|

市場調查報告書

商品編碼

2073558

印度無線音箱市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Wireless Speaker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

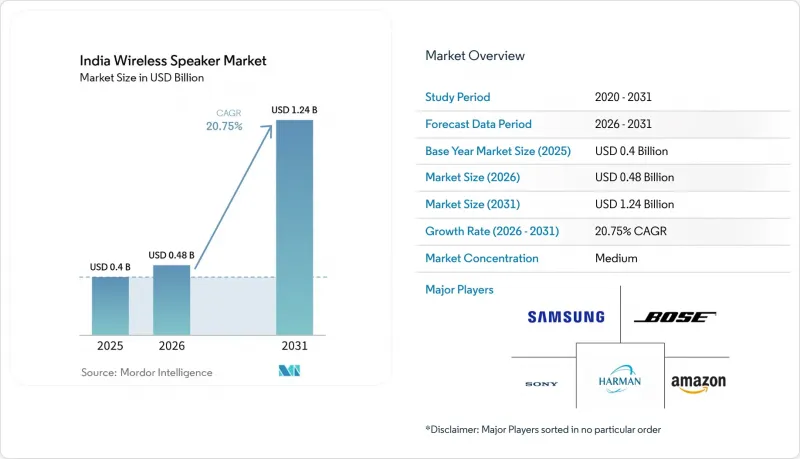

根據Mordor Intelligence預測,印度無線音箱市場規模預計在2026年達到4.8億美元,高於2025年的4億美元。預計到2031年,該市場規模將達到12.4億美元,2026年至2031年的複合年成長率為20.75%。

本報告按設備類型(僅藍牙、僅Wi-Fi、智慧音箱、混合型)、分銷管道(線下零售通路、線下專業音訊商店等)、價格區間(入門級、150美元以下等)、最終用戶(住宅、商用)和地區(印度北部、印度西部、印度南部、印度東部、印度中部、印度東北部)進行細分。市場預測以美元計價。

印度無線音箱市場趨勢與洞察

智慧型手機的普及和價格合理的資料通訊。

4G/5G網路覆蓋範圍的擴大以及行動電話分期付款計劃的推行,已將數百萬首次購機者帶入數位生態系統。目前,二、三線城市的智慧型手機普及率正以兩位數的速度成長,而一線大都會圈的成長率僅為個位數。這些地區的用戶每月平均使用35-40GB的數據流量,比都市區用戶高出15-20%。設備擁有量的激增直接推動了入門級藍牙音箱的硬體普及率,隨著可支配收入的增加,這將為用戶升級到高階音訊設備鋪平道路。

OTT串流服務的普及正在改變音訊消費模式。

串流音樂收入佔錄製音樂總收入的88%,印度用戶每周平均聽歌26.7小時,遠高於全球平均。付費訂閱用戶成長了58.5%,上個月有69.4%的用戶觀看了音樂直播。 YouTube 95.2%的滲透率印證了「行動優先」的消費習慣,這與可攜式音箱的普及相符。同時,隨著對更高音質的需求不斷成長,都市區消費者也開始轉向支援Wi-Fi功能的智慧音箱。

高階市場的價格敏感度限制了市場擴張。

雖然高階市場成長最快,但在可支配收入仍在恢復正常的小規模城鎮,500美元以上的價位區間成長已趨於穩定。研究表明,60%的Z世代消費者會選擇分期付款購買體驗型產品,這凸顯了為高階音箱提供更靈活的資金籌措方案的重要性。各大品牌也紛紛響應,推出中價位的奢華設計產品,例如boAt的“Stone Opus”,它以三分之一的價格復刻了Marshall Acton的設計。

細分市場分析

到2025年,僅支援藍牙的型號將佔52.40%的銷量,凸顯了印度無線音箱市場對簡單智慧型手機配對方式的偏好。在多語言語音助理的推動下,智慧音箱正以22.60%的複合年成長率快速成長,預計2031年將縮小與藍牙音箱的差距。在印度無線音箱市場中,智慧音箱的市場規模預計將從2025年的6,000萬美元成長到2031年的2億美元。配備顯示器的型號,例如亞馬遜Echo Spot,正在拓展其應用場景,從音訊播放擴展到食譜指導和安全資訊顯示。僅支援Wi-Fi的型號和混合型設備滿足了高階住宅對高品質音效和多房間配置的需求,而印度標準局(BIS)強制執行的射頻限制則確保所有外形規格均符合安全標準。

