|

市場調查報告書

商品編碼

2073519

智慧型手機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Smartphones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

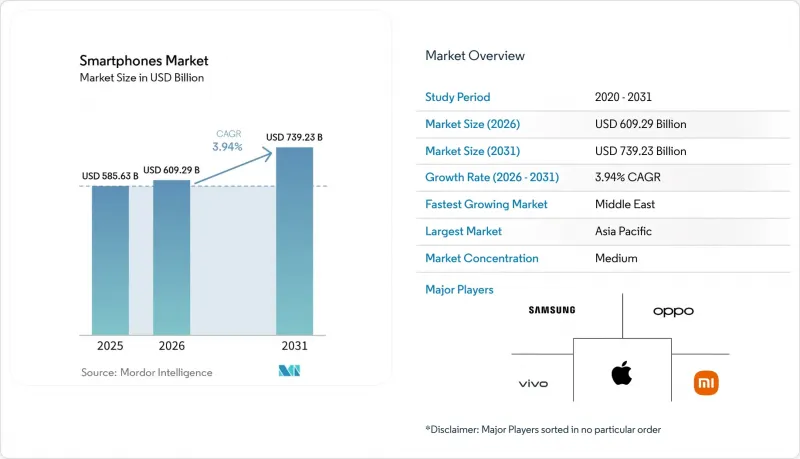

根據 Mordor Intelligence 預測,智慧型手機市場規模將從 2025 年的 5,856.3 億美元成長到 2026 年的 6,092.9 億美元,然後在 2031 年達到 7,392.3 億美元,2026 年至 2031 年的複合年成長率為 3.94%。

本報告按作業系統(Android、iOS 等)、價格區間(入門級、中階等)、技術(5G、4G/LTE 等)、外形規格(直板型、折疊式/翻蓋型等)、銷售管道(通訊業者門市、品牌門市等)、最終用戶(一般消費者/個人用戶等)和地區進行細分。市場預測以價值(美元)及銷售量(台)兩種單位呈現。

全球智慧型手機市場趨勢與洞察

人工智慧加速升級週期將促進更換。

目前,每秒鐘可執行超過40兆次運算的裝置端生成式人工智慧已成為新款旗艦機型的標配功能。蘋果的A18 Pro和高通的驍龍8 Elite都配備了神經網路引擎,能夠實現即時翻譯、影像合成和個人助理功能,且無需雲端延遲。在北美和歐洲,這項功能縮短了智慧型手機的更換週期。在2025年的一項調查中,38%的受訪用戶表示,人工智慧是更換的主要原因。高階用戶能夠實際感受到這些功能帶來的日常便利,例如即時會議摘要和設備內照片編輯,這促使他們願意為旗艦機型支付更高的價格。中國廠商也迅速做出反應。聯發科的天璣9400晶片將多模態助手的能源效率提升了30%,使人工智慧成為一項標準的跨平台功能。隨著晶片製造商不斷研發針對智慧型手機散熱設計最佳化的複雜晶片,這場技術競賽預計將持續到2029年。

優質化可享有融資、以舊換新和長期軟體支援。

憑藉免息分期付款計劃和極具吸引力的以舊換新優惠,消費者的關注點正從預付成本轉向降低月供。美國通訊業者目前已將付款期限延長至36個月,這意味著原本售價1,200美元的旗艦機型,每月付款只需33美元。同時,蘋果在2024年處理了超過1,200萬筆以舊換新交易,最高可享500美元的折扣。三星和Google提供的七年更新保障進一步降低了整體擁有成本,確保高階機型在正常換代週期之外仍能保持安全性和豐富的功能。這些機制共同作用,即使在宏觀經濟低迷時期,也維持了對高階智慧型手機的強勁需求,推動了收入流入更高平均售價(ASP)的區間。類似的趨勢也開始在新興市場出現,當地銀行和金融科技公司開始提供分期付款的設備貸款服務。

