場機會

第25章 亞洲的類神經形態運算市場機會

第26章 中東·北非(MENA)的類神經形態運算市場機會

第27章 南美的類神經形態運算市場機會

第28章 其他地區的類神經形態運算市場機會

第29章 市場集中分析:各主要企業

第30章 鄰近市場的分析

章節7 策略性工具

第31章 關鍵制勝策略

第32章 波特的五力分析

第33章 SWOT的分析

第34章 價值鏈的分析

第35章 Roots的策略性建議

章節8 其他獨家知識見解

第36章 初步研究結果

第37章 報告的結論

章節9 附錄

Neuromorphic Computing Market Overview

As per Roots Analysis, the global neuromorphic computing market size is estimated to grow from USD 2.60 billion in the current year to USD 61.48 billion by 2035, at a CAGR of 33.32% during the forecast period, till 2035.

The opportunity for neuromorphic computing market has been distributed across the following segments:

Type of Offering

- Hardware

- Memory

- Processors

- Sensors

- Others

- Software

- Platform for Neuromorphic Development

- Simulation and Modeling Tools

Type of Application

- Data Processing

- Image Processing

- Object Processing

- Pattern Recognition

- Signal Processing

- Others

Type of Deployment

- Cloud Computing

- Edge Computing

Type of End User

- Automotive

- Consumer Electronics

- Healthcare

- Industrial

- IT & Telecom

- Military & Defense

- Retail

- Others

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Neuromorphic Computing Market: Growth and Trends

Neuromorphic computing is a computing paradigm that mimics the functioning of the human brain. It typically involves both hardware and software designed to emulate the brain's neural structure and synapses, allowing for more natural and efficient information processing. The first silicon neurons and synapses were created by Misha Mahowald and Carver Mead, who established the neuromorphic computing model in 1980. This approach is based on the biological method where the brain processes information in parallel through a network of interconnected neurons and synapses, which transmit chemical and electrical signals to facilitate communication between neurons.

In this regard, spiking neural networks (SNNs) represent a fundamental concept of neuromorphic computing, reflecting how biological systems communicate. SNNs consist of artificial neurons and synapses that spike, differing from traditional artificial neural networks (ANNs) that rely on continuous synchronous signals; instead, SNNs use spikes for data processing, improving power efficiency in real-time edge applications.

Within this framework, the hardware for neuromorphic computing includes specialized chips designed to replicate brain-like processing, playing a crucial role. These neuromorphic chips function based on neuromorphic principles to execute various artificial intelligence tasks, such as recognition, learning, and decision-making, more effectively than conventional silicon-based architectures. This advanced computing technology has enabled industries to develop machines capable of performing complex tasks with greater efficiency and precision.

The aim of neuromorphic systems is to function with significantly reduced power consumption, excelling in low-power applications such as mobile devices, edge computing solutions, and sensor networks. Furthermore, their ability to process data in parallel, handle real-time information, and adaptively learn with scalability underscores their significance across diverse sectors, including AI, robotics, healthcare, and energy-efficient computing. As the demand for artificial intelligence and machine learning rises, along with the integration of neuromorphic systems in healthcare, the neuromorphic computing market is expected to experience significant growth during the forecast period.

Neuromorphic Computing Market: Key Segments

Market Share by Type of Offering

Based on type of offering, the global neuromorphic computing market is segmented into hardware and software. According to our estimates, currently, the hardware segment which consists of neuromorphic processors, memory chips, sensors, and other devices, captures the majority share of the market. This can be attributed to the extensive development of neuromorphic chips, essential for brain-inspired computing architectures, which are crucial for executing tasks like real-time data processing, decision-making, and pattern recognition, thereby propelling market growth.

However, the market for software segment is expected to grow at a higher CAGR during the forecast period, driven by the growing adoption of neuromorphic computing software across various sectors for simulation and algorithm development, particularly with cloud deployment options available.

Market Share by Type of Application

Based on type of application, the neuromorphic computing market is segmented into data processing, image processing, object processing, pattern recognition, signal processing, and others. According to our estimates, currently, the image-processing application captures the majority of the market. This can be attributed to the substantial demand from autonomous vehicles where image processing is crucial for tasks like object detection, lane tracking, and real-time decision-making. Further, the extensive utilization of image processing in medical imaging, robotics, drones, and consumer electronics boosts the demand for neuromorphic computing.

However, the signal processing segment is expected to grow at a higher CAGR during the forecast period. This can be ascribed to the increasing demand from telecommunications aimed at optimizing network traffic management, signal transmission, and data routing. Additionally, the growing adoption of this technology in hearing aids, radar, and sonar systems is also expected to contribute to market growth.

Market Share by Type of Deployment

Based on type of deployment, the neuromorphic computing market is segmented into edge computing and cloud computing deployment. According to our estimates, currently, edge computing deployment captures the majority share of the market. This can be attributed to the critical role of edge computing in achieving low latency and real-time processing, enabling devices to react immediately without delays in data transmission. Additionally, edge devices typically operate with limited power resources, making them energy-efficient, which aligns well with neuromorphic chips designed for local data processing.

However, the cloud computing segment is expected to grow at a higher CAGR during the forecast period. This can be ascribed to the continuous technological advancements in a comprehensive platform for managing large volumes of data for businesses.

Market Share by Type of End User

Based on type of end user, the neuromorphic computing market is segmented into automotive, consumer electronics, healthcare, industrial, IT& telecom, military & defense, retail, and others. According to our estimates, currently, military and defense sector captures the majority share of the market. This can be attributed to the sector's specific needs and its uses in areas such as radar systems, surveillance, and combat systems, which require real-time decision-making, sophisticated data processing, and energy efficiency, thereby driving the growth of the neuromorphic computing market.

However, the automotive sector is expected to grow at a higher CAGR during the forecast period, owing to the increasing production of autonomous vehicles and advanced driver-assistance systems.

Market Share by Geographical Regions

Based on geographical regions, the neuromorphic computing market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently, North America captures the majority share of the market. However, the market in Asia is expected to grow at a higher CAGR during the forecast period, owing to the increased adoption of artificial intelligence, machine learning, IoT, and deep learning technologies, along with the growth of the IT sector in the region.

Example Players in Neuromorphic Computing Market

- Accenture

- Brain Chip Holdings

- Cadence-Design

- CEA-Leti

- General Vision

- Gr AI Matter Labs

- Hewlett Packard

- HP

- HRL Laboratories

- IBM

- Innatera Nanosytems

- Instar Robotics

- Intel

- Known

- Koniku

- Numenta

- Qualcomm

- Samsung Electronics

- SK HynixNVIDIA

- SynsSense

- Vicarious

Neuromorphic Computing Market: Research Coverage

The report on the neuromorphic computing market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the neuromorphic computing market, focusing on key market segments, including [A] type of offering, [B] type of application, [C] type of deployment, [D] type of end user, and [E] geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the neuromorphic computing market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the neuromorphic computing market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] neuromorphic computing portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in neuromorphic computing industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the neuromorphic computing domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the neuromorphic computing market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the neuromorphic computing market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the neuromorphic computing market.

Key Questions Answered in this Report

- How many companies are currently engaged in neuromorphic computing market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Neuromorphic Computing Market

- 6.2.1. Type of Offering

- 6.2.2. Type of Application

- 6.2.3. Type of Deployment

- 6.2.4. Type of End User

- 6.3. Future Perspective

7. REGULATORY SCENARIO

SECTION III: MARKET OVERVIEW

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Neuromorphic Computing: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Ownership Structure

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM IN THE NEUROMORPHIC COMPUTING MARKET

- 12.1. Neuromorphic Computing: Market Landscape of Startups

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Company Size and Year of Establishment

