|

市場調查報告書

商品編碼

2073526

自動化貼標機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automatic Labeling Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

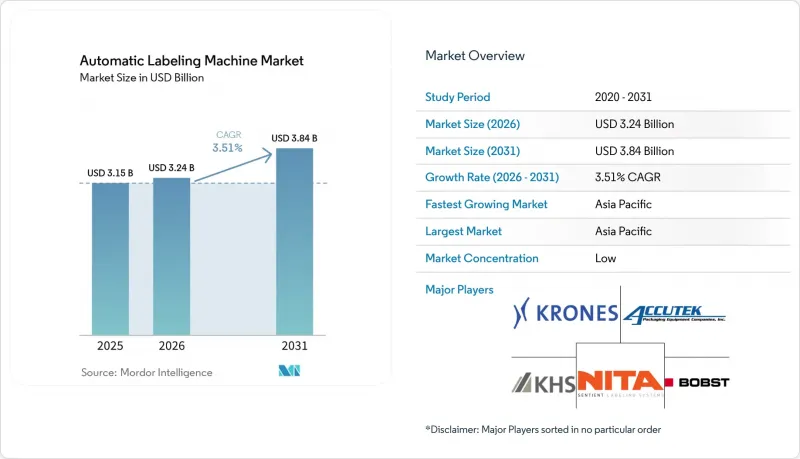

根據 Mordor Intelligence 預測,自動貼標機市場規模將從 2025 年的 31.5 億美元和 2026 年的 32.4 億美元成長到 2031 年的 38.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 3.51%。

本報告按技術(壓敏貼膜、收縮套標等)、機器配置(線上式、旋轉式、列印貼標式、模組化/混合式)、貼標速度(低於 60 BPM、61–200 BPM、201–400 BPM、高於 400 BPM)、最終用戶(飲料、藥品、個人護理/地區進行細分)。市場預測以美元 (USD) 為單位。

全球自動化貼標機市場趨勢及洞察

醫藥和醫療設備產業需要更嚴格的序列化和UDI法規。

為遵守美國《藥品供應鏈安全法案》(DSCSA)、歐盟《反仿冒藥品指令》以及中國2024年《藥品管理法》,製藥和醫療設備製造商必須在其銷售的每個單位、包裝盒和托盤上列印唯一識別碼。過去依賴獨立機械貼標機的公司正在對其生產線進行改造,加裝2D資料矩陣印表機、視覺檢驗系統和資料庫連接功能,以即時同步序號。契約製造製造商正在加速這些升級,以維持出口認證,並將採購預算從通用包裝設備轉向整合式列印貼標模組。這種轉變有利於擁有ISO 9001和FDA 21 CFR Part 11認證的供應商,因為他們能夠提供監管審查所需的驗證方案。

精釀飲料小批量 SKU 激增

精釀啤酒廠和手工釀酒廠的平均SKU數量從五年前的20個增加到今天的75個。這種快速成長使得預印標籤的庫存管理效率低落。模組化自動化貼標機平台結合了噴墨或熱轉印列印以及壓敏標籤功能,使生產商能夠在幾分鐘內更換標籤圖案,從而最大限度地減少季節性產品和合作款產品的標籤過時問題。例如,SwiftColor SCC-4000D等解決方案能夠以高達每分鐘60英尺的速度列印全彩可變數據標籤,使限量版飲品能夠在概念獲批後的幾天內上架商店。這一趨勢也正在蔓延到特色食品和直銷化妝品領域,擴大了能夠提供中速快速標籤更換功能的貼標機的收入基礎。

高額資本支出(CAPEX)與租賃或外包包裝方案的比較

許多面臨融資困境的食品和個人護理品牌正在增加設備租賃和生產外包,推遲直接採購。據ProMach公司稱,隨著負責人將資金從機械設備轉向數位宣傳活動,2024年設備租賃諮詢量激增35%。像達美樂披薩的「貼標即服務」這樣的訂閱模式,將硬體、耗材和遠端監控包含在月費中,從而將風險從品牌所有者轉移到供應商。雖然這些服務拓展了使用機會,但也給初始收入帶來了壓力,短期內會減緩自動貼標機的市場成長。

細分市場分析

預計從2025年到2031年,套標機將以4.24%的複合年成長率成長,成為自動化貼標機市場所有技術中成長最快的。 2025年,壓敏貼標機仍將佔據自動化貼標機市場39.83%的佔有率,其優勢在於可進行合規性標記、可變數據處理以及易於更換標籤。全包覆式收縮套標因其防篡改功能和360度全方位圖形展示(無需瓶身壓紋)而備受能量飲料和即飲雞尾酒品牌的青睞。拉伸套採用單一材料,可回收利用,因此受到遵守歐洲生產者責任法規的果汁和乳製品生產商的青睞。雖然冷膠貼標機由於單張標籤成本較低,在傳統啤酒生產線中仍佔據主導地位,但其固定格式會導致SKU更換時停機時間延長,促使釀酒商轉向模組化套標和壓敏貼標頭。伺服控制接縫重疊修剪等創新技術減少了 15% 的薄膜浪費,實現了降低成本和永續性的目標。

客製印刷的融合正在重新定義技術邊界。 Domino 的 N610i 噴墨列印頭可直接安裝到現有的壓敏貼標機上,並支援每分鐘 300 公尺的可變資料流,從而消除了列印和貼標之間的傳統鴻溝。供應商將 RFID嵌體嵌入壓敏卷材中,使物流用戶無需人工掃描即可追蹤小包裹,從而拓展了應用範圍。由此,永續性、裝飾性和合規性正在融合,推動著自動化貼標機市場的技術多元化發展。

預計從2026年到2031年,模組化和混合式系統將成長4.52%,超過2025年市佔率62.42%的線上旗艦機型。這些機架允許在通用底盤上安裝壓敏型、黏合劑或套筒型貼標頭,使代工包裝商能夠將投資分散到多個品牌和產品上。 KHS的「Innoket Neo Flex」面積減少了30%,並支援免工具換型,有助於提高中型乳製品生產商和啤酒廠的整體設備效率(OEE)。在大型工廠中,轉速超過600 BPM的旋轉伺服機仍然必不可少,但由於產品系列分散,批量縮小,運轉率可能會降低。在電子商務物流中心,「列印貼標」機正變得越來越受歡迎,因為不同尺寸的小包裹需要動態標籤尺寸和運輸資料。

訂閱模式的引入消除了初始成本的障礙,擴大了模組化自動化貼標機的市場。供應商透過物聯網診斷來確保運作,確保耗材的穩定收入來源,並避免了疫情期間因採購凍結而導致的資本投資停滯。因此,配置選擇如今已成為確保包裝生產線面向未來、適應產品種類波動的重要策略手段。

區域分析

預計到2025年,亞太地區將佔據自動化貼標機市場40.37%的佔有率,複合年成長率達4.78%。在中國,修訂後的《藥品管理法》擴大了藥品序列化範圍,將中藥納入其中,迫使數千家本土包裝企業採用視覺檢測模組和瑕疵產品剔除模組。印度的契約製造生產商正在投資建造高速生產線,以滿足符合美國FDA標準的出口規格,進一步鞏固其在該地區的生產規模優勢。在日本,擴大生產者責任制正在加速無底紙標籤的普及;而在韓國,電池供應鏈的可追溯性是符合歐盟法規的必要條件。

在北美,電子商務物流正推動自動化貼標機市場的發展,美國履約中心紛紛採用人工智慧視覺技術和列印貼標單元。即便飲料製造商延長了設備更換週期,這些措施也帶動了自動化貼標機的市場收入成長。製藥生產線持續推進設備升級,以滿足《藥品供應鏈安全法案》(DSCSA)2026年的最終目標,尤其是在合約研發生產機構(CDMO)中,冗餘和驗證至關重要。在歐洲,永續性和監管要求正在尋求平衡。德國、法國和義大利正在採用單一材料薄膜和模組化貼標頭,以履行2030年《包裝和包裝廢棄物法規》規定的回收義務。飲料製造商正從多材料套筒轉向可回收收縮膜,從而促進了中速貼標機的銷售。西班牙和波蘭的合約包裝公司正在租賃線上貼標機,為跨國品牌商提供服務,推動著市場緩慢但穩定的成長。

在南美洲,巴西飲料業和阿根廷藥品出口推動了設備安裝量的逐步成長,而外匯波動則刺激了租賃和二手設備的流通。在中東和非洲地區,沙烏地阿拉伯的學名藥生產和南非的食品出口是關注的焦點,在這些地區,具備視覺檢測功能的中階機型既滿足清真標籤要求,也滿足歐盟可追溯性要求。在哥倫比亞和智利,政府為安裝節能型貼標生產線的工廠提供稅收優惠,這鼓勵了猶豫不決的包裝公司重啟自動化計畫。在全部區域,提供遠端監控和訂閱服務相結合的供應商越來越受歡迎,因為這種方式可以幫助加工商避免外匯波動和意外維護成本的風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧包裝對可追溯性的需求日益成長

- 小批量精釀飲料(SKU)生產激增

- 電子商務履約中心的成長

- 加強藥品和醫療設備的序列化和UDI法規

- 整合按需數位印刷

- 永續發展驅動的無襯紙標籤轉型

- 市場限制因素

- 高資本支出(CAPEX)與租賃或合約式包裝方案的比較。

- 控制和維護領域工程師短缺

- 原料(標籤庫存)價格波動

- 多廠商產品之間的互通性差距

- 產業價值鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過技術

- 壓敏/不乾膠標籤機

- 收縮套標機

- 黏合劑式(冷膠、熱熔膠)標籤機

- 袖標機(拉伸,耐熱)

- 套模貼標機

- 其他技術

- 透過機器配置

- 線上貼標機

- 旋轉式/旋轉伺服式貼標機

- 列印和應用系統

- 模組化/混合系統

- 貼標速度

- 低於每分鐘 60 次

- 61~200 BPM

- 201~400 BPM

- 每分鐘400次或以上

- 最終用戶

- 食物

- 飲料

- 製藥

- 個人護理化妝品

- 化學和工業用途

- 物流與電子商務

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Krones AG

- Sidel Group(Tetra Laval)

- KHS GmbH

- SACMI Imola SC

- Accutek Packaging Company, Inc.

- ProMach Inc.

- HERMA GmbH

- Domino Printing Sciences PLC

- Fuji Seal International

- Avery Dennison Corporation

- Weber Packaging Solutions

- Markem-Imaje(Dover)

- Videojet Technologies

- PE Labellers SpA

- Nita Labeling Systems

- Quadrel Labeling Systems

- Pack Leader Machinery

- World Pack Automation Systems

- Arca Labeling and Marking

- Bobst Group SA

- Sato Holdings Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the automatic labeling machine market size is projected to expand from USD 3.15 billion in 2025 and USD 3.24 billion in 2026 to USD 3.84 billion by 2031, registering a CAGR of 3.51% between 2026 to 2031.

This report is Segmented by Technology (Pressure-Sensitive, Shrink-Sleeve, and More), Machine Configuration (In-Line, Rotary, Print-And-Apply, and Modular / Hybrid), Labelling Speed (Less Than 60 BPM, 61-200 BPM, 201-400 BPM, and More Than 400 BPM), End User (Beverages, Pharmaceuticals, Personal Care and Cosmetics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automatic Labeling Machine Market Trends and Insights

Stricter Serialization and UDI Rules in Pharma and Med-Device

Pharmaceutical and medical-device producers must imprint unique identifiers on every saleable unit, case, and pallet to comply with the U.S. DSCSA, Europe's Falsified Medicines Directive, and China's 2024 Drug Administration Law. Companies that once relied on standalone mechanical labelers are retrofitting lines with 2D DataMatrix printers, vision verification, and database connectivity that synchronize serial numbers in real time. Contract manufacturers are fast-tracking these upgrades to retain export certifications, diverting procurement budgets toward integrated print-and-apply modules rather than general packaging assets. The shift rewards suppliers certified under ISO 9001 and FDA 21 CFR Part 11 because they can furnish validation protocols required during regulatory audits.

Surge in Craft Beverage Short-Run SKUs

Craft brewers and artisanal distilleries now average 75 distinct SKUs per plant, compared with 20 just five years ago, a proliferation that makes pre-printed label inventories uneconomical. Modular automatic labeling machine platforms that combine inkjet or thermal transfer printing with pressure-sensitive application enable producers to switch graphics in minutes, squeezing obsolescence out of seasonal or collaboration runs. Solutions such as the SwiftColor SCC-4000D deliver full-color, variable-data labels at up to 60 ft/min, letting limited-edition beverages reach shelves within days of concept approval. This trend is spilling into specialty foods and direct-to-consumer cosmetics, broadening the revenue base for mid-speed, quick-change applicators.

High CAPEX Versus Rental or Contract Packaging Options

Cash-constrained food and personal-care brands increasingly rent equipment or outsource production, delaying outright purchases. ProMach noted a 35% jump in rental inquiries during 2024 as marketers funneled capital toward digital campaigns instead of machinery. Subscription models such as Domino's Labeling-as-a-Service bundle hardware, consumables, and remote monitoring into monthly fees, shifting risk from brand owners to suppliers. While these offerings expand access, they compress up-front revenues, tempering automatic labeling machine market growth in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-Commerce Fulfillment Centers

- Sustainability-Driven Shift to Linerless Labels

- Volatile Raw-Material (Label Stock) Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sleeve applicators expanded at a 4.24% CAGR between 2025 and 2031, the briskest pace among technologies in the automatic labeling machine market. Pressure-sensitive units still delivered 39.83% automatic labeling machine market share in 2025, favored for compliance text, variable data, and easy changeovers. Full-body shrink sleeves attract energy drink and ready-to-drink cocktail brands that seek tamper evidence and 360-degree graphics without bottle embossing. Stretch sleeves, promoted for mono-material recyclability, appeal to juice and dairy processors complying with European producer-responsibility rules. Although cold-glue stations dominate legacy beer lines for their low per-label cost, their rigid format lengthens downtime during SKU switches, nudging brewers toward modular sleeves or pressure-sensitive heads. Innovations such as servo-controlled seam overlap trimming reduce film waste by 15%, aligning cost and sustainability goals.

Print-on-demand integration is redefining technological boundaries. Domino's N610i inkjet head bolts onto existing pressure-sensitive applicators and supports 300 m/min variable-data streams, erasing the historical divide between printing and labeling. Suppliers embedding RFID inlays within pressure-sensitive webs let logistics users track parcels without manual scans, widening application breadth. Sustainability, decoration, and compliance thus coalesce to propel technology diversification within the automatic labeling machine market.

Modular and hybrid systems are projected to grow 4.52% from 2026-2031, outpacing in-line workhorses that owned 62.42% of market share in 2025. These frames accept pressure-sensitive, glue, or sleeve heads on a common chassis, allowing co-packers to amortize investment across multiple brands and products. KHS Innoket Neo Flex cuts footprint by 30% and delivers tool-free changeovers, translating into higher overall equipment effectiveness for midsized dairies and breweries. Rotary-servo machines exceeding 600 BPM remain indispensable in mega-plants but risk under-utilization as portfolio fragmentation shortens run lengths. Print-and-apply boxes proliferate in e-commerce distribution centers where variable-dimension parcels demand dynamic label sizing and shipping data.

The automatic labeling machine market size tied to modular systems is expanding as subscription pricing removes up-front barriers. Vendors guarantee uptime via IoT diagnostics, secure a consumable revenue stream, and sidestep procurement freezes that stalled capital expenditure during pandemic years. As a result, configuration choice is now a strategic lever that can future-proof packaging lines against SKU volatility.

Complete Report Scope:

- By Technology

- Pressure-Sensitive / Self-Adhesive Labelers

- Shrink-Sleeve Labelers

- Glue-Based (Cold Glue, Hot-Melt) Labelers

- Sleeve (Stretch, Heat) Labelers

- In-Mold Labelers

- Other Technologies

- By Machine Configuration

- In-Line Labeling Machines

- Rotary / Rotary-Servo Labelers

- Print-and-Apply Systems

- Modular / Hybrid Systems

- By Labelling Speed

- Less Than 60 BPM

- 61-200 BPM

- 201-400 BPM

- More Than 400 BPM

- By End User

- Food

- Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Chemicals and Industrial

- Logistics and E-Commerce

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific contributed 40.37% of automatic labeling machine market share in 2025 and is forecast to advance at 4.78% CAGR. China's amended Drug Administration Law extends serialization to traditional Chinese medicine, compelling thousands of regional packagers to add vision and reject modules. India's contract manufacturers invest in high-speed lines to meet FDA-aligned export specs, reinforcing the region's volume dominance. Japan's extended producer-responsibility rules accelerate linerless adoption, while South Korea's battery supply chain demands traceability for EU compliance.

North America capitalizes on e-commerce logistics, with U.S. fulfillment centers embedding AI vision and print-and-apply cells that uplift automatic labeling machine market revenue despite beverage producers stretching replacement cycles. Pharmaceutical lines meeting the final 2026 DSCSA milestone continue to drive U.S. upgrades, especially among contract development and manufacturing organizations that require redundant, validated equipment.Europe balances sustainability and regulation. Germany, France, and Italy adopt mono-material films and modular heads to meet the 2030 Packaging and Packaging Waste Regulation recycle mandate. Beverage firms transition from multi-material sleeves to recyclable shrink films, sustaining mid-speed system sales. Contract packers in Spain and Poland lease in-line units to service multinational brand owners, reinforcing modest but steady growth.

South America leverages Brazil's beverage sector and Argentina's pharma exports to support incremental installations, though currency volatility encourages rental or used-equipment channels. Middle East and Africa concentrate on Saudi localization of generics and South African food exports, where mid-range machines with vision inspection satisfy both halal labeling and EU traceability requirements. Government incentives in Colombia and Chile now provide tax abatements for plants that adopt energy-efficient labeling lines, nudging hesitant packagers to revive automation plans. Across these regions, suppliers that bundle remote monitoring with subscription pricing gain traction because the approach shields converters from foreign-exchange swings and unexpected maintenance expenses.

- Krones AG

- Sidel Group (Tetra Laval)

- KHS GmbH

- SACMI Imola SC

- Accutek Packaging Company, Inc.

- ProMach Inc.

- HERMA GmbH

- Domino Printing Sciences PLC

- Fuji Seal International

- Avery Dennison Corporation

- Weber Packaging Solutions

- Markem-Imaje (Dover)

- Videojet Technologies

- P.E. Labellers S.p.A.

- Nita Labeling Systems

- Quadrel Labeling Systems

- Pack Leader Machinery

- World Pack Automation Systems

- Arca Labeling and Marking

- Bobst Group SA

- Sato Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Smart Packaging Traceability

- 4.2.2 Surge in Craft Beverage Short-Run SKUs

- 4.2.3 Growth of E-Commerce Fulfillment Centers

- 4.2.4 Stricter Serialization and UDI Rules in Pharma and Med-Device

- 4.2.5 Digital Print-On-Demand Integration

- 4.2.6 Sustainability-Driven Shift to Linerless Labels

- 4.3 Market Restraints

- 4.3.1 High CAPEX Versus Rental or Contract Packaging Options

- 4.3.2 Skill Shortage in Controls and Maintenance

- 4.3.3 Volatile Raw-Material (Label Stock) Prices

- 4.3.4 Interoperability Gaps Across Multi-Vendor Lines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Pressure-Sensitive / Self-Adhesive Labelers

- 5.1.2 Shrink-Sleeve Labelers

- 5.1.3 Glue-Based (Cold Glue, Hot-Melt) Labelers

- 5.1.4 Sleeve (Stretch, Heat) Labelers

- 5.1.5 In-Mold Labelers

- 5.1.6 Other Technologies

- 5.2 By Machine Configuration

- 5.2.1 In-Line Labeling Machines

- 5.2.2 Rotary / Rotary-Servo Labelers

- 5.2.3 Print-and-Apply Systems

- 5.2.4 Modular / Hybrid Systems

- 5.3 By Labelling Speed

- 5.3.1 Less Than 60 BPM

- 5.3.2 61-200 BPM

- 5.3.3 201-400 BPM

- 5.3.4 More Than 400 BPM

- 5.4 By End User

- 5.4.1 Food

- 5.4.2 Beverages

- 5.4.3 Pharmaceuticals

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Chemicals and Industrial

- 5.4.6 Logistics and E-Commerce

- 5.4.7 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Krones AG

- 6.4.2 Sidel Group (Tetra Laval)

- 6.4.3 KHS GmbH

- 6.4.4 SACMI Imola SC

- 6.4.5 Accutek Packaging Company, Inc.

- 6.4.6 ProMach Inc.

- 6.4.7 HERMA GmbH

- 6.4.8 Domino Printing Sciences PLC

- 6.4.9 Fuji Seal International

- 6.4.10 Avery Dennison Corporation

- 6.4.11 Weber Packaging Solutions

- 6.4.12 Markem-Imaje (Dover)

- 6.4.13 Videojet Technologies

- 6.4.14 P.E. Labellers S.p.A.

- 6.4.15 Nita Labeling Systems

- 6.4.16 Quadrel Labeling Systems

- 6.4.17 Pack Leader Machinery

- 6.4.18 World Pack Automation Systems

- 6.4.19 Arca Labeling and Marking

- 6.4.20 Bobst Group SA

- 6.4.21 Sato Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

自動貼標機市場:2026-2032年全球市場預測(依機器類型、標籤材料、標籤類型、最終用途產業、標籤應用和銷售管道)

自動貼標機市場:2026-2032年全球市場預測(依機器類型、標籤材料、標籤類型、最終用途產業、標籤應用和銷售管道) 工業自動化貼標機市場預測至2034年-按類型、最終用戶和地區分類的全球分析高速醫藥旋轉貼標機市場:按技術、機器配置、驅動類型、速度範圍、整合度、應用、最終用戶和分銷管道分類的全球預測(2026-2032年)

工業自動化貼標機市場預測至2034年-按類型、最終用戶和地區分類的全球分析高速醫藥旋轉貼標機市場:按技術、機器配置、驅動類型、速度範圍、整合度、應用、最終用戶和分銷管道分類的全球預測(2026-2032年) 2026年全球自動貼標機市場報告注射器貼標機市場:按技術類型、按產品類型、按生產規模、按標籤類型、按標籤材料、按注射器類型、按最終用戶 - 2025-2030 年全球預測

2026年全球自動貼標機市場報告注射器貼標機市場:按技術類型、按產品類型、按生產規模、按標籤類型、按標籤材料、按注射器類型、按最終用戶 - 2025-2030 年全球預測 自動貼標機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

自動貼標機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測