|

市場調查報告書

商品編碼

2073563

東南亞火力發電:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Southeast Asia Thermal Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

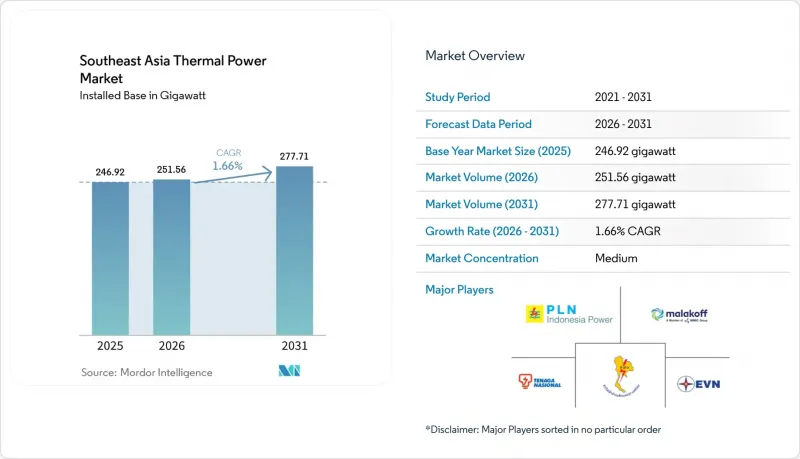

根據 Mordor Intelligence 預測,東南亞火力發電市場規模(以裝置容量計算)預計到 2025 年將達到 246.92 吉瓦,到 2026 年將達到 251.56 吉瓦,到 2031 年將達到 277.71 吉瓦,2026 年為 203%。

本報告按燃料類型(燃煤、燃氣、燃油)、技術(蒸氣循環、燃氣渦輪機/聯合循環、熱電聯產)、燃燒方式(粉煤燃燒、流化床燃燒、氣化、內燃機、燃氣渦輪機)、應用領域(公用事業規模、自用、分佈式、高峰需求)和地區(越南、印尼、菲律賓、泰國、馬來西亞、新加坡和菲律賓國家)進行細分。市場預測以容量(吉瓦)為單位。

東南亞火力發電市場趨勢與洞察

工業化導致基本負載需求激增

製造業的轉移導致東南亞電網電力需求集中激增,而該電網的設計並未考慮應對工業負載的快速成長。印尼正處於這一轉變的核心,該國的鎳加工走廊和其他資源型產業叢集需要全天候供電,而火力發電因其可靠性和成本可見性仍然是首選。在此背景下,私營燃煤電廠仍然是首選,因為它們能夠以冶煉廠和其他連續生產設施所需的規模提供穩定的電力輸出。印尼私營燃煤電廠的裝置容量在2024年達到16.6吉瓦,另有14吉瓦正在規劃或興建中。這表明,工業需求正在超越併入輸電網的燃煤發電禁令框架之外不斷擴張。這種「影子建設」意味著東南亞火電市場的實際規模遠大於僅從國有電力公司統計數據所能推斷出的規模。

液化天然氣發電價值鏈擴張

越南液化天然氣(LNG)發電計畫於2026年從政策目標階段進入計畫實施階段。越南石油電力公司(PetroVietnam Power)的農特拉3號和4號電廠採用通用電氣Vernova 9HA.02燃氣渦輪機,並與越南光伏天然氣公司(PV Gas)簽訂了為期25年的LNG供應契約,成為越南首批LNG發電廠,並於2026年1月5日投入商業運營。隨後,越南電力集團(EVN)推進了廣特拉二號電廠的EPC總承包合約。此外,卡納LNG計畫(Ca Na LNG project)——根據第八期能源發展競標(PDP VIII)透過國際競標選定的首個LNG計畫——於2026年4月完成融資。主要挑戰不僅在於燃料和設備的供應,還在於能否在購電協議(PPA)框架內合理分配風險,從而為企劃案融資提供支援。 2026年5月,越南能源監管機構指出,目前的購電協議仍未能充分分擔國家和投資者之間的風險。