語音助理最初在大都會圈普及,但對印地語、泰米爾語和旁遮普語的支持刺激了二線城市首次使用語音助理用戶層的需求。 JBL 的 Auracast 功能 PartyBox 系列展示了老牌音訊品牌如何透過採用面向未來的無線協議來維持市場地位。固定式智慧音箱的更換週期比可攜式藍牙裝置更長,因此平均售價更高,每位用戶收入成長潛力也更大。印度無線音箱產業的領導者將此視為策略成長的驅動力。

到2025年,線上零售商將佔據印度無線音箱市場65.90%的佔有率,這得益於大幅折扣、快速配送承諾以及覆蓋90%郵政編碼區域的廣泛分銷網路。同時,有組織的音訊專賣店正以每年22.30%的速度成長,因為購買150美元以上產品的消費者通常希望在購買前試用。預計到2031年,印度無線音箱專賣店的市場規模將達到1.2億美元。在大都會圈,品牌自營展示室也兼具體驗中心的功能;而在二線城市,連鎖店則透過特許經營的方式開設小規模門市,將產品展示與即時服務結合。

電子商務在入門級產品和更換需求方面仍然扮演著重要角色,因為在線比價最為便利。然而,購買高級產品的顧客通常會諮詢轉碼器相容性、房間聲學效果以及額外的保固選項,而門市員工也接受過相關培訓,能夠解答這些疑問。一些成功的品牌正在推行「同步發布」策略,即產品在同一天於官網和實體商店同步發售,並將發票資料直接導入中央客戶關係管理系統(CRM),從而簡化售後服務。未來,線上購買、線下取貨的混合模式可望成為主流。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧型手機普及率的提高和價格合理的資料通訊服務的普及

- OTT音樂和影片串流服務的普及

- 可支配收入增加以及對智慧家居設備的興趣日益濃厚

- 國內音響電子設備製造商的PLI獎勵

- 部署與本地語言相容的語音助手

- 通訊業者銷售揚聲器和內容捆綁包

- 市場限制因素

- 高階消費者對價格高度敏感

- 射頻輻射及其對兒童健康的擔憂

- 在大都會圈以外,售後服務網不足。

- BIS射頻合規認證延誤

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 依設備類型

- 限藍牙

- 僅限 Wi-Fi

- 智慧音箱

- 組合式(藍牙+Wi-Fi)

- 透過分銷管道

- 線上(電商平台、Brand.com)

- 線下零售-有組織的零售

- 線下 - 音響專賣店

- 線下 -大賣場/超級市場

- 按價格範圍

- 入門級(低於 150 美元)

- 中階(150-500美元)

- 高級版(超過 500 美元)

- 最終用戶

- 住宅

- 商業

- 按地區(印度)

- 印度北部

- 西印度群島

- 南印度

- 東印度

- 印度中部

- 印度東北部

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Retail India Private Limited

- Imagine Marketing Limited(boAt)

- HARMAN International(India)Pvt. Ltd.(JBL)

- Sony India Private Limited

- Xiaomi Technology India Private Limited

- Samsung India Electronics Private Limited

- Google India Private Limited

- Bose Corporation India Private Limited

- GN Audio A/S(Jabra)

- Koninklijke Philips NV

- Portronics Digital Pvt. Ltd.

- Zebronics India Pvt. Ltd.

- Sennheiser Electronics India Pvt. Ltd.

- Marshall Group India

- Logitech Electronics India Private Limited

- Panasonic India Pvt. Ltd.

- OPPO Mobile India Pvt. Ltd.(realme and Dizo speakers)

- Anker Innovations Technology(India)Pvt. Ltd.(Soundcore)

- Fire-Boltt(Savex Technologies Pvt. Ltd.)

- Lenovo(India)Private Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, india wireless speaker market size in 2026 is estimated at USD 0.48 billion, growing from 2025 value of USD 0.4 billion with 2031 projections showing USD 1.24 billion, growing at 20.75% CAGR over 2026-2031.

