|

市場調查報告書

商品編碼

2073555

北美工業電池:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Industrial Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

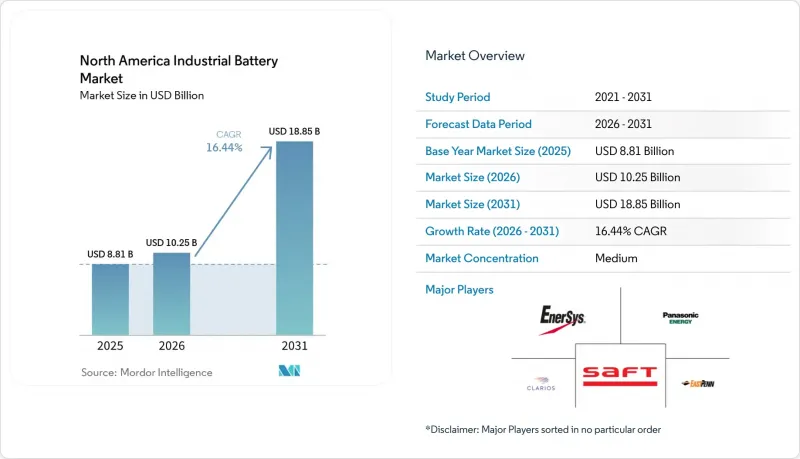

根據 Mordor Intelligence 預測,北美工業電池市場規模預計將在 2025 年達到 88.1 億美元,2026 年達到 102.5 億美元,到 2031 年達到 188.5 億美元,2026 年至 2031 年的複合年成長率為 16.44%。

本報告按技術(鋰離子電池、鉛酸電池、鎳基電池、液流電池、鋅混合電池及其他)、應用(堆高機和自動導引車、通訊備用電源、UPS和資料中心、可再生能源整合工業儲能系統以及鐵路和船舶輔助電源)和地區(美國、加拿大和墨西哥)進行細分。市場預測以美元計價。

北美工業電池市場趨勢與洞察

資料中心彈性系統服務合約“電池即武器”

在北美工業電池市場,資料中心正成為大型UPS和彈性系統最重要的全新需求來源。北美電力可靠性公司(NERC)於2026年5月7日發布了3級警報,指出人工智慧驅動的超大規模負載對美國大型電力系統構成可靠性風險。這提升了快速回應工業電池在關鍵設施中的價值。這項轉變意義重大,因為電池系統不再僅僅作為緊急備用電源,而是被視為能夠穩定電壓、管理短期負載波動並支援高密度運算環境持續運作的重要資產。截至2026年3月,Fluence公司報告稱其已簽訂的累積訂單56億美元,並在2026會計年度第二季與兩家大型超大規模資料中心業者營運商簽訂了主供貨協議。這表明北美工業電池市場已開始將這種需求轉化為實際銷售。因此,北美工業電池市場正從一些應用案例中獲得發展動力,在這些案例中,可靠性價值和作為電網服務的潛在價值被作為一個整體來評估,而不是單獨評估。

北美纖維素細胞和重要礦物可享有IRA稅額扣抵抵免

美國工業關係局(IRA)的生產稅額扣抵框架仍然是北美工業電池市場最重要的結構性支撐之一。 EnerSys公司在2024會計年度累計了1.364億美元的第45X條稅額扣抵,較2023會計年度的1730萬美元大幅成長,這表明受監管的國內生產能夠迅速改變現有製造商的成本結構。 Fluence公司也報告稱,在2026會計年度上半年,其在猶他州的電池模組製造業務因IRA相關政策節省了1090萬美元的成本,證實這些獎勵已經開始影響北美工業電池市場的利潤率結構。從2026年到2030年,隨著《俄勒岡州電池、電池和電池法案》(OBBBA)法規的收緊,限制了外國公司使用零件的範圍,這一優勢將進一步增強,因為獲得聯邦相關需求將越來越取決於價格以及是否遵守國內採購規定。這正在重塑整個北美工業電池市場的採購決策,尤其是對於那些能夠從可追溯的北美地點提供整合電芯、模組和電池組的供應商。

高能量LFP設施職場消防安全法規的責任

由於北美工業電池市場對固定式儲能系統的消防安全法規日益嚴格,其營運面臨許多限制。 2026版NFPA 855標準提高了許多工業裝置的合規標準,擴大了風險緩解分析的範圍,並強化了對認證系統進行大規模防火測試的要求。對於容量超過600千瓦時的裝置,現在需要更嚴格的室內設計要求和防爆措施,這可能會增加專案設計成本,並使現有倉庫和製造地的維修更加複雜。雖然這些法規並未阻止北美工業電池市場採用這些標準,但它們延長了核准流程,並增加了對文件、測試歷史和安裝人員經驗的依賴,從而影響了系統選擇。這給小規模供應商帶來了更大的負擔,但使擁有經過測試和認證系統的大型整合商能夠以最小的延誤完成核准流程。

細分市場分析

到2025年,鋰離子電池將佔據北美工業電池市場59.2%的佔有率,鞏固其在高循環次數工業應用場景中作為標準化學系統的地位。過去幾年,北美工業電池產業一直在穩步朝著這個方向轉型。根據美國製造業數據,出貨收益從2013年的53億美元下降到2022年的22億美元,而同期非鉛酸電池的產值則從7億美元增加到166億美元。這一轉變趨勢在2025年和2026年仍在持續。這是因為,從整體擁有成本的角度來看,鋰離子電池的採用變得更加合理,這得益於其免維護運行、卓越的循環性能以及與自動化運作循環的高度兼容性。 EnerSys 決定關閉其位於蒂華納的鉛酸電池工廠,並將生產轉移到密蘇裡州斯普林菲爾德,這表明現有供應商正在將資本重新分配到更適合北美工業電池市場新結構的產品線和製造地。

預計到2031年,液流電池和鋅混合電池的複合年成長率將達到18.3%,成為北美工業電池市場成長最快的技術類別。這些長壽命化學電池在工業微電網和可再生能源整合設施中最具吸引力,因為在這些應用中,其放電持續時間、不可燃性或運行柔軟性等優勢可能超過主流鋰電池系統在空間和成本方面的優勢。這表明,北美工業電池行業的技術組合比表面上的市場佔有率所顯示的更為廣泛,因為北美工業電池行業並未趨向於為所有應用都採用單一的化學系統。鎳基電池在通訊設備(其工作環境溫度波動劇烈)、鐵路輔助電源以及其他高可靠性環境中仍然發揮著重要作用,在這些環境中,嚴苛運作條件下的穩定性比絕對成本更為重要。因此,就以金額為準,鋰離子電池將繼續主導北美工業電池市場,但長壽命和具有特定用途的化學成分電池將在應用需求比簡單備用電源更為具體的新計畫中佔據更大的佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於承諾的車輛電氣化義務(2026 年起提供購車獎勵)

- 需要全天候運作的自動化倉庫(AGV/AMR)的建設正在迅速增加。

- 電池武器契約,一種確保資料中心容錯能力的電網服務。

- 鋰離子電池組的成本(美元/千瓦時)正在下降。

- 原始設備製造商從開放式鉛酸電池過渡到免維護電池

- 北美電池和關鍵礦產的IRA稅額扣抵抵免累積

- 市場限制因素

- 該地區電池用1級鎳錳提煉能力短缺。

- 高能量LFP設施的職場消防安全法規責任

- 由於美國環保署監理標準收緊,鉛回收出現瓶頸

- 資本密集型單元製造和堆高機需求週期波動。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 價格分析

第5章 市場規模與成長預測

- 透過技術

- 鋰離子

- 鉛酸

- 鎳基

- 流動和鋅混合

- 其他

- 透過使用

- 堆高機和自動化運輸系統

- 通訊備份

- UPS 和資料中心

- 可再生能源整合工業儲能系統

- 鐵路和船舶的輔助動力

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- EnerSys

- East Penn Manufacturing

- Exide Technologies

- Saft Groupe SA

- C&D Technologies

- Panasonic Energy(Panasonic Holdings)

- GS Yuasa Corp.

- Leoch International

- Crown Battery Mfg. Co.

- Clarios

- Tesla(Megapack & Industrial Storage)

- BYD Company Ltd.

- LG Energy Solution

- KORE Power

- Fluence Energy

- ABB(BESS division)

- Mitsubishi Power Americas

- EVE Energy USA

- Navitas Systems

- Amara Raja Batteries USA

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america industrial battery market size is projected to be USD 8.81 billion in 2025, USD 10.25 billion in 2026, and reach USD 18.85 billion by 2031, growing at a CAGR of 16.44% from 2026 to 2031.

This report is Segmented by Technology (Lithium-Ion, Lead-Acid, Nickel-Based, Flow & Zinc-Hybrid, Others), Application (Forklift & Automated Material Handling, Telecom Backup, UPS & Data-Center, Renewable-Integrated Industrial ESS, Rail & Marine Auxiliary Power), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Industrial Battery Market Trends and Insights

Grid-Service "Battery-as-a-Weapon" Contracts for Data-Center Resiliency

The North America industrial batteries market is seeing data centers emerge as the most important new demand center for large-scale UPS and resiliency systems. NERC issued a Level 3 Alert on May 7, 2026, and identified AI-driven hyperscale loads as a reliability risk to the US bulk power system, which raised the value of fast-response industrial batteries in critical facilities. This shift matters because battery systems are no longer being purchased only for emergency backup, they are now being evaluated as assets that can stabilize voltage, manage short-duration load swings, and support continuity in high-density compute environments. Fluence reported a contracted backlog of USD 5.6 billion as of March 2026 and signed master supply agreements with 2 major hyperscalers in fiscal Q2 2026, showing that the North America industrial batteries market is already converting this demand into booked revenue. As a result, the North America industrial batteries market is gaining support from a use case where reliability value and potential grid-service value are being assessed together instead of separately.

IRA Tax-Credit Stack for North America-Sourced Cells and Critical Minerals

The IRA production credit framework remains one of the clearest structural supports for the North America industrial batteries market. EnerSys recognized USD 136.4 million in Section 45X credits in fiscal 2024, up from USD 17.3 million in fiscal 2023, which shows how quickly compliant domestic production can change the cost position of established manufacturers. Fluence also reported USD 10.9 million in IRA-linked cost reductions in the first half of fiscal 2026 tied to its Utah battery module manufacturing, confirming that these incentives are already influencing margin structures in the North America industrial batteries market. The OBBBA restrictions that tighten prohibited foreign entity content from 2026 through 2030 deepen this advantage, because access to federal-linked demand increasingly depends on domestic sourcing compliance rather than price alone. This is reshaping procurement decisions across the North America industrial batteries market, especially for suppliers that can offer cells, modules, and pack integration from a traceable North American base.

Workplace Fire-Code Liabilities for High-Energy LFP Installations

The North America industrial batteries market faces a real execution constraint from tighter fire-code requirements around stationary storage. The 2026 edition of NFPA 855 raised the compliance threshold for many industrial installations by requiring Hazard Mitigation Analysis more broadly and reinforcing large-scale fire testing expectations for qualifying systems. Installations above 600 kWh now face stricter room design and explosion-prevention expectations, which raises project design cost and can complicate retrofits in existing warehouses and manufacturing sites. These rules do not stop deployment in the North America industrial batteries market, but they do extend approval cycles and make system selection more dependent on documentation, testing history, and installer experience. The burden is heavier for smaller suppliers, while larger integrators with tested and listed systems can move through the permitting process with fewer delays.

Other drivers and restraints analyzed in the detailed report include:

- Surging Automated-Warehouse Build-Outs Demanding 24X7 Motive Power (AGV/AMR)

- Commitment-Driven Fleet Electrification Mandates

- Lead Recycling Bottlenecks Amid Tightened EPA Thresholds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 59.2% of the North America industrial batteries market share in 2025, which confirms that it has become the default chemistry across high-cycle industrial use cases. The North America industrial batteries industry has moved steadily in this direction for several years, as US domestic manufacturing data already showed lead-acid shipment value falling from USD 5.3 billion in 2013 to USD 2.2 billion in 2022 while non-lead-acid output rose from USD 0.7 billion to USD 16.6 billion over the same period. This shift continued through 2025 and 2026 because maintenance-free operation, better cycling performance, and stronger compatibility with automated duty cycles make lithium-ion easier to justify on a total ownership basis. EnerSys's decision to close its Tijuana lead-acid plant and shift production to Springfield, Missouri shows how incumbent suppliers are redirecting capital toward product lines and manufacturing footprints that fit the new structure of the North America industrial batteries market.

Flow & Zinc-hybrid is projected to expand at an 18.3% CAGR through 2031, making it the fastest-growing technology group in the North America industrial batteries market. The appeal of these long-duration chemistries is strongest in industrial microgrids and renewable-linked installations where discharge duration, non-flammability, or operating flexibility can outweigh the space and cost advantages of mainstream lithium systems. This opens a wider technology mix than the headline share split suggests, because the North America industrial batteries industry is not moving toward a single chemistry for every application. Nickel-based batteries still retain relevance in temperature-variable telecom, rail auxiliary power, and other high-reliability settings where stability under harsher operating conditions remains more important than absolute cost. The practical result is that lithium-ion will continue to dominate the North America industrial batteries market by value, but long-duration and niche chemistries will capture a larger share of new projects where application needs are more specific than simple backup power.

Complete Report Scope:

- By Technology

- Lithium-ion

- Lead-acid

- Nickel-based

- Flow & Zinc-hybrid

- Others

- By Application

- Forklift & Automated Material Handling

- Telecom Backup

- UPS & Data-Center

- Renewable-integrated Industrial ESS

- Rail & Marine Auxiliary Power

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- EnerSys

- East Penn Manufacturing

- Exide Technologies

- Saft Groupe SA

- C&D Technologies

- Panasonic Energy (Panasonic Holdings)

- GS Yuasa Corp.

- Leoch International

- Crown Battery Mfg. Co.

- Clarios

- Tesla (Megapack & Industrial Storage)

- BYD Company Ltd.

- LG Energy Solution

- KORE Power

- Fluence Energy

- ABB (BESS division)

- Mitsubishi Power Americas

- EVE Energy USA

- Navitas Systems

- Amara Raja Batteries USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commitment-driven fleet electrification mandates (post-2026 purchase incentives)

- 4.2.2 Surging automated-warehouse build-outs demanding 24/7 motive-power (AGV/AMR)

- 4.2.3 Grid-service "battery-as-a-weapon" contracts for data-center resiliency

- 4.2.4 Declining USD/kWh lithium-ion pack costs

- 4.2.5 OEM shift from flooded lead-acid to maintenance-free chemistries

- 4.2.6 IRA tax-credit stack for NA-sourced cells and critical minerals

- 4.3 Market Restraints

- 4.3.1 Scarcity of regional Class-1 nickel & battery-grade manganese refining

- 4.3.2 Workplace fire-code liabilities for high-energy LFP installations

- 4.3.3 Lead recycling bottlenecks amid tightened EPA thresholds

- 4.3.4 Capital-intensive cell manufacturing vs. volatile forklift demand cycle

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Pricing Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Nickel-based

- 5.1.4 Flow & Zinc-hybrid

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Forklift & Automated Material Handling

- 5.2.2 Telecom Backup

- 5.2.3 UPS & Data-Center

- 5.2.4 Renewable-integrated Industrial ESS

- 5.2.5 Rail & Marine Auxiliary Power

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 EnerSys

- 6.4.2 East Penn Manufacturing

- 6.4.3 Exide Technologies

- 6.4.4 Saft Groupe SA

- 6.4.5 C&D Technologies

- 6.4.6 Panasonic Energy (Panasonic Holdings)

- 6.4.7 GS Yuasa Corp.

- 6.4.8 Leoch International

- 6.4.9 Crown Battery Mfg. Co.

- 6.4.10 Clarios

- 6.4.11 Tesla (Megapack & Industrial Storage)

- 6.4.12 BYD Company Ltd.

- 6.4.13 LG Energy Solution

- 6.4.14 KORE Power

- 6.4.15 Fluence Energy

- 6.4.16 ABB (BESS division)

- 6.4.17 Mitsubishi Power Americas

- 6.4.18 EVE Energy USA

- 6.4.19 Navitas Systems

- 6.4.20 Amara Raja Batteries USA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球工業電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球工業電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 工業電池市場報告:按驅動系統、技術、應用和地區分類(2026-2034 年)

工業電池市場報告:按驅動系統、技術、應用和地區分類(2026-2034 年) 工業電池市場:2026-2032年全球市場預測(依電池化學成分、產品類型、容量範圍、安裝方式、應用領域、終端用戶產業及通路分類)

工業電池市場:2026-2032年全球市場預測(依電池化學成分、產品類型、容量範圍、安裝方式、應用領域、終端用戶產業及通路分類) 工業電池市場:按電池類型、應用和地區分類

工業電池市場:按電池類型、應用和地區分類 工業電池市場規模、佔有率和成長分析(適用於物料輸送設備):按電池類型、應用、最終用戶、技術採用、銷售管道和地區分類-2026-2033年產業預測

工業電池市場規模、佔有率和成長分析(適用於物料輸送設備):按電池類型、應用、最終用戶、技術採用、銷售管道和地區分類-2026-2033年產業預測 2026年全球工業機器人電池市場報告2026年全球工業電池市場報告

2026年全球工業機器人電池市場報告2026年全球工業電池市場報告 工業電池市場 - 全球產業規模、佔有率、趨勢、機會、預測(按類型、應用、地區和競爭格局分類),2021-2031年

工業電池市場 - 全球產業規模、佔有率、趨勢、機會、預測(按類型、應用、地區和競爭格局分類),2021-2031年 工業電池市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測

工業電池市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測 施工機械電池:全球市佔率及排名、總收入及需求預測(2025-2031年)

施工機械電池:全球市佔率及排名、總收入及需求預測(2025-2031年)