更嚴格的ESG貸款標準和多元化的提款方式

儘管根據東協永續金融分類標準,天然氣仍被視為過渡能源,但與2010年代初期相比,融資條件已變得更加嚴格。根據2025年撤資記分卡,截至2024年,該地區煤炭和天然氣的累積貸款額仍然龐大,國際銀行和日本國際協力銀行(JBIC)在支持計畫方面持續發揮重要作用。目前的限制因素是多邊和混合融資的結構,因為如果各國政府不願承認無法收回的資本損失,早期退役模式仍然難以實施。井裡汶1號電廠早期退役計畫的取消表明,即使是備受矚目的過渡機制,如果缺乏政治協議和補償條件,也可能失敗。因此,東南亞火力發電市場目前處於融資的“中間地帶”,天然氣融資在許多情況下仍然容易獲得,而燃煤資金籌措的退役仍然緩慢且困難重重。

細分市場分析

截至2025年,燃煤發電廠佔東南亞火力發電總裝置容量的58.1%,煤炭仍是東南亞火力發電市場最大的燃料來源。印尼57吉瓦的發電裝置容量以及越南現有發電結構中對煤炭的持續依賴,共同支撐了這一主導地位。印尼以外地區新建燃煤發電廠的開發速度已大幅放緩,近期提出的許多提案旨在滿足工業自用需求,而非用於電網擴建。天然氣發電是成長最快的燃料類型,越南、馬來西亞和菲律賓的液化天然氣發電管道計畫均取得了進展,預計到2031年將以4.9%的複合年成長率成長。

從越南運作中的發電結構來看,轉型之路仍然漫長。根據越南電力集團(EVN)報告顯示,2026年第一季,燃煤發電將佔越南電力總產量的52.8%,而燃氣渦輪機發電僅佔7%。然而,隨著液化天然氣(LNG)電廠從合約階段過渡到運作,預計未來幾年這一差距將有所縮小。燃油電廠目前仍佔發電結構的一部分,在菲律賓和印尼偏遠島嶼地區等輸電網路和燃料選擇有限的地區,燃油電廠在緊急情況下仍發揮著至關重要的作用,滿足高峰用電需求。因此,儘管東南亞火力發電市場在可預見的未來仍將依賴煤炭,但新建設的趨勢正朝著天然氣、提高能源效率和增強燃料柔軟性的方向發展。

預計到2025年,燃氣渦輪機和聯合循環技術將佔火力發電裝置容量的48.3%,並在2031年之前以2.1%的複合年成長率成長。這反映了新加坡、泰國和馬來西亞數十年來在該領域的投資,這些國家很早就建造了燃氣發電廠,而如今能源效率標準的提高正推動著老舊設施的現代化改造,使其成為先進的聯合循環電廠。下一階段的成長可能並非由單一的大型企劃驅動,而是由老舊開式循環燃氣發電廠的大規模中型現代化改造所驅動。蒸氣循環發電廠仍然擁有相當大的規模,在印尼和越南的燃煤發電中佔有相當大的比例,預計其中許多電廠將在預測期內繼續運作。

電力公司正努力透過升級改造至超臨界壓力和生質能混燒計畫來維持蒸氣循環發電設施的效用。印尼國家電力公司(PLN Energi Primer Indonesia)在2025年供應了240萬噸生質能,並在2026年第一季供應了460,368噸用於混燒。這顯示維修活動正從測試階段過渡到全面實施階段。儘管柔佛州和雪蘭莪州的工業叢集適合建設能夠同時提供電力和工藝熱的設施,但東南亞火力發電產業的熱電聯產(CHP)利用率仍然不足。越南三菱電力公司訂單的「O Mon 4」專案採用了江淮系列燃氣渦輪機,其聯合循環效率超過64%,顯示東南亞火力發電產業重視高效平台。隨著這些平台的日益普及,老舊蒸氣循環設備的競爭力將逐漸下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 工業化導致基本負載需求激增