This report is Segmented by Device Type (Bluetooth-Only, Wi-Fi-Only, Smart Speakers, Combo), Distribution Channel (Offline-Organised Retail, Offline-Specialist Audio Stores, and More), Price Range (Entry-Level Less Than USD 150, and More), End-User (Residential, Commercial), and Geography (North, West, South, East, Central, North-East India). The Market Forecasts are Provided in Terms of Value (USD).

India Wireless Speaker Market Trends and Insights

Rising Smartphone and Affordable Data Penetration

Expanded 4G/5G coverage and aggressive handset financing have drawn millions of first-time buyers into the digital ecosystem. Tier-2 and tier-3 cities now post double-digit smartphone growth versus single-digit gains in metros, and their users stream 35-40 GB of data each month, 15-20% higher than urban counterparts. The leap in handset ownership directly fuels hardware attach rates for entry-level Bluetooth speakers and opens a gateway for premium audio upgrades once disposable incomes rise.

OTT Streaming Services Proliferation Reshapes Audio Consumption Patterns

Streaming accounts for 88% of recorded-music revenue, with Indian users listening 26.7 hours weekly, well above global averages. Paid subscriptions rose 58.5%; 69.4% tuned into music livestreams in the previous month. YouTube's 95.2% penetration confirms a mobile-first habit that aligns with portable speaker ownership, while the demand for higher fidelity is steering urban buyers toward Wi-Fi-enabled smart speakers.

Premium Segment Price Sensitivity Constrains Market Expansion

Although the premium tier is registering the quickest growth, the >USD 500 bracket faces a ceiling in smaller towns where disposable incomes are still normalizing. Surveys show 60% of Gen Z shoppers rely on installment options for experiential buys, making flexible financing essential for premium speaker uptake. Brands counter by offering luxurious designs at mid-range prices, as seen in boAt's Stone Opus that mirrors the Marshall Acton aesthetic at one-third the cost.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Home Aspirations Fuel Premium Segment Growth

- PLI Scheme Manufacturing Incentives Strengthen Domestic Supply Chains

- RF-Radiation Health Concerns Create Consumer Hesitancy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bluetooth-only units held 52.40% revenue in 2025, underscoring the India wireless speaker market preference for simple pairing with smartphones. Smart speakers, propelled by multilingual voice assistants, are advancing at a 22.60% CAGR and are likely to close the gap by 2031. The India wireless speaker market size for smart speakers is projected to climb from USD 0.06 billion in 2025 to USD 0.2 billion in 2031. Display-equipped models such as Amazon Echo Spot broaden use cases from audio playback to recipe help and security feeds. Wi-Fi-only and combo devices address high-fidelity and multi-room needs in premium homes, while BIS-mandated RF caps keep all form factors within safety norms.

Early adoption began in metros, but Hindi, Tamil, and Punjabi language support is unlocking demand among first-time voice-assistant users in tier-2 cities. JBL's Auracast-enabled PartyBox range demonstrates how legacy audio brands are embedding future-proof wireless protocols to maintain relevance. Longer replacement cycles for fixed smart speakers versus portable Bluetooth units imply higher average selling prices and greater revenue-per-user upside, which the India wireless speaker industry leaders view as a strategic growth lever.

Online vendors controlled 65.90% of the India wireless speaker market in 2025, benefiting from deep discounting, fast delivery pledges, and reach across 90% of PIN codes. Organized audio boutiques, however, are growing 22.30% annually as shoppers in the USD 150-plus bracket look to audition devices before paying. The India wireless speaker market size attributed to specialist stores is forecast at USD 0.12 billion by 2031. In metros, brand-owned showrooms double as experience centers, while in tier-2 cities, chains are franchising smaller footprints that combine product demos with immediate service options.

E-commerce remains crucial for entry-level and refresh sales because price comparisons are easiest online. Yet premium buyers often seek advice on codec support, room acoustics, and warranty add-ons that store staff are trained to supply. Successful brands now execute synchronized releases: product goes live on websites and shelves the same day, and invoice data feeds directly into central CRMs to streamline after-sales. Over time, hybrid strategies that let customers buy online and pick up in store are poised to dominate.