- 12.1.4. Analysis by Location of Headquarters

- 12.1.5. Analysis by Company Size and Location of Headquarters

- 12.1.6. Analysis by Ownership Structure

- 12.2. Key Findings

SECTION IV: COMPANY PROFILES

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Accenture *

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- 13.3. BrainChip Holdings

- 13.4. Cadence Design Systems

- 13.5. CEA-Leti

- 13.6. General Vision

- 13.7. Gr AI Matter Labs

- 13.8. Hewlett Packard

- 13.9. HRL Laboratories

- 13.10. IBM

- 13.11. Innatera Nanosystems

- 13.12. Instar Robotics

- 13.13. Intel

- 13.14. Known

- 13.15. Koniku

- 13.16. Numenta

- 13.17. Qualcomm

- 13.18. Samsung Electronics

- 13.19. SK Hynix

- 13.20. NVIDIA

- 13.21. SynSense

- 13.22. Vicarious

SECTION V: MARKET TRENDS

14. MEGA TRENDS ANALYSIS

15. UNMEET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

SECTION VI: MARKET OPPORTUNITY ANALYSIS

18. GLOBAL NEUROMORPHIC COMPUTING MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Neuromorphic Computing, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF OFFERING

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Neuromorphic Computing Market for Hardware: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. Neuromorphic Computing Market for Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. Data Triangulation and Validation

- 19.8.1. Secondary Sources

- 19.8.2. Primary Sources

- 19.8.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF APPLICATION

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Neuromorphic Computing Market for Data Processing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Neuromorphic Computing Market for Image Processing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.8. Neuromorphic Computing Market for Object Processing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.9. Neuromorphic Computing Market for Pattern Recognition: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.10. Neuromorphic Computing Market for Signal Processing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.11. Neuromorphic Computing Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.12. Data Triangulation and Validation

- 20.12.1. Secondary Sources

- 20.12.2. Primary Sources

- 20.12.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON TYPE OF DEPLOYMENT

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Neuromorphic Computing Market for Cloud Computing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Neuromorphic Computing Market for Edge Computing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.8. Data Triangulation and Validation

- 21.8.1. Secondary Sources

- 21.8.2. Primary Sources

- 21.8.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON TYPE OF END USER

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Neuromorphic Computing Market for Automotive: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Neuromorphic Computing Market for Consumer Electronics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.8. Neuromorphic Computing Market for Healthcare: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.9. Neuromorphic Computing Market for Industrial: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.10. Neuromorphic Computing Market for IT & Telecom: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.11. Neuromorphic Computing Market for Military & Defense: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.12. Neuromorphic Computing Market for Retail: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.13. Neuromorphic Computing Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.14. Data Triangulation and Validation

- 22.14.1. Secondary Sources

- 22.14.2. Primary Sources

- 22.14.3. Statistical Modeling

23. MARKET OPPORTUNITIES FOR NEUROMORPHIC COMPUTING IN NORTH AMERICA

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Neuromorphic Computing Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.1. Neuromorphic Computing Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.2. Neuromorphic Computing Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.3. Neuromorphic Computing Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.4. Neuromorphic Computing Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR NEUROMORPHIC COMPUTING IN EUROPE

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Neuromorphic Computing Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.1. Neuromorphic Computing Market in Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.2. Neuromorphic Computing Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.3. Neuromorphic Computing Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.4. Neuromorphic Computing Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.5. Neuromorphic Computing Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.6. Neuromorphic Computing Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.7. Neuromorphic Computing Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.8. Neuromorphic Computing Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.9. Neuromorphic Computing Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.10. Neuromorphic Computing Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.11. Neuromorphic Computing Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.12. Neuromorphic Computing Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.13. Neuromorphic Computing Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.14. Neuromorphic Computing Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.15. Neuromorphic Computing Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.16. Neuromorphic Computing Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR NEUROMORPHIC COMPUTING IN ASIA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Neuromorphic Computing Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. Neuromorphic Computing Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.2. Neuromorphic Computing Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. Neuromorphic Computing Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.4. Neuromorphic Computing Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.5. Neuromorphic Computing Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.6. Neuromorphic Computing Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR NEUROMORPHIC COMPUTING IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Neuromorphic Computing Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.1. Neuromorphic Computing Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 26.6.2. Neuromorphic Computing Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.3. Neuromorphic Computing Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.4. Neuromorphic Computing Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.5. Neuromorphic Computing Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.6. Neuromorphic Computing Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.7. Neuromorphic Computing Marke in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.8. Neuromorphic Computing Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR NEUROMORPHIC COMPUTING IN LATIN AMERICA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Neuromorphic Computing Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.1. Neuromorphic Computing Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.2. Neuromorphic Computing Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.3. Neuromorphic Computing Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.4. Neuromorphic Computing Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.5. Neuromorphic Computing Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.6. Neuromorphic Computing Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR NEUROMORPHIC COMPUTING IN REST OF THE WORLD

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Neuromorphic Computing Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.1. Neuromorphic Computing Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.2. Neuromorphic Computing Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.3. Neuromorphic Computing Market in Other Countries

- 28.7. Data Triangulation and Validation

29. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

- 29.1. Leading Player 1

- 29.2. Leading Player 2

- 29.3. Leading Player 3

- 29.4. Leading Player 4

- 29.5. Leading Player 5

- 29.6. Leading Player 6

- 29.7. Leading Player 7

- 29.8. Leading Player 8

30. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

31. KEY WINNING STRATEGIES

32. PORTER'S FIVE FORCES ANALYSIS

33. SWOT ANALYSIS

34. VALUE CHAIN ANALYSIS

35. ROOTS STRATEGIC RECOMMENDATIONS

- 35.1. Chapter Overview

- 35.2. Key Business-related Strategies

- 35.2.1. Research & Development

- 35.2.2. Product Manufacturing

- 35.2.3. Commercialization / Go-to-Market

- 35.2.4. Sales and Marketing

- 35.3. Key Operations-related Strategies

- 35.3.1. Risk Management

- 35.3.2. Workforce

- 35.3.3. Finance

- 35.3.4. Others

SECTION VIII: OTHER EXCLUSIVE INSIGHTS

36. INSIGHTS FROM PRIMARY RESEARCH

37. REPORT CONCLUSION

SECTION IX: APPENDIX

38. TABULATED DATA

39. LIST OF COMPANIES AND ORGANIZATIONS

40. CUSTOMIZATION OPPORTUNITIES

41. ROOTS SUBSCRIPTION SERVICES

42. AUTHOR DETAILS

神經形態運算市場:2026-2032年全球市場預測(以交付方式、運算模型、應用、部署和最終用戶分類)

神經形態運算市場:2026-2032年全球市場預測(以交付方式、運算模型、應用、部署和最終用戶分類) 2026年全球神經型態計算市場報告

2026年全球神經型態計算市場報告 神經形態計算市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、解決方案分類

神經形態計算市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、解決方案分類 神經形態計算市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球神經形態計算市場規模、佔有率、趨勢和成長分析報告(2026-2034年)神經形態計算市場:2025-2030 年預測

神經形態計算市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球神經形態計算市場規模、佔有率、趨勢和成長分析報告(2026-2034年)神經形態計算市場:2025-2030 年預測 2032 年神經型態計算市場預測:按組件、部署、應用、最終用戶和地區進行的全球分析

2032 年神經型態計算市場預測:按組件、部署、應用、最終用戶和地區進行的全球分析 全球神經型態運算市場:市場規模、佔有率、趨勢分析(按部署方法、組件、最終用途、應用和地區)、展望和未來預測(2025-2032 年)

全球神經型態運算市場:市場規模、佔有率、趨勢分析(按部署方法、組件、最終用途、應用和地區)、展望和未來預測(2025-2032 年) 神經型態運算市場:全球按產品、部署、應用、垂直和地區分類 - 預測至 2030 年

神經型態運算市場:全球按產品、部署、應用、垂直和地區分類 - 預測至 2030 年 神經形態計算市場規模、佔有率和成長分析(按組件、按部署方法、按應用、按最終用途、按地區):產業預測 (2024-2031)

神經形態計算市場規模、佔有率和成長分析(按組件、按部署方法、按應用、按最終用途、按地區):產業預測 (2024-2031)