- 將價值鏈從液化天然氣擴展到發電領域

- 政策重點關注電網穩定性和能源安全。

- 日本和韓國為高能量低排放煤計畫提供資金

- 資料中心現場發電的興起

- 煤炭和生質能混燒產生的排碳權所帶來的商機

- 市場限制因素

- 更嚴格的ESG貸款和多邊撤資

- 太陽能發電和電池儲能混合系統的平準化度電成本快速下降

- 印度和馬來西亞上游天然氣產量下降,加劇了供應風險。

- 東協電網交易正在抑制新建設。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按燃料類型

- 燃煤發電廠

- 天然氣發電廠

- 燃油發電廠

- 透過技術

- 蒸氣循環系統

- 燃氣渦輪機/聯合循環

- 熱電聯產(CHP)

- 燃燒法

- 粉煤燃燒

- 流體化床燃燒

- 氣化

- 內燃機

- 渦輪燃燒

- 透過使用

- 公用事業規模的火力發電廠

- 工業私營發電廠

- 分散式火力發電廠

- 尖峰容量發電廠

- 按地區

- 越南

- 印尼

- 菲律賓

- 泰國

- 馬來西亞

- 新加坡

- 東南亞其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- PT PLN(Persero)

- Vietnam Electricity(EVN)

- Electricity Generating Authority of Thailand(EGAT)

- Malakoff Corporation Berhad

- First Gen Corporation

- Aboitiz Power Corp

- Tenaga Nasional Berhad

- PETRONAS Gas Berhad

- PT Adaro Energy Indonesia Tbk

- PT Bayan Resources Tbk

- Vinacomin(TKV)

- JERA Co. Inc.

- KEPCO Engineering & Construction

- Siemens Energy AG

- General Electric Co.

- Mitsubishi Power

- Shanghai Electric Group

- Doosan Enerbility

- Babcock & Wilcox

第7章 市場機會與未來展望

According to Mordor Intelligence, the southeast asia thermal power market size in terms of installed base is projected to be 246.92 gigawatt in 2025, 251.56 gigawatt in 2026, and reach 277.71 gigawatt by 2031, growing at a CAGR of 1.66% from 2026 to 2031.

This report is Segmented by Fuel Type (Coal-Fired, Gas-Fired, Oil-Fired), Technology (Steam Cycle, Gas Turbine/CC, CHP), Combustion Method (PF, FBC, Gasification, ICE, Turbine-Based), Application (Utility-Scale, Captive, Distributed, Peaker), and Geography (Vietnam, Indonesia, Philippines, Thailand, Malaysia, Singapore, Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Volume (GW).

Southeast Asia Thermal Power Market Trends and Insights

Surging Baseload Demand from Industrialisation

Manufacturing relocation is pushing concentrated electricity demand into Southeast Asian grids that were not built for such rapid industrial load growth. Indonesia is at the center of this shift, as its nickel-processing corridor and other resource-based industrial clusters require round-the-clock power and continue to favor thermal generation for reliability and cost visibility . In this setting, captive coal and gas plants remain the preferred option because they can deliver firm output at the scale needed by smelters and other continuous-process facilities. Captive coal capacity in Indonesia reached 16.6 GW in 2024, and another 14 GW was either planned or under construction, which shows how industrial demand is expanding outside the grid-connected coal moratorium framework. This shadow build-out means the Southeast Asia thermal power market is larger in practice than public utility statistics alone would suggest.

Expansion of LNG-to-Power Value Chains

Vietnam's LNG-to-power program moved from policy ambition to project execution in 2026. PetroVietnam Power's Nhon Trach 3 and 4 plants entered commercial operation on January 5, 2026, as the country's first LNG-fired facility, using GE Vernova 9HA.02 turbines and a 25-year LNG supply contract with PV Gas. EVN then moved ahead with the Quang Trach II EPC contract, and the Ca Na LNG project reached financial close in April 2026 as the first LNG project selected through international competitive bidding under PDP VIII. The main challenge is not only fuel supply or equipment access, but also whether power purchase agreements can allocate risk in a way that supports project finance. Vietnam's Energy Regulatory Authority stated in May 2026 that current PPAs still do not provide adequate risk-sharing between the state and investors.