Complete Report Scope:

- By Device Type

- Bluetooth-only

- Wi-Fi-only

- Smart Speakers

- Combo (Bluetooth + Wi-Fi)

- By Distribution Channel

- Online (E-tailers, Brand.com)

- Offline - Organised Retail

- Offline - Specialist Audio Stores

- Offline - Hyper/Super-markets

- By Price Range

- Entry-Level (Less than USD 150)

- Mid-Range (USD 150 - 500)

- Premium (Greater than USD 500)

- By End-User

- Residential

- Commercial

- By Region (India)

- North India

- West India

- South India

- East India

- Central India

- North-East India

List of Companies Covered in this Report:

- Amazon Retail India Private Limited

- Imagine Marketing Limited (boAt)

- HARMAN International (India) Pvt. Ltd. (JBL)

- Sony India Private Limited

- Xiaomi Technology India Private Limited

- Samsung India Electronics Private Limited

- Google India Private Limited

- Bose Corporation India Private Limited

- GN Audio A/S (Jabra)

- Koninklijke Philips N.V.

- Portronics Digital Pvt. Ltd.

- Zebronics India Pvt. Ltd.

- Sennheiser Electronics India Pvt. Ltd.

- Marshall Group India

- Logitech Electronics India Private Limited

- Panasonic India Pvt. Ltd.

- OPPO Mobile India Pvt. Ltd. (realme and Dizo speakers)

- Anker Innovations Technology (India) Pvt. Ltd. (Soundcore)

- Fire-Boltt (Savex Technologies Pvt. Ltd.)

- Lenovo (India) Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising smartphone and affordable data penetration

- 4.2.2 Proliferation of OTT music/video streaming services

- 4.2.3 Rising disposable income and aspiration for smart-home gadgets

- 4.2.4 PLI incentives for domestic audio-electronics manufacturing

- 4.2.5 Regional-language voice-assistant roll-outs

- 4.2.6 Telco-bundled speaker + content offers

- 4.3 Market Restraints

- 4.3.1 High price sensitivity in premium tier

- 4.3.2 RF-radiation and child-health concerns

- 4.3.3 Patchy after-sales network beyond metros

- 4.3.4 BIS RF-compliance certification delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Bluetooth-only

- 5.1.2 Wi-Fi-only

- 5.1.3 Smart Speakers

- 5.1.4 Combo (Bluetooth + Wi-Fi)

- 5.2 By Distribution Channel

- 5.2.1 Online (E-tailers, Brand.com)

- 5.2.2 Offline - Organised Retail

- 5.2.3 Offline - Specialist Audio Stores

- 5.2.4 Offline - Hyper/Super-markets

- 5.3 By Price Range

- 5.3.1 Entry-Level (Less than USD 150)

- 5.3.2 Mid-Range (USD 150 - 500)

- 5.3.3 Premium (Greater than USD 500)

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Region (India)

- 5.5.1 North India

- 5.5.2 West India

- 5.5.3 South India

- 5.5.4 East India

- 5.5.5 Central India

- 5.5.6 North-East India

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Retail India Private Limited

- 6.4.2 Imagine Marketing Limited (boAt)

- 6.4.3 HARMAN International (India) Pvt. Ltd. (JBL)

- 6.4.4 Sony India Private Limited

- 6.4.5 Xiaomi Technology India Private Limited

- 6.4.6 Samsung India Electronics Private Limited

- 6.4.7 Google India Private Limited

- 6.4.8 Bose Corporation India Private Limited

- 6.4.9 GN Audio A/S (Jabra)

- 6.4.10 Koninklijke Philips N.V.

- 6.4.11 Portronics Digital Pvt. Ltd.

- 6.4.12 Zebronics India Pvt. Ltd.

- 6.4.13 Sennheiser Electronics India Pvt. Ltd.

- 6.4.14 Marshall Group India

- 6.4.15 Logitech Electronics India Private Limited

- 6.4.16 Panasonic India Pvt. Ltd.

- 6.4.17 OPPO Mobile India Pvt. Ltd. (realme and Dizo speakers)

- 6.4.18 Anker Innovations Technology (India) Pvt. Ltd. (Soundcore)

- 6.4.19 Fire-Boltt (Savex Technologies Pvt. Ltd.)

- 6.4.20 Lenovo (India) Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment