|

市場調查報告書

商品編碼

1762523

分子診斷市場:產業趨勢與全球預測 - 依檢測類型、依產品類型、依樣本類型、依技術類型、依治療領域、依最終用戶、依地區Molecular Diagnostics Market: Industry Trends and Global Forecasts - Distribution by Test Type, Type of Offering, Type of Sample, Type of Technology, Therapeutic Area, End Users, and Geographical Regions |

||||||

分子診斷市場:概覽

預計2035年,全球分子診斷市場規模將從目前的159億美元成長到309億美元,預測期間的年複合成長率為6.2%。

市場區隔包括以下參數的市場規模和機會分析:

檢測類型

- 實驗室檢測

- 即時偵測

產品類型

- 試劑

- 檢測設備

- 服務

樣本類型

- 血液、血清、血漿

- 尿液

- 其他

技術類型

- 聚合酶鍊式反應(PCR)

- 原位雜交

- 恆溫核酸擴增技術

- 新一代定序

- 微陣列

- 質譜

- 其他

治療領域

- 心血管疾病

- 基因疾病

- 傳染病

- 神經系統疾病

- 腫瘤疾病

- 其他

最終使用者

- 醫院

- 實驗室

- 其他

主要地區

- 北美(美國、加拿大)

- 歐洲(奧地利、比利時、 (例如:法國、德國、義大利、荷蘭、波蘭、西班牙、瑞士、英國等)

- 亞洲(中國、印度、印尼、日本、新加坡、韓國、泰國等)

- 拉丁美洲(阿根廷、巴西、墨西哥等)

- 中東和北非(埃及、以色列、沙烏地阿拉伯等)

- 世界其他地區(澳洲、紐西蘭)

分子診斷市場:成長與趨勢

分子診斷測試是用於分析基因組和蛋白質組中生物標記的先進技術和工具。這些診斷解決方案對於檢測和監測疾病、識別基因異常以及指導個人化治療計劃非常重要。分子診斷領域使用的主要技術包括聚合酶鍊式反應、新一代定序和微陣列。 PCR是一種高度特異性的技術,可以擴增和檢測微量的DNA和RNA,而NGS可以對整個基因組進行高通量定序。因此,分子診斷解決方案在癌症、傳染病、基因檢測和個人化醫療等各個醫療領域中發揮著非常重要的作用。這些解決方案能夠提高診斷的準確性,並支持個人化的治療策略,最終目的是改善診斷結果並改善公眾健康。此外,超過 70%的醫療保健決策是基於實驗室檢測結果,這反映了此類診斷工具在患者護理中的重要性。

此外,由於分子診斷解決方案具有快速檢測、縮短週轉時間和快速決策等諸多優勢,預計預測期內市場將維持健康的年複合成長率。

分子診斷市場:關鍵洞察

本報告分析了分子診斷市場的現狀,並揭示了潛在的成長機會。報告的主要調查結果包括:

- 分子診斷領域市場格局充滿活力,參與者使用各種先進技術來實現各種診斷應用。

- 本分析涵蓋的許多主要參與者均成立於1951年至2000年之間,其中60%位於北美。

- 憑藉其多樣化的分子診斷解決方案組合以及近年來的強勁表現,Roche已成為該領域最具實力的主要參與者。

- 為了研究各種趨勢對分子診斷市場的影響,開發了一種獨特的研究方法,並根據波特五力模型分析了各種參數。

- 預防性醫療保健意識的不斷增強推動了分子診斷市場的發展,然而,監管的複雜性仍然是該行業參與者面臨的主要障礙。

- 受全球慢性病盛行率上升的推動,預計預測期內分子診斷市場將以 6.2%的健康成長率成長。

- 預期未來機會將均衡分佈在檢測類型、樣本類型、治療領域和最終用戶等多個細分領域。

分子診斷市場:關鍵細分市場

根據檢測類型,市場分為實驗室檢測和即時檢測。目前,實驗室檢測在分子診斷市場中佔有最大佔有率。預計未來這一趨勢將保持不變。此外,預計在預測期內,即時檢測領域的分子診斷市場將展現出最高的市場成長潛力。

依產品類型劃分,試劑是全球分子診斷市場中成長最快的細分市場。

分子診斷市場細分為試劑、儀器和服務。目前,試劑在全球分子診斷市場中佔有最大佔有率。此外,由於試劑需要頻繁補充,這有助於產生經常性收入,因此預計在預測期內,試劑市場的年複合成長率將更高。

依樣本類型劃分,市場細分為血液、血清/血漿、尿液和其他樣本。目前,血液、血清和血漿在全球分子診斷市場中佔有最大佔有率。然而,預計在預測期內,尿液市場的年複合成長率將更高。

依技術類型,市場細分為聚合酶鍊式反應(PCR)、原位雜交、恆溫核酸擴增技術、新一代定序、微陣列、質譜等。雖然聚合酶鍊式反應(PCR)細分市場預計將成為整體市場的主要驅動力,但值得注意的是,新一代定序細分市場的全球分子診斷市場很可能會以相對較高的年複合成長率成長。這可以歸因於新一代定序儀提供的許多優勢,例如高通量、更高的準確性以及同時對多個基因進行定序的能力。

依治療領域,市場細分為心血管疾病、遺傳疾病、傳染病、神經系統疾病、腫瘤疾病等。目前,傳染病細分市場佔據分子診斷市場的最大佔有率。此外,預計神經系統疾病細分市場在預測期內將展現最高的成長潛力,並且相比其他細分市場,其年複合成長率更高。

依最終用戶劃分,全球市場分為醫院、實驗室和其他。目前,醫院佔據最大的市場佔有率。然而,預計未來幾年實驗室分子診斷市場將大幅成長。

依主要地區劃分,市場分為北美、歐洲、亞洲、拉丁美洲、中東和非洲以及拉丁美洲其他地區。目前,北美在全球分子診斷市場佔據主導地位,佔據最大的收入佔有率。此外,預計未來幾年亞太地區市場將以更高的年複合成長率成長。