Stricter ESG Lending and Multilateral Exit

Financing conditions are tighter than they were earlier in the decade, even though natural gas still qualifies as a transition fuel under the ASEAN Taxonomy for Sustainable Finance. The 2025 divestment scorecard still showed large cumulative coal and gas financing in the region through 2024, with international banks and JBIC continuing to play major roles in project support. The harder constraint now comes from multilateral and blended-finance structures, because early retirement models still struggle when governments resist recognizing unrecovered capital losses. The cancellation of the Cirebon-1 early-retirement effort showed that even high-profile transition structures can fail when political alignment and compensation terms do not hold. This leaves the Southeast Asia thermal power market in a financing middle ground where gas remains bankable in many cases, but coal retirement is still slow and difficult.

Other drivers and restraints analyzed in the detailed report include:

- Policy Focus on Grid Stability & Energy Security

- Rise of Captive On-Site Power for Data Centres

- Rapid LCOE Decline of Solar-Battery Hybrids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coal-fired power plants held 58.1% share of installed thermal capacity in 2025, which kept coal as the largest fuel base in the Southeast Asia thermal power market. That dominance remained anchored by Indonesia's 57 GW fleet and by Vietnam's continued reliance on coal within its existing generation mix. New coal development outside Indonesia has already slowed sharply, and the most visible recent proposals have been tied to captive industrial use rather than utility-grid expansion. Natural gas-fired power plants are the fastest-growing fuel segment, with 4.9% CAGR projected through 2031 as LNG-to-power pipelines move forward in Vietnam, Malaysia, and the Philippines.

Vietnam's operating mix still showed how far the transition has to go, because EVN reported that coal thermal contributed 52.8% of electricity output in the first quarter of 2026, while gas turbines contributed 7%. Even so, that gap is likely to narrow as LNG plants move from contract award to operation over the next several years. Oil-fired plants remain a residual part of the mix and continue to serve emergency peaking roles in the Philippines and in remote Indonesian island systems where grid and fuel options remain limited. The Southeast Asia thermal power market is therefore still coal-heavy in the near term, but its new-build path is moving toward gas, efficiency, and greater fuel flexibility.

Gas turbine and combined cycle technology claimed 48.3% of installed thermal capacity in 2025, and it is projected to grow at 2.1% CAGR through 2031. This position reflects decades of investment in Singapore, Thailand, and Malaysia, where gas-based fleets were built earlier and where efficiency standards are now steering replacement decisions toward modern combined-cycle assets. The next phase of growth is coming less from single mega projects and more from a broad wave of medium-scale replacements for aging open-cycle gas units. Steam cycle plants still hold a large base because they represent most of the coal fleet in Indonesia and Vietnam, and many of those assets will remain operational through the forecast period.

Utilities are trying to extend the relevance of steam-cycle assets through ultra-supercritical upgrades and biomass co-firing programs. PLN Energi Primer Indonesia supplied 460,368 tonnes of biomass for co-firing in the first quarter of 2026 after supplying 2.4 million tonnes during 2025, which shows that retrofit activity is moving from the pilot stage to broader execution. Combined heat and power remains underused in the Southeast Asia thermal power industry, even though industrial clusters in Johor and Selangor are well suited to facilities that can supply both electricity and process heat. Mitsubishi Power's O Mon 4 award in Vietnam, using JAC-series gas turbines with combined-cycle efficiency above 64%, shows that the Southeast Asia thermal power industry is rewarding high-efficiency platforms that can make older steam-cycle assets look less competitive over time.

Complete Report Scope:

- By Fuel Type

- Coal-Fired Power Plants

- Natural Gas-Fired Power Plants

- Oil-Fired Power Plants

- By Technology

- Steam Cycle-Based

- Gas Turbine/Combined Cycle

- Combined Heat and Power (CHP)

- By Combustion Method

- Pulverized Fuel (PF) Combustion

- Fluidized Bed Combustion

- Gasification

- Internal Combustion Engines

- Turbine-Based Combustion

- By Application

- Utility-Scale Thermal Plants

- Industrial Captive Power Plants

- Distributed Thermal Plants

- Peaker Plants

- By Geography

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

- Singapore

- Rest of Southeast Asia

List of Companies Covered in this Report:

- PT PLN (Persero)

- Vietnam Electricity (EVN)

- Electricity Generating Authority of Thailand (EGAT)

- Malakoff Corporation Berhad

- First Gen Corporation

- Aboitiz Power Corp

- Tenaga Nasional Berhad

- PETRONAS Gas Berhad

- PT Adaro Energy Indonesia Tbk

- PT Bayan Resources Tbk

- Vinacomin (TKV)

- JERA Co. Inc.

- KEPCO Engineering & Construction

- Siemens Energy AG

- General Electric Co.

- Mitsubishi Power

- Shanghai Electric Group

- Doosan Enerbility

- Babcock & Wilcox

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging baseload demand from industrialisation

- 4.2.2 Expansion of LNG to Power value chains

- 4.2.3 Policy focus on grid stability & energy security

- 4.2.4 Financing of HELE coal by Japan & Korea

- 4.2.5 Rise of captive on-site power for data centres

- 4.2.6 Carbon-credit upside from coal/biomass co-firing

- 4.3 Market Restraints

- 4.3.1 Stricter ESG lending & multilateral exit

- 4.3.2 Rapid LCOE decline of solar-battery hybrids

- 4.3.3 Upstream gas decline in ID & MY raising supply risk

- 4.3.4 ASEAN power-grid trade curbing new builds

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Coal-Fired Power Plants

- 5.1.2 Natural Gas-Fired Power Plants

- 5.1.3 Oil-Fired Power Plants

- 5.2 By Technology

- 5.2.1 Steam Cycle-Based

- 5.2.2 Gas Turbine/Combined Cycle

- 5.2.3 Combined Heat and Power (CHP)

- 5.3 By Combustion Method

- 5.3.1 Pulverized Fuel (PF) Combustion

- 5.3.2 Fluidized Bed Combustion

- 5.3.3 Gasification

- 5.3.4 Internal Combustion Engines

- 5.3.5 Turbine-Based Combustion

- 5.4 By Application

- 5.4.1 Utility-Scale Thermal Plants

- 5.4.2 Industrial Captive Power Plants

- 5.4.3 Distributed Thermal Plants

- 5.4.4 Peaker Plants

- 5.5 By Geography

- 5.5.1 Vietnam

- 5.5.2 Indonesia

- 5.5.3 Philippines

- 5.5.4 Thailand

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of Southeast Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PT PLN (Persero)

- 6.4.2 Vietnam Electricity (EVN)

- 6.4.3 Electricity Generating Authority of Thailand (EGAT)

- 6.4.4 Malakoff Corporation Berhad

- 6.4.5 First Gen Corporation

- 6.4.6 Aboitiz Power Corp

- 6.4.7 Tenaga Nasional Berhad

- 6.4.8 PETRONAS Gas Berhad

- 6.4.9 PT Adaro Energy Indonesia Tbk

- 6.4.10 PT Bayan Resources Tbk

- 6.4.11 Vinacomin (TKV)

- 6.4.12 JERA Co. Inc.

- 6.4.13 KEPCO Engineering & Construction

- 6.4.14 Siemens Energy AG

- 6.4.15 General Electric Co.

- 6.4.16 Mitsubishi Power

- 6.4.17 Shanghai Electric Group

- 6.4.18 Doosan Enerbility

- 6.4.19 Babcock & Wilcox

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment