|

市場調查報告書

商品編碼

2073479

低調添加劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Low Profile Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

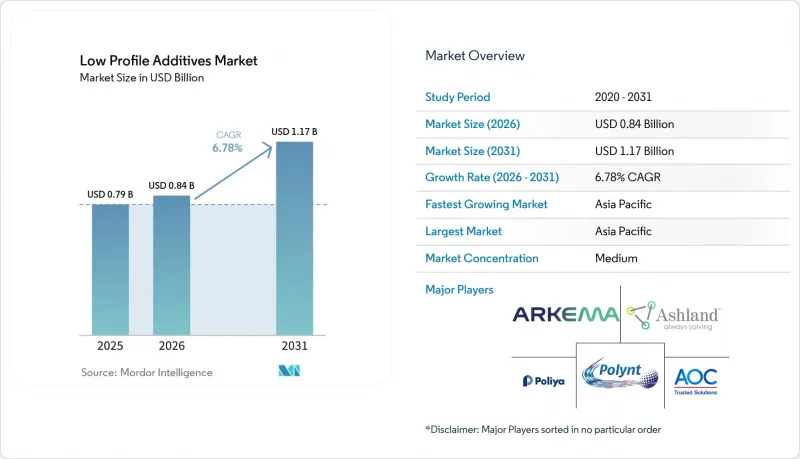

據 Mordor Intelligence 稱,低調添加劑的市場規模預計在 2026 年達到 8.4 億美元,高於 2025 年的 7.9 億美元,預計到 2031 年將達到 11.7 億美元。

預計 2026 年至 2031 年的複合年成長率為 6.78%。

本報告按產品類型(聚苯乙烯基、聚醋酸乙烯酯基及其他)、應用(射出成型/壓縮成型、Plutonion成型及其他)、終端用戶行業(汽車/交通運輸、建築/施工及其他)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球低調添加劑市場趨勢及洞察

汽車產業對高性能SMC複合材料的需求不斷成長

汽車製造商正在拓展SMC(片狀模塑膠)的應用範圍,用於模製電池外殼、車身面板和結構嵌件,這些部件都需要達到完美的A級表面光潔度。低收縮率添加劑能夠抑制體積收縮,並確保在熱循環下的尺寸穩定性。陶氏化學的聚氨酯碳纖維頂蓋固化效率超過90%,充分展現了新一代添加劑如何協助高速壓平機成型。隨著汽車平臺尺寸的增大和零件厚度的增加,控制收縮率的需求變得愈發關鍵,這使得超低收縮率添加劑在快速發展的亞太地區電動車(EV)中心至關重要。

對輕量化電動車的需求日益成長

歐盟的二氧化碳排放法規和中國的新能源汽車配額制度正在推動纖維增強塑膠的快速應用。低黏度添加劑能夠防止複合材料下陷和翹曲,即使在多材料組合中也能發揮作用。維吉尼亞大學的一項研究發現,石墨烯改質水泥複合材料的重量減輕了31%,這表明在汽車結構中實現類似減重的潛力。人們對更長電池續航里程的日益成長的期望預計將繼續推動對輕質複合材料的需求,並進而帶動對添加劑的需求。

含交聯苯乙烯單體的不飽和聚酯樹脂的高聚合收縮率

UPR-苯乙烯樹脂在固化過程中會發生固有的收縮,導致出現空隙和透印(即底層表面顯露出來),必須透過添加低黏度添加劑來抑制這種現象。供應商正在測試活性稀釋劑並改善交聯劑以抑制收縮,但這些調整會導致成本增加和生產週期延長。汽車A級塗料對品質要求極高,即使在快速變化的大規模生產線上,配方設計師也需要不斷創新。

細分市場分析

截至2025年,聚苯乙烯基產品在低排放添加劑市場中佔據38.62%的佔有率,這主要得益於其在汽車SMC應用中展現出的卓越成本績效。隨著汽車製造商尋求獲得碳減排積分,預計到2031年,「其他」類型(主要為生物基)低排放添加劑的市場規模將以8.74%的複合年成長率快速成長。

聚醋酸乙烯酯和聚甲基丙烯酸甲酯(PMMA)基產品佔據了對衝擊強度和光學透明度有較高要求的細分市場,而高密度聚苯乙烯則適用於對成本敏感的零件。聚酯基產品(純聚酯和聚氨酯改質型)適用於腐蝕性和高溫環境。BASF的生質能平衡EPS清楚地展示了現有供應商如何將永續性融入現有的生產過程中。