進入分子診斷市場的公司範例

- Abbott Laboratories

- Agilent Technologies

- Becton Dickinson

- BGI Genomics

- bioMerieux

- Bio-Rad

- Danaher

- DiaSorin

- Grifols

- Hologic

- Illumina

- Qiagen

- QuidelOrtho

- Revvity

- Roche

- Sansure

- Seegene

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

目錄

第1章 背景

第2章 研究方法論

第3章 經濟及其他專案具體考量

第4章 執行摘要

第5章 導論

- 分子診斷概述

- 分子診斷解決方案中採用的關鍵技術

- 分子診斷領域面臨的挑戰

- 分子診斷領域的最新趨勢

- 分子診斷領域的未來展望

第6章 市場影響分析:驅動因素、限制因素、機會與挑戰

第7章 全球分子診斷市場

- 關鍵假設與研究方法

- 全球分子診斷市場2035

第8章 分子診斷市場:依檢測類型

- 市場動態分析

- 分子診斷市場:依檢測類型

- 2035年前臨床檢測的分子診斷市場

- 2035年前即時檢測的分子診斷市場

第9章 分子診斷市場:依產品類型

- 市場動態分析

- 分子診斷市場:依產品類型

第10章 分子診斷市場:依樣本類型

- 市場動態分析

- 分子診斷市場:依樣本類型

第11章 分子診斷市場:依技術類型

- 市場動態分析

- 分子診斷市場:依技術類型

第12章 分子診斷市場:依治療領域

- 市場波動分析

- 分子診斷市場:依治療領域

第13章 分子診斷市場:依最終用戶

- 市場波動分析

- 分子診斷市場:依最終用戶

第14章 分子診斷市場:依地區

- 市場波動分析

- 分子診斷市場:依地區

第15章 分子診斷市場:依主要公司

- 分子診斷市場:按年銷售額的主要公司

第16章 市場概覽:領先的分子診斷解決方案提供者

- 分子診斷解決方案:市場格局

- 分子診斷:解決方案提供者格局

第17章 公司競爭力分析:分子診斷解決方案提供者

- 評估研究方法和關鍵參數

- 分子診斷解決方案提供者:領先公司競爭力分析

- 分子診斷解決方案提供者:領先公司競爭力分析

- 基準分析:領先的分子診斷解決方案提供商

第18章 公司簡介:北美分子診斷解決方案提供者

- 公司詳情個人資料

- Abbott

- Agilent Technologies

- BD

- Danaher

- Thermo Fisher Scientific

- 其他公司簡介

- Bio-Rad

- Illumina

- Hologic

- PerkinElmer

- QuidelOrtho

第19章 公司簡介:歐洲分子診斷解決方案提供者

- 詳細的公司簡介

- bioMerieux

- Grifols

- Roche

- Siemens Healthineers

- 其他公司簡介

- DiaSorin

- Qiagen

第20章 公司簡介:亞洲分子診斷解決方案提供者

- 詳細公司簡介

- Sysmex

- 其他公司簡介

- BGI Genomics

- Sansure

- Seegene

第21章 波特五力分析

第22章 附錄1:表格資料

第23章 附錄2:公司列表及組織

MOLECULAR DIAGNOSTICS MARKET: OVERVIEW

As per Roots Analysis, the global molecular diagnostics market is estimated to grow from USD 15.9 billion in the current year to USD 30.9 billion by 2035, at a CAGR of 6.2% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Test Type

- Laboratory Testing

- Point-of-Care Testing

Type of Offering

- Reagents

- Instruments

- Services

Type of Sample

- Blood, Serum and Plasma

- Urine

- Others

Type of Technology

- Polymerase Chain Reaction (PCR)

- In situ Hybridization

- Isothermal Nucleic Acid Amplification Technology

- Next Generation Sequencing

- Microarrays

- Mass Spectrometry

- Others

Therapeutic Area

- Cardiovascular Diseases

- Genetic Diseases

- Infectious Diseases

- Neurological Diseases

- Oncological Diseases

- Others

End Users

- Hospitals

- Laboratories

- Others

Key Geographical Regions

- North America (US, Canada)

- Europe (Austria, Belgium, France, Germany, Italy, Netherlands, Poland, Spain, Switzerland, UK, Rest of the Europe)

- Asia (China, India, Indonesia, Japan, Singapore, South Korea, Thailand, Rest of Asia)

- Latin America (Argentina, Brazil, Mexico, Rest of Latin America)

- Middle East and North Africa (Egypt, Israel, Saudi Arabia, Rest of Middle East and North Africa)

- Rest of the World (Australia and New Zealand)

MOLECULAR DIAGNOSTICS MARKET: GROWTH AND TRENDS

Molecular diagnostic tests are advanced techniques and tools used to analyze biological markers in the genome and proteome. These diagnostic solutions are essential for detecting and monitoring diseases, identifying genetic abnormalities, and guiding personalized treatment plans. The primary technologies used in the molecular diagnostics domain include polymerase chain reaction, next-generation sequencing and microarrays. While PCR is a highly specific technique that enables the amplification and detection of trace amounts of DNA or RNA, NGS allows for high-throughput sequencing of entire genomes. Thus, molecular diagnostic solutions are pivotal across various medical fields, including oncological disorders, infectious diseases, genetic testing, and personalized medicine. These solutions enhance the accuracy of diagnosis, enable and support tailored treatment strategies aiming to ultimately improve diagnostic outcomes and advancing public health. In addition, it is worth mentioning that more than 70% of the healthcare decisions are made based on laboratory test results, which reflects the importance of such diagnostic tools in patient care.

Further, owing to the several benefits offered by these molecular diagnostic solutions, such as providing rapid testing, reducing turnaround times and enabling quicker decision-making, the market is expected to grow at a healthy compounded annual growth rate (CAGR) during the forecast period.

MOLECULAR DIAGNOSTICS MARKET: KEY INSIGHTS

The report delves into the current state of the molecular diagnostics market and identifies potential growth opportunities within industry. Some key findings from the report include:

- The molecular diagnostic domain features a dynamic market landscape of players that utilize various types of advanced technologies in order to offer a variety of diagnostic applications.

- A number of leading players considered in this analysis were established during 1951 to 2000; 60% of such players are based in North America.

- Owing to its diverse portfolio of molecular diagnostics solutions and strong financial performance in recent fiscal year, Roche emerged as the most competent company among the leading players in this domain.

- In order to study the impact of various trends in the molecular diagnostics market, we developed our proprietary research methodology to analyze different parameters under Porter's Five Forces framework.

- The molecular diagnostics market is fueled by growing awareness towards preventive healthcare; however, factors, such as navigating through regulatory complexities remain significant hurdles for industry players.

- Driven by the increasing prevalence of chronic disorders across the globe, the global molecular diagnostics market is expected to grow at a healthy growth rate of 6.2% during the forecast period.

- The anticipated future opportunity is expected to be well distributed across multiple segments, such as test type, sample type, therapeutic area, and end users.

MOLECULAR DIAGNOSTICS MARKET: KEY SEGMENTS

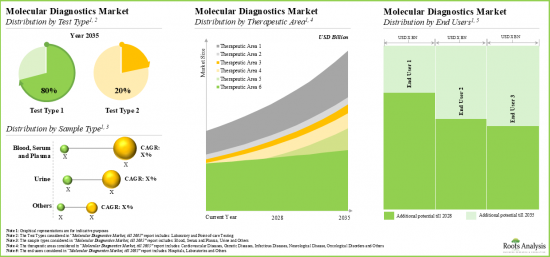

Laboratory Testing Segment holds the Largest Share of the Molecular Diagnostics Market

Based on the test type, the market is segmented into laboratory testing and point-of-care testing. At present, the laboratory testing segment holds the maximum share of the molecular diagnostics market. This trend is likely to remain the same in the coming future. Further, the molecular diagnostics market for point-of-care testing segment is expected to show the highest market growth potential during the forecast period.

By Type of Offering, Reagents is the Fastest Growing Segment of the Global Molecular Diagnostics Market

Based on the type of offering, the market is segmented into reagents, instruments and services. At present, the reagents segment holds the maximum share of the global molecular diagnostics market. Further, owing to the fact that reagents are required to be replenished frequently, which contributes to the recurrent revenues, the market for reagents segment is expected to grow at a higher CAGR during the forecast period.

By Type of Sample, Blood, Serum and Plasma Segment Accounts for the Largest Share of the Global Molecular Diagnostics Market

Based on the type of sample, the market is segmented into blood, serum and plasma, urine, and other samples. Currently, the blood, serum and plasma segment capture the highest proportion of the global molecular diagnostics market. However, the urine segment is expected to grow at a higher CAGR during the forecast period.

The Polymerase Chain Reaction (PCR) Segment by Type of Technology Occupy the Largest Share of the Molecular Diagnostics Market

Based on the type of technology, the market is segmented into Polymerase Chain Reaction (PCR), in situ hybridization, isothermal nucleic acid amplification technology, next generation sequencing, microarrays, mass spectrometry and others. While the polymerase chain reaction (PCR) segment is expected to be the primary driver of the overall market, it is worth highlighting that the global molecular diagnostics market for next generation sequencing segment is likely to grow at a relatively higher CAGR. This can be attributed to the several benefits offered by next generation sequencing, such as high-throughput, improved accuracy, and the capability to simultaneously sequence multiple genes.

By Therapeutic Area, Infectious Disease Segment is Likely to Dominate the Molecular Diagnostics Market

Based on the therapeutic area, the market is segmented into cardiovascular diseases, genetic diseases, infectious diseases, neurological diseases, oncological diseases and others. At present the infectious diseases segment holds the maximum share of the molecular diagnostics market. Additionally, the neurological diseases segment is expected to show the highest growth potential during the forecast period, growing at a higher CAGR, compared to the other segments.

Currently, Hospitals Segment Holds the Largest Share of the Molecular Diagnostics Market

Based on end users, the global market is segmented into hospitals, laboratories, and others. Currently, the hospitals segment holds the largest market share. However, the molecular diagnostics market for laboratories segment is expected to witness substantial growth in the coming years.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and Rest of the World. Currently, North America dominates the global molecular diagnostics market and accounts for the largest revenue share. Further, the market in Asia-Pacific is likely to grow at a higher CAGR in the coming future.

