|

市場調查報告書

商品編碼

2073390

無底紙標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Linerless Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

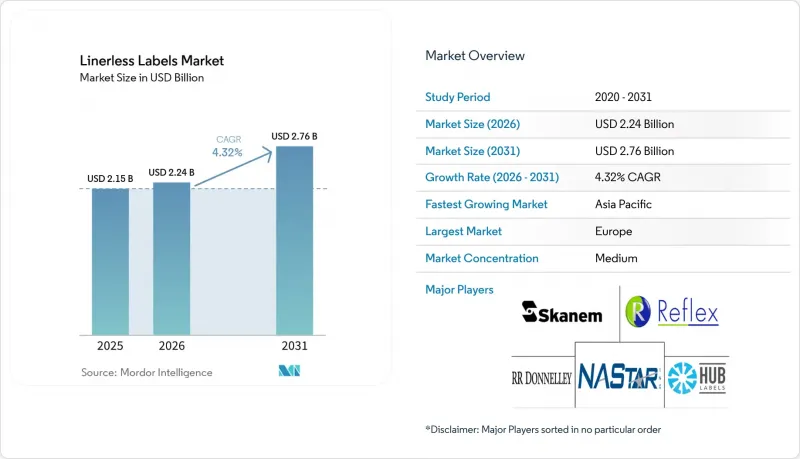

根據 Mordor Intelligence 預測,無底紙標籤市場預計將從 2025 年的 21.5 億美元成長到 2026 年的 22.4 億美元,到 2031 年達到 27.6 億美元,2026 年至 2031 年的複合年成長率預計為 4.26%。

本報告按印刷技術(數位印刷、柔版印刷、凹版印刷等)、承印物(紙張、薄膜、特殊/再生承印物)、黏合劑類型(丙烯酸黏合劑、熱熔黏合劑等)、終端用戶行業(食品、飲料、醫療保健/製藥、化妝品/個人護理等)和地區進行細分。市場預測以美元計價。

全球無底紙標籤市場趨勢與洞察

食品飲料包裝對永續性的要求日益提高。

包裝食品和飲料的永續性要求正從自願性目標轉向營運要求,這一轉變正在推動各大包裝產品類別中無底紙標籤市場的發展。 2026年,FINAT指出,進入歐盟市場的包裝材料需要滿足PPWR框架下更嚴格的可回收性要求,凸顯了減少廢棄物和簡化材料流轉的標籤形式的重要性。 2025年,Ravenwood Packaging指出,無底紙標籤透過消除離型紙,將有助於生產商適應英國和歐盟的政策變化,從而減少廢棄物產生並減輕廢棄物處理的負擔。這在冷藏食品行業的影響尤其顯著,因為該行業的標籤使用量巨大,且廢棄物處理合約正在接受審查。因此,無底紙標籤市場正在蓬勃發展,永續性目標正與成本和合規性一起,成為採購決策的關鍵因素。

電子商務物流的快速發展需要長度不一的運輸標籤。

小包裹數量的持續成長持續推動著無底紙標籤市場的發展。這是因為連續卷材標籤非常適合大批量運輸作業,能夠滿足標籤長度可變和快速更換的需求。根據美國人口普查局估計,2025年零售電商銷售額將顯著成長,零售履約和第三方物流(3PL) 網路對小包裹的需求將保持旺盛。 Lowry Solutions 預測,到 2025 年,無底紙標籤非常適合需要高效列印和應用流程以適應不斷變化的包裝形式的物流和倉儲環境。在人口密集的都市區履約中心,這種模式的價值更為顯著,因為營運商可以減少物料搬運流程,並降低標籤庫存所需的空間。因此,無底紙標籤市場正從傳統的食品服務服務業擴展到主流的履約和物流應用領域。

維修傳統貼標生產線的成本

改裝成本仍然是無底紙標籤市場面臨的最主要短期限制因素之一,尤其是在那些圍繞傳統底紙系統建造的工廠和物流中心。 Lowry Solutions 在 2025 年指出,標準桌上型和行動式熱敏印表機不支援無底紙格式,而專用系統則需要特殊的組件,例如不沾滾筒和專用活化單元。這使得食品和受監管的終端用戶行業的轉型路徑更加漫長,因為硬體變更必須通過內部認證和合規性審核。因此,無底紙標籤市場呈現出兩極化的局面:一方面是能夠從一開始就指定使用無底紙系統的新興場所,另一方面是需要更有力地證明成本節約才能進行投資的老舊場所。即使出現了模組化升級方案,對於資本預算有限的中小型加工商和合約包裝公司而言,無底紙標籤市場的普及速度仍然緩慢。

細分市場分析

2025年,柔版印刷在無底紙標籤市場佔據了40.43%的佔有率。這反映了其悠久的歷史、大規模生產的經濟優勢以及與塗膠面材的廣泛兼容性。凹版印刷仍然作為一種較為有限的選擇,應用於某些高階飲料和化妝品領域,在這些領域,圖像一致性至關重要。其他印刷方法,包括網版印刷和膠印混合印刷,更多用於小規模、要求更高的項目,而非滿足核心的大規模生產需求。儘管柔版印刷擁有悠久的歷史,但無底紙標籤市場正日益明顯地向數位化印刷轉型,數位化印刷不僅注重印版效率,還注重可變數據、小批量生產和整合追蹤功能等附加價值。

預計到2031年,數位(噴墨和熱敏)印刷將以5.43%的複合年成長率成長,這一成長正在改變無底紙標籤行業加工商在產能、批量大小和數據複雜性之間的平衡方式。 Labels and Labeling 發布的一份2026年報告指出,1200 DPI噴墨系統對那些尋求在小批量到大批量應用中實現穩定品質和可擴展生產力的加工商來說,正變得越來越有吸引力。混合噴墨系統也越來越受歡迎,因為它們在不放棄現有表面處理工程或傳統印刷設備的前提下,增加了數位柔軟性。隨著網路標籤訂單的成長和智慧標籤需求的日益普及,無底紙標籤市場可能會繼續向混合生產模式轉型,柔版印刷仍然很重要,而數位印刷則承擔了快速成長的工作量。

2025年,PP、PET和PE等薄膜基材將佔據無底紙標籤市場48.23%的佔有率,這主要得益於其在食品、飲料和個人護理應用領域優異的耐濕性、耐化學性和尺寸穩定性。同時,紙質面材在對印刷品質要求相對較低、成本控制更為重要的領域,例如保存食品標籤、熱敏列印應用、快餐店小票和運輸標籤,仍然發揮著重要作用。特種和再生基材是成長最快的表面材料類別,預計到2031年將以5.72%的複合年成長率成長。這一構成表明,儘管採購標準中越來越重視可回收性和廢舊產品衍生材料的比例,但無底紙標籤市場仍然主要由成熟的高性能材料支撐。

2026年5月,UPM膠黏材料公司發布了食品飲料和家居/個人護理用品領域的硬質PET和HDPE包裝的「UPM ProCycle」產品組合。這些材料經過獨立檢驗,可在所有包裝類型和市場中回收。 2024年10月,UPM Raflatac公司推出了適用於可回收和可重複使用塑膠食品容器的「OptiCut WashOff」無底紙標籤。本產品可在工業清洗過程中實現更順暢的剝離,進而提高與包裝再利用循環的兼容性。在無底紙標籤產業,這些新產品的推出表明,材料創新正從「新穎性」轉向展現與實際回收和再利用系統的兼容性。這表明,無底紙標籤市場正在拓展到那些永續性聲明需要實際應用證據的應用領域,而不僅僅是空泛的訊息。

區域分析

2025年,歐洲佔據了無底紙標籤市場38.82%的佔有率,繼續保持其在該地區的主導地位,這主要得益於相關法規、加工能力以及大型零售連鎖店的推動。 FINAT在2026年發布的報告指出,PPWR(塑膠包裝法規)的發展方向將提升那些既能滿足歐盟市場准入要求又能滿足可回收性要求的包裝形式的商業性重要性。在英國,透過生產者延伸責任制(EPR)和強調可回收性的收費結構,經濟促進因素共同促進了不可回收底紙廢棄物的消除。德國和法國仍然是歐洲國內市場發展最成熟的國家,而義大利和其他歐洲國家的無底紙標籤市場主要集中在大規模食品和物流業者。

預計到2031年,亞太地區將以6.04%的複合年成長率成長,成為無底紙標籤市場成長最快的區域市場。 2025年9月,佐藤株式會社宣布,Askul公司已在其關東物流中心採用其「NonSepa」無底紙標籤,並使用專用自動化標籤列印和貼標設備取代了傳統的帶底紙標籤。此外,由於一線城市的廢棄物費用超過每噸300元人民幣(約每噸42美元),中國物流業者面臨龐大的營運成本,底紙處理成為一項重要的營運支出。因此,印度、印尼、越南、日本、韓國和澳洲等國正在推動該地區的成長,這主要得益於小包裹的增加和標籤自動化技術的進步。

北美地區在無底紙標籤市場仍處於成熟階段,其普及性更多地受到零售商評估標準、物流量和營運效率的驅動,而非聯邦包裝法規的限制。美國人口普查局發布的2025年電子商務銷售預測顯示,小包裹量的持續成長將繼續推動對無底紙標籤包裝形式的持續需求。 Lowry Solutions也指出,到2025年,無底紙標籤包裝形式非常適合倉儲、物流和快餐店等應用場景,因為在這些場景中,高效的列印和貼標作業至關重要。南美洲仍處於無底紙標籤市場發展的早期階段,其中巴西和阿根廷是重要的成長市場,而中東和非洲則蘊藏著與物流現代化和低溫運輸投資相關的長期發展機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強食品和飲料包裝永續性的監管

- 電子商務物流的快速成長對可變長度運輸標籤的需求日益成長

- 歐洲和北美關於減少廢棄物的監管義務

- 快餐店的廚房自動化正在推動按需無底紙印刷。

- 推出支援RFID技術的互聯包裝和微型倉配。

- 碳邊境調節機制提高了對低廢棄物標籤的需求。

- 市場限制因素

- 維修舊貼標生產線的成本

- 黏合劑和脫模塗料原料價格波動

- 低溫運輸環境中的黏合劑累積問題

- 高性能無矽黏合劑供不應求

- 宏觀經濟因素對市場的影響

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過印刷技術

- 數位(噴墨和熱敏)

- 柔版印刷

- 凹版印刷

- 其他印刷技術

- 按基礎材料

- 紙

- 薄膜(PP、PET、PE)

- 特殊回收基材

- 黏合劑類型

- 丙烯酸黏合劑

- 黏合劑

- 特殊黏合劑

- 其他類型的黏合劑

- 按最終用戶行業分類

- 食物

- 飲料

- 醫療和藥品

- 化妝品和個人護理

- 家用化學品

- 物流與電子商務

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 澳洲

- 印度

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avery Dennison Corporation

- CCL Industries Inc. and Innovia Films

- 3M Company

- Beontag

- UPM Raflatac

- Coveris

- Hub Labels Inc.

- Reflex Labels Ltd

- Skanem AS

- NAStar Inc.

- Optimum Group

- SATO Europe GmbH

- ProPrint Group

- Lexit Group AS

- RR Donnelley and Sons Company

- Gipako UAB

- Lintec Corporation

- HERMA GmbH

- Zebra Technologies Corporation

- Multi-Color Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the linerless labels market size is expected to increase from USD 2.15 billion in 2025 to USD 2.24 billion in 2026 and reach USD 2.76 billion by 2031, growing at a CAGR of 4.26% over 2026-2031.

This report is Segmented by Printing Technology (Digital, Flexographic, Gravure, and More), Facestock Material (Paper, Film, and Specialty and Recycled Substrates), Adhesive Type (Acrylic Adhesives, Hot-Melt Adhesives, and More), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, Cosmetics and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Linerless Labels Market Trends and Insights

Rising Sustainability Mandates in Food and Beverage Packaging

Sustainability requirements in packaged food and beverage are moving from voluntary goals toward operating requirements, and that shift is supporting the linerless labels market across major packaged goods categories. FINAT stated in 2026 that packaging placed on the EU market will need to meet stricter recyclability requirements under the PPWR framework, underscoring the importance of label formats that reduce waste and simplify material flows. Ravenwood Packaging noted in 2025 that linerless formats help producers respond to UK and EU policy shifts by removing the release liner, thereby reducing disposal needs and supporting lower waste-handling burdens. That matters most in chilled food lines, where label volumes are high, and disposal contracts are already under review. As a result, the linerless labels market is gaining traction, with sustainability goals now sitting alongside cost and compliance in procurement decisions.

E-Commerce Logistics Boom Requiring Variable-Length Shipping Labels

Parcel growth continues to support the linerless labels market, as continuous rolls suit high-volume shipping operations that require variable label lengths and fast changeovers. The United States Census Bureau estimated that retail e-commerce sales in 2025 grew significantly, keeping parcel demand elevated across retail fulfillment and third-party logistics networks. Lowry Solutions explained in 2025 that linerless labeling is well-suited to logistics and warehouse settings that need efficient print-and-apply workflows across changing package formats. The value of this model increases further in dense urban fulfillment sites, where operators benefit from fewer material-handling steps and lower space requirements for label stock. These conditions are helping the linerless labels market expand beyond its earlier food-service base into mainstream fulfillment and shipping applications.

Retrofit Costs for Legacy Labeling Lines

Retrofit spending remains one of the clearest near-term constraints on the linerless labels market, especially in plants and distribution centers built around conventional liner systems. Lowry Solutions noted in 2025 that standard thermal desktop and mobile printers do not support linerless formats, and that dedicated systems require specialized components, such as non-stick rollers and purpose-built activation units. This creates a longer conversion path for food and regulated end uses, where hardware changes must also pass internal qualification and compliance reviews. The linerless labels market is therefore splitting between newer sites that can specify linerless systems from the start and older sites that need a stronger savings case before investing. Even where modular upgrade paths are emerging, the linerless labels market still faces slower adoption among smaller converters and contract packagers with tighter capital budgets.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Waste-Reduction Mandates in Europe and North America

- RFID-Enabled Connected Packaging and Micro-Fulfillment Adoption

- Raw-Material Price Volatility in Adhesives and Release Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexographic printing held a 40.43% share of the linerless labels market in 2025, reflecting its long installed base, efficient economics in long runs, and broad compatibility with adhesive-coated facestocks. Gravure printing remained a narrower option used in selected premium beverage and cosmetics applications where high image consistency still matters. Other printing formats, including screen and offset hybrids, served smaller, specification-heavy programs rather than core-volume demand. Even with that installed base, the linerless labels market is shifting more clearly toward digital formats where variable data, shorter runs, and integrated tracking functions carry more value than plate efficiency alone.

Digital (inkjet and thermal) printing is projected to grow at a 5.43% CAGR through 2031, and that expansion is changing how converters in the linerless labels industry balance capacity, run length, and data complexity. Labels and Labeling reported in 2026 that 1,200 DPI inkjet systems are becoming more attractive to converters seeking consistent quality and scalable productivity across short- to long-run applications. Hybrid inkjet systems are also gaining ground because they let converters add digital flexibility without abandoning existing finishing and conventional print assets. As web-to-label ordering expands and smart-label requirements become more common, the linerless labels market is likely to keep moving toward a mixed production base where flexo stays important but digital absorbs the faster-growing workloads.

Film substrates, including PP, PET, and PE, accounted for 48.23% of the linerless labels market size in 2025 because they offered strong moisture resistance, chemical durability, and dimensional stability across food, beverage, and personal care use. Paper facestocks remained important for ambient food labeling, direct thermal applications, quick-service restaurant ticketing, and shipping labels, where print quality needs are simpler and cost control matters more. Specialty and recycled substrates formed the fastest-growing facestock group, with a 5.72% CAGR expected through 2031. This mix shows that the linerless labels market is still anchored by proven performance materials, even as procurement standards are increasingly rewarding recyclability and post-consumer content.

UPM Adhesive Materials introduced the UPM ProCycle portfolio in May 2026 for rigid PET and HDPE packaging in food and beverage and home and personal care applications, with the materials independently verified as recycling-compatible across packaging types and markets. UPM Raflatac also launched the OptiCut WashOff linerless label in October 2024 for returnable and reusable plastic food containers, supporting cleaner removal during industrial washing and better alignment with packaging reuse cycles. Within the linerless labels industry, these launches show that material innovation is focused less on novelty and more on proving compatibility with real recycling and reuse systems. That is helping the linerless labels market expand into applications where sustainability claims now need operational evidence rather than broad messaging.

Complete Report Scope:

- By Printing Technology

- Digital (Inkjet and Thermal)

- Flexographic

- Gravure

- Other Printing Technologies

- By Facestock Material

- Paper

- Film (PP, PET, PE)

- Specialty and Recycled Substrates

- By Adhesive Type

- Acrylic Adhesives

- Hot-Melt Adhesives

- Specialty Adhesives

- Other Adhesive Types

- By End-User Industry

- Food

- Beverage

- Healthcare and Pharmaceuticals

- Cosmetics and Personal Care

- Household Chemicals

- Logistics and E-commerce

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Australia

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held 38.82% of the linerless labels market in 2025, maintaining its leading regional position, as regulations, converter capabilities, and large retail chains all supported adoption. FINAT reported in 2026 that the PPWR direction strengthens the commercial importance of packaging formats that can meet recyclability expectations and maintain access to the EU market. The UK added a parallel economic driver through Extended Producer Responsibility, with recyclability-weighted fees reinforcing the case for eliminating non-recyclable liner waste. Germany and France remained the most advanced national markets in Europe, while adoption in Italy and the rest of the region stayed more concentrated among larger food and logistics operators.

Asia-Pacific is projected to expand at a 6.04% CAGR through 2031, which makes it the fastest-growing regional segment in the linerless labels market. SATO Corporation announced in September 2025 that ASKUL adopted its NonSepa linerless label at the Kanto Distribution Center, using dedicated automatic label-printing and application machines to replace conventional liner labels. China's logistics operators are also working in an environment where Tier-1 city waste fees above CNY 300 per tonne (USD 42 per tonne), make liner disposal a visible operating cost. India, Indonesia, Vietnam, Japan, South Korea, and Australia are therefore contributing to a regional growth pattern that combines parcel expansion with more automated labeling practices.

North America remained a mature region in the linerless labels market, where adoption was driven more by retailer scorecards, logistics throughput, and operating efficiency than by broad federal packaging mandates. The United States Census Bureau's 2025 e-commerce sales estimate shows why parcel intensity remains a durable demand driver for linerless shipping formats. Lowry Solutions also noted in 2025 that linerless formats align well with warehouse, logistics, and quick-service restaurant labeling use cases that depend on efficient print-and-apply operations. South America remained earlier in its adoption curve, with Brazil and Argentina standing out as the main growth markets, while the Middle East and Africa represented a longer-duration opportunity tied to logistics modernization and cold-chain investment.

- Avery Dennison Corporation

- CCL Industries Inc. and Innovia Films

- 3M Company

- Beontag

- UPM Raflatac

- Coveris

- Hub Labels Inc.

- Reflex Labels Ltd

- Skanem AS

- NAStar Inc.

- Optimum Group

- SATO Europe GmbH

- ProPrint Group

- Lexit Group AS

- R.R. Donnelley and Sons Company

- Gipako UAB

- Lintec Corporation

- HERMA GmbH

- Zebra Technologies Corporation

- Multi-Color Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Sustainability Mandates in Food and Beverage Packaging

- 4.2.2 E-commerce Logistics Boom Requiring Variable-Length Shipping Labels

- 4.2.3 Regulatory Waste-Reduction Mandates in Europe and North America

- 4.2.4 Quick-Service Restaurant Kitchen Automation Driving On-Demand Linerless Printing

- 4.2.5 RFID-Enabled Connected Packaging and Micro-Fulfillment Adoption

- 4.2.6 Carbon Border Adjustment Mechanisms Elevating Demand for Low-Waste Labeling

- 4.3 Market Restraints

- 4.3.1 Retrofit Costs for Legacy Labeling Lines

- 4.3.2 Raw-Material Price Volatility in Adhesives and Release Coatings

- 4.3.3 Adhesive Build-Up Issues in Cold-Chain Environments

- 4.3.4 Shortage of High-Performance Silicone-Free Adhesives

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Digital (Inkjet and Thermal)

- 5.1.2 Flexographic

- 5.1.3 Gravure

- 5.1.4 Other Printing Technologies

- 5.2 By Facestock Material

- 5.2.1 Paper

- 5.2.2 Film (PP, PET, PE)

- 5.2.3 Specialty and Recycled Substrates

- 5.3 By Adhesive Type

- 5.3.1 Acrylic Adhesives

- 5.3.2 Hot-Melt Adhesives

- 5.3.3 Specialty Adhesives

- 5.3.4 Other Adhesive Types

- 5.4 By End-User Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare and Pharmaceuticals

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Household Chemicals

- 5.4.6 Logistics and E-commerce

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Australia

- 5.5.4.5 India

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc. and Innovia Films

- 6.4.3 3M Company

- 6.4.4 Beontag

- 6.4.5 UPM Raflatac

- 6.4.6 Coveris

- 6.4.7 Hub Labels Inc.

- 6.4.8 Reflex Labels Ltd

- 6.4.9 Skanem AS

- 6.4.10 NAStar Inc.

- 6.4.11 Optimum Group

- 6.4.12 SATO Europe GmbH

- 6.4.13 ProPrint Group

- 6.4.14 Lexit Group AS

- 6.4.15 R.R. Donnelley and Sons Company

- 6.4.16 Gipako UAB

- 6.4.17 Lintec Corporation

- 6.4.18 HERMA GmbH

- 6.4.19 Zebra Technologies Corporation

- 6.4.20 Multi-Color Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球無底紙標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無底紙標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 無底紙標籤市場:依技術、材料、黏合劑類型、成分、最終用途產業和分銷管道分類-2026-2032年全球市場預測

無底紙標籤市場:依技術、材料、黏合劑類型、成分、最終用途產業和分銷管道分類-2026-2032年全球市場預測 2026-2030年全球無底紙標籤市場

2026-2030年全球無底紙標籤市場 無底紙標籤市場規模、佔有率和成長分析(按配方、黏合劑類型、產品、印刷油墨、印刷技術、最終用途產業和地區分類)—產業預測(2026-2033 年)無底紙標籤市場-2025-2030年預測

無底紙標籤市場規模、佔有率和成長分析(按配方、黏合劑類型、產品、印刷油墨、印刷技術、最終用途產業和地區分類)—產業預測(2026-2033 年)無底紙標籤市場-2025-2030年預測 全球無底紙標籤市場(2025年)

全球無底紙標籤市場(2025年) 無底紙標籤市場,按成分、按油墨類型、按應用、按印刷技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

無底紙標籤市場,按成分、按油墨類型、按應用、按印刷技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 無底紙標籤市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

無底紙標籤市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測