|

市場調查報告書

商品編碼

2073632

北美工業空氣污染控制系統:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Industrial Air Quality Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

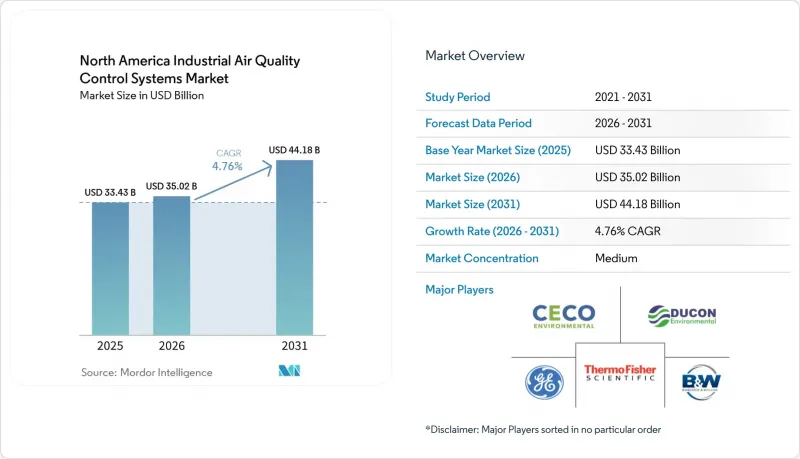

根據 Mordor Intelligence 預測,北美工業空氣污染控制系統市場規模將從 2025 年的 334.3 億美元成長到 2026 年的 350.2 億美元,然後在 2031 年達到 441.8 億美元,2026 年至 2031 年的複合年成長率為 4.76%。

本報告按類型(靜電除塵器、排煙脫硫系統、洗滌器等)、目標污染物(顆粒物、硫氧化物、氮氧化物、揮發性有機化合物等)、終端用戶產業(發電、水泥、鋼鐵、化學和石化等)和地區(美國、加拿大、墨西哥)進行細分。市場預測以美元計價。

北美工業空氣污染控制系統市場趨勢與洞察

對 PM2.5 和臭氧的更嚴格監管正在重塑授權的經濟結構。

2024年2月,美國環保署(EPA)將PM2.5一次排放的年平均基準值降低至9.0微克/立方公尺。此舉立即收緊了大規模工業排放源的監管合規要求。這項變化減少了許多企業在規劃工廠擴建或許可證續約時所依賴的營運裕度。先前只需進行有限的排放排放不達標,被重新分類為「中度」污染區和「重度」污染區,進一步加劇了壓力。這項變更將主要排放源的閾值降低至每年 50 噸,並將 RACT(相對可實現的最佳技術)義務的截止日期提前至 2026 年。在北美空氣品質管理系統市場,這些法規的協同效應正在將對過濾器、洗滌器和氮氧化物 (NOx) 控制的投資納入當前的資本投資計畫週期。

石油和天然氣產業甲烷和硫控制技術的升級,擴大了對多種污染物控制措施的需求。

2024年3月,美國環保署(EPA)最終確定了石油和天然氣產業甲烷和揮發性有機化合物(VOC)排放的大規模監管方案。這是影響重工業排放設備最重大的合規性變更之一。該法規涵蓋了美國28%的人為甲烷排放和23%的人為VOC排放。法規要求部署零排放氣動控制器,在多井場進行季度光學氣體成像,並將某些脫硫裝置的二氧化硫(SO2)排放減少99.9%。這正在促使採購行為發生轉變,天然氣加工和煉油設施擴大將脫硫、蒸氣回收、氮氧化物(NOx)減排和連續監測納入單一投資週期進行評估,而不是作為單獨的項目。加拿大也正在加強對大型排放的工業排放法規,這有助於擴大區域空氣污染控制設備的採購基礎。因此,在北美空氣污染控制系統市場,包括墨西哥灣沿岸、二疊紀盆地、亞伯達和不列顛哥倫比亞省,對多污染物防護產品的需求正在增加。