Example Players in the Molecular Diagnostics Market

- Abbott Laboratories

- Agilent Technologies

- Becton Dickinson

- BGI Genomics

- bioMerieux

- Bio-Rad

- Danaher

- DiaSorin

- Grifols

- Hologic

- Illumina

- Qiagen

- QuidelOrtho

- Revvity

- Roche

- Sansure

- Seegene

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

MOLECULAR DIAGNOSTICS MARKET: RESEARCH COVERAGE

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global molecular diagnostics market, focusing on key market segments, including [A] test type, [B] type of offering, [C] type of sample, [D] type of technology, [E] therapeutic area, [F] end users and [D] key geographical regions.

- Market Impact Analysis: A thorough analysis of various factors, such as drivers, restraints, opportunities, and existing challenges that are likely to impact market growth.

- Market Landscape: A comprehensive evaluation of the leading molecular diagnostics companies, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] company ownership and [D] location of the headquarters. Further, the section includes a comprehensive evaluation of molecular diagnostic solutions, focusing on the parameters, such as [A] type of technology used and [B] diagnostic applications.

- Company Competitiveness Analysis: A comprehensive competitive analysis of molecular diagnostic companies, examining factors, such as [A] years of experience and [B] company competitiveness.

- Regulatory Landscape for Medical Devices: A comprehensive discussion of the various guidelines established by major regulatory bodies for medical device approval across different countries. Additionally, a multi-dimensional bubble analysis was done, focusing on the comparison of contemporary regulatory scenario in key geographies across the globe.

- Company Profiles: In-depth profiles of key players that specialize in molecular diagnostic solutions, focusing on [A] overview of the company, [B] financial information, [C] molecular diagnostic offerings and [D] recent developments and an informed future outlook.

- Porter's Five Forces Analysis: A qualitative assessment of Porter's Five Forces framework based on the five competitive forces, including [A] threats to new entrants, [B] bargaining power of product providers, [C] bargaining power of buyers, [D] threat of substitute products and [E] rivalry among existing competitors.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. BACKGROUND

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Project Methodology

- 2.4. Forecast Methodology

- 2.5. Robust Quality Control

- 2.6. Key Market Segmentations

- 2.7. Key Factors

- 2.7.1. Demographics

- 2.7.2. Economic Factors

- 2.7.3. Government Regulations

- 2.7.4. Supply Chain

- 2.7.5. COVID Impact

- 2.7.6. Market Access

- 2.7.7. Healthcare Policies

- 2.7.8. Industry Consolidation

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Market Dynamics

- 3.2.1. Time Period

- 3.2.1.1. Historical Trends

- 3.2.1.2. Current and Future

- 3.2.2. Currency Coverage and Foreign Exchange Rate

- 3.2.2.1. Major Currencies Affecting the Market

- 3.2.2.2. Factors Affecting Currency Fluctuations and Foreign Exchange Rates

- 3.2.2.3. Impact of Foreign Exchange Rate Volatility on the Market

- 3.2.2.4. Strategies for Mitigating Foreign Exchange Risk

- 3.2.3. Trade Policies

- 3.2.3.1. Impact of Trade Barriers on the Market

- 3.2.3.2. Strategies for Mitigating the Risks Associated with Trade Barriers

- 3.2.4. Recession

- 3.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 3.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 3.2.5. Inflation

- 3.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 3.2.5.2. Potential Impact of Inflation on the Market Evolution

- 3.2.1. Time Period

4. EXECUTIVE SUMMARY

5. INTRODUCTION

- 5.1. Overview of Molecular Diagnostics

- 5.2. Key Technologies Employed in Molecular Diagnostic Solution

- 5.3. Challenges in the Molecular Diagnostics Domain

- 5.4. Recent Developments in the Molecular Diagnostics Domain

- 5.5. Future Perspective in the Molecular Diagnostics Domain

6. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 6.1. Market Drivers

- 6.2. Market Restraints

- 6.3. Market Opportunities

- 6.4. Market Challenges

7. GLOBAL MOLECULAR DIAGNOSTICS MARKET

- 7.1. Key Assumptions and Methodology

- 7.2. Global Molecular Diagnostics Market, Till 2035

- 7.2.1. Scenario Analysis

- 7.2.1.1. Conservative Scenario

- 7.2.1.2. Optimistic Scenario

- 7.2.1. Scenario Analysis

8. MOLECULAR DIAGNOSTICS MARKET, BY TEST TYPE

- 8.1. Market Movement Analysis

- 8.2. Molecular Diagnostics Market: Distribution by Test Type

- 8.2.1. Molecular Diagnostics Market for Laboratory Testing, Till 2035

- 8.2.2. Molecular Diagnostics Market for Point-of-Care Testing, Till 2035

9. MOLECULAR DIAGNOSTICS MARKET, BY TYPE OF OFFERING

- 9.1. Market Movement Analysis

- 9.2. Molecular Diagnostics Market: Distribution by Type of Offering

- 9.2.1. Molecular Diagnostics Market for Instruments, Till 2035

- 9.2.1.1. Molecular Diagnostics Market for In-house Instruments, Till 2035

- 9.2.1.2. Molecular Diagnostics Market for Outsourced Instruments, Till 2035

- 9.2.2. Molecular Diagnostics Marlet for Reagents, till 2035

- 9.2.3. Molecular Diagnostics Market for Services, till 2035

- 9.2.1. Molecular Diagnostics Market for Instruments, Till 2035

10. MOLECULAR DIAGNOSTICS MARKET, BY SAMPLE TYPE

- 10.1. Market Movement Analysis

- 10.2. Molecular Diagnostics Market: Distribution by Sample Type

- 10.2.1. Molecular Diagnostics Market for Blood, Serum and Plasma, till 2035

- 10.2.2. Molecular Diagnostics Market for Urine, till 2035

- 10.2.3. Molecular Diagnostics Market for Other Samples, till 2035

11. MOLECULAR DIAGNOSTICS MARKET, BY TYPE OF TECHNOLOGY

- 11.1. Market Movement Analysis

- 11.2. Molecular Diagnostics Market: Distribution by Type of Technology

- 11.2.1. Molecular Diagnostics Market for PCR, till 2035

- 11.2.2. Molecular Diagnostics Market for In Situ Hybridization, till 2035

- 11.2.3. Molecular Diagnostics Market for Isothermal Nucleic Acid Amplification Technology, till 2035

- 11.2.4. Molecular Diagnostics Market for Next Generation Sequencing, till 2035

- 11.2.5. Molecular Diagnostics Market for Microarrays, till 2035

- 11.2.6. Molecular Diagnostics Market for Mass Spectrometry, till 2035

- 11.2.7. Molecular Diagnostics Market for Other Technologies, till 2035

12. MOLECULAR DIAGNOSTICS MARKET, BY THERAPEUTIC AREA

- 12.1. Market Movement Analysis

- 12.2. Molecular Diagnostics Market: Distribution by Therapeutic Area

- 12.2.1. Molecular Diagnostics Market for Infectious Diseases, till 2035

- 12.2.1.1. Molecular Diagnostics Market for COVID-19, till 2035

- 12.2.1.2. Molecular Diagnostics Market for Respiratory Infections (Excluding COVID-19), till 2035

- 12.2.1.3. Molecular Diagnostics Market for Healthcare-associated Infections, till 2035

- 12.2.1.4. Molecular Diagnostics Market for Hepatitis, till 2035

- 12.2.1.5. Molecular Diagnostics Market for HIV, till 2035

- 12.2.1.6. Molecular Diagnostics Market for Sexually Transmitted Diseases, till 2035

- 12.2.1.7. Molecular Diagnostics Market for Other Infectious Diseases, till 2035

