|

市場調查報告書

商品編碼

2073481

國防領域衛星通訊市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)。Satellite Communication In The Defense Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

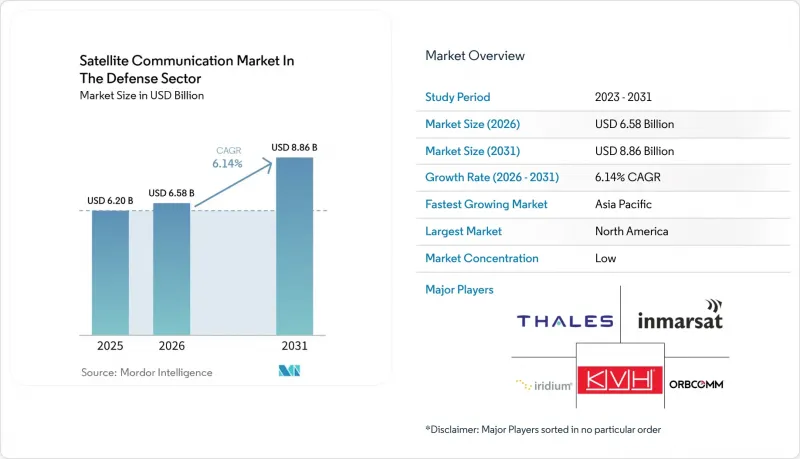

根據 Mordor Intelligence 預測,國防領域的衛星通訊市場規模預計將從 2025 年的 62 億美元成長到 2026 年的 65.8 億美元,然後從 2026 年到 2031 年以 6.14% 的複合年成長率成長,到 2031 年達到 88.6 億美元。

本報告按類型(地面設備、服務)、平台(陸軍、海軍、飛機)、頻段(L波段、S波段、C波段、 X波段Ku波段、Ka波段波段、Q/V波段、光纖通訊)、應用(C3、ISR、遙感探測、災害救援、電子情報/訊號情報)和地區進行細分。市場預測以美元計價。

國防領域衛星通訊市場的趨勢與發展

網路中心戰中對即時數據鏈路的需求日益成長。

以網路為中心的作戰行動依賴不間斷、低延遲的連接,但傳統的地球靜止軌道架構難以在前線戰術層面滿足這項要求。美國國防部已撥款2.48億美元用於開發抗干擾衛星星系,該星座將連接低軌道、中軌道和地球靜止軌道資產,以消除單點故障。 ThinKom公司的Ka2517等多軌道終端已展示了在SES公司的O3b mPOWER中地球軌道(MEO)網路和地球靜止軌道(GEO)疊加網路之間動態漫遊的能力,即使在蓄意干擾下也能保持通訊鏈路。烏克蘭的實戰經驗再次印證了商業通訊能力在軍事閘道器備份方面的重要性,並促使作戰條令更新,將商業衛星通訊(SATCOM)視為“前線資產”,而非“最後的冗餘手段”。軟體定義無線電(SDR)現在整合了自適應零陷功能,使部隊即使在干擾激增的情況下也能切換到干擾較小的頻道。此外,衛星群級路由演算法能夠分散流量負載並維持延遲限制。隨著感測器融合技術在各個平台上的普及,營運商越來越傾向於採用「即服務」模式,這種模式能夠在不強制硬體升級的情況下保證頻寬彈性。

無人系統的激增需要安全的衛星通訊。

無人機、艦艇和地面機器人的使用推動了戰場上對超視距(BVLOS)可靠通訊鏈路的需求。 L3Harris 的 Hawkeye III Lite VSAT 就是一個典型的例子,它是一款新型的堅固耐用型終端,能夠在幾分鐘內自動追蹤多條軌跡,即使在移動過程中也能保持高解析度視訊串流。人工智慧有效載荷帶來的資料量激增,使得採用高頻率的Ka波段和雷射交聯來最大限度地減少延遲成為必要。 Orbit Communication Systems 的超薄 MPT 天線提供符合進階資訊保障標準的加密,同時整合慣性導航系統以增強平台機動性。由於不安全的通訊鏈路可能導致車輛劫持,軍方採購負責人強烈要求即使在臨時租賃協議中也採用跳頻和抗量子加密層。商業營運商正在透過制定新的「政府計畫」來應對這一需求,這些計畫旨在保護頻段、增強網路安全並包含優先恢復條款。

衛星通訊網路易受網路入侵破壞的漏洞

電子戰領域敵方的技術進步正在暴露衛星傳輸通道和標準化協議的可預測性。 GPS欺騙案例表明,即使是低功率發送器也能癱瘓物流樞紐,而專為民用運作而設計的商用閘道器很少能達到軍用等級的穩健性標準。 5G非地面網路標準的整合擴大了覆蓋範圍,但也擴大了攻擊面,使駭客能夠利用跨域協定握手漏洞。因此,世界各國國防部正加速採用頻譜技術、抗截獲波形和抗量子加密金鑰。這些措施增加了終端的複雜性和成本,可能會延緩老舊設備的現代化。

細分市場分析

到2025年,地面設備在國防領域的衛星通訊市場仍佔60.70%的佔有率。這得歸功於自2000年代初以來部署的大量固定和移動天線、數據機和收發器。目前,終端升級的重點是電子控制相控相位陣列,這種天線可以縮小面積並實現多軌道漫遊。軟體定義調變解調器能夠動態切換波形,即使在競爭頻段也能保持連線。同時,基於門戶的管理套件使指揮官能夠全面了解整個衛星群的連結狀態。

同時,服務領域預計將以7.03%的複合年成長率實現最高成長,這主要得益於從硬體所有權向容量訂閱的轉變。北約與SES簽訂的價值2億歐元的O3b mPOWER頻寬管理服務契約,就體現了對可擴展吞吐量且無需新建地面基礎設施的需求。在這種模式下,供應商承擔衛星折舊免稅額、過時風險和發射延遲等風險,使軍方能夠將資金重新分配到用戶設備和網路防禦方面。生命週期分析表明,當衛星群更換週期小於10年時,服務模式可以降低總擁有成本(TCO),而許多低地球軌道(LEO)系統目前正接近這個閾值。

在2025年的國防衛星通訊市場中,陸基平台將佔據主導地位,市佔率高達38.10%。這反映了數十年來對車載系統和固定指揮所的持續投入。然而,機載系統正以6.74%的複合年成長率引領成長,這主要得益於中高度無人機和旋翼式情報、監視與偵察(ISR)飛機的日益普及。 L3Harris的混合無線電將衛星通訊、視距內通訊和蜂窩通訊整合於單一機殼內,在確保冗餘性的同時,簡化了飛機整合。

飛機通訊領域的成長也得益於有人駕駛飛機現代化改造項目,這些項目以更輕的Ka波段或雙波段孔徑天線取代傳統的Ku波段天線罩,以適應即時感測器資料流。如今,用於醫療運輸和VIP任務的客運機隊需要與商用飛機機上網路連接相當的加密寬頻,而像Gogo Business Aviation這樣的整合商正在努力將GEO-LEO-ATG混合網路適配到軍用規格。隨著分散式作戰理論下飛行架次的增加,頻寬彈性至關重要,而託管服務正成為標準的部署方式。

區域分析

預計到2025年,北美將佔全球收入的40.80%,這主要得益於美國優先發展多層韌性的現代化項目,以及加拿大對「五眼聯盟」的承諾——該聯盟要求建立可互通的閘道器。美國太空軍的商業增強太空儲備模式正式定義了危機期間獲取商業容量的途徑,並納入了服務等級協定(SLA),以確保頻寬激增回應和網路安全優先權。憑藉強大的工業基礎,該地區能夠確保終端的快速部署和安全的波形認證,並在雷射交聯和抗量子加密技術的應用方面處於領先地位。

亞太地區預計將以7.78%的複合年成長率實現最高成長,主要得益於中國北斗系統的擴建、印度的通用衛星通訊(SATCOM)藍圖以及日本內閣已通過核准的X波段升級。主權方面的考量推動了國內計畫的資金投入,而四國間的聯合演習則促進了互通性標準的建立。澳洲的遠程打擊和海上巡邏平台依賴跨越廣闊海洋的衛星回程傳輸,從而對地球-中地球-低地球混合衛星產生了穩定的需求。韓國的「千兆衛星計畫」(Kilo Satellite Project)進一步增強了該地區的市場深度。該計畫旨在2020年代末將40多顆微型衛星聯網,以實現影像中繼和安全通訊。

在歐洲,為因應日益緊張的安全局勢,相關支出正在加速成長。德國的「SATCOMBw 第三階段」計畫正在推動歐洲大陸自主能力的轉型,法國的「錫拉丘茲四號」和英國的「天網六號」計畫與之相輔相成,這兩項計畫都強調Ka波段吞吐量和電子防護。歐盟的「IRIS2」框架旨在將私人和政府需求整合到一個單一的採購管道,但成員國仍在就其對管治和出口管制的影響進行辯論。 SES收購IntelSat後,將地球同步軌道(GEO)和中地球軌道(MEO)衛星星座納入單一的歐洲組織,但各國正在對該公司過去的合資企業進行審查,以確保其技術主權。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 網路中心戰中對即時數據鏈路的需求日益成長。

- 需要安全衛星通訊的無人系統的激增。

- 快速部署容錯小型衛星星系

- 增加國防預算用於衛星通訊現代化建設

- 引入星間雷射通訊技術以緩解射頻擁塞。

- 將5G-NTN標準整合到軍用衛星通訊中

- 市場限制因素

- 衛星通訊網路易受網路入侵破壞的漏洞

- 下一代衛星通訊基礎設施需要大量的資本投資和啟動成本。

- 由於軌道碎片減少,衛星群規模受到限制

- 與5G地面電波網路共用射頻頻段的衝突

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟影響評估

- 波特五力分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 地面設備

- 天線

- 數據機和收發器

- 終端機(背負式、手提式、車載式)

- 服務

- 託管衛星通訊服務

- 租賃、整合、維護

- 地面設備

- 按平台

- 地面部隊

- 海軍

- 飛機(有人駕駛/無人駕駛)

- 按頻段

- L波段

- S波段

- C波段

- X波段

- Ku波段

- Ka波段

- Q/V 和光纖通訊(雷射)

- 透過使用

- 指揮、控制和通訊(C3)

- 情報與監視偵察(ISR)

- 遙感探測與地球觀測

- 災害救援和人道援助活動

- 電子情報(ELINT/SIGINT)

- 地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 土耳其

- 以色列

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措和趨勢

- 市佔率分析

- 公司簡介

- Thales Group

- Airbus Defence and Space

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- L3Harris Technologies Inc.

- Inmarsat Communications

- ViaSat Inc.

- Iridium Communications Inc.

- SES Government Solutions

- Cobham PLC

- ST Engineering iDirect

- Hughes Network Systems(EchoStar)

- Eutelsat Communications SA

- OneWeb Ltd.

- KVH Industries Inc.

- ORBCOMM Inc.

- Thuraya(Yahsat)

- General Dynamics Mission Systems

- Gilat Satellite Networks

第7章 市場機會與未來展望

According to Mordor Intelligence, the satellite communication market size In The Defense Sector market is expected to grow from USD 6.20 billion in 2025 to USD 6.58 billion in 2026 and is forecast to reach USD 8.86 billion by 2031 at 6.14% CAGR over 2026-2031.

This report is Segmented by Type (Ground Equipment, Services), Platform (Land Forces, Naval Forces, Airborne), Frequency Band (L-Band, S-Band, C-Band, X-Band, Ku-Band, Ka-Band, Q/V and Optical), Application (C3, ISR, Remote Sensing, Disaster Relief, ELINT/SIGINT), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Satellite Communication Market In The Defense Sector

Growing Demand for Real-Time Data Links for Network-Centric Warfare

Net-centric operations hinge on uninterrupted, low-latency connectivity, a requirement that legacy geostationary architectures struggle to satisfy at the tactical edge. The Pentagon has allocated USD 248 million to develop jam-resistant constellations that mesh low-, medium- and geostationary-orbit assets, eliminating single points of failure. Multi-orbit terminals such as ThinKom's Ka2517 already demonstrate dynamic roaming across SES's O3b mPOWER MEO network and GEO overlays, sustaining links even under deliberate interference. Combat experience in Ukraine reinforced the value of commercial capacity backstopping military gateways, prompting doctrine updates that treat commercial SATCOM as a first-line asset rather than last-resort redundancy. Software-defined radios now integrate adaptive nulling so forces can pivot to cleaner channels when jamming spikes, and constellation-level routing algorithms balance traffic loads to maintain latency ceilings. As sensor fusion proliferates across platforms, operators gravitate toward as-a-service contracts that guarantee bandwidth elasticity without forcing hardware refresh.

Proliferation of Unmanned Systems Requiring Secure SATCOM

Unmanned aircraft, maritime vessels and ground robots are escalating theater demand for assured beyond-visual-line-of-sight links. L3Harris's Hawkeye III Lite VSAT exemplifies the new breed of rugged terminals that auto-acquire multiple orbits in minutes and sustain high-definition video streams under movement. Artificial-intelligence-enabled payloads multiply data volumes, compelling adoption of higher-frequency Ka-band and laser cross-links to contain latency. Orbit Communication Systems' low-profile MPT antennas integrate inertial navigation units for platform agility while offering encryption compliant with advanced information assurance standards. Because unsecured links translate into commandeered vehicles, military buyers insist on frequency-hopping, quantum-resistant encryption layers even for interim leases. Commercial operators have responded by carving out government tiers that reserve spectrum, harden cybersecurity and furnish priority restoration clauses.

Cyber-Intrusion and Jamming Vulnerabilities of SATCOM Networks

Adversarial advances in electronic warfare expose predictable satellite passes and standardized protocols. Incidents of GPS spoofing illustrate how even modest power transmitters can paralyze logistics nodes, while commercial gateways built for civilian uptime rarely meet military hardening thresholds. Integration of 5G-non-terrestrial-network standards, though expanding coverage, widens the attack surface as hackers exploit cross-domain protocol handshakes. Defense ministries therefore accelerate fielding of spread-spectrum, low-probability-of-intercept waveforms and quantum-safe encryption keys. These countermeasures elevate terminal complexity and price, potentially delaying replacement of legacy assets.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Deployment of Resilient Small-Satellite Constellations

- Rising Defense Budgets Allocated to SATCOM Modernization

- High Capital and Launch Costs of Next-Gen SATCOM Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ground equipment retained 60.70% share of the satellite communication market in the defense sector in 2025, underpinned by the vast inventory of fixed and mobile antennas, modems and transceivers fielded since the early 2000s. Terminal upgrades now center on electronically steered phased arrays that shrink footprint and enable multi-orbit roaming. Software-defined modems execute on-the-fly waveform shifts to maintain connectivity in contested bands, while portal-based management suites give commanders visibility into link health across fleets.

Services, however, are projected to register the strongest 7.03% CAGR, validating the shift from hardware ownership to capacity subscription. NATO's EUR 200 million contract with SES for managed O3b mPOWER bandwidth epitomizes demand for scalable throughput without new ground footprint. Under these constructs, vendors absorb satellite depreciation, obsolescence risk and launch delays, allowing militaries to redirect capital toward user equipment and cyber defense. Lifecycle analytics also reveal that service models cut total cost of ownership when constellation refresh periods fall below 10 years, a threshold many LEO-based systems now approach.

Land platforms dominated the satellite communication market size in the defense sector in 2025 with 38.10% share, reflecting decades of investment in vehicle-mounted systems and fixed command posts. Yet the airborne category leads growth at 6.74% CAGR, propelled by expanded use of medium-altitude long-endurance drones and rotary-wing ISR aircraft. L3Harris hybrid radios combine SATCOM, line-of-sight and cellular links inside a single enclosure, simplifying aircraft integration while ensuring redundancy.

Airborne growth also stems from manned aircraft modernization programs that replace legacy Ku-band radomes with lighter Ka-band or dual-band apertures to support real-time sensor streaming. Passenger-transport fleets assigned to medical evacuation or VIP missions now demand encrypted broadband comparable to commercial inflight connectivity, prompting integrators such as Gogo Business Aviation to adapt GEO-LEO-ATG hybrids for militarized configurations. As sortie rates intensify under distributed-operations doctrine, bandwidth elasticity becomes indispensable, positioning managed services as the default acquisition route.

Complete Report Scope:

- By Type

- Ground Equipment

- Antennas

- Modems and Transceivers

- Terminals (Manpack, Fly-Away, Vehicular)

- Services

- Managed SATCOM Services

- Leasing, Integration and Maintenance

- Ground Equipment

- By Platform

- Land Forces

- Naval Forces

- Airborne (Manned and Unmanned)

- By Frequency Band

- L-band

- S-band

- C-band

- X-band

- Ku-band

- Ka-band

- Q/V and Optical (Laser)

- By Application

- Command, Control and Communications (C3)

- Intelligence, Surveillance and Reconnaissance (ISR)

- Remote Sensing and Earth Observation

- Disaster Relief and Humanitarian Ops

- Electronic Intelligence (ELINT and SIGINT)

- Geography

- North America

- United States

- Canada

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Turkey

- Israel

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

North America held 40.80% of 2025 revenue, anchored by U.S. modernization programs that prioritize layered resilience and by Canada's Five Eyes commitments that require interoperable gateways. The U.S. Space Force's Commercial Augmentation Space Reserve model formalizes access to commercial capacity during crises, embedding service-level agreements that guarantee surge bandwidth and cyber priority. Industrial-base depth ensures rapid terminal fielding and secure waveform certification, enabling the region to spearhead adoption of laser cross-links and quantum-safe encryption.

Asia-Pacific is projected to record the fastest 7.78% CAGR, catalyzed by China's BeiDou expansion, India's tri-service SATCOM roadmap and Japan's Cabinet-approved X-band upgrades. Sovereignty concerns drive indigenous program funding while quad-nation exercises push interoperability standards. Australia's long-range strike and maritime patrol platforms rely on satellite backhauls that traverse vast oceanic gaps, creating steady demand for GEO-MEO-LEO hybrids. Regional market depth is further reinforced by South Korea's kilo-satellite plan, which aims to network 40-plus microsats for imagery relay and secure communications by the end of the decade.

Europe accelerates its spend in the wake of heightened security tensions. Germany's SATCOMBw Stage 3 anchors a continental shift toward sovereign capability, complemented by France's Syracuse IV and the UK's Skynet 6, both of which emphasize Ka-band throughput and electronic protection. The European Union's IRIS2 framework seeks to federate commercial and governmental demand into a single procurement vehicle, though member states debate governance and export-control implications. SES's acquisition of Intelsat consolidates GEO and MEO fleets under one European roof, but national security reviews scrutinize the company's historical joint ventures to ensure technology sovereignty.

- Thales Group

- Airbus Defence and Space

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- L3Harris Technologies Inc.

- Inmarsat Communications

- ViaSat Inc.

- Iridium Communications Inc.

- SES Government Solutions

- Cobham PLC

- ST Engineering iDirect

- Hughes Network Systems (EchoStar)

- Eutelsat Communications SA

- OneWeb Ltd.

- KVH Industries Inc.

- ORBCOMM Inc.

- Thuraya (Yahsat)

- General Dynamics Mission Systems

- Gilat Satellite Networks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for real-time data links for network-centric warfare

- 4.2.2 Proliferation of unmanned systems requiring secure SATCOM

- 4.2.3 Rapid deployment of resilient small-satellite constellations

- 4.2.4 Rising defense budgets allocated to SATCOM modernisation

- 4.2.5 Adoption of laser inter-satellite links to ease RF congestion

- 4.2.6 Integration of 5G-NTN standards into military SATCOM

- 4.3 Market Restraints

- 4.3.1 Cyber-intrusion and jamming vulnerabilities of SATCOM networks

- 4.3.2 High capital and launch costs of next-gen SATCOM infrastructure

- 4.3.3 Orbital-debris mitigation constraints on constellation size

- 4.3.4 RF-spectrum sharing conflict with 5G terrestrial networks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Macroeconomic Impact Assessment

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Ground Equipment

- 5.1.1.1 Antennas

- 5.1.1.2 Modems and Transceivers

- 5.1.1.3 Terminals (Manpack, Fly-Away, Vehicular)

- 5.1.2 Services

- 5.1.2.1 Managed SATCOM Services

- 5.1.2.2 Leasing, Integration and Maintenance

- 5.1.1 Ground Equipment

- 5.2 By Platform

- 5.2.1 Land Forces

- 5.2.2 Naval Forces

- 5.2.3 Airborne (Manned and Unmanned)

- 5.3 By Frequency Band

- 5.3.1 L-band

- 5.3.2 S-band

- 5.3.3 C-band

- 5.3.4 X-band

- 5.3.5 Ku-band

- 5.3.6 Ka-band

- 5.3.7 Q/V and Optical (Laser)

- 5.4 By Application

- 5.4.1 Command, Control and Communications (C3)

- 5.4.2 Intelligence, Surveillance and Reconnaissance (ISR)

- 5.4.3 Remote Sensing and Earth Observation

- 5.4.4 Disaster Relief and Humanitarian Ops

- 5.4.5 Electronic Intelligence (ELINT and SIGINT)

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 Turkey

- 5.5.5.3 Israel

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thales Group

- 6.4.2 Airbus Defence and Space

- 6.4.3 Lockheed Martin Corp.

- 6.4.4 Northrop Grumman Corp.

- 6.4.5 L3Harris Technologies Inc.

- 6.4.6 Inmarsat Communications

- 6.4.7 ViaSat Inc.

- 6.4.8 Iridium Communications Inc.

- 6.4.9 SES Government Solutions

- 6.4.10 Cobham PLC

- 6.4.11 ST Engineering iDirect

- 6.4.12 Hughes Network Systems (EchoStar)

- 6.4.13 Eutelsat Communications SA

- 6.4.14 OneWeb Ltd.

- 6.4.15 KVH Industries Inc.

- 6.4.16 ORBCOMM Inc.

- 6.4.17 Thuraya (Yahsat)

- 6.4.18 General Dynamics Mission Systems

- 6.4.19 Gilat Satellite Networks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球核心衛星網路市場報告

2026年全球核心衛星網路市場報告 軟體定義衛星市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

軟體定義衛星市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 全球衛星通訊市場:2026-2036年

全球衛星通訊市場:2026-2036年 衛星通訊及通訊整合市場預測至2034年-全球組件、網路架構、軌道類型、頻段、應用、最終用戶及區域分析

衛星通訊及通訊整合市場預測至2034年-全球組件、網路架構、軌道類型、頻段、應用、最終用戶及區域分析 衛星通訊市場:按組件、軌道類型、技術、頻段、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測衛星通訊網路市場預測至2034年-按軌道類型、頻段、組件、應用、最終用戶和地區分類的全球分析

衛星通訊市場:按組件、軌道類型、技術、頻段、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測衛星通訊網路市場預測至2034年-按軌道類型、頻段、組件、應用、最終用戶和地區分類的全球分析 高通量衛星市場報告:按類型、應用和地區分類(2026-2034 年)衛星通訊:寬頻用戶和終端 - 市場數據概覽(2026 年第一季)衛星通訊:寬頻訂閱和終端衛星通訊:政府部門的寬頻訂閱和終端

高通量衛星市場報告:按類型、應用和地區分類(2026-2034 年)衛星通訊:寬頻用戶和終端 - 市場數據概覽(2026 年第一季)衛星通訊:寬頻訂閱和終端衛星通訊:政府部門的寬頻訂閱和終端