|

市場調查報告書

商品編碼

2073556

北美工業離心機:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Industrial Centrifuge - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

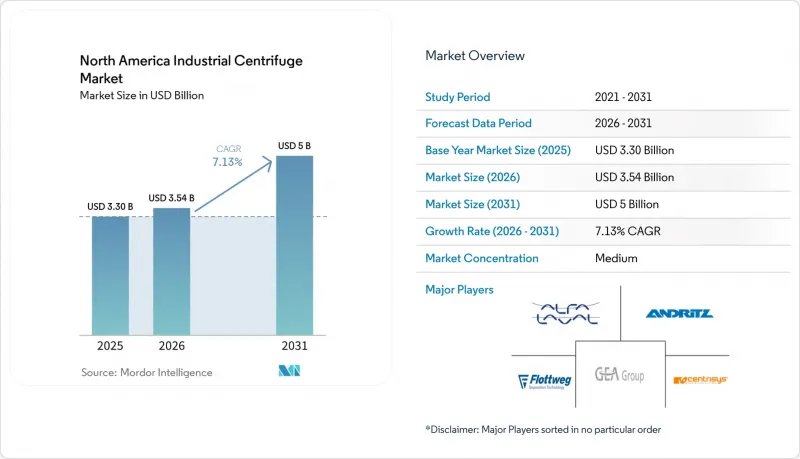

據 Mordor Intelligence 稱,2025 年北美工業離心機市值為 33 億美元,預計到 2031 年將達到 50 億美元,而 2026 年為 35.4 億美元,預測期(2026-2031 年)的複合年成長率為 7.13%。

本報告按「類型(沉澱、過濾)」、「設計(水平、垂直)」、「運作模式(間歇式、連續式)」、「產業領域(食品飲料、製藥和生物技術、水和廢水處理、化學、金屬和採礦、發電等)」以及「地區(美國、加拿大、墨西哥)」對產業進行分類。市場預測以美元計價。

北美工業離心機市場趨勢與洞察

美國和加拿大生物製藥生產能力的擴張正在改變離心機的採購模式。

北美生物製藥產業正經歷大規模的國內製造地擴張,這推動了對用於細胞回收、澄清和蛋白質分離的高速盤式分離器和連續式臥螺離心機的需求。 2026年3月,UCB決定在喬治亞格溫內特縣新建一座佔地46萬平方英尺的生物製藥園區,從而在美國東南部地區新增一個醫藥級離心機的採購基地。這些新建的生物製藥設施計劃長期運作並進行大規模商業化生產,這將進一步推高對具有大規模處理能力的可靠分離設備的需求。一個顯著的變化是,許多此類設施從一開始就被設計為連續生物製造,其設計優先考慮高速分離設備,以取代間歇式過濾。一旦這些佈局獲得批准,離心機的需求往往會在整個工廠運作中與生產線緊密相關。因此,生物製藥產業是北美工業離心機市場最明確的長期需求支柱之一。

旨在減少污水和污泥的法規的推廣,正在創造永續的基礎設施需求。

對生物固形物處理的監管力道加大,推動了市政和工業污水處理系統對臥螺離心機的需求。美國環保署 (EPA) 於 2024 年 1 月最終確定了用於監測污水污泥中 40 種 PFAS 分析物的 1633 方法,並隨後透過 2024 年 12 月簽署的《方法更新規則》將其納入《聯邦法規》第 40 篇第 136 部分。此流程要求污水處理廠業者證明其擁有更強的脫水能力,因為濾餅的乾燥程度會影響用於土地施用的污泥中 PFAS 的濃度。其他合規要求還包括《聯邦法規》第 40 篇第 503 部分、國家污染物排放消除系統 (NPDES) 計劃以及相關的州生物固形物法規,這些法規規定了基於離心機的脫水管線的許可和性能檢驗標準。乾燥固態含量的提高也有助於降低運輸和處置成本,即使在更嚴格的聯邦法規完全實施之前,也為投資設備升級提供了更多理由。因此,污水基礎設施仍是北美工業離心機的穩定需求來源。