- 12.2.2. Molecular Diagnostics Market for Oncological Disorders, till 2035

- 12.2.2.1. Molecular Diagnostics Market for Lung Cancer, till 2035

- 12.2.2.2. Molecular Diagnostics Market for Breast Cancer, till 2035

- 12.2.2.3. Molecular Diagnostics Market for Colorectal Cancer, till 2035

- 12.2.2.4. Molecular Diagnostics Market for Prostate Cancer, till 2035

- 12.2.2.5. Molecular Diagnostics Market for Gastric Cancer, till 2035

- 12.2.2.6. Molecular Diagnostics Market for Other Oncological Disorders, till 2035

- 12.2.3. Molecular Diagnostics Market for Cardiovascular Diseases, till 2035

- 12.2.4. Molecular Diagnostics Market for Neurological Diseases, till 2035

- 12.2.5. Molecular Diagnostics Market for Genetic Diseases, till 2035

- 12.2.6. Molecular Diagnostics Market for Other Therapeutic Areas, till 2035

- 12.2.1. Molecular Diagnostics Market for Infectious Diseases, till 2035

13. MOLECULAR DIAGNOSTICS MARKET, BY END USERS

- 13.1. Market Movement Analysis

- 13.2. Molecular Diagnostics Market: Distribution by End Users

- 13.2.1. Molecular Diagnostics Market for Laboratories, till 2035

- 13.2.1.1. Molecular Diagnostics Market for Large Laboratories, till 2035

- 13.2.1.2. Molecular Diagnostics Market for Small and Medium-sized Laboratories, till 2035

- 13.2.2. Molecular Diagnostics Market for Hospitals, till 2035

- 13.2.3. Molecular Diagnostics Market for Other End Users, till 2035

- 13.2.1. Molecular Diagnostics Market for Laboratories, till 2035

14. MOLECULAR DIAGNOSTICS MARKET, BY GEOGRAPHICAL REGIONS

- 14.1. Market Movement Analysis

- 14.2. Molecular Diagnostics Market: Distribution by Geographical Regions

- 14.2.1. Molecular Diagnostics Market in North America, till 2035

- 14.2.1.1. Molecular Diagnostics Market in the US, till 2035

- 14.2.1.2. Molecular Diagnostics Market in Canada, till 2035

- 14.2.2. Molecular Diagnostics Market in Europe, till 2035

- 14.2.2.1. Molecular Diagnostics Market in Austria, till 2035

- 14.2.2.2. Molecular Diagnostics Market in Belgium, till 2035

- 14.2.2.3. Molecular Diagnostics Market in France, till 2035

- 14.2.2.4. Molecular Diagnostics Market in Germany, till 2035

- 14.2.2.5. Molecular Diagnostics Market in Italy, till 2035

- 14.2.2.6. Molecular Diagnostics Market in the Netherlands, till 2035

- 14.2.2.7. Molecular Diagnostics Market in Poland, till 2035

- 14.2.2.8. Molecular Diagnostics Market in Spain, till 2035

- 14.2.2.9. Molecular Diagnostics Market in Switzerland, till 2035

- 14.2.2.10. Molecular Diagnostics Market in the UK, till 2035

- 14.2.2.11. Molecular Diagnostics Market in the Rest of Europe, till 2035

- 14.2.3. Molecular Diagnostics Market in Asia, till 2035

- 14.2.3.1. Molecular Diagnostics Market in China, till 2035

- 14.2.3.2. Molecular Diagnostics Market in India, till 2035

- 14.2.3.3. Molecular Diagnostics Market in Indonesia, till 2035

- 14.2.3.4. Molecular Diagnostics Market in Japan, till 2035

- 14.2.3.5. Molecular Diagnostics Market in Singapore, till 2035

- 14.2.3.6. Molecular Diagnostics Market in South Korea, till 2035

- 14.2.3.7. Molecular Diagnostics Market in Thailand, till 2035

- 14.2.3.8. Molecular Diagnostics Market in Rest of Asia, till 2035

- 14.2.4. Molecular Diagnostics Market in Latin America, till 2035

- 14.2.4.1. Molecular Diagnostics Market in Brazil, till 2035

- 14.2.4.2. Molecular Diagnostics Market in Argentina, till 2035

- 14.2.4.3. Molecular Diagnostics Market in Mexico, till 2035

- 14.2.4.4. Molecular Diagnostics Market in Rest of Latin America, till 2035

- 14.2.5. Molecular Diagnostics Market in Middle East and North Africa, till 2035

- 14.2.5.1. Molecular Diagnostics Market in Egypt, till 2035

- 14.2.5.2. Molecular Diagnostics Market in Israel, till 2035

- 14.2.5.3. Molecular Diagnostics Market in Saudi Arabia, till 2035

- 14.2.5.4. Molecular Diagnostics Market in the Rest of Middle East and North Africa, till 2035

- 14.2.6. Molecular Diagnostics Market in Rest of the World, till 2035

- 14.2.6.1. Molecular Diagnostics Market in Australia, till 2035

- 14.2.6.2. Molecular Diagnostics Market in New Zealand, till 2035

- 14.2.1. Molecular Diagnostics Market in North America, till 2035

15. MOLECULAR DIAGNOSTICS MARKET, BY LEADING PLAYERS

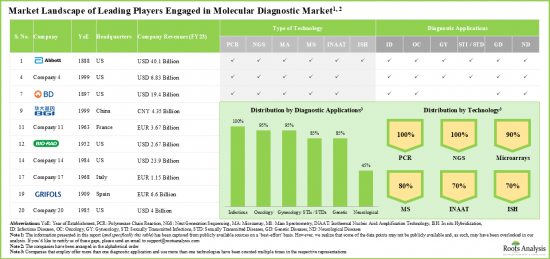

- 15.1. Molecular Diagnostics Market: Distribution of Leading Players by Annual Revenues

16. MARKET OVERVIEW: LEADING MOLECULAR DIAGNOSTIC SOLUTION PROVIDERS

- 16.1. Molecular Diagnostic Solution: Overall Market Landscape

- 16.1.1. Analysis by Type of Technology

- 16.1.2. Analysis by Diagnostic Applications

- 16.1.3. Analysis by Type of Technology and Diagnostic Applications

- 16.2. Molecular Diagnostics: Solution Providers Landscape

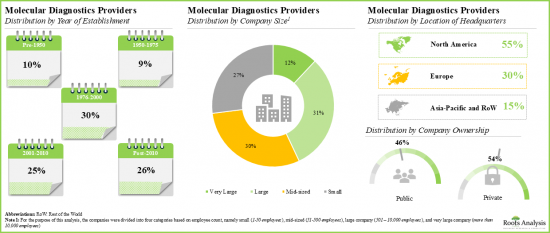

- 16.2.1. Analysis by Year of Establishment

- 16.2.2. Analysis by Company Size

- 16.2.3. Analysis by Location of Headquarters

- 16.2.4. Analysis by Company Ownership

17. COMPANY COMPETITIVENESS ANALYSIS: MOLECULAR DIAGNOSTIC SOLUTION PROVIDERS

- 17.1. Methodology and Key Parameters Assessed

- 17.2. Molecular Diagnostic Solution Providers: Competitiveness Analysis of Very Large Players

- 17.3. Molecular Diagnostic Solution Providers: Competitiveness Analysis of Large Players

- 17.4. Benchmarking Analysis: Leading Molecular Diagnostics Solution Providers

- 17.4.1. Benchmarking of Companies

- 17.4.1.1. Roche: Benchmarking Analysis

- 17.4.1.2. Abbott: Benchmarking Analysis

- 17.4.1.3. Thermo Fisher Scientific: Benchmarking Analysis

- 17.4.1.4. Qiagen: Benchmarking Analysis

- 17.4.1.5. bioMerieux: Benchmarking Analysis

- 17.4.1.6. DiaSorin: Benchmarking Analysis

- 17.4.1.7. Illumina: Benchmarking Analysis

- 17.4.1.8. Sysmex: Benchmarking Analysis

- 17.4.1.9. Perkin Elmer: Benchmarking Analysis

- 17.4.1.10. Bio-Rad: Benchmarking Analysis

- 17.4.2. Benchmarking of Parameters

- 17.4.2.1. Leading Molecular Diagnostics Solution Providers: Benchmarking by Competitiveness

- 17.4.2.2. Leading Molecular Diagnostic Solution Providers: Benchmarking by Type of Technology Score

- 17.4.2.3. Leading Molecular Diagnostic Solution Providers: Benchmarking by Diagnostic Applications Score

- 17.4.1. Benchmarking of Companies

18. COMPANY PROFILES: MOLECULAR DIAGNOSTICS SOLUTION PROVIDERS BASED IN NORTH AMERICA

- 18.1. Detailed Company Profiles

- 18.1.1. Abbott

- 18.1.1.1. Company Overview

- 18.1.1.2. Product Portfolio

- 18.1.1.3. Financial Information

- 18.1.1.4. Recent Developments and Future Outlook

- 18.1.2. Agilent Technologies

- 18.1.3. BD

- 18.1.4. Danaher

- 18.1.5. Thermo Fisher Scientific

- 18.1.1. Abbott

- 18.2. Short Company Profiles

- 18.2.1. Bio-Rad

- 18.2.1.1. Company Overview

- 18.2.1.2. Product Portfolio

- 18.2.2. Illumina

- 18.2.3. Hologic

- 18.2.4. PerkinElmer

- 18.2.5. QuidelOrtho

- 18.2.1. Bio-Rad

19. COMPANY PROFILES: MOLECULAR DIAGNOSTICS SOLUTION PROVIDERS BASED IN EUROPE

- 19.1. Detailed Company Profiles

- 19.1.1. bioMerieux

- 19.1.1.1. Company Overview

- 19.1.1.2. Product Portfolio

- 19.1.1.3. Financial Information

- 19.1.1.4. Recent Developments and Future Outlook

- 19.1.2. Grifols

- 19.1.3. Roche

- 19.1.4. Siemens Healthineers

- 19.1.1. bioMerieux

- 19.2. Brief Company Profiles

- 19.2.1. DiaSorin

- 19.2.1.1. Company Overview

- 19.2.1.2. Product Portfolio

- 19.2.2. Qiagen

- 19.2.1. DiaSorin

20. COMPANY PROFILES: MOLECULAR DIAGNOSTICS SOLUTION PROVIDERS BASED IN ASIA

- 20.1. Detailed Company Profiles

- 20.1.1. Sysmex

- 20.1.1.1. Company Overview

- 20.1.1.2. Product Portfolio

- 20.1.1.3. Financial Information

- 20.1.1.4. Recent Developments and Future Outlook

- 20.1.1. Sysmex

- 20.2. Brief Company Profiles

- 20.2.1. BGI Genomics

- 20.2.1.1. Company Overview

- 20.2.1.2. Product Portfolio

- 20.2.2. Sansure

- 20.2.3. Seegene

- 20.2.1. BGI Genomics

21. PORTER'S FIVE FORCES ANALYSIS

- 21.1. Methodology and Assumptions

- 21.2. Key Parameters

- 21.2.1. Threats of New Entrants

- 21.2.2. Bargaining Power of Buyers

- 21.2.3. Bargaining Power of Suppliers

- 21.2.4. Threats of Substitute Products

- 21.2.5. Rivalry among Existing Competitors

- 21.3. Porter's Five Force Analysis: Harvey Ball Analysis

- 21.4. Concluding Remarks

22. APPENDIX I: TABULATED DATA

23. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 16.1 Leading Molecular Diagnostics Solution Providers: Information on Year of Establishment, Headquarters, Company Ownership, Type of Technology and Diagnostic Applications

- Table 16.2 Other Leading Molecular Diagnostics Solution Providers: Information on Year of Establishment, Headquarters and Company Ownership

- Table 18.1 Abbott: Company Overview

- Table 18.2 Abbott: Product Portfolio

- Table 18.3 Abbott: Recent Developments and Future Outlook

- Table 18.4 Agilent Technologies: Company Overview

- Table 18.5 Agilent Technologies: Product Portfolio

- Table 18.6 Agilent Technologies: Recent Developments and Future Outlook

- Table 18.7 BD: Company Overview

- Table 18.8 BD: Product Portfolio

- Table 18.9 BD: Recent Developments and Future Outlook

- Table 18.10 Danaher: Company Overview

- Table 18.11 Danaher: Product Portfolio

- Table 18.12 Danaher: Recent Developments and Future Outlook

- Table 18.13 Roche: Company Overview

- Table 18.14 Roche: Product Portfolio

- Table 18.15 Roche: Recent Developments and Future Outlook

- Table 18.16 Thermo Fisher Scientific: Company Overview

- Table 18.17 Thermo Fisher Scientific: Product Portfolio

- Table 18.18 Thermo Fisher Scientific: Recent Developments and Future Outlook

- Table 18.19 Bio-Rad: Company Overview

- Table 18.20 Bio-Rad: Product Portfolio

- Table 18.21 Illumina: Company Overview

- Table 18.22 Illumina: Product Portfolio

- Table 18.23 Hologic: Company Overview

- Table 18.24 Hologic: Product Portfolio

- Table 18.25 PerkinElmer: Company Overview

- Table 18.26 PerkinElmer: Product Portfolio

- Table 18.27 QuidelOrtho: Company Overview

- Table 18.28 QuidelOrtho: Product Portfolio

- Table 19.1 bioMerieux: Company Overview

- Table 19.2 bioMerieux: Product Portfolio

- Table 19.3 bioMerieux: Recent Developments and Future Outlook

- Table 19.4 Grifols: Company Overview

- Table 19.5 Grifols: Product Portfolio

- Table 19.6 Grifols: Recent Developments and Future Outlook

- Table 19.7 Siemens Healthineers: Company Overview

- Table 19.8 Siemens Healthineers: Product Portfolio

- Table 19.9 Siemens Healthineers: Recent Developments and Future Outlook

- Table 19.10 DiaSorin: Company Overview

- Table 19.11 DiaSorin: Product Portfolio

- Table 19.12 Qiagen: Company Overview

- Table 19.13 Qiagen: Product Portfolio

- Table 20.1 Sysmex: Company Overview

- Table 20.2 Sysmex: Product Portfolio

- Table 20.3 Sysmex: Recent Developments and Future Outlook

- Table 20.4 BGI Genomics: Company Overview

- Table 20.5 BGI Genomics: Product Portfolio

- Table 20.6 Sansure: Company Overview

- Table 20.7 Sansure: Product Portfolio

- Table 20.8 Seegene: Company Overview

- Table 20.9 Seegene: Product Portfolio

- Table 22.1 Global Molecular Diagnostics Market, Till 2035 (USD Billion)

- Table 22.2 Global Molecular Diagnostics Market, Conservative Scenario, till 2035 (USD Billion)

- Table 22.3 Global Molecular Diagnostics Market, Optimistic Scenario, till 2035 (USD Billion)

- Table 22.4 Molecular Diagnostics Market: Distribution by Test Type

- Table 22.5 Molecular Diagnostics Market for Laboratory Testing, Till 2035 (USD Billion)

- Table 22.6 Molecular Diagnostics Market for Point-of-Care Testing, Till 2035 (USD Billion)

- Table 22.7 Molecular Diagnostics Market: Distribution by Type of Offering

- Table 22.8 Molecular Diagnostics Market for Instruments, Till 2035 (USD Billion)

- Table 22.9 Molecular Diagnostics Market for In-house Instruments, Till 2035 (USD Billion)

- Table 22.10 Molecular Diagnostics Market for Outsourced Instruments, Till 2035 (USD Billion)

- Table 22.11 Molecular Diagnostics Market for Reagents, Till 2035 (USD Billion)

- Table 22.12 Molecular Diagnostics Market for Services, Till 2035 (USD Billion)

- Table 22.13 Molecular Diagnostics Market: Distribution by Sample Type

- Table 22.14 Molecular Diagnostics Market for Blood, Serum and Plasma, Till 2035 (USD Billion)

- Table 22.15 Molecular Diagnostics Market for Urine, Till 2035 (USD Billion)

- Table 22.16 Molecular Diagnostics Market for Others, Till 2035 (USD Billion)

- Table 22.17 Molecular Diagnostics Market: Distribution by Type of Technology

- Table 22.18 Molecular Diagnostics Market for PCR, Till 2035 (USD Billion)

- Table 22.19 Molecular Diagnostics Market for In situ Hybridization, Till 2035 (USD Billion)

- Table 22.20 Molecular Diagnostics Market for Isothermal Nucleic Acid Amplification Technology, Till 2035 (USD Billion)

- Table 22.21 Molecular Diagnostics Market for Next Generation Sequencing, Till 2035 (USD Billion)

- Table 22.22 Molecular Diagnostics Market for Microarrays, Till 2035 (USD Billion)

- Table 22.23 Molecular Diagnostics Market for Mass Spectrometry, Till 2035 (USD Billion)

- Table 22.24 Molecular Diagnostics Market for Other Technologies, Till 2035 (USD Billion)

- Table 22.25 Molecular Diagnostics Market: Distribution by Therapeutic Area

- Table 22.26 Molecular Diagnostics Market for Infectious Diseases, Till 2035 (USD Billion)

- Table 22.27 Molecular Diagnostics Market for COVID-19, Till 2035 (USD Billion)

- Table 22.28 Molecular Diagnostics Market for Respiratory Infections (Excluding COVID-19), Till 2035 (USD Billion)

- Table 22.29 Molecular Diagnostics Market for Healthcare-associated Infections, Till 2035 (USD Billion)

- Table 22.30 Molecular Diagnostics Market for Hepatitis, Till 2035 (USD Billion)

- Table 22.31 Molecular Diagnostics Market for HIV, Till 2035 (USD Billion)

- Table 22.32 Molecular Diagnostics Market for Sexually Transmitted Diseases, Till 2035 (USD Billion)

- Table 22.33 Molecular Diagnostics Market for Other Infectious Diseases, Till 2035 (USD Billion)

- Table 22.34 Molecular Diagnostics Market for Oncological Disorders, Till 2035 (USD Billion)

- Table 22.35 Molecular Diagnostics Market for Lung Cancer, Till 2035 (USD Billion)

- Table 22.36 Molecular Diagnostics Market for Breast Cancer, Till 2035 (USD Billion)

- Table 22.37 Molecular Diagnostics Market for Colorectal Cancer, Till 2035 (USD Billion)

- Table 22.38 Molecular Diagnostics Market for Prostate Cancer, Till 2035 (USD Billion)

- Table 22.39 Molecular Diagnostics Market for Gastric Cancer, Till 2035 (USD Billion)

- Table 22.40 Molecular Diagnostics Market for Other Oncological Disorders, Till 2035 (USD Billion)

- Table 22.41 Molecular Diagnostics Market for Cardiovascular Diseases, Till 2035 (USD Billion)

- Table 22.42 Molecular Diagnostics Market for Neurological Diseases, Till 2035 (USD Billion)

- Table 22.43 Molecular Diagnostics Market for Genetic Diseases, Till 2035 (USD Billion)

- Table 22.44 Molecular Diagnostics Market for Other Therapeutic Areas, Till 2035 (USD Billion)

- Table 22.45 Molecular Diagnostics Market: Distribution by End Users

- Table 22.46 Molecular Diagnostics Market for Laboratories, Till 2035 (USD Billion)

- Table 22.47 Molecular Diagnostics Market for Large Laboratories, Till 2035 (USD Billion)

- Table 22.48 Molecular Diagnostics Market for Small and Medium-sized Laboratories, Till 2035 (USD Billion)

- Table 22.49 Molecular Diagnostics Market for Hospitals, Till 2035 (USD Billion)

- Table 22.50 Molecular Diagnostics Market for Other End Users, Till 2035 (USD Billion)

- Table 22.51 Molecular Diagnostics Market: Distribution by Geographical Regions

- Table 22.52 Molecular Diagnostics Market in North America, Till 2035 (USD Billion)

- Table 22.53 Molecular Diagnostics Market in the US, Till 2035 (USD Billion)

- Table 22.54 Molecular Diagnostics Market in Canada, Till 2035 (USD Billion)

- Table 22.55 Molecular Diagnostics Market in Europe, Till 2035 (USD Billion)

- Table 22.56 Molecular Diagnostics Market in Austria, Till 2035 (USD Billion)

- Table 22.57 Molecular Diagnostics Market in Belgium, Till 2035 (USD Billion)

- Table 22.58 Molecular Diagnostics Market in France, Till 2035 (USD Billion)

- Table 22.59 Molecular Diagnostics Market in Germany, Till 2035 (USD Billion)

- Table 22.60 Molecular Diagnostics Market in Italy, Till 2035 (USD Billion)

- Table 22.61 Molecular Diagnostics Market in the Netherlands, Till 2035 (USD Billion)

- Table 22.62 Molecular Diagnostics Market in Poland, Till 2035 (USD Billion)

- Table 22.63 Molecular Diagnostics Market in Spain, Till 2035 (USD Billion)

- Table 22.64 Molecular Diagnostics Market in Switzerland, Till 2035 (USD Billion)

- Table 22.65 Molecular Diagnostics Market in the UK, Till 2035 (USD Billion)

- Table 22.66 Molecular Diagnostics Market in Rest of the Europe, Till 2035 (USD Billion)

- Table 22.67 Molecular Diagnostics Market in Asia, Till 2035 (USD Billion)

- Table 22.68 Molecular Diagnostics Market in China, Till 2035 (USD Billion)

- Table 22.69 Molecular Diagnostics Market in India, Till 2035 (USD Billion)

- Table 22.70 Molecular Diagnostics Market in Indonesia, Till 2035 (USD Billion)

- Table 22.71 Molecular Diagnostics Market in Japan, Till 2035 (USD Billion)

- Table 22.72 Molecular Diagnostics Market in Singapore, Till 2035 (USD Billion)

- Table 22.73 Molecular Diagnostics Market in South Korea, Till 2035 (USD Billion)

- Table 22.74 Molecular Diagnostics Market in Thailand, Till 2035 (USD Billion)

- Table 22.75 Molecular Diagnostics Market in Rest of Asia, Till 2035 (USD Billion)

- Table 22.76 Molecular Diagnostics Market in Latin America, Till 2035 (USD Billion)

- Table 22.77 Molecular Diagnostics Market in Brazil, Till 2035 (USD Billion)

- Table 22.78 Molecular Diagnostics Market in Argentina, Till 2035 (USD Billion)

- Table 22.79 Molecular Diagnostics Market in Mexico, Till 2035 (USD Billion)

- Table 22.80 Molecular Diagnostics Market in Rest of Latin America, Till 2035 (USD Billion)

- Table 22.81 Molecular Diagnostics Market in Middle East and North Africa, Till 2035 (USD Billion)

- Table 22.82 Molecular Diagnostics Market in Egypt, Till 2035 (USD Billion)

- Table 22.83 Molecular Diagnostics Market in Israel, Till 2035 (USD Billion)

- Table 22.84 Molecular Diagnostics Market in Saudi Arabia, Till 2035 (USD Billion)

- Table 22.85 Molecular Diagnostics Market in Rest of Middle East and North Africa, Till 2035 (USD Billion)

- Table 22.86 Molecular Diagnostics Market in Rest of the World, Till 2035 (USD Billion)

- Table 22.87 Molecular Diagnostics Market in Australia, Till 2035 (USD Billion)

- Table 22.88 Molecular Diagnostics Market in New Zealand, Till 2035 (USD Billion)

- Table 22.89 Molecular Diagnostics Market: Distribution of Leading Players by Annual Revenues (FY23, USD Billion

- Table 22.90 Molecular Diagnostic Solution: Distribution by Type of Technology

- Table 22.91 Molecular Diagnostic Solution: Distribution by Diagnostic Applications

- Table 22.92 Molecular Diagnostic Solution: Distribution by Type of Technology and Diagnostic Applications

- Table 22.93 Molecular Diagnostics Solution Providers: Distribution by Year of Establishment

- Table 22.94 Molecular Diagnostics Solution Providers: Distribution by Company Size

- Table 22.95 Molecular Diagnostics Solution Providers: Distribution by Location of Headquarters

- Table 22.96 Molecular Diagnostics Solution Providers: Distribution by Company Ownership

- Table 22.97 Abbott: Financial Information (USD Billion)

- Table 22.98 Agilent Technologies: Financial Information (USD Billion)

- Table 22.99 BD: Financial Information (USD Billion)

- Table 22.100 Danaher: Financial Information (USD Billion)

- Table 22.101 Thermo Fisher Scientific: Financial Information (CHF Billion)

- Table 22.102 bioMerieux: Financial Information (EUR Billion)

- Table 22.103 Grifols: Financial Information (EUR Billion)

- Table 22.104 Roche: Financial Information (CHF Billion)

- Table 22.105 Siemens Healthineers: Financial Information (EUR Billion)

- Table 22.106 Sysmex: Financial Information (JPY Billion)

List of Figures

- Figure 2.1 Research Methodology: Research Assumptions

- Figure 2.2 Research Methodology: Project Methodology

- Figure 2.3 Research Methodology: Forecast Methodology

- Figure 2.4 Research Methodology: Robust Quality Control

- Figure 2.5 Research Methodology: Key Market Segmentations

- Figure 5.1 Key Technologies Employed in Molecular Diagnostic Solution

- Figure 5.2 Challenges in the Molecular Diagnostics Domain

- Figure 6.1 Market Drivers

- Figure 6.2 Market Restraints

- Figure 6.3 Market Opportunities

- Figure 6.4 Market Challenges

- Figure 7.1 Global Molecular Diagnostics Market, Till 2035 (USD Billion)

- Figure 7.2 Global Molecular Diagnostics Market, Conservative Scenario, Till 2035 (USD Billion)

- Figure 7.3 Global Molecular Diagnostics Market, Optimistic Scenario, Till 2035 (USD Billion)

- Figure 8.1 Molecular Diagnostics Market: Distribution by Test Type

- Figure 8.2 Molecular Diagnostics Market for Laboratory Testing, Till 2035 (USD Billion)

- Figure 8.3 Molecular Diagnostics Market for Point-of-Care Testing, Till 2035 (USD Billion)

- Figure 9.1 Molecular Diagnostics Market: Distribution by Type of Offering

- Figure 9.2 Molecular Diagnostics Market for Instruments, Till 2035 (USD Billion)

- Figure 9.3 Molecular Diagnostics Market for In-house Instruments, Till 2035 (USD Billion)

- Figure 9.4 Molecular Diagnostics Market for Outsourced Instruments, Till 2035 (USD Billion)

- Figure 9.5 Molecular Diagnostics Market for Reagents, Till 2035 (USD Billion)

- Figure 9.6 Molecular Diagnostics Market for Services, Till 2035 (USD Billion)

- Figure 10.1 Molecular Diagnostics Market: Distribution by Sample Type

- Figure 10.2 Molecular Diagnostics Market for Blood, Serum and Plasma, Till 2035 (USD Billion)

- Figure 10.3 Molecular Diagnostics Market for Urine, Till 2035 (USD Billion)

- Figure 10.4 Molecular Diagnostics Market for Others, Till 2035 (USD Billion)

- Figure 11.1 Molecular Diagnostics Market: Distribution by Type of Technology

- Figure 11.2 Molecular Diagnostics Market for PCR, Till 2035 (USD Billion)

- Figure 11.3 Molecular Diagnostics Market for In Situ Hybridization, Till 2035 (USD Billion)

- Figure 11.4 Molecular Diagnostics Market for Isothermal Nucleic Acid Amplification Technology, Till 2035 (USD Billion)

- Figure 11.5 Molecular Diagnostics Market for Next Generation Sequencing, Till 2035 (USD Billion)

- Figure 11.6 Molecular Diagnostics Market for Microarrays, Till 2035 (USD Billion)

- Figure 11.7 Molecular Diagnostics Market for Mass Spectrometry, Till 2035 (USD Billion)

- Figure 11.8 Molecular Diagnostics Market for Other Technologies, Till 2035 (USD Billion)

- Figure 12.1 Molecular Diagnostics Market: Distribution by Therapeutic Area

- Figure 12.2 Molecular Diagnostics Market for Infectious Diseases, Till 2035 (USD Billion)

- Figure 12.3 Molecular Diagnostics Market for COVID-19, Till 2035 (USD Billion)

- Figure 12.4 Molecular Diagnostics Market for Respiratory Infections (Excluding COVID-19), Till 2035 (USD Billion)

- Figure 12.5 Molecular Diagnostics Market for Healthcare-associated Infections, Till 2035 (USD Billion)

- Figure 12.6 Molecular Diagnostics Market for Hepatitis, Till 2035 (USD Billion)

- Figure 12.7 Molecular Diagnostics Market for HIV, Till 2035 (USD Billion)

- Figure 12.8 Molecular Diagnostics Market for Sexually Transmitted Diseases, Till 2035 (USD Billion)

- Figure 12.9 Molecular Diagnostics Market for Other Infectious Diseases, Till 2035 (USD Billion)

- Figure 12.10 Molecular Diagnostics Market for Oncological Disorders, Till 2035 (USD Billion)

- Figure 12.11 Molecular Diagnostics Market for Lung Cancer, Till 2035 (USD Billion)

- Figure 12.12 Molecular Diagnostics Market for Breast Cancer, Till 2035 (USD Billion)

- Figure 12.13 Molecular Diagnostics Market for Colorectal Cancer, Till 2035 (USD Billion)

- Figure 12.14 Molecular Diagnostics Market for Prostate Cancer, Till 2035 (USD Billion)

- Figure 12.15 Molecular Diagnostics Market for Gastric Cancer, Till 2035 (USD Billion)

- Figure 12.16 Molecular Diagnostics Market for Other Oncological Disorders, Till 2035 (USD Billion)

- Figure 12.17 Molecular Diagnostics Market for Cardiovascular Diseases, Till 2035 (USD Billion)

- Figure 12.18 Molecular Diagnostics Market for Neurological Diseases, Till 2035 (USD Billion)

- Figure 12.19 Molecular Diagnostics Market for Genetic Diseases, Till 2035 (USD Billion)

- Figure 12.20 Molecular Diagnostics Market for Other Therapeutic Areas, Till 2035 (USD Billion)

- Figure 13.1 Molecular Diagnostics Market: Distribution by End Users

- Figure 13.2 Molecular Diagnostics Market for Laboratories, Till 2035 (USD Billion)

- Figure 13.3 Molecular Diagnostics Market for Large Laboratories, Till 2035 (USD Billion)

- Figure 13.4 Molecular Diagnostics Market for Small and Medium-sized Laboratories, Till 2035 (USD Billion)

- Figure 13.5 Molecular Diagnostics Market for Hospitals, Till 2035 (USD Billion)

- Figure 13.6 Molecular Diagnostics Market for Other End Users, Till 2035 (USD Billion)

- Figure 14.1 Molecular Diagnostics Market: Distribution by Geographical Regions

- Figure 14.2 Molecular Diagnostics Market in North America, Till 2035 (USD Billion)

- Figure 14.3 Molecular Diagnostics Market in the US, Till 2035 (USD Billion)

- Figure 14.4 Molecular Diagnostics Market in Canada, Till 2035 (USD Billion)

- Figure 14.5 Molecular Diagnostics Market in Europe, Till 2035 (USD Billion)

- Figure 14.6 Molecular Diagnostics Market in Austria, Till 2035 (USD Billion)

- Figure 14.7 Molecular Diagnostics Market in Belgium, Till 2035 (USD Billion)

- Figure 14.8 Molecular Diagnostics Market in France, Till 2035 (USD Billion)

- Figure 14.9 Molecular Diagnostics Market in Germany, Till 2035 (USD Billion)

- Figure 14.10 Molecular Diagnostics Market in Italy, Till 2035 (USD Billion)

- Figure 14.11 Molecular Diagnostics Market in the Netherlands, Till 2035 (USD Billion)

- Figure 14.12 Molecular Diagnostics Market in Poland, Till 2035 (USD Billion)

- Figure 14.13 Molecular Diagnostics Market in Spain, Till 2035 (USD Billion)

- Figure 14.14 Molecular Diagnostics Market in Switzerland, Till 2035 (USD Billion)

- Figure 14.15 Molecular Diagnostics Market in the UK, Till 2035 (USD Billion)

- Figure 14.16 Molecular Diagnostics Market in Rest of Europe, Till 2035 (USD Billion)

- Figure 14.17 Molecular Diagnostics Market in Asia, Till 2035 (USD Billion)

- Figure 14.18 Molecular Diagnostics Market in China, Till 2035 (USD Billion)

- Figure 14.19 Molecular Diagnostics Market in India, Till 2035 (USD Billion)

- Figure 14.20 Molecular Diagnostics Market in Indonesia, Till 2035 (USD Billion)

- Figure 14.21 Molecular Diagnostics Market in Japan, Till 2035 (USD Billion)

- Figure 14.22 Molecular Diagnostics Market in Singapore, Till 2035 (USD Billion)

- Figure 14.23 Molecular Diagnostics Market in South Korea, Till 2035 (USD Billion)

- Figure 14.24 Molecular Diagnostics Market in Thailand, Till 2035 (USD Billion)

- Figure 14.25 Molecular Diagnostics Market in Rest of the Asia, Till 2035 (USD Billion)

- Figure 14.26 Molecular Diagnostics Market in Latin America, Till 2035 (USD Billion)

- Figure 14.27 Molecular Diagnostics Market in Brazil, Till 2035 (USD Billion)

- Figure 14.28 Molecular Diagnostics Market in Argentina, Till 2035 (USD Billion)

- Figure 14.29 Molecular Diagnostics Market in Mexico, Till 2035 (USD Billion)

- Figure 14.30 Molecular Diagnostics Market in Rest of Latin America, Till 2035 (USD Billion)

- Figure 14.31 Molecular Diagnostics Market in Middle East and North Africa, Till 2035 (USD Billion)

- Figure 14.32 Molecular Diagnostics Market in Egypt, Till 2035 (USD Billion)

- Figure 14.33 Molecular Diagnostics Market in Israel, Till 2035 (USD Billion)

- Figure 14.34 Molecular Diagnostics Market in Saudi Arabia, Till 2035 (USD Billion)

- Figure 14.35 Molecular Diagnostics Market in Rest of Middle East and North Africa, Till 2035 (USD Billion)

- Figure 14.36 Molecular Diagnostics Market in Rest of the World, Till 2035 (USD Billion)

- Figure 14.37 Molecular Diagnostics Market in Australia, Till 2035 (USD Billion)

- Figure 14.38 Molecular Diagnostics Market in New Zealand, Till 2035 (USD Billion)

- Figure 15.1 Molecular Diagnostics Market: Distribution of Leading Players by Annual Revenue (FY23, USD Billion)

- Figure 16.1 Molecular Diagnostic Solution: Distribution by Type of Technology

- Figure 16.2 Molecular Diagnostic Solution: Distribution by Diagnostic Applications

- Figure 16.3 Molecular Diagnostic Solution: Distribution by Type of Technology and Diagnostic Applications

- Figure 16.4 Molecular Diagnostics Solution Providers: Distribution by Year of Establishment

- Figure 16.5 Molecular Diagnostics Solution Providers: Distribution by Company Size

- Figure 16.6 Molecular Diagnostics Solution Providers: Distribution by Location of Headquarters

- Figure 16.7 Molecular Diagnostics Solution Providers: Distribution by Company Ownership

- Figure 17.1 Molecular Diagnostic Solution Providers: Competitiveness Analysis of Very Large Players

- Figure 17.2 Molecular Diagnostic Solution Providers: Competitiveness Analysis of Large Players

- Figure 17.3 Roche: Benchmarking Analysis

- Figure 17.4 Abbott: Benchmarking Analysis

- Figure 17.5 Thermo Fisher Scientific: Benchmarking Analysis

- Figure 17.6 Qiagen: Benchmarking Analysis

- Figure 17.7 bioMerieux: Benchmarking Analysis

- Figure 17.8 DiaSorin: Benchmarking Analysis

- Figure 17.9 Illumina: Benchmarking Analysis

- Figure 17.10 Sysmex: Benchmarking Analysis

- Figure 17.11 Perkin Elmer: Benchmarking Analysis

- Figure 17.12 Bio-Rad: Benchmarking Analysis

- Figure 17.13 Leading Molecular Diagnostic Solution Providers: Benchmarking by Competitiveness

- Figure 17.14 Leading Molecular Diagnostic Solution Providers: Benchmarking by Type of Technology Score

- Figure 17.15 Leading Molecular Diagnostic Solution Providers: Benchmarking by Diagnostic Applications Score

- Figure 18.1 Abbott: Financial Information (USD Billion)

- Figure 18.2 Agilent Technologies: Financial Information (USD Billion)

- Figure 18.3 BD: Financial Information (USD Billion)

- Figure 18.4 Danaher: Financial Information (USD Billion)

- Figure 18.5 Thermo Fisher Scientific: Financial Information (CHF Billion)

- Figure 19.1 bioMerieux: Financial Information (EUR Billion)

- Figure 19.2 Grifols: Financial Information (EUR Billion)

- Figure 19.3 Roche: Financial Information (CHF Billion)

- Figure 19.4 Siemens Healthineers: Financial Information (EUR Billion)

- Figure 20.1 Sysmex: Financial Information (JPY Billion)

- Figure 21.1 Threats of New Entrants

- Figure 21.2 Bargaining Power of Buyers

- Figure 21.3 Bargaining Power of Suppliers

- Figure 21.4 Threats of Substitute Products

- Figure 21.5 Rivalry among Existing Competitors

- Figure 21.6 Porter's Five Force Analysis: Harvey Ball Analysis

分子診斷原料市場規模、佔有率和成長分析:按產品類型、技術、應用、最終用戶和地區分類-2026-2033年產業預測

分子診斷原料市場規模、佔有率和成長分析:按產品類型、技術、應用、最終用戶和地區分類-2026-2033年產業預測 2026年全球分子診斷設備與儀器市場報告2026年全球性行為感染傳染病分子診斷市場報告

2026年全球分子診斷設備與儀器市場報告2026年全球性行為感染傳染病分子診斷市場報告 日本分子診斷市場報告:按產品、技術、應用、最終用戶和地區分類(2026-2034年)

日本分子診斷市場報告:按產品、技術、應用、最終用戶和地區分類(2026-2034年) 全球分子診斷市場(第14版)

全球分子診斷市場(第14版) 核心臨床分子診斷市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、技術、應用、最終用戶、地區及競爭格局分類,2021-2031年)

核心臨床分子診斷市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、技術、應用、最終用戶、地區及競爭格局分類,2021-2031年) 2026-2030年全球分子診斷市場

2026-2030年全球分子診斷市場 臨床和分子診斷人工智慧市場(按產品類型、技術、應用、最終用戶和測試環境分類),全球預測(2026-2032年)

臨床和分子診斷人工智慧市場(按產品類型、技術、應用、最終用戶和測試環境分類),全球預測(2026-2032年) 分子診斷市場規模、佔有率和成長分析(按產品類型、檢測類型、檢體類型、技術、應用、最終用戶和地區分類)-2026-2033年產業預測

分子診斷市場規模、佔有率和成長分析(按產品類型、檢測類型、檢體類型、技術、應用、最終用戶和地區分類)-2026-2033年產業預測 分子診斷市場規模、佔有率和趨勢分析報告:按產品、檢測地點、技術、應用、地區和細分市場預測,2026-2033年

分子診斷市場規模、佔有率和趨勢分析報告:按產品、檢測地點、技術、應用、地區和細分市場預測,2026-2033年