記憶體供應緊張推高了元件成本。

2024年下半年,由於晶圓產能轉向高頻寬伺服器模組,DRAM現貨價格上漲了約20%。三星和SK海力士優先滿足汽車和資料中心客戶的需求,導致行動裝置用LPDDR記憶體供不應求,迫使入門級安卓手機廠商降低記憶體配置。在價格敏感的市場中,10美元的漲幅促使消費者轉向4GB記憶體機型和功能手機,導致銷售預測下調。飆升的零件價格進一步擠壓了本已微薄的毛利率,迫使一些二線品牌推遲新品發布或減少配件數量。預計到2026年中期新晶圓廠全面運作之前,情況不會有所改善,智慧型手機市場低階產品的平均售價(ASP)將持續承壓,這可能會進一步加劇數位落差。

細分市場分析

預計到2025年,Android仍將維持69.21%的智慧型手機市場佔有率,但鴻蒙作業系統和KaiOS正以每年5.29%的速度成長,預示著市場將逐漸分散。華為在2024年出貨了超過7,000萬部搭載鴻蒙作業系統的智慧型手機,進一步鞏固了其以中國為中心的、獨立於Google服務的生態系統。 KaiOS主要應用於超低價設備,累計啟動量已超過1.5億,為初次接觸網際網路的用戶帶來了基於應用程式的體驗。儘管目前其他平台智慧型手機的市場規模仍然較小,但其成長動能正在挑戰Android在某些細分市場的絕對優勢。歐盟的《數位市場法案》和印度的互通性提案等監管趨勢,透過強制推行第三方應用商店和跨平台通訊,正在確保公平競爭。隨著合規成本的上升,iOS 和 Android 的市佔率可能會逐漸被那些承諾資料主權和卓越低階效能的地區性或應用性平台所取代。

同時,蘋果的iOS系統正日益增強其定價權。在面向超高階市場的「Pro」機型的推動下,iPhone在2024會計年度的銷售額達到了2,000億美元。蘋果對晶片、作業系統和服務進行垂直整合,打造了一致的用戶體驗,使其平均售價(ASP)達到1,100美元,從而有效抵禦了競爭。安卓廠商的應對策略包括承諾更快的系統更新和更嚴格的谷歌安全認證。在整個預測期內,智慧型手機市場的平台多元化將更多地受到區域法規、應用商店經濟模式和開發者獎勵的驅動,而非純粹的技術實力。

售價超過 800 美元的超高階智慧型手機市場預計到 2031 年將以 6.42% 的年均成長率成長,超過所有其他價格區間。 iPhone 16 Pro Max 和 Galaxy S25 Ultra 等旗艦機型憑藉著鈦金屬邊框、潛望式鏡頭和內建人工智慧等功能提升了消費者的感知價值。以舊換新折扣和營運商提供的分期付款計劃降低了實際購買門檻,吸引了許多渴望擁有高階手機的消費者。與此同時,售價低於 200 美元的入門級機型正面臨著不斷上漲的物料成本和來自翻新產品的競爭,進一步擠壓了本已微薄的利潤空間。

2025年,售價在200美元至499美元之間的中階機型將佔據大部分銷量,它們以實惠的價格提供5G連接、多感測器相機和快速充電功能。廠商正利用這個價格區間作為提升銷售方式,引導消費者向更高階的機種進軍。隨著消費者在「成本績效」和「旗艦體驗」之間搖擺不定,高階市場(500美元至799美元)正在萎縮。雖然中階中階智慧型手機市場預計將繼續成長,但銷售構成比將轉向超高階市場,該市場透過硬體升級可獲得極高的利潤率。

區域分析

亞太地區受中國龐大的用戶群體和印度製造業發展勢頭的推動,預計到2025年將佔全球銷售額的42.81%,並繼續保持主導地位。隨著中國半導體自主研發的步伐加快,例如華為Mate 60 Pro的問世,高階消費者正轉向本土品牌。同時,印度的生產連結獎勵計畫計畫(PLI)已累積吸引150億美元的行動電話投資,擴大了出口能力,並降低了全球平均售價(ASP)。

北美地區的手機升級速度依賴於通訊業者的融資方案,掩蓋了旗艦機型的實際價格。蘋果公司受惠於以舊換新優惠,預計到2025年將佔據美國高階市場一半以上的市佔率。同時,三星憑藉著獎勵,Galaxy S25的預購量較去年同期成長了15%。加拿大和墨西哥也出現了類似的趨勢,大都會圈對高階產品的需求與經濟低度開發地區中階產品的滲透率相平衡。