燃煤發電廠的退役減少了對現有設施維修的需求,但這種減少的速度並不平衡。

燃煤發電廠的退役正在減少洗滌器、選擇性催化還原(SCR)系統和顆粒物控制設備翻新維修這一歷史悠久且最穩定的經常性收入來源之一。傳統上,燃煤發電廠需要頻繁升級改造以符合相關法規,這為售後市場和替換需求提供了可靠的來源。隨著老舊機組退出電網,中西部、阿巴拉契亞地區、東南部以及加拿大部分地區的興建電廠數量正在減少。然而,這種下降趨勢並不均衡,因為一些老舊機組由於可靠性問題和燃料價格波動,仍在比預期更長的時間內繼續運作。這種不均衡的退役模式意味著,儘管對煤炭的依賴程度總體下降,但催化劑更換、布袋除塵器維護和洗滌器維護仍然是電廠基礎設施的一部分。對於北美空氣污染控制系統市場而言,這種影響並非電力產業需求的突然崩壞,而是需求結構逐漸向天然氣、垃圾焚化發電和碳捕集、利用與封存(CCUS)相關的預處理技術轉變。

細分市場分析

到2025年,排煙脫硫(FGD)將佔據北美空氣污染控制系統市場32.1%的佔有率,並繼續保持其在受監管的重工業設施中領先的技術地位。這一地位反映了發電、煉油和酸性氣體處理產業對硫控制的持續需求,在這些產業中,濕式、乾式和半乾式系統分別適用於不同的運作條件。濕式FGD仍然是高硫負載、脫硫效率要求嚴格的大型發電廠和煉油廠的首選方法。半乾式系統在工業鍋爐和類似設施中越來越受歡迎,因為這些設施的水處理相對容易,而污水處理則較為困難。因此,儘管北美空氣污染控制系統市場的技術格局不斷變化,但FGD仍保持著良好的市場表現和強勁的更新換代需求。

布基和陶瓷過濾器是成長最快的類型,預計到2031年,北美空氣污染控制系統市場在該領域的規模將以5.3%的複合年成長率成長。需求量最大的是水泥窯、垃圾焚化發電發電廠和鋼鐵廠,這些企業需要捕捉細顆粒物,而老式靜電集塵機在日益嚴格的顆粒物排放法規下無法持續有效地完成這項工作。脈衝噴氣布基過濾器仍然是一種極具吸引力的選擇,因為即使在許多高溫環境下,它們也能實現極高的除塵效率,同時將壓降控制在可接受的範圍內。選擇性催化還原(SCR)和選擇性非催化還原(SNCR)系統在滿足氮氧化物(NOx)排放法規的設施中也繼續發揮著重要作用,尤其是在鄰近空氣盆地臭氧法規日益嚴格的地區。靜電集塵機仍能提供穩定的維護收入,但隨著維修決策轉向過濾器、洗滌器和整合式多污染物處理平台,其在北美空氣污染控制系統產業的成長速度正在放緩。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 調查範圍

- 市場的定義

- 研究的先決條件

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 近期趨勢與發展

- 市場促進因素

- 加強對PM2.5和臭氧的監管

- 加強石油和天然氣產業的甲烷和硫控制

- 水泥和鋼鐵業掀起了一波符合碳捕集、利用與封存(CCUS)標準的維修浪潮。

- 人工智慧驅動的最佳化和預測性維護

- PM2.5 安全檢查等級 (SIL) 的降低將減少獲得授權的範圍。

- 市場限制因素

- 燃煤發電廠的退役減少了對現有設施維修的需求。

- 維修所需的設備投資成本高昂,而且停工過程也十分複雜。

- 熟練勞動力和催化劑前置作業時間造成的瓶頸

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 靜電集塵器(乾式和濕式)

- 廢氣脫硫(濕法、乾法和半乾法)

- 洗滌器(濕式、乾式、船舶用)

- 選擇性催化還原與非催化還原

- 布質和陶瓷過濾器

- 汞和揮發性有機化合物控制設備

- 按目標污染物

- 顆粒物(PM)

- SOx

- NOx

- 揮發性有機化合物(VOCs)

- 汞和空氣傳播危害

- 按最終用戶行業分類

- 發電

- 水泥

- 鋼

- 化工/石油化工

- 紙漿和造紙

- 垃圾焚化發電

- 其他行業(玻璃、採礦等)

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Babcock & Wilcox Enterprises, Inc.

- CECO Environmental Corp.

- Ducon Technologies Inc.

- GE Vernova Inc.

- ANDRITZ AG

- Fuel Tech, Inc.

- Tri-Mer Corporation

- SLY LLC

- Donaldson Company, Inc.

- Nederman Holding AB

- Anguil Environmental Systems, Inc.

- Camfil AB

- ProcessBarron

- Valmet Oyj

- FLSmidth & Co. A/S

- Mitsubishi Power, Ltd.

- Thermax Limited

- Monroe Environmental Corporation

- Beltran Technologies, Inc.

- Hamon

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america industrial air quality control systems market size is expected to grow from USD 33.43 billion in 2025 to USD 35.02 billion in 2026 and is forecast to reach USD 44.18 billion by 2031 at 4.76% CAGR over 2026-2031.

This report is Segmented by Type (Electrostatic Precipitators, Flue-Gas Desulfurization, Scrubbers, and More), Pollutant Controlled (PM, Sox, Nox, VOC, and More), End-User Industry (Power Generation, Cement, Iron and Steel, Chemicals and Petrochemicals, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Industrial Air Quality Control Systems Market Trends and Insights

Stricter PM2.5 and Ozone Compliance Reshapes Permitting Economics

The U.S. Environmental Protection Agency lowered the primary annual PM2.5 standard to 9.0 µg/m3 in February 2024, which immediately tightened the compliance context for large industrial sources. This change reduced the operating cushion that many facilities had relied on when planning plant expansions or permit renewals. Projects that could once move forward with limited control upgrades now face a stronger need to prove lower emissions performance under stricter air quality review. The pressure increased further when Dallas-Fort Worth, Houston-Galveston-Brazoria, and San Antonio were reclassified from Moderate to Serious ozone nonattainment, effective in July 2024. That change lowered major source thresholds to 50 tons per year and pushed RACT obligations toward 2026 implementation windows. In the North America air quality control systems market, these combined rules are moving filter, scrubber, and NOx-control spending into current capital planning cycles.

Oil and Gas Methane and Sulfur Control Upgrades Expand Multi-Pollutant Demand

The EPA finalized a major package of methane and VOC controls for the oil and natural gas sector in March 2024, making this one of the most important compliance shifts affecting heavy industrial emissions equipment. The rule covers 28% of U.S. anthropogenic methane emissions and 23% of anthropogenic VOC emissions from the sector. It requires zero-emissions pneumatic controllers, quarterly optical gas imaging at multi-well sites, and 99.9% SO2 reduction from certain sweetening units. This is changing purchase behavior because gas processing and refining sites are increasingly evaluating sulfur scrubbing, vapor recovery, NOx reduction, and continuous monitoring as part of one investment cycle rather than as separate projects. Canada is also tightening industrial emissions policy for large emitters, which supports a broader regional procurement base for air quality control equipment. As a result, the North America air quality control systems market is seeing stronger multi-pollutant demand across the Gulf Coast, the Permian Basin, Alberta, and British Columbia.

Coal Retirements Reduce Legacy Retrofit Demand, but the Pace Is Uneven

Coal retirements are reducing one of the oldest recurring revenue pools for scrubbers, SCR systems, and particulate control retrofits. Coal-fired plants historically required frequent compliance upgrades, which made them a dependable source of aftermarket and replacement demand. As older units leave the grid, the installed base becomes smaller across the Midwest, Appalachia, the Southeast, and parts of Canada. The decline is still uneven because reliability concerns and fuel-price shifts have kept some aging units online longer than earlier assumptions suggested. That uneven retirement pattern preserves catalyst replacement, baghouse maintenance, and scrubber service work as part of the fleet even as total coal exposure falls. For the North America air quality control systems market, the effect is a gradual mix shift toward gas, waste-to-energy, and CCUS-related pretreatment rather than a sudden collapse in power-sector demand.

Other drivers and restraints analyzed in the detailed report include:

- CCUS-Ready Cement and Steel Retrofit Wave Creates Pre-Treatment Hardware Demand

- AI-Enabled Optimization and Predictive Maintenance Shifts the Value Proposition

- High Retrofit Capex and Outage Complexity Constrain Project Conversion Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flue-gas desulfurization held 32.1% of the North America air quality control systems market share in 2025, which kept it as the leading technology group across regulated heavy industrial sites. Its position reflects the continued need for sulfur control in power generation, refining, and sour-gas processing, where wet, dry, and semi-dry systems each serve different operating conditions. Wet FGD remains the preferred route in large-capacity power and refinery settings where sulfur loads are high and removal efficiency requirements are strict. Semi-dry systems are gaining ground in industrial boilers and similar sites where water handling and wastewater disposal are harder to manage. This leaves FGD with a broad installed base and strong replacement demand even as the technology mix evolves within the North America air quality control systems market.

Fabric and ceramic filters are the fastest-growing type, and the North America air quality control systems market size for this segment is expected to rise at a 5.3% CAGR through 2031. Demand is strongest in cement kilns, waste-to-energy plants, and steel facilities that need finer particulate capture than older electrostatic precipitators can consistently deliver under tighter PM limits. Pulse-jet fabric filters remain attractive because they can achieve very high collection efficiency while keeping pressure drop manageable in many high-temperature settings. SCR and SNCR systems also remain important for facilities managing NOx obligations, especially where ozone compliance is tightening in nearby air basins. Electrostatic precipitators still provide stable maintenance revenue, but growth is slower because more retrofit decisions are shifting toward filters, scrubbers, and integrated multi-pollutant platforms in the North America air quality control systems industry.

Complete Report Scope:

- By Type

- Electrostatic Precipitators (Dry & Wet)

- Flue-Gas Desulfurization (Wet, Dry, Semi-dry)

- Scrubbers (Wet, Dry, Marine)

- Selective Catalytic and Non-Catalytic Reduction

- Fabric/Ceramic Filters

- Mercury and VOC Control Units

- By Pollutant Controlled

- Particulate Matter (PM)

- SOx

- NOx

- Volatile Organic Compounds (VOC)

- Mercury and Air Toxics

- By End-user Industry

- Power Generation

- Cement

- Iron and Steel

- Chemicals and Petrochemicals

- Pulp and Paper

- Waste-to-Energy

- Others (Glass, Mining, etc.)

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Babcock & Wilcox Enterprises, Inc.

- CECO Environmental Corp.

- Ducon Technologies Inc.

- GE Vernova Inc.

- ANDRITZ AG

- Fuel Tech, Inc.

- Tri-Mer Corporation

- SLY LLC

- Donaldson Company, Inc.

- Nederman Holding AB

- Anguil Environmental Systems, Inc.

- Camfil AB

- ProcessBarron

- Valmet Oyj

- FLSmidth & Co. A/S

- Mitsubishi Power, Ltd.

- Thermax Limited

- Monroe Environmental Corporation

- Beltran Technologies, Inc.

- Hamon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends and Developments

- 4.3 Market Drivers

- 4.3.1 Stricter PM2.5 and ozone compliance

- 4.3.2 Oil and gas methane and sulfur control upgrades

- 4.3.3 CCUS-ready cement and steel retrofit wave

- 4.3.4 AI-enabled optimization and predictive maintenance

- 4.3.5 Tighter permit headroom from lower PM2.5 SILs

- 4.4 Market Restraints

- 4.4.1 Coal retirements reduce legacy retrofit demand

- 4.4.2 High retrofit capex and outage complexity

- 4.4.3 Skilled labor and catalyst lead-time bottlenecks

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Electrostatic Precipitators (Dry & Wet)

- 5.1.2 Flue-Gas Desulfurization (Wet, Dry, Semi-dry)

- 5.1.3 Scrubbers (Wet, Dry, Marine)

- 5.1.4 Selective Catalytic and Non-Catalytic Reduction

- 5.1.5 Fabric/Ceramic Filters

- 5.1.6 Mercury and VOC Control Units

- 5.2 By Pollutant Controlled

- 5.2.1 Particulate Matter (PM)

- 5.2.2 SOx

- 5.2.3 NOx

- 5.2.4 Volatile Organic Compounds (VOC)

- 5.2.5 Mercury and Air Toxics

- 5.3 By End-user Industry

- 5.3.1 Power Generation

- 5.3.2 Cement

- 5.3.3 Iron and Steel

- 5.3.4 Chemicals and Petrochemicals

- 5.3.5 Pulp and Paper

- 5.3.6 Waste-to-Energy

- 5.3.7 Others (Glass, Mining, etc.)

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Babcock & Wilcox Enterprises, Inc.

- 6.4.2 CECO Environmental Corp.

- 6.4.3 Ducon Technologies Inc.

- 6.4.4 GE Vernova Inc.

- 6.4.5 ANDRITZ AG

- 6.4.6 Fuel Tech, Inc.

- 6.4.7 Tri-Mer Corporation

- 6.4.8 SLY LLC

- 6.4.9 Donaldson Company, Inc.

- 6.4.10 Nederman Holding AB

- 6.4.11 Anguil Environmental Systems, Inc.

- 6.4.12 Camfil AB

- 6.4.13 ProcessBarron

- 6.4.14 Valmet Oyj

- 6.4.15 FLSmidth & Co. A/S

- 6.4.16 Mitsubishi Power, Ltd.

- 6.4.17 Thermax Limited

- 6.4.18 Monroe Environmental Corporation

- 6.4.19 Beltran Technologies, Inc.

- 6.4.20 Hamon

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment

空氣品質管理系統市場:依產品類型、技術、應用、最終用戶和通路分類-2026-2032年全球市場預測

空氣品質管理系統市場:依產品類型、技術、應用、最終用戶和通路分類-2026-2032年全球市場預測 空氣清淨機市場預測至2034年-按產品、技術、應用、最終用戶和地區分類的全球分析2034年自動化室內空氣品質監測艙市場預測-按產品類型、部署模式、感測器類型、連接技術、安裝模式、最終用戶和地區分類的全球分析

空氣清淨機市場預測至2034年-按產品、技術、應用、最終用戶和地區分類的全球分析2034年自動化室內空氣品質監測艙市場預測-按產品類型、部署模式、感測器類型、連接技術、安裝模式、最終用戶和地區分類的全球分析 2026年全球空氣品質管理系統市場報告全球環境顆粒物空氣監測器市場(按技術、產品、顆粒尺寸、應用和最終用戶分類)預測(2026-2032)

2026年全球空氣品質管理系統市場報告全球環境顆粒物空氣監測器市場(按技術、產品、顆粒尺寸、應用和最終用戶分類)預測(2026-2032) 2035年船舶靜電集塵器市場分析及預測:按類型、產品、服務、技術、組件、應用、材料類型、最終用戶和功能分類2026年全球燃燒排放分析儀市場報告

2035年船舶靜電集塵器市場分析及預測:按類型、產品、服務、技術、組件、應用、材料類型、最終用戶和功能分類2026年全球燃燒排放分析儀市場報告 室內空氣品質 (IAQ) 監測系統市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2026–2034)2026年全球二氧化碳(CO2)通風控制器市場報告全球空氣排放管理軟體市場(依最終用戶產業、部署模式、組件、公司規模和定價模式分類)預測(2026-2032年)

室內空氣品質 (IAQ) 監測系統市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2026–2034)2026年全球二氧化碳(CO2)通風控制器市場報告全球空氣排放管理軟體市場(依最終用戶產業、部署模式、組件、公司規模和定價模式分類)預測(2026-2032年)