|

市場調查報告書

商品編碼

2073562

東南亞水力發電:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Southeast Asia Hydropower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

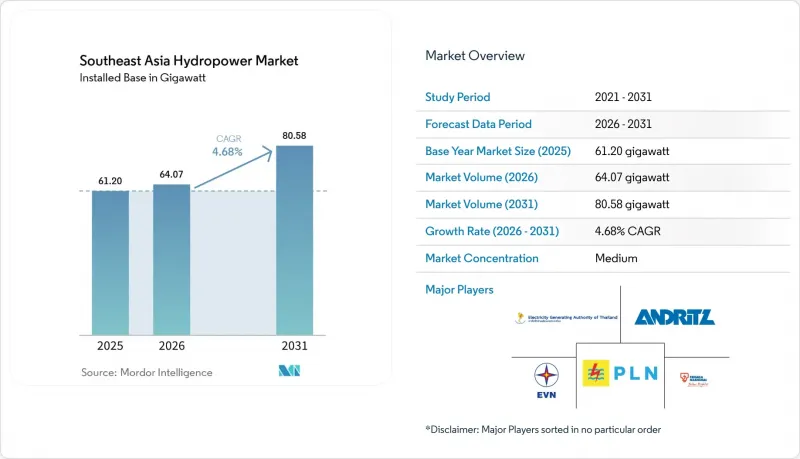

根據 Mordor Intelligence 預測,東南亞水力發電市場將從 2025 年的 61.20 吉瓦成長到 2026 年的 64.07 吉瓦,然後從 2026 年到 2031 年以 4.68% 的複合年成長率成長,到 2031 年達到 2031 年吉瓦。

本報告按裝置容量(大型水力發電、中型水力發電、小規模和微型水力發電)、技術(水庫式、徑流式、抽水蓄能式、河道式和微型管道式)、最終用戶(公共產業、獨立發電企業、工業和私人用途)以及地區(越南、寮國、東帝汶等)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

東南亞水電市場趨勢與洞察

隨著波動性極大的太陽能和風能發電的引入,對電網穩定的需求正在迅速增加。

泰國一套於2023年投入運作的電池儲能系統可提供兩小時的電力供應,但日落後空調需求激增,晚間用電高峰依然存在。位於林塔克隆(Lam Ta Klong)的一座500兆瓦抽水蓄能電站的可行性研究計劃提供8至12小時的放電時間,以補償日落至午夜期間的用電需求波動。在菲律賓,一個5.7吉瓦的抽水蓄能電站計畫正在建設中,其位於呂宋島和棉蘭老島的中心位置符合能源部關於可調儲能系統的規定,因此需要優先併網。越南第八個電力發展規劃也體現了類似的轉變,該規劃限制了新建大型水力發電項目,同時鼓勵投資建設日循環抽水蓄能電站,以平衡16.5吉瓦的太陽能發電裝置容量。根據其“公正能源轉型夥伴關係”,印尼國家電力公司 (PLN) 計劃建造 3.7 吉瓦的抽水蓄能電站,同時逐步淘汰 9.2 吉瓦的燃煤電廠。

資金流入低息東協綠色債券

2023年,東協未償付永續債券總額達7,27億美元,其中37%的資金用於可再生能源計畫。東協綠色催化融資機制(ACGF)向15個符合氣候債券舉措( CBI)標準的水力發電發電工程提供了總計23億美元的資金,其中包括寮國和菲律賓的徑流式水力發電叢集。印尼主權綠色伊斯蘭債券(Soureign Green Sukuk)在2024年籌集了30億美元,用於資金籌措成本,該大壩計劃於2027年竣工。

由印尼和馬來西亞資料中心支持的私人購電協議

微軟、Google和亞馬遜網路服務(AWS)宣布,2024年將共投資120億美元用於資料中心建置。由於光纖基礎設施完善且土地易於獲取,投資主要集中在爪哇島和柔佛州。這些超大規模資料中心業者企業需要全天候的無碳電力供應,促使印尼國家電力公司(PLN)從阿薩漢鏈水力發電廠分配150兆瓦電力,並簽署了首個以水電為支撐的企業購電協議(PPA),該協議採用區塊鏈每小時檢驗的方式。隨後,砂拉越能源公司以高價合約的形式,從巴貢和穆魯姆兩個水力發電廠向超大規模資料中心業者分配了300兆瓦電力。阿博伊蒂茲電力公司(Aboitiz Power)和長江電力公司(CK Power)等獨立電力生產商(IPP)目前正瞄準資料中心託管公司和加密貨幣礦工,透過20-50兆瓦抽水蓄能電站和小規模水力發電廠的購電協議來爭取客戶。

細分市場分析

裝置容量低於10兆瓦的小規模和超小規模水力發電廠成長最快,年複合成長率達5.62%,開發商看重的是其簡化的授權程序和較低的社會接受風險。在菲律賓,到2024年將新建175兆瓦的小規模水力發電廠,另有500兆瓦的建設計劃,旨在取代與電網隔離島嶼上的柴油發電。越南擁有超過2500座小規模水力發電廠,但已暫停發放2024年的新許可證,直到獲得累積影響評估結果。

即使到了2025年,以巴貢水電站(2400兆瓦)和斯里那加林水電站(720兆瓦)等現有資產為核心的100兆瓦以上的大型水電站,仍將佔據東南亞水電市場63.90%的佔有率。新增發電容量目前集中在寮國,中國投資的沙耶武里水電站(1285兆瓦)計畫將於2024年全面運作。 10至100兆瓦的中型水力發電廠被定位為一種過渡策略。印尼國家電力公司(PLN)計劃在蘇門答臘島和加里曼丹島建造類似的680兆瓦項目,以平衡建設週期、機組規模和社會接受度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 隨著波動性極大的太陽能和風能發電的引入,對電網穩定化的需求正在迅速增加。

- 低利率推動資金流入東協綠色債券。

- 基於東協電網路線藍圖的區域間電力交易

- 基於印尼和馬來西亞資料中心的私有購電協議

- 利用水力發電和電池驅動的抽水蓄能發電來滿足過剩太陽能發電的需求。

- 利用人工智慧水文預測降低維運成本。

- 市場限制因素

- 降低公用事業規模電池儲能的價格

- 反對興建水壩的社會運動愈演愈烈

- 拉尼娜/厄爾尼諾現象導致水流長期波動

- 跨境ESG實質審查正在延緩中國EPC融資。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按產能

- 大型水力發電(100兆瓦或以上)

- 中型水力發電(10-100兆瓦)

- 小規模和超小規模水力發電(小於10兆瓦)

- 透過技術

- 儲存底部

- 河川水力發電

- 抽水蓄能水力發電

- 串流內和微型導管

- 依成分(僅限定性分析)

- 渦輪

- 發電機

- 控制與自動化

- 工廠輔助設備

- 最終用戶

- 公共產業(國有和公有)

- 獨立發電機

- 工業和專屬式

- 按地區

- 越南

- 印尼

- 菲律賓

- 泰國

- 馬來西亞

- 新加坡

- 其他東南亞國家(汶萊、柬埔寨、寮國、緬甸、東帝汶)

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Vietnam Electricity(EVN)

- Electricity Generating Authority of Thailand(EGAT)

- PT Perusahaan Listrik Negara(PLN)

- Tenaga Nasional Berhad(TNB)

- Aboitiz Power Corp.

- Power Construction Corp. of China(PowerChina)

- Sinohydro

- Andritz AG

- Voith Hydro

- General Electric Vernova

- Toshiba Energy Systems

- Hitachi Energy

- China Yangtze Power

- China Three Gorges South-East Asia

- Datang Hydropower

- CK Power PLC

- Sarawak Energy Berhad

- Banpu Power

- AC Energy Holdings

- EDC Hydro

第7章 市場機會與未來展望

According to Mordor Intelligence, the southeast asia hydropower market size is expected to grow from 61.20 gigawatt in 2025 to 64.07 gigawatt in 2026 and is forecast to reach 80.58 gigawatt by 2031 at 4.68% CAGR over 2026-2031.

This report is Segmented by Capacity (Large Hydro, Medium Hydro, and Small and Micro Hydro), Technology (Reservoir-Based, Run-Of-River, Pumped-Storage, and In-Stream and Micro-Conduit), End-User (Utilities, Independent Power Producers, and Industrial and Captive), and Geography (Vietnam, Laos, Timor-Leste, and More). The Market Size and Forecasts are Provided in Terms of Installed Capacity (GW).

Southeast Asia Hydropower Market Trends and Insights

Surging Grid-Stabilization Need Amid Variable Solar and Wind Integration

Battery energy-storage systems commissioned in Thailand in 2023 offer a two-hour duration, yet evening peaks persist when air-conditioning demand climbs after sunset. Feasibility studies for 500 MW pumped-storage at Lam Ta Khlong target 8- to 12-hour discharge windows, bridging the sunset-to-midnight ramp. In the Philippines, a 5.7 GW pumped-storage pipeline is anchored by Luzon and Mindanao sites that satisfy a Department of Energy rule mandating dispatchable storage for grid-connection priority. Similar pivots appear in Vietnam's Power Development Plan 8, which caps new large hydro while steering investment toward daily-cycling pumped storage that balances a 16.5 GW solar fleet. Indonesia's PLN plans 3.7 GW of pumped storage as it retires 9.2 GW of coal capacity under the Just Energy Transition Partnership.

Low-Interest ASEAN Green-Bond Inflows

Outstanding ASEAN sustainable bonds climbed to USD 72.7 billion in 2023, with 37% of proceeds earmarked for renewable energy. The ASEAN Catalytic Green Finance Facility committed USD 2.3 billion across 15 hydropower projects that meet Climate Bonds Initiative criteria, including run-of-river clusters in Laos and the Philippines. Indonesia's sovereign green sukuk raised USD 3 billion in 2024, channeling funds to pumped-storage pre-development in West Java and Sumatra. Malaysia's SRI sukuk lowered Sarawak Energy's financing cost for the 1,285 MW Baleh dam scheduled for 2027 completion.

Data-Center-Backed Private PPAs in Indonesia and Malaysia

Microsoft, Google, and Amazon Web Services announced USD 12 billion in data-center investment during 2024, clustering in Java and Johor due to fiber connectivity and land availability. These hyperscalers require 24/7 carbon-free energy, spurring PLN's first hydro-backed corporate PPA that allocates 150 MW from the Asahan cascade with hourly blockchain verification. Sarawak Energy followed by assigning 300 MW from Bakun and Murum to a hyperscaler under a premium-priced contract. IPPs such as Aboitiz Power and CK Power now target 20-50 MW pumped-storage and small-hydro PPAs with colocation firms and cryptocurrency miners.

Other drivers and restraints analyzed in the detailed report include:

- Regional Power Trade Under ASEAN Power Grid Roadmap

- Cheaper Utility-Scale Battery Prices

- Escalating Anti-Dam Social Activism

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Small and micro plants below 10 MW posted the fastest growth, expanding at a 5.62% CAGR as developers favored streamlined permitting and lower social-license risk. The Philippines added 175 MW of small hydro by 2024 with another 500 MW in the pipeline, targeting diesel displacement on off-grid islands. Vietnam hosts more than 2,500 small plants, but suspended new licenses in 2024 pending cumulative-impact studies.

Large hydro above 100 MW still held 63.90% of the Southeast Asia hydropower market share in 2025, anchored by legacy assets such as Bakun (2,400 MW) and Srinagarind (720 MW). New capacity now concentrates in Laos, where the Chinese-financed Xayaburi (1,285 MW) reached full operation in 2024. Medium hydro between 10-100 MW fulfills a middle-ground strategy; PLN scheduled 680 MW of such schemes in Sumatra and Kalimantan to balance build-time, unit size, and social acceptance.

Complete Report Scope:

- By Capacity

- Large Hydro (Above 100 MW)

- Medium Hydro (10 to 100 MW)

- Small and Micro Hydro (Below 10 MW)

- By Technology

- Reservoir-Based

- Run-of-River

- Pumped-Storage

- In-Stream and Micro-conduit

- By Component (Qualitative Analysis only)

- Turbines

- Generators

- Control and Automation

- Balance-of-Plant

- By End-User

- Utilities (State & Public)

- Independent Power Producers

- Industrial and Captive

- By Geography

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

- Singapore

- Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste)

List of Companies Covered in this Report:

- Vietnam Electricity (EVN)

- Electricity Generating Authority of Thailand (EGAT)

- PT Perusahaan Listrik Negara (PLN)

- Tenaga Nasional Berhad (TNB)

- Aboitiz Power Corp.

- Power Construction Corp. of China (PowerChina)

- Sinohydro

- Andritz AG

- Voith Hydro

- General Electric Vernova

- Toshiba Energy Systems

- Hitachi Energy

- China Yangtze Power

- China Three Gorges South-East Asia

- Datang Hydropower

- CK Power PLC

- Sarawak Energy Berhad

- Banpu Power

- AC Energy Holdings

- EDC Hydro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging grid-stabilization need amid variable solar & wind integration

- 4.2.2 Low-interest ASEAN green-bond inflows

- 4.2.3 Regional power-trade under ASEAN Power Grid roadmap

- 4.2.4 Data-centre backed private PPAs in Indonesia & Malaysia

- 4.2.5 Water-battery pumped-storage for solar over-generation

- 4.2.6 AI-assisted hydrology forecasting cuts O&M costs

- 4.3 Market Restraints

- 4.3.1 Cheaper utility-scale battery prices

- 4.3.2 Escalating anti-dam social activism

- 4.3.3 Prolonged La Nia/El Nio driven flow volatility

- 4.3.4 Cross-border ESG due-diligence delays Chinese EPC loans

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity

- 5.1.1 Large Hydro (Above 100 MW)

- 5.1.2 Medium Hydro (10 to 100 MW)

- 5.1.3 Small and Micro Hydro (Below 10 MW)

- 5.2 By Technology

- 5.2.1 Reservoir-Based

- 5.2.2 Run-of-River

- 5.2.3 Pumped-Storage

- 5.2.4 In-Stream and Micro-conduit

- 5.3 By Component (Qualitative Analysis only)

- 5.3.1 Turbines

- 5.3.2 Generators

- 5.3.3 Control and Automation

- 5.3.4 Balance-of-Plant

- 5.4 By End-User

- 5.4.1 Utilities (State & Public)

- 5.4.2 Independent Power Producers

- 5.4.3 Industrial and Captive

- 5.5 By Geography

- 5.5.1 Vietnam

- 5.5.2 Indonesia

- 5.5.3 Philippines

- 5.5.4 Thailand

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Vietnam Electricity (EVN)

- 6.4.2 Electricity Generating Authority of Thailand (EGAT)

- 6.4.3 PT Perusahaan Listrik Negara (PLN)

- 6.4.4 Tenaga Nasional Berhad (TNB)

- 6.4.5 Aboitiz Power Corp.

- 6.4.6 Power Construction Corp. of China (PowerChina)

- 6.4.7 Sinohydro

- 6.4.8 Andritz AG

- 6.4.9 Voith Hydro

- 6.4.10 General Electric Vernova

- 6.4.11 Toshiba Energy Systems

- 6.4.12 Hitachi Energy

- 6.4.13 China Yangtze Power

- 6.4.14 China Three Gorges South-East Asia

- 6.4.15 Datang Hydropower

- 6.4.16 CK Power PLC

- 6.4.17 Sarawak Energy Berhad

- 6.4.18 Banpu Power

- 6.4.19 AC Energy Holdings

- 6.4.20 EDC Hydro

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

水力發電市場-全球產業規模、佔有率、趨勢、機會、預測:產能、應用、區域及競爭格局(2021-2031年)

水力發電市場-全球產業規模、佔有率、趨勢、機會、預測:產能、應用、區域及競爭格局(2021-2031年) 水力發電市場規模、佔有率、趨勢和預測:按規模、應用和地區分類,2026-2034年

水力發電市場規模、佔有率、趨勢和預測:按規模、應用和地區分類,2026-2034年 水力發電市場:2026-2032年全球市場預測(按服務和產品、組件、類型、容量、安裝和所有權模式分類)水力發電市場:依技術類型、功率範圍、類型、模組和終端用戶產業分類-2026-2032年全球市場預測水力發電控制系統市場:按產品類型、渦輪機類型、電壓等級、應用和最終用戶分類-2026-2032年全球市場預測水力發電閘門市場:2026-2032年全球市場預測(以閘門類型、閘門操作方式、材質、安裝配置和最終用戶分類)微型水力發電市場:按類型、渦輪機類型、組件、輸出功率、最終用戶和安裝類型分類-2026-2030年全球市場預測

水力發電市場:2026-2032年全球市場預測(按服務和產品、組件、類型、容量、安裝和所有權模式分類)水力發電市場:依技術類型、功率範圍、類型、模組和終端用戶產業分類-2026-2032年全球市場預測水力發電控制系統市場:按產品類型、渦輪機類型、電壓等級、應用和最終用戶分類-2026-2032年全球市場預測水力發電閘門市場:2026-2032年全球市場預測(以閘門類型、閘門操作方式、材質、安裝配置和最終用戶分類)微型水力發電市場:按類型、渦輪機類型、組件、輸出功率、最終用戶和安裝類型分類-2026-2030年全球市場預測 水力發電市場:按類型、應用和地區分類

水力發電市場:按類型、應用和地區分類 水力發電市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、製程、最終用戶及安裝類型日本水電市場規模、佔有率、趨勢及預測(依電廠類型、組件、最終用途及地區分類),2026-2034年

水力發電市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、製程、最終用戶及安裝類型日本水電市場規模、佔有率、趨勢及預測(依電廠類型、組件、最終用途及地區分類),2026-2034年