|

市場調查報告書

商品編碼

2073548

認同分析:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Identity Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

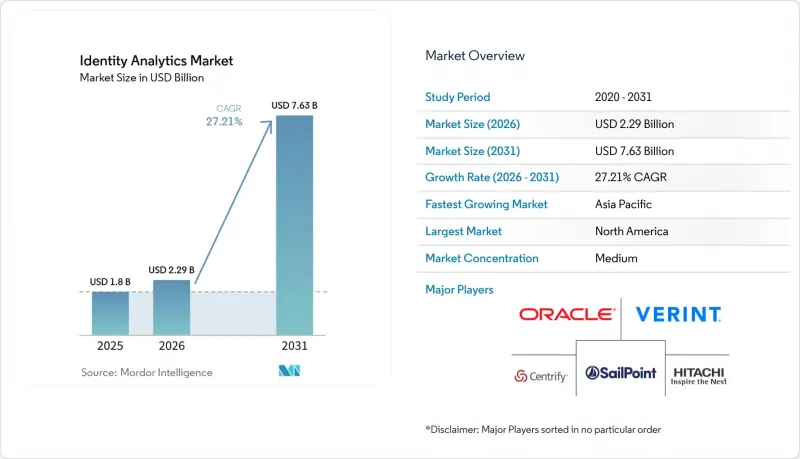

根據 Mordor Intelligence 預測,身分分析市場規模將從 2025 年的 18 億美元成長到 2026 年的 22.9 億美元,然後在 2031 年達到 76.3 億美元,2026 年至 2031 年的複合年成長率為 27.21%。

本報告按元件類型(解決方案、服務)、部署模式(本地部署、雲端部署)、企業規模(中小企業、大型企業)、最終用戶產業(資訊科技和電信、銀行、金融服務和保險、其他)以及地區進行細分。市場預測以美元計價。

全球身分分析市場趨勢與洞察

利用深度造假進行的身份攻擊激增

預計到2024年,深度造假將激增3,000%,目前佔全球所有詐騙的6.5%。根據美國國防安全保障部統計,合成身分佔所有身分詐騙案件的85%。人工智慧生成工具的普及使得攻擊者能夠繞過靜態生物識別驗證,迫使企業實施融合行為、裝置和加密訊號的多層分析。能夠即時偵測人工智慧產生內容的供應商在試點計畫中佔據優勢,而深度造假應對措施正迅速成為競標中的關鍵評估標準。這項威脅的迫切性正促使身分分析投資從可選項提升為董事會層面的風險緩解策略。

強制性零信任與機器身分管治

行政命令 14144 號要求美國聯邦機構在 2025 年 12 月前實施防釣魚身分驗證,從而推動企業更廣泛地採用零信任架構。機器間身分的數量已經超過了人類帳戶的數量,而未託管的服務憑證會使雲端工作負載面臨橫向移動攻擊的風險。 IBM 對 HashiCorp 技術的整合標誌著向統一身分架構的轉變,該架構能夠發現、分類和管理數百萬個 API 金鑰和憑證。合規期限導致採購週期時間緊迫,迫使各組織優先考慮具有內建管治策略的分析平台。由此產生的需求成長遍及公共和私營部門,身分分析市場的成長已被納入多年預算藍圖。

Petabyte級即時分析的高總擁有成本

處理Petabyte身分資料可能導致大型企業每年基礎設施支出超過1,000萬美元,而安全事件期間查詢的意外激增會進一步加劇成本波動。當客戶以持續吞吐量攝取串流日誌時,雲端收費模式通常缺乏價格可預測性。因此,中型企業為了確保預算確定性,不得不犧牲透明度,例如延遲採用進階分析或限制遙測資料的保留期限。雖然將運算資源成本分攤到各個租戶的託管SaaS模式正在逐漸普及,但利潤率仍然極易受到雲端出口費用和GPU租賃費用的影響。在成本管理工具成熟之前,對於預算緊張的買家而言,採購週期可能會非常漫長。

細分市場分析

預計到2025年,解決方案將維持62.40%的收入佔有率,透過提供管治、風險評分和編配等功能的整合平台,推動身分分析市場的發展。同時,服務收入正以33.17%的複合年成長率成長,反映出企業在遷移藍圖、合規性和模型最佳化方面對供應商專業知識的依賴。預計到2031年,身分分析市場的服務佔有率將超過35.4億美元,凸顯了專業顧問公司在將平台功能轉化為實際營運成果方面發揮的關鍵作用。身分分析資料科學家長期短缺進一步推動了服務需求,迫使企業採用SailPoint等供應商提供的「成功加速套件」。

專業服務旨在應對部署後的挑戰,例如持續的模型微調和攻擊面重新評估。隨著經營團隊尋求風險降低的證據,服務團隊會對詐欺指標進行基準測試,最佳化偵測閾值,並建立補救工作流程。這種生命週期支援將一次性專案轉化為持續性收入。同時,解決方案格局正在向模組化微服務演進,使企業能夠按需啟用分析功能,並僅為實際使用的容量付費。軟體包與全面支援服務之間的協同作用,使全端提供者能夠在整體身分分析市場中佔據更大的佔有率。

預計到 2025 年,雲端採用將佔營收的 70.30%,並在預測期內成長 30.62%。這部分歸功於企業致力於舊有系統進行現代化改造。彈性運算、API 優先整合和內建高可用性是推動此需求的主要因素。然而,許多組織仍在維護混合環境,並行運行本地和 SaaS 目錄,而遷移過程則需要數年時間。這種共存階段增加了分析工作量,因為必須從兩個環境中收集資料並即時執行相關性分析。因此,雲端平台正在著重開發各種連接器和策略調整引擎,以便能夠解析傳統的屬性結構。

身分分析市場佔有率正迅速轉向基於使用量的定價模式,像AIG這樣的保險公司現在為透過雲端平台進行持續監控的客戶提供保費折扣。這一遷移藍圖是基於微軟公開的Entra ID方案和參考架構,這些方案和架構已成為業界事實上的實施模式。雖然在本地部署和雲端混合部署階段整體擁有成本(TCO)可能會增加,但如果消除本地硬體更新周期,從長遠來看,雲端模式將更具經濟優勢。能夠提供精細化的基於使用量的收費以及租戶間資料隔離的供應商在採購中具有競爭優勢,尤其對於受資料居住法規約束的跨國公司而言更是如此。

區域分析

北美在2025年仍維持41.60%的市場佔有率,這得益於第14144號行政命令的強制實施以及分析供應商的高度集中。儘管聯邦政府的最後期限推動了短期支出的激增,但美國企業正在利用與複雜身分管理系統相關的豐厚網路保險收益。加拿大的數位認證框架和墨西哥快速發展的金融科技生態系統正在促進市場成長,並鞏固該地區的領先地位。遵守NIST SP-800-63指南進一步加速了平台升級,並將北美打造為零信任成熟度的標竿市場。

在《歐洲數位身分法規》的推動下,歐洲也紛紛效仿,該法規要求在2027年實現錢包解決方案的互通性。英國目前已有270家數位身分相關企業,年收入達20.5億美元。德國和法國則強調“隱私設計”,要求供應商將使用者同意管理和策略版本控制納入其分析工作流程。資料主權條款和跨境資料傳輸法規推動了對區域資料中心和使用中資料加密功能的需求。因此,雲端服務供應商正在歐洲各地擴展其可用區,以滿足本地化處理需求並保持競爭優勢。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到32.86%。政府主導的電子身分(eID)計劃,例如印尼12億美元的「數位轉型夥伴關係」和澳洲2024年的《數位身分法案》,正在建立必要的檢驗層,而這些驗證層需要大規模的分析。印度Aadhaar的成功以及中國龐大的數位交易量,為鄰國提供了最佳實踐,加速了東協地區的普及。該地區對5G基礎設施的投資以及行動支付的普及,正在催生高速身分遙測數據,這需要基於雲端的分析能力。隨著跨境數位商務的成長,提供語言無關介面和本地託管資料選項的供應商將佔據有利地位,擴大其市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 利用深度造假進行身分冒用攻擊的案件激增

- 強制性零信任與機器身分管治

- 遷移到雲端原生身分架構

- 利用生成式人工智慧提升詐欺偵測效能

- 基於分析結果的網路保險保費折扣

- 引入政府主導的電子識別計劃

- 市場限制因素

- Petabyte級即時分析的高總擁有成本

- 重視身分識別的資料科學人才短缺。

- 傳統身分與存取管理 (IAM) 技術堆疊之間的互通性差距

- UEBA中關於「隱私設計」的監理挑戰

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 投資分析

第5章 市場規模與成長預測

- 依組件類型

- 解決方案

- 服務

- 按部署模式

- 現場

- 雲

- 按公司規模

- 小型企業

- 大公司

- 按最終用戶行業分類

- 資訊科技和通訊

- 銀行、金融服務和保險(BFSI)

- 政府/公共部門

- 零售與消費

- 醫療保健和生命科學

- 製造業、能源、公共產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Okta Inc.

- Microsoft Corporation

- Oracle Corporation

- International Business Machines Corporation

- SailPoint Technologies Holdings Inc.

- Ping Identity Holding Corp.

- CyberArk Software Ltd.

- Saviynt Inc.

- Thales Group(Thales Digital Identity and Security)

- HID Global Corporation

- Idemia Group SAS

- Verint Systems Inc.

- LogRhythm Inc.

- Securonix Inc.

- Gurucul Solutions LLC

- MicroStrategy Incorporated

- One Identity LLC

- ForgeRock Inc.

- Centrify Corporation

- Transmit Security Ltd.

- Eviden(an Atos business)

第7章 市場機會與未來展望

According to Mordor Intelligence, the identity analytics market size is expected to grow from USD 1.8 billion in 2025 to USD 2.29 billion in 2026 and is forecast to reach USD 7.63 billion by 2031 at 27.21% CAGR over 2026-2031.

This report is Segmented by Component Type (Solutions, Services), Deployment Model (On-Premises, Cloud), Enterprise Size (Small & Medium Enterprises, Large Enterprises), End-User Industry (Information Technology & Telecommunication, BFSI and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Identity Analytics Market Trends and Insights

Surge in Deep-fake-driven Identity Attacks

Deepfake-enabled impersonation skyrocketed 3,000% in 2024, now representing 6.5% of global fraud attempts. Synthetic identities account for 85% of total identity fraud cases, according to the U.S. Department of Homeland Security. The democratization of generative-AI tooling means threat actors can bypass static biometric checks, compelling enterprises to deploy multilayered analytics that fuse behavioural, device and cryptographic signals. Vendors able to detect AI-generated content in real time are winning proof-of-concept trials, and deepfake mitigation is rapidly becoming a core evaluation criterion in competitive tenders. The urgency of this threat elevates identity analytics investments from discretionary spending to board-level risk mitigation.

Zero-Trust and Machine-Identity Governance Mandates

Executive Order 14144 requires U.S. federal agencies to implement phishing-resistant authentication by December 2025, catalysing broader enterprise zero-trust adoption. Machine-to-machine identities already outnumber human accounts, and unmanaged service credentials expose cloud workloads to lateral-movement attacks. IBM's integration of HashiCorp technology illustrates a shift toward unified identity fabrics that discover, classify and govern millions of API keys and certificates. Compliance deadlines translate into time-boxed procurement cycles, pushing organizations to favour analytics platforms that ship with embedded governance policies. The resulting demand uplift spans public and private sectors, embedding identity analytics market growth into multi-year budget roadmaps.

High TCO of Real-time Analytics at Petabyte Scale

Processing petabyte-level identity data can push annual infrastructure outlays above USD 10 million for large enterprises, and unexpected query spikes during security incidents aggravate cost volatility. Cloud billing models often lack price predictability when customers ingest streaming logs at sustained throughput. Mid-size organizations therefore delay advanced analytics deployments or limit telemetry retention windows, trading visibility for budget certainty. Managed SaaS models that amortize compute across tenants are gaining traction, but margins remain sensitive to cloud egress and GPU leasing rates. Until cost-management tooling matures, procurement cycles may lengthen for budget-constrained buyers.

Other drivers and restraints analyzed in the detailed report include:

- Migration to Cloud-native Identity Fabric

- Gen-AI-based Fraud-detection Performance Gains

- Shortage of Identity-centric Data-science Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained a 62.40% revenue share in 2025, anchoring the identity analytics market with integrated platforms that deliver governance, risk scoring and orchestration. Yet services revenue is advancing at a 33.17% CAGR, reflecting enterprises' dependence on vendor expertise for migration roadmaps, regulatory alignment and model optimization. The services contribution to the identity analytics market size is forecast to surpass USD 3.54 billion by 2031, underscoring professional consultancies' role in translating platform capabilities into operational outcomes. Ongoing shortages of identity-centric data scientists further fuel services demand, compelling organizations to engage success-acceleration packages from vendors like SailPoint.

Professional services also address post-implementation challenges such as continuous model tuning and attack-surface reassessment. As executive leadership demands evidence of risk reduction, service teams benchmark fraud metrics, refine detection thresholds and structure remediation workflows. This lifecycle support converts one-time projects into recurring revenue. Conversely, the solutions segment is evolving toward modular micro-services, allowing enterprises to activate analytics functions on demand and pay only for utilized capacity. The interplay between packaged software and high-touch services positions full-stack providers to capture larger wallet share across the identity analytics market.

Cloud deployments represented 70.30% of 2025 revenue and are projected to grow at 30.62% over the forecast horizon, driven in part by enterprise legacy modernization initiatives. Demand is fuelled by elastic compute, API-first integration and built-in high availability. Many organizations, however, operate hybrid estates during multiyear transitions, with parallel on-premises and SaaS directories. This coexistence phase elevates analytics workloads because data must be collected across both environments and correlated in real time. Cloud platforms therefore emphasize connector breadth and policy reconciliation engines that interpret legacy attribute structures.

Identity analytics market share is shifting decisively toward consumption-based pricing, and insurers such as AIG now link premium discounts to customers that evidence continuous monitoring via cloud platforms. Migration roadmaps are informed by Microsoft's published Entra ID playbooks and reference architectures, setting de-facto industry implementation patterns. While total cost of ownership can rise during dual-running periods, long-term economics favour cloud models once on-premises hardware refresh cycles are avoided. Vendors offering granular usage billing and cross-tenant data isolation are positioned to win procurement rounds, especially within multinational enterprises subject to data-residency regulations.

Complete Report Scope:

- By Component Type

- Solutions

- Services

- By Deployment Model

- On-Premise

- Cloud

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Industry

- Information Technology and Telecommunication

- Banking, Financial Services and Insurance (BFSI)

- Government and Public Sector

- Retail and Consumer

- Healthcare and Life Sciences

- Manufacturing, Energy and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America retained a 41.60% revenue share in 2025, buoyed by the Executive Order 14144 mandate and a dense concentration of analytics vendors. Federal deadlines drive near-term spending spikes, while U.S. enterprises leverage favourable cyber-insurance economics tied to advanced identity postures. Canada's digital credential framework and Mexico's burgeoning fintech ecosystem contribute incremental growth, reinforcing regional leadership. Compliance alignment with NIST SP-800-63 guidelines further stimulates platform upgrades and positions North America as the reference market for zero-trust maturity.

Europe follows closely, propelled by the European Digital Identity Regulation that requires interoperable wallet solutions by 2027. The United Kingdom already hosts 270 digital-identity companies, generating USD 2.05 billion in annual revenue. Germany and France emphasize privacy-by-design, obliging vendors to embed consent orchestration and policy versioning into analytics workflows. Data-sovereignty clauses and cross-border transfer rules drive demand for regional data centers and encryption-in-use capabilities. As a result, cloud providers expand European availability zones to accommodate localized processing and maintain competitive parity.

Asia-Pacific represents the fastest-growing region with a 32.86% CAGR forecast through 2031. Government-backed eID schemes, such as Indonesia's USD 1.2 billion digital-transformation partnership and Australia's Digital ID Act 2024, establish mandatory verification layers that require analytics at scale. India's Aadhaar success and China's vast volume of digital transactions provide proof points for neighbouring economies, catalysing uptake across ASEAN. The region's investment in 5G infrastructure and mobile-money adoption creates high-velocity identity telemetry that demands cloud-based analytic performance. Vendors offering language-agnostic interfaces and regionally hosted data options are well placed to gain share as cross-border digital-commerce expands.

- Okta Inc.

- Microsoft Corporation

- Oracle Corporation

- International Business Machines Corporation

- SailPoint Technologies Holdings Inc.

- Ping Identity Holding Corp.

- CyberArk Software Ltd.

- Saviynt Inc.

- Thales Group (Thales Digital Identity and Security)

- HID Global Corporation

- Idemia Group SAS

- Verint Systems Inc.

- LogRhythm Inc.

- Securonix Inc.

- Gurucul Solutions LLC

- MicroStrategy Incorporated

- One Identity LLC

- ForgeRock Inc.

- Centrify Corporation

- Transmit Security Ltd.

- Eviden (an Atos business)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in deep-fake-driven identity attacks

- 4.2.2 Zero-Trust and machine-identity governance mandates

- 4.2.3 Migration to cloud-native identity fabric

- 4.2.4 Gen-AI-based fraud-detection performance gains

- 4.2.5 Cyber-insurance premium discounts tied to analytics

- 4.2.6 Government-backed eID program roll-outs

- 4.3 Market Restraints

- 4.3.1 High TCO of real-time analytics at petabyte scale

- 4.3.2 Shortage of identity-centric data-science talent

- 4.3.3 Inter-operability gaps across legacy IAM stacks

- 4.3.4 Privacy-by-design regulatory hurdles for UEBA

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component Type

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Information Technology and Telecommunication

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Government and Public Sector

- 5.4.4 Retail and Consumer

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Manufacturing, Energy and Utilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Okta Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 SailPoint Technologies Holdings Inc.

- 6.4.6 Ping Identity Holding Corp.

- 6.4.7 CyberArk Software Ltd.

- 6.4.8 Saviynt Inc.

- 6.4.9 Thales Group (Thales Digital Identity and Security)

- 6.4.10 HID Global Corporation

- 6.4.11 Idemia Group SAS

- 6.4.12 Verint Systems Inc.

- 6.4.13 LogRhythm Inc.

- 6.4.14 Securonix Inc.

- 6.4.15 Gurucul Solutions LLC

- 6.4.16 MicroStrategy Incorporated

- 6.4.17 One Identity LLC

- 6.4.18 ForgeRock Inc.

- 6.4.19 Centrify Corporation

- 6.4.20 Transmit Security Ltd.

- 6.4.21 Eviden (an Atos business)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

身分分析市場規模、佔有率、趨勢和預測:按分析類型、組件、部署方式、組織規模、行業和地區分類,2026-2034 年

身分分析市場規模、佔有率、趨勢和預測:按分析類型、組件、部署方式、組織規模、行業和地區分類,2026-2034 年 身分分析市場:2026-2032年全球市場預測(依產品類型、部署模式、組織規模、技術、最終用戶產業及銷售管道)

身分分析市場:2026-2032年全球市場預測(依產品類型、部署模式、組織規模、技術、最終用戶產業及銷售管道) 全球身分分析市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球身分分析市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 人工智慧身分分析解決方案市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭對手分類,2021-2031年身分管治與管理解決方案市場:2026-2032 年全球預測(按組件、部署類型、組織規模和產業分類)

人工智慧身分分析解決方案市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭對手分類,2021-2031年身分管治與管理解決方案市場:2026-2032 年全球預測(按組件、部署類型、組織規模和產業分類) 身分分析市場規模、佔有率和成長分析(按組件、組織規模、部署類型、應用、最終用途和地區分類)-2026-2033年產業預測身分分析市場 - 2025-2030 年預測

身分分析市場規模、佔有率和成長分析(按組件、組織規模、部署類型、應用、最終用途和地區分類)-2026-2033年產業預測身分分析市場 - 2025-2030 年預測