歐洲市場依然分散。德國和法國重視資料隱私保護,而英國則以通訊業者合約捆綁的無限資料通訊為主導。 《數位市場法案》有望改變應用商店的經濟結構,並為本地企業和替代支付系統創造新的機會。

南美市場的成長依賴巴西的在地化生產,聯想旗下的摩托羅拉憑藉著迎合當地消費者購買力的中階設備,在巴西市場佔據領先地位。儘管外匯波動影響定價,但主要城市的5G部署正在刺激更換需求。

中東地區以10.83%的複合年成長率領先預測成長。沙烏地阿拉伯和阿拉伯聯合大公國的高可支配收入,加上政府的數位化舉措,正在推動高階設備的銷售。通訊業者正在加速部署毫米波技術,支援需要旗艦智慧型手機的AR旅遊指南和企業物聯網先導計畫。

非洲市場對價格依然極為敏感,而傳音品牌憑藉其雙卡雙待和長續航能力,在市場上佔據主導地位。儘管奈及利亞和肯亞的5G頻段競標可能會逐步推動設備升級,但價格限制意味著入門級和翻新機在可預見的未來仍將佔據主導地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AI驅動的升級週期加快了更換(GenAI設備內建多模態助理)

- 透過融資、以舊換新和延長軟體支援來優質化。

- 新興市場入門級5G的採用

- 折疊式設備的成熟正在擴大高價值的細分市場。

- 成熟市場中主導的促銷活動和通訊業者分期付款計劃

- 透過獎勵,在各個地區(印度、越南、中東和非洲)進行在地化生產,從而降低成本並前置作業時間。

- 市場限制因素

- 內存供應緊張推高了零件成本,給低階安卓設備帶來了壓力。

- 二手和翻新智慧型手機的成長正在蠶食對新設備的需求。

- 耐用性和持續創新延長了產品更新周期。

- 地緣政治和關稅導致 SKU 變化,物流日益複雜化。

- 產業價值鏈分析

- 宏觀經濟影響分析

- 監理情勢

- 頻率分配和許可(2G/3G/4G/5G)

- 為 eSIM 實施做準備並利用物聯網設備

- 關於終端進口政策以及本地製造和組裝的規定

- 技術展望

- SoC藍圖(NPU TOPS、射頻整合、衛星NTN)

- 顯示堆疊(LTPO、微透鏡OLED、UDR玻璃、抗反射膜)

- 相機與運算攝影(潛望鏡、堆疊感光元件、影像訊號處理器、人工智慧融合)

- 電池與充電技術(矽負極、氮化鎵快速充電、電池管理系統安全)

- 連接技術(Wi-Fi 7、藍牙低功耗音訊、UWB、5G-Advanced)

- 智慧型手機設備生命週期分析

- 相關人員生命週期圖

- 相關人員對關鍵問題的分析

- 波特五力分析

第5章 市場規模與成長預測

- 整個市場的估算

- 總市值(以美元計)

- 市場總規模

- 透過作業系統

- Android

- iOS

- 其他(HarmonyOS、KaiOS)

- 按價格範圍

- 入門級(低於 200 美元)

- 中價位(200-499 美元)

- 高級版(500-799 美元)

- 超高階(800 美元或以上)

- 透過科技(透過網路產生)

- 5G

- 4G 或 LTE

- 3G及更早版本

- 按外形規格

- Bar

- 折疊式或翻蓋式

- 重型或工業

- 透過分銷管道

- 通訊業者經營的商店

- 品牌自有零售

- 多品牌實體零售店

- 線上直接面對消費者 (D2C)

- 最終用戶

- 消費者或個人

- 大型或小型企業

- 公共部門或政府

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞(新加坡、泰國、印尼、越南、菲律賓、馬來西亞)

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合作、關於在地化組裝的合作備忘錄)

- 市佔率分析

- 公司簡介

- Apple Inc.

- Samsung Electronics Co. Ltd

- Xiaomi Corporation

- OPPO(incl. OnePlus)

- Vivo Communication Technology Co., Ltd.

- Transsion Holdings Co., Ltd.(TECNO, Infinix, itel)

- Huawei Technologies Co., Ltd

- Honor Device Co., Ltd.

- Google LLC

- Motorola Mobility LLC(Lenovo Group Ltd)

- Realme Chongqing Mobile Telecommunications Corp., Ltd.

- HMD Global Oy(Nokia)

- Sony Corp.

- ASUSTeK Computer Inc.

- ZTE Corp.

- TCL Technology(Group)Co. Ltd(Alcatel)

- Nothing Technology Ltd

- Kyocera Corporation

- Sharp Corporation

- Fairphone BV

第7章 市場機會與未來展望

According to Mordor Intelligence, the smartphones market size is expected to grow from USD 585.63 billion in 2025 to USD 609.29 billion in 2026 and is forecast to reach USD 739.23 billion by 2031 at 3.94% CAGR over 2026-2031.

This report is Segmented by Operating System (Android, IOS, and More), Price Band (Entry-Level, Mid-Range and More), Technology (5G, 4G/LTE, and More), Form Factor (Bar, Foldable/Flip, and More), Distribution Channel (Operator/Carrier Stores, Brand-Owned Retail, and More), End-User (Consumer/Individual and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Smartphones Market Trends and Insights

AI-Enabled Upgrade Cycle Accelerates Replacements

On-device generative AI, now capable of more than 40 trillion operations per second, has become a headline feature in flagship launches. Apple's A18 Pro and Qualcomm's Snapdragon 8 Elite showcase neural engines that deliver real-time translation, image synthesis, and personal-assistant tasks without cloud latency. In North America and Europe, this capability shortened replacement cycles in the smartphones market, as 38% of surveyed users in 2025 cited AI as their primary upgrade trigger. Premium buyers perceive tangible day-to-day benefits, such as instant meeting summaries and on-device photo editing, which reinforce a willingness to pay flagship pricing. Chinese vendors are responding quickly: MediaTek's Dimensity 9400 delivers a 30% power-efficiency gain for multimodal assistants, making AI a cross-platform baseline. The arms race is likely to persist through 2029 as chipmakers chase ever-larger parameter models optimized for handset thermals.

Premiumization Sustained by Financing, Trade-Ins, and Extended Software Support

Zero-interest installment plans and aggressive trade-in credits are shifting consumer focus from upfront cost to monthly affordability. U.S. carriers now stretch payments over 36 months, effectively turning a USD 1,200 flagship into a USD 33 obligation, while Apple processed more than 12 million trade-ins in 2024 that shaved up to USD 500 off the sticker price. Seven-year update pledges from Samsung and Google further lower total cost of ownership, reassuring buyers that premium models will stay secure and current well past typical refresh cycles. Together, these mechanisms keep premium demand in the smartphones market resilient even during macro softness and funnel more revenue into higher ASP tiers. Emerging markets are beginning to mirror this behavior as local banks and fintechs roll out installment-based handset loans.

Memory Supply Tightness Lifts BoM Costs

DRAM spot prices climbed roughly 20% in late 2024 as wafer capacity was diverted to high-bandwidth server modules. Samsung and SK Hynix prioritized automotive and data-center customers, leaving mobile LPDDR shortfalls that forced entry-level Android vendors to dial back memory configurations. In price-sensitive markets, a USD 10 increase pushes buyers toward 4 GB variants or even feature phones, eroding volume forecasts. Component inflation also squeezes razor-thin gross margins, prompting some tier-two brands to postpone launches or bundle fewer accessories. Relief is unlikely before mid-2026 when new fabs ramp, keeping pressure on low-end ASPs across the smartphones market and potentially widening the digital divide.

Other drivers and restraints analyzed in the detailed report include:

- Entry-Level 5G Proliferation in Emerging Markets

- Foldable Maturation Expands High-Value Niches

- Used or Refurbished Smartphone Growth Cannibalizes New Device Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Android retained 69.21% smartphones market share in 2025, yet HarmonyOS and KaiOS are growing at 5.29% annually, signaling gradual fragmentation. Huawei shipped more than 70 million HarmonyOS phones in 2024, fortifying a China-centric ecosystem that operates without Google services. KaiOS, powering ultra-low-cost devices, surpassed 150 million cumulative activations, introducing first-time internet users to app-based experiences. The smartphones market size for alternative platforms remains small today, but their trajectory challenges Android's ubiquity in specific niches. Regulatory shifts, including the EU Digital Markets Act and India's interoperability proposals, level the playing field by mandating third-party app stores and cross-platform messaging. As compliance costs rise, both iOS and Android may concede incremental share to regional or purpose-built platforms that promise data sovereignty or superior low-end performance.

Apple's iOS meanwhile consolidates pricing power: fiscal 2024 iPhone revenue hit USD 200 billion, driven by Pro variants that anchor the ultra-premium tranche. Apple's vertical integration of silicon, operating system, and services delivers a cohesive experience that justifies a USD 1,100 ASP, insulating iOS from price-based competition. For Android vendors, strategic responses include faster update pledges and tighter Google security certifications. Over the forecast, platform diversification in the smartphones market will hinge on localized regulation, app-store economics, and developer incentives rather than pure technological capability.

Ultra-premium smartphones above USD 800 are projected to grow at 6.42% through 2031, outpacing every other tier. Flagships such as iPhone 16 Pro Max and Galaxy S25 Ultra integrate titanium frames, periscope lenses, and on-device AI that elevate perceived value. Trade-in credits and carrier financing reduce the effective purchase hurdle, drawing aspirational buyers into the segment. At the other extreme, entry-level models below USD 200 face BoM inflation and heightened competition from refurbished units, which narrows already thin margins.

Mid-range devices, priced USD 200-499, captured the bulk of 2025 revenue by offering 5G connectivity, multi-sensor cameras, and fast charging at palatable prices. Vendors use this band as a stepping stone, upselling via limited-time promotions or bundling accessories. Premium (USD 500-799) occupies a shrinking middle ground as consumers polarize toward either value or flagship experiences. The smartphones market size for mid-range will still expand, but the revenue mix will tilt toward ultra-premium where incremental hardware upgrades command outsized margins.

Complete Report Scope:

- Overall Market Estimates

- Total Market Value (USD)

- Total Market Volume (Units)

- By Operating System (Value, and Volume)

- Android

- iOS

- Others (HarmonyOS, KaiOS)

- By Price Band (Value, and Volume)

- Entry-Level (Less Than USD 200)

- Mid-Range (USD 200-499)

- Premium (USD 500-799)

- Ultra-Premium (More Than USD 800)

- By Technology (Network Generation) (Value)

- 5G

- 4G or LTE

- 3G and Below

- By Form Factor (Value)

- Bar

- Foldable or Flip

- Rugged or Industrial

- By Distribution Channel (Value)

- Operator or Carrier Stores

- Brand-Owned Retail

- Multi-Brand Physical Retail

- Online Direct-to-Consumer

- By End User (Value)

- Consumer or Individual

- Enterprise or SME

- Public Sector or Government

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Southeast Asia (Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia)

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of the Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia Pacific retained leadership with 42.81% of 2025 revenue, driven by China's vast installed base and India's manufacturing momentum. China's shift to domestically designed silicon, exemplified by Huawei's Mate 60 Pro, is steering premium buyers toward local brands, while India's Production-Linked Incentive scheme attracted USD 15 billion in cumulative handset investment, scaling export capacity and lowering global ASPs.

North America's upgrade cadence relies on carrier financing that conceals flagship prices. Apple captured over half of the U.S. premium segment in 2025, aided by trade-in credits, while Samsung boosted pre-orders 15% year-over-year with Galaxy S25 incentives. Canada and Mexico echo similar dynamics, balancing premium demand in metro areas with mid-range uptake in less affluent regions.

Europe's market remains fragmented: Germany and France highlight data-privacy features, whereas the United Kingdom leans on carrier deals that bundle unlimited data. The Digital Markets Act may reshape app-store economics, creating openings for regional players and alternative payment systems.

South America's growth hinges on Brazil's localized production, where Lenovo-owned Motorola commands share through mid-range devices adapted to local spending power. Currency volatility complicates pricing, yet 5G deployments in major cities stimulate replacement demand.

The Middle East leads forecast growth at a 10.83% CAGR. High disposable incomes in Saudi Arabia and the United Arab Emirates, coupled with government digitalization agendas, lift premium device sales. Operators accelerate mmWave rollouts, supporting AR tourism guides and enterprise IoT pilots that require flagship-grade smartphones.

Africa's market remains fiercely price sensitive, dominated by Transsion brands optimized for dual-SIM use and long battery life. 5G spectrum auctions in Nigeria and Kenya will spur gradual upgrades, but affordability constraints keep entry-level and refurbished devices prominent in the near term.

- Apple Inc.

- Samsung Electronics Co. Ltd

- Xiaomi Corporation

- OPPO (incl. OnePlus)

- Vivo Communication Technology Co., Ltd.

- Transsion Holdings Co., Ltd. (TECNO, Infinix, itel)

- Huawei Technologies Co., Ltd

- Honor Device Co., Ltd.

- Google LLC

- Motorola Mobility LLC (Lenovo Group Ltd)

- Realme Chongqing Mobile Telecommunications Corp., Ltd.

- HMD Global Oy (Nokia)

- Sony Corp.

- ASUSTeK Computer Inc.

- ZTE Corp.

- TCL Technology (Group) Co. Ltd (Alcatel)

- Nothing Technology Ltd

- Kyocera Corporation

- Sharp Corporation

- Fairphone B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Enabled Upgrade Cycle Accelerates Replacements (On-Device GenAI, Multimodal Assistants)

- 4.2.2 Premiumization Sustained by Financing, Trade-Ins, and Extended Software Support

- 4.2.3 Entry-Level 5G Proliferation in Emerging Markets

- 4.2.4 Foldable Maturation Expands High-Value Niches

- 4.2.5 Carrier-Led Promotions and Device Financing in Mature Markets

- 4.2.6 Regional Manufacturing Localization Incentives (India, Vietnam, Middle East, and Africa) Reduce Costs and Lead Times

- 4.3 Market Restraints

- 4.3.1 Memory Supply Tightness Lifts BoM Costs, Pressuring Low-End Android

- 4.3.2 Used or Refurbished Smartphone Growth Cannibalizes New Device Demand

- 4.3.3 Slower Refresh Cycles from Durability and Incremental Innovation

- 4.3.4 Geopolitics and Tariffs Shifting SKUs, Raising Logistics Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Macroeconomic Impact Analysis

- 4.6 Regulatory Landscape

- 4.6.1 Spectrum Allocation and Licensing (2G/3G/4G/5G)

- 4.6.2 eSIM Readiness and IoT Device Enablement

- 4.6.3 Device Import Policy and Local Manufacturing or Assembly Rules

- 4.7 Technological Outlook

- 4.7.1 SoC Roadmaps (NPU TOPS, RF Integration, Satellite NTN)

- 4.7.2 Display Stack (LTPO, Micro-Lens OLED, UDR Glass, Anti-Reflective Coatings)

- 4.7.3 Camera or Computational Photography (Periscope, Stacked Sensors, ISP or AI Fusion)

- 4.7.4 Battery or Charging (Silicon Anodes, GaN Fast Charge, BMS Safety)

- 4.7.5 Connectivity (Wi-Fi 7, Bluetooth LE Audio, UWB, 5G-Advanced)

- 4.8 Smartphone Device Lifecycle Analysis

- 4.8.1 Stakeholder Lifecycle Mapping

- 4.8.2 Key Pain-Point Analysis by Stakeholder

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Overall Market Estimates

- 5.1.1 Total Market Value (USD)

- 5.1.2 Total Market Volume (Units)

- 5.2 By Operating System (Value, and Volume)

- 5.2.1 Android

- 5.2.2 iOS

- 5.2.3 Others (HarmonyOS, KaiOS)

- 5.3 By Price Band (Value, and Volume)

- 5.3.1 Entry-Level (Less Than USD 200)

- 5.3.2 Mid-Range (USD 200-499)

- 5.3.3 Premium (USD 500-799)

- 5.3.4 Ultra-Premium (More Than USD 800)

- 5.4 By Technology (Network Generation) (Value)

- 5.4.1 5G

- 5.4.2 4G or LTE

- 5.4.3 3G and Below

- 5.5 By Form Factor (Value)

- 5.5.1 Bar

- 5.5.2 Foldable or Flip

- 5.5.3 Rugged or Industrial

- 5.6 By Distribution Channel (Value)

- 5.6.1 Operator or Carrier Stores

- 5.6.2 Brand-Owned Retail

- 5.6.3 Multi-Brand Physical Retail

- 5.6.4 Online Direct-to-Consumer

- 5.7 By End User (Value)

- 5.7.1 Consumer or Individual

- 5.7.2 Enterprise or SME

- 5.7.3 Public Sector or Government

- 5.8 By Geography (Value)

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Chile

- 5.8.2.4 Colombia

- 5.8.2.5 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 France

- 5.8.3.3 United Kingdom

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 India

- 5.8.4.3 Japan

- 5.8.4.4 South Korea

- 5.8.4.5 Southeast Asia (Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia)

- 5.8.4.6 Australia

- 5.8.4.7 Rest of Asia-Pacific

- 5.8.5 Middle East

- 5.8.5.1 Saudi Arabia

- 5.8.5.2 United Arab Emirates

- 5.8.5.3 Rest of the Middle East

- 5.8.6 Africa

- 5.8.6.1 South Africa

- 5.8.6.2 Nigeria

- 5.8.6.3 Rest of Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, Local Assembly MoUs)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd

- 6.4.3 Xiaomi Corporation

- 6.4.4 OPPO (incl. OnePlus)

- 6.4.5 Vivo Communication Technology Co., Ltd.

- 6.4.6 Transsion Holdings Co., Ltd. (TECNO, Infinix, itel)

- 6.4.7 Huawei Technologies Co., Ltd

- 6.4.8 Honor Device Co., Ltd.

- 6.4.9 Google LLC

- 6.4.10 Motorola Mobility LLC (Lenovo Group Ltd)

- 6.4.11 Realme Chongqing Mobile Telecommunications Corp., Ltd.

- 6.4.12 HMD Global Oy (Nokia)

- 6.4.13 Sony Corp.

- 6.4.14 ASUSTeK Computer Inc.

- 6.4.15 ZTE Corp.

- 6.4.16 TCL Technology (Group) Co. Ltd (Alcatel)

- 6.4.17 Nothing Technology Ltd

- 6.4.18 Kyocera Corporation

- 6.4.19 Sharp Corporation

- 6.4.20 Fairphone B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球功能手機市場報告

2026年全球功能手機市場報告 智慧型手機市場:市場規模、佔有率和趨勢分析(按作業系統、分銷管道、價格範圍和地區分類),細分市場預測(2026-2033 年)

智慧型手機市場:市場規模、佔有率和趨勢分析(按作業系統、分銷管道、價格範圍和地區分類),細分市場預測(2026-2033 年) 智慧型手機市場:按組件、作業系統、儲存容量、顯示器類型、顯示器尺寸、記憶體容量和銷售管道分類——2026-2032年全球市場預測平板手機與超級手機市場:2026-2032年全球市場預測(依作業系統、螢幕大小、最終用戶及銷售管道)2026年全球平板手機市場報告2026年全球智慧型功能手機市場報告

智慧型手機市場:按組件、作業系統、儲存容量、顯示器類型、顯示器尺寸、記憶體容量和銷售管道分類——2026-2032年全球市場預測平板手機與超級手機市場:2026-2032年全球市場預測(依作業系統、螢幕大小、最終用戶及銷售管道)2026年全球平板手機市場報告2026年全球智慧型功能手機市場報告 智慧型手機市場報告:按作業系統、顯示技術、記憶體容量、價格範圍、銷售管道和地區分類(2026-2034 年)

智慧型手機市場報告:按作業系統、顯示技術、記憶體容量、價格範圍、銷售管道和地區分類(2026-2034 年) 智慧型手機市場:按作業系統、通路和地區分類

智慧型手機市場:按作業系統、通路和地區分類 智慧型手機市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,以及2026-2034年的預測2026年智慧型手機射頻前端(RFFE)全球市場報告

智慧型手機市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,以及2026-2034年的預測2026年智慧型手機射頻前端(RFFE)全球市場報告