高額資本支出 (CAPEX) 和較長的投資回收期限制了中型企業的採用率。

高昂的初始投資成本仍是中型企業加速採用工業離心機的最大障礙。高階製藥用碟片式分離器和大型都市污水污泥滗析機的投資回收期通常超過五年,這對資本預算有限的企業來說難以負擔。這個問題在都市污水處理領域尤為突出,即使營運和監管合規需求明確,核准提價和債券資金籌措也可能導致採購延遲18至36個月。此外,本世紀前五年利率上升的壓力增加了專案評估所需的資本成本,使得設備升級的批准更加困難。因此,一些企業選擇繼續延長舊設備的使用壽命,而不是加快設備升級。這仍然是北美工業離心機市場成長面臨的現實障礙。

細分市場分析

到2025年,沉澱離心機將佔據北美工業離心機市場62.2%的佔有率。這主要得益於臥螺離心機和碟片式離心機系統在污水處理、乳製品加工和生物製藥領域的廣泛應用。臥螺離心機憑藉其穩定可靠的機械性能,能夠處理高固態都市污水污泥,因此在該類離心機中佔據最大佔有率。碟片式離心機仍然是製藥和飲料行業澄清製程的首選,因為這些製程需要更嚴格的顆粒分離和原位清洗。在採礦和紙漿造紙行業的初級脫水工藝中,水力旋流器、澄清罐和濃縮罐系統仍然被廣泛使用,因為在這些行業中,處理能力比最終乾燥度更為重要。此外,與持續改善計畫相關的能源審計也促使工業企業考慮更換老舊的沉澱系統。

預計到2031年,過濾離心機的複合年成長率將達到8.1%,成為北美工業離心機市場成長最快的類型。這一成長主要得益於電池活性物質的分離和精細化學品的結晶,這些領域對更清潔、乾燥的固態以及更嚴格的製程控制提出了更高的要求。橡樹嶺國家實驗室和田納西大學的一項研究(發表於2026年1月的《RSC Advances》期刊)表明,重液離心法在鋰離子電池黑塊回收方面效率超過95%。此結果從技術上支持了過濾方法在高純度資源回收應用的應用。因此,在特種化學品和原料藥(API)的生產中,推料式和剝離式離心機的需求日益成長,因為濾餅純度和低殘留水分是這些領域的核心製程要求。

到2025年,臥式離心機將佔據北美工業離心機市場69.3%的佔有率,這反映了其在連續、大批量作業(例如污水污泥脫水、食用油加工和礦山廢棄物處理)中的優勢。成熟的售後服務網路進一步鞏固了其市場主導地位,提高了各業者的零件供應和技術人員技能水準。這項久經考驗的業績記錄使得連續運轉工廠的擁有成本更具可預測性。這也解釋了為什麼臥式系統仍然是全部區域大批量、高固態含量處理的標準選擇。在2025年年度報告中,阿法拉伐公司宣布其分離技術組合擁有超過4,200項專利,這充分展現了其在食品和水處理應用領域最廣泛使用的設計方案方面深厚的產品研發實力。

預計2026年至2031年間,立式離心機的複合年成長率將達到7.5%,在北美工業離心機市場中超越水平離心機。其需求主要集中在製藥和生物技術工廠,因為垂直離心機的筒體形狀易於融入無塵室佈局,並符合GMP規範下的原位就地清洗(CIP)驗證要求。此外,其形狀也適用於對樓層平面圖和污染控制要求極高的受控生產環境。另一個新興的應用場景是鋰的直接提取,在室溫下進行精確的液液分離即可得到可銷售的碳酸鋰當量,無需傳統的加熱處理。因此,立式離心機的設計與先進的生物製程和特定的清潔能源礦物流密切相關。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 減少污水污泥的監理措施

- 擴大美國和加拿大的生物製藥生產能力

- 食品飲料加工商正在向連續澄清製程過渡。

- 提高能源效率以促進維修(DOE 50001)

- 由美國稅務局 (IRA) 資助的清潔氫能中心需要一台鹽水離心機。

- 電池回收中對「黑色塊」分離的需求

- 市場限制因素

- 高額資本投入和較長的投資回收期

- 透過膜分離技術展開競爭

- 缺乏具備離心機維護和修理專業知識的人員。

- 軸承供應鏈的延誤導致前置作業時間延長。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 地面沉降

- 沉澱池/濃縮池

- 醒酒器

- 磁碟堆疊

- 水力旋流器

- 其他降水處理方法

- 過濾

- 籃子

- 滾動螢幕

- 削皮器

- 推手

- 其他過濾

- 地面沉降

- 有意為之

- 水平的

- 垂直的

- 按操作模式

- 批次

- 連續型

- 按行業

- 食品/飲料

- 製藥和生物技術

- 供水和廢水處理

- 化學品

- 金屬和採礦

- 發電

- 紙漿和造紙

- 其他行業

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合資、資金籌措)

- 市佔率分析

- 公司簡介

- Alfa Laval AB

- Andritz AG

- GEA Group AG

- Flottweg SE

- Centrisys Corp.

- Ferrum AG

- SPX Flow Inc.

- HAUS Centrifuge Technologies

- Hiller GmbH

- B&P Littleford

- Mitsubishi Kakoki Kaisha

- Pieralisi Group

- FLSmidth & Co.

- US Centrifuge Systems

- Tomoe Engineering

- GN Separation

- Trucent Inc.

- Multotec Pty Ltd

- Separation Equipment Co.

- Centrifuges Unlimited Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america industrial centrifuge market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 3.54 billion in 2026 to reach USD 5 billion by 2031, at a CAGR of 7.13% during the forecast period (2026-2031).

This report Segments the Industry Into Type (Sedimentation, Filtering), Design (Horizontal, Vertical), Operation Mode (Batch, Continuous), Industry (Food and Beverages, Pharmaceutical and Biotech, Water and Wastewater Treatment, Chemical, Metals and Mining, Power Generation, and More), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Industrial Centrifuge Market Trends and Insights

Biopharma Capacity Expansion in the U.S. & Canada Is Reshaping Centrifuge Procurement Patterns

North America's biopharmaceutical sector is going through a large domestic manufacturing build-out, and that is sustaining demand for high-speed disc-stack separators and continuous decanters used in cell harvest, clarification, and protein separation. UCB selected Gwinnett County, Georgia, for a new 460,000-square-foot biologics campus in March 2026, adding another procurement center for pharmaceutical-grade centrifuges in the U.S. Southeast. New biologics sites of this kind are being planned for long operating lives and large commercial volumes, which raises the need for reliable separation equipment that can perform at scale. A major shift is that many of these facilities are being designed around continuous biomanufacturing from the outset, and that design choice favors high-speed separators over batch filtration alternatives. Once those layouts are approved, centrifuge demand tends to stay tied to the production line for the life of the plant. This makes biopharma one of the clearest long-cycle demand anchors for the North America industrial centrifuge market.

Regulatory Push for Wastewater-Sludge Reduction Creates Durable Infrastructure Demand

Tighter oversight of biosolids handling is supporting demand for decanter centrifuges across municipal and industrial wastewater systems. The U.S. Environmental Protection Agency finalized Method 1633 in January 2024 for monitoring 40 PFAS analytes in sewage sludge and later moved to incorporate it into 40 CFR Part 136 through a Methods Update Rule signed in December 2024. This process is pushing plant operators to show stronger dewatering performance because cake dryness affects PFAS concentration in sludge that is sent for land application. The compliance burden also sits alongside 40 CFR Part 503, the NPDES program, and related state biosolids rules, which shape permitting and performance verification for centrifuge-based dewatering trains. Better dry solids content also reduces transport and disposal costs, which strengthens the investment case for equipment upgrades even before stricter federal rules are fully implemented. This keeps wastewater infrastructure as a steady demand source for the North America industrial centrifuge market.

High CAPEX and Long Pay-Back Periods Constrain Adoption Velocity Across Mid-Market Operators

High installed cost remains the clearest barrier to faster adoption across mid-market operators. Premium pharmaceutical disc-stack separators and large municipal sludge decanters often require payback periods that stretch beyond 5 years, which is difficult for operators with constrained capital budgets. The issue is strongest in municipal wastewater, where rate-case approvals and bond financing can delay procurement by 18 to 36 months even when the operating and compliance need is clear. Interest rate pressure from the earlier part of the decade also raised the cost of capital used in project appraisal, which made replacement programs harder to approve. Because of this, some operators continue to extend the life of older equipment instead of renewing fleets on a faster schedule. This remains a practical brake on growth for the North America industrial centrifuge market.

Other drivers and restraints analyzed in the detailed report include:

- Food & Beverage Processors Shifting to Continuous Clarification Drives High-Speed Separator Upgrades

- Energy-Efficiency Mandates Under DOE 50001 Framework Are Accelerating Centrifuge Retrofits

- Competition from Membrane-Based Separation Erodes Centrifuge Addressable Market in Select Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sedimentation centrifuges accounted for 62.2% of the North America industrial centrifuge market share in 2025, supported by the entrenched use of decanter and disc-stack systems in wastewater treatment, dairy processing, and biopharma clarification. Decanters retain the widest footprint within this group because they handle high-solids municipal sludge duty cycles with steady mechanical reliability. Disc-stack units remain the premium choice in pharmaceutical and beverage clarification, where tighter particle separation and in-place cleaning are required. Hydrocyclone and clarifier or thickener systems continue to serve primary dewatering stages in mining and pulp and paper operations, where throughput often matters more than final dryness. Energy audits tied to continuous improvement programs are also bringing older sedimentation systems into replacement discussions at industrial sites.

Filtering centrifuges are projected to grow at 8.1% CAGR through 2031, making them the fastest-expanding type in the North America industrial centrifuge market. Growth is being driven by battery-active-material separation and fine-chemical crystallization, where buyers need cleaner dry solids and tighter process control. Research published in RSC Advances in January 2026 by Oak Ridge National Laboratory and the University of Tennessee showed that heavy liquid centrifugal separation achieved more than 95% efficiency in lithium-ion battery black mass recovery. That result gives technical support to the filtering route in high-purity resource recovery applications. Pusher and peeler centrifuges are therefore receiving more procurement attention in specialty chemicals and API manufacturing, where cake purity and low residual moisture are core process requirements.

Horizontal centrifuges held 69.3% of the North America industrial centrifuge market size in 2025, reflecting their strength in continuous high-throughput duties such as sewage sludge dewatering, edible oil processing, and mining tailings management. Their lead is reinforced by a mature service and aftermarket network, which improves parts access and technician familiarity across operator groups. This installed-base advantage keeps ownership costs more predictable for plants that run continuously. It also helps explain why horizontal systems remain the default choice in large-volume and solids-heavy duties across the region. Alfa Laval reported more than 4,200 patents in its separation portfolio in its 2025 annual report, which shows the depth of product development around the designs most used in food and water processing applications.

Vertical centrifuges are forecast to expand at 7.5% CAGR over 2026-2031, outpacing horizontal units in the North America industrial centrifuge market. Demand is centered in pharmaceutical and biotech facilities, where vertical bowl geometries fit cleanroom layouts more easily and support CIP validation in GMP-regulated settings. Their form factor also suits controlled production environments where floor planning and contamination management carry more weight. Another emerging use case is direct lithium extraction, where precise liquid-liquid separation at ambient temperature can support saleable lithium carbonate equivalent without conventional thermal processing. This keeps vertical designs tied to both advanced bioprocessing and selected clean-energy mineral flows.

Complete Report Scope:

- By Type

- Sedimentation

- Clarifier/Thickener

- Decanter

- Disc-stack

- Hydrocyclone

- Other Sedimentation

- Filtering

- Basket

- Scroll-screen

- Peeler

- Pusher

- Other Filtering

- Sedimentation

- By Design

- Horizontal

- Vertical

- By Operation Mode

- Batch

- Continuous

- By Industry

- Food and Beverages

- Pharmaceutical and Biotech

- Water and Wastewater Treatment

- Chemical

- Metals and Mining

- Power Generation

- Pulp and Paper

- Other Industries

- By Country

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Alfa Laval AB

- Andritz AG

- GEA Group AG

- Flottweg SE

- Centrisys Corp.

- Ferrum AG

- SPX Flow Inc.

- HAUS Centrifuge Technologies

- Hiller GmbH

- B&P Littleford

- Mitsubishi Kakoki Kaisha

- Pieralisi Group

- FLSmidth & Co.

- US Centrifuge Systems

- Tomoe Engineering

- GN Separation

- Trucent Inc.

- Multotec Pty Ltd

- Separation Equipment Co.

- Centrifuges Unlimited Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for wastewater-sludge reduction

- 4.2.2 Biopharma capacity expansion in the U.S. & Canada

- 4.2.3 Food & beverage processors shifting to continuous clarification

- 4.2.4 Energy-efficiency mandates (DOE 50001) driving retrofits

- 4.2.5 IRA-funded clean-hydrogen hubs needing brine centrifuges

- 4.2.6 Battery-recycling "black-mass" separation demand

- 4.3 Market Restraints

- 4.3.1 High CAPEX & long pay-back periods

- 4.3.2 Competition from membrane-based separation

- 4.3.3 Skilled centrifuge-maintenance talent shortage

- 4.3.4 Bearings supply-chain delays lengthen lead-times

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Sedimentation

- 5.1.1.1 Clarifier/Thickener

- 5.1.1.2 Decanter

- 5.1.1.3 Disc-stack

- 5.1.1.4 Hydrocyclone

- 5.1.1.5 Other Sedimentation

- 5.1.2 Filtering

- 5.1.2.1 Basket

- 5.1.2.2 Scroll-screen

- 5.1.2.3 Peeler

- 5.1.2.4 Pusher

- 5.1.2.5 Other Filtering

- 5.1.1 Sedimentation

- 5.2 By Design

- 5.2.1 Horizontal

- 5.2.2 Vertical

- 5.3 By Operation Mode

- 5.3.1 Batch

- 5.3.2 Continuous

- 5.4 By Industry

- 5.4.1 Food and Beverages

- 5.4.2 Pharmaceutical and Biotech

- 5.4.3 Water and Wastewater Treatment

- 5.4.4 Chemical

- 5.4.5 Metals and Mining

- 5.4.6 Power Generation

- 5.4.7 Pulp and Paper

- 5.4.8 Other Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global- & Market-level Overview, Core Segments, Financials, Strategic Info, Products & Services, Recent Developments)

- 6.4.1 Alfa Laval AB

- 6.4.2 Andritz AG

- 6.4.3 GEA Group AG

- 6.4.4 Flottweg SE

- 6.4.5 Centrisys Corp.

- 6.4.6 Ferrum AG

- 6.4.7 SPX Flow Inc.

- 6.4.8 HAUS Centrifuge Technologies

- 6.4.9 Hiller GmbH

- 6.4.10 B&P Littleford

- 6.4.11 Mitsubishi Kakoki Kaisha

- 6.4.12 Pieralisi Group

- 6.4.13 FLSmidth & Co.

- 6.4.14 US Centrifuge Systems

- 6.4.15 Tomoe Engineering

- 6.4.16 GN Separation

- 6.4.17 Trucent Inc.

- 6.4.18 Multotec Pty Ltd

- 6.4.19 Separation Equipment Co.

- 6.4.20 Centrifuges Unlimited Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

水力旋流器市場:按類型、材質、壓力等級、技術、終端用戶產業、應用和銷售管道分類-2026-2032年全球市場預測

水力旋流器市場:按類型、材質、壓力等級、技術、終端用戶產業、應用和銷售管道分類-2026-2032年全球市場預測 沉澱和離心分離市場報告:按產品和地區分類 2026-2034 年工業離心分離機市場:按類型、物質分離、速度與應用分類-2026-2032年全球市場預測離心分離器市場:按類型、容量、材質、設計、最終用戶和銷售管道分類-2026-2032年全球市場預測澱粉回收系統市場:按設備類型、終端用戶產業、分銷管道和應用分類的全球預測,2026-2032年濕式離心離合器市場:依產品類型、摩擦材料、額定功率、銷售管道、應用、最終用戶分類,全球預測(2026-2032年)鑽井液減速器市場:按類型、設備配置、技術、鑽井應用、最終用戶分類,全球預測(2026-2032年)旋風乾燥機市場:依技術、運作模式、產能、終端用戶產業及通路分類,全球預測,2026-2032年鑽井泥漿界面活性劑市場按應用、化學成分、功能類型和最終用途產業分類,全球預測(2026-2032年)離心式油分離器市場按類型、材料、流量、終端用戶產業、應用和銷售管道,全球預測,2026-2032年

沉澱和離心分離市場報告:按產品和地區分類 2026-2034 年工業離心分離機市場:按類型、物質分離、速度與應用分類-2026-2032年全球市場預測離心分離器市場:按類型、容量、材質、設計、最終用戶和銷售管道分類-2026-2032年全球市場預測澱粉回收系統市場:按設備類型、終端用戶產業、分銷管道和應用分類的全球預測,2026-2032年濕式離心離合器市場:依產品類型、摩擦材料、額定功率、銷售管道、應用、最終用戶分類,全球預測(2026-2032年)鑽井液減速器市場:按類型、設備配置、技術、鑽井應用、最終用戶分類,全球預測(2026-2032年)旋風乾燥機市場:依技術、運作模式、產能、終端用戶產業及通路分類,全球預測,2026-2032年鑽井泥漿界面活性劑市場按應用、化學成分、功能類型和最終用途產業分類,全球預測(2026-2032年)離心式油分離器市場按類型、材料、流量、終端用戶產業、應用和銷售管道,全球預測,2026-2032年