區域分析

亞太地區正引領低調的添加劑市場發展,預計到2025年將佔據44.12%的市場佔有率,到2031年將以7.55%的複合年成長率成長。中國電動車的蓬勃發展和政府主導的基礎設施建設推動了複合材料的應用,同時,當地供應商也在擴大熱固性樹脂的產能。印度汽車產業的擴張和韓國電子產品出口的成長也為市場發展提供了助力。BASF擴建其南京工廠,凸顯了對區域生產的戰略重視。

北美位居第二,這得益於電動車平台的推出、航太業的重組以及風力發電設施的宣傳活動。美國擁有先進的樹脂實驗室和鈽生產線,而墨西哥則利用接近性原始設備製造商(OEM)工廠的優勢,促進本地零件生產。陶氏化學的風力渦輪機葉片樹脂計畫凸顯了該地區的技術實力。

其次,歐洲的特點是嚴格的永續性要求,這加速了生物基低排放添加劑的普及應用。德國豪華汽車品牌正在車身本體件中使用複合材料,北歐國家則大力投資可再生能源,用於大型渦輪葉片。贏創的木質素計畫和BYK的無VOC界面活性劑,都體現了該地區對創新的承諾。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車產業對高性能SMC(片狀成型塑膠)配方的需求不斷成長。

- 加快制定降低電動車重量的法規

- 鋼筋(用於加固水泥建築物的鋼材)的替代品

- 纖維增強塑膠(FRP)的新應用

- 源自木質素和蓖麻油的生物基LPA正受到關注。

- 市場限制因素

- 含交聯苯乙烯單體的不飽和聚酯樹脂的高聚合收縮率

- 與熱塑性複合材料的競爭

- 熱固性部件可修復性的局限性

- 價值鏈分析

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 聚苯乙烯

- 聚乙酸乙烯酯

- PMMA型

- 高密度聚苯乙烯(HDPE)

- 聚酯纖維

- 純飽和聚酯

- PU改質飽和聚酯

- 其他產品類型(EVA、SAN、生物基)

- 透過使用

- 射出成型/壓縮成型(SMC/BMC)

- 冥王星

- 樹脂轉注成形(RTM)

- 手工積層

- 噴灑

- 按最終用戶行業分類

- 汽車和交通運輸

- 建築/施工

- 電氣和電子設備

- 工業機械

- 其他(消費品、船舶)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ALTANA AG

- AOC

- Arkema

- Ashland

- Clariant

- Composites One

- Evonik Industries AG

- INEOS

- Link Composites Pvt. Ltd.

- Mechemco

- Mitsubishi Chemical Group Corporation

- Monachem

- Poliya

- Polynt SpA

- Scott Bader Company Ltd

- Swancor

- Synthomer Plc

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, low profile additives market size in 2026 is estimated at USD 0.84 billion, growing from 2025 value of USD 0.79 billion with 2031 projections showing USD 1.17 billion, growing at 6.78% CAGR over 2026-2031.

This report is Segmented by Product Type (Polystyrene-Based, Polyvinyl Acetate-Based, and More), Application (Injection and Compression Molding, Pultrusion, and More), End-User Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Low Profile Additives Market Trends and Insights

Increase in Demand for High-performance SMC Formulations from Automotive Industry

Automakers are scaling SMC to mold battery enclosures, body panels, and structural inserts that need flawless Class A finishes. Low profile additives limit volumetric shrinkage, securing dimensional stability under thermal cycling. Dow's polyurethane-carbon fiber spar cap demonstrates cure efficiencies exceeding 90%, exemplifying how next-generation additives support high-speed presses. Larger vehicle platforms and thick-section parts further raise shrinkage control requirements, making advanced low profile additives indispensable across Asia-Pacific's fast-growing electric vehicle hubs.

Accelerated EV Lightweighting Mandates

The European Union's CO2 rules and China's New Energy Vehicle quotas spur rapid fiber-reinforced plastic adoption. Low profile additives underpin these composites by preventing sink marks and waviness even in multi-material assemblies. University of Virginia research shows weight savings of 31% in graphene-modified cement composites, a proxy for similar mass-reduction prospects in auto structures. Rising battery range expectations will continue to pull lightweight composites, sustaining additive demand.

High Polymerization Shrinkage of Unsaturated Polyester Resin with Crosslinking Styrene Monomer

UPR-styrene systems inherently contract during cure, generating voids and print-through that low profile additives must counteract. Suppliers experiment with reactive diluents and modified crosslinkers to curb shrinkage, but such tweaks add cost and cycle-time complexity. Automotive Class A finishes set a high bar, pressuring formulators to keep innovating even in fast-moving, high-volume lines.

Other drivers and restraints analyzed in the detailed report include:

- Replacement of Steel Rebar with Fiber-reinforced Plastics

- Growing Emphasis on Bio-based LPAs from Lignin & Castor Oil

- Competition from Thermoplastic Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polystyrene-based grades retained 38.62% low profile additives market share in 2025 through proven cost-performance balance in automotive SMC. The low profile additives market size for "Other" product types-largely bio-based-should rise swiftly, expanding at 8.74% CAGR to 2031 as OEMs chase carbon reduction credits.

Polyvinyl acetate and PMMA variants occupy niches that demand impact strength or optical clarity, while high-density polyethylene grades suit budget-sensitive parts. Polyester-based offerings, both pure and PU-modified, tackle corrosive or high-temperature environments. BASF's biomass-balance EPS underscores how incumbent suppliers blend sustainability with incumbent processes.

Complete Report Scope:

- By Product Type

- Polystyrene-based

- Polyvinyl Acetate-based

- PMMA-based

- High Density Polyethylene (HDPE)

- Polyester-based

- Pure Saturated Polyester

- PU-modified Saturated Polyester

- Other Product Types (EVA, SAN, Bio-based)

- By Application

- Injection and Compression Molding (SMC/BMC)

- Pultrusion

- Resin Transfer Molding (RTM)

- Hand Lay-Up

- Spray-Up

- By End-User Industry

- Automotive and Transportation

- Building and Construction

- Electrical and Electronics

- Industrial Machinery

- Others (Consumer Goods, Marine)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific dominated the low profile additives market with 44.12% share in 2025 and an 7.55% CAGR outlook to 2031. China's electric vehicle surge and state-backed infrastructure rollouts underpin composite adoption, while local suppliers scale thermoset capacity. India's automotive expansion and South Korea's electronics exports add tailwinds. BASF's Nanjing site enlargement underscores strategic focus on regional production.

North America ranked second, buoyed by EV platform launches, aerospace rebuilds, and wind-repowering campaigns. The United States houses advanced resin labs and pultrusion lines, while Mexico's proximity to OEM plants fuels part localization. Dow's wind-blade resin programs highlight regional technical prowess.

Europe follows, characterized by strict sustainability requirements that hasten bio-based low profile additives uptake. Germany's premium auto brands adopt composites for body-in-white elements, and Nordic nations channel renewables investments into large turbine blades. Evonik's lignin programs and BYK's VOC-free surfactants typify the innovation thrust.

- ALTANA AG

- AOC

- Arkema

- Ashland

- Clariant

- Composites One

- Evonik Industries AG

- INEOS

- Link Composites Pvt. Ltd.

- Mechemco

- Mitsubishi Chemical Group Corporation.

- Monachem

- Poliya

- Polynt S.p.A

- Scott Bader Company Ltd

- Swancor

- Synthomer Plc

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand for High-performance SMC (Sheet Molding Compound) Formulations from Automotive Industry.

- 4.2.2 Accelerated EV lightweighting mandates

- 4.2.3 Replacement of Steel Rebar (Reinforcing Bar Employed to Strengthen Concrete Structures)

- 4.2.4 Emerging Applications in Fiber-reinforced Plastics (FRP)

- 4.2.5 Growing emphasis on Bio-based LPAs from lignin & castor oil

- 4.3 Market Restraints

- 4.3.1 High Polymerization Shrinkage of Unsaturated Polyester Resin with the Crosslinking Styrene Monomer

- 4.3.2 Competition from thermoplastic composites

- 4.3.3 Limited repairability of thermoset parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polystyrene-based

- 5.1.2 Polyvinyl Acetate-based

- 5.1.3 PMMA-based

- 5.1.4 High Density Polyethylene (HDPE)

- 5.1.5 Polyester-based

- 5.1.5.1 Pure Saturated Polyester

- 5.1.5.2 PU-modified Saturated Polyester

- 5.1.6 Other Product Types (EVA, SAN, Bio-based)

- 5.2 By Application

- 5.2.1 Injection and Compression Molding (SMC/BMC)

- 5.2.2 Pultrusion

- 5.2.3 Resin Transfer Molding (RTM)

- 5.2.4 Hand Lay-Up

- 5.2.5 Spray-Up

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Building and Construction

- 5.3.3 Electrical and Electronics

- 5.3.4 Industrial Machinery

- 5.3.5 Others (Consumer Goods, Marine)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 ALTANA AG

- 6.4.2 AOC

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 Clariant

- 6.4.6 Composites One

- 6.4.7 Evonik Industries AG

- 6.4.8 INEOS

- 6.4.9 Link Composites Pvt. Ltd.

- 6.4.10 Mechemco

- 6.4.11 Mitsubishi Chemical Group Corporation.

- 6.4.12 Monachem

- 6.4.13 Poliya

- 6.4.14 Polynt S.p.A

- 6.4.15 Scott Bader Company Ltd

- 6.4.16 Swancor

- 6.4.17 Synthomer Plc

- 6.4.18 Wacker Chemie AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment