|

市場調查報告書

商品編碼

2073375

安全軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Security Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

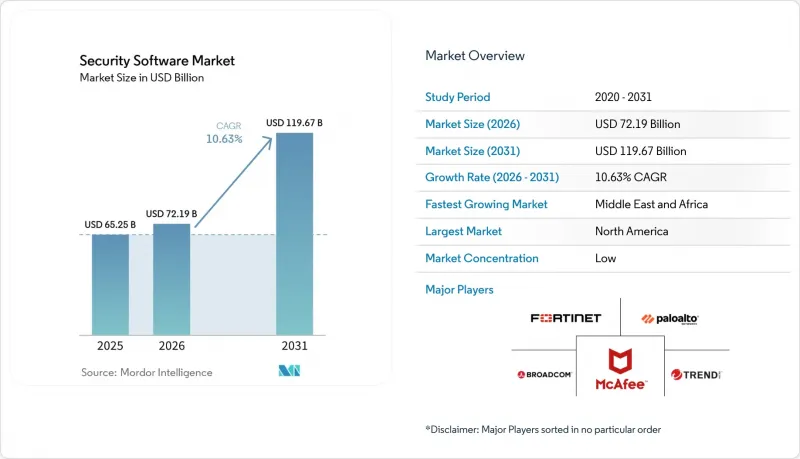

據 Mordor Intelligence 稱,2025 年安全軟體市場價值為 652.5 億美元,預計到 2031 年將達到 1196.7 億美元,而 2026 年為 721.9 億美元,預測期(2026-2031 年)的複合年成長率為 10.63%。

本報告按產品類型(防毒/反惡意軟體、防火牆和統一威脅管理 (UTM) 裝置、其他)、部署模式(本地部署、雲端部署、其他)、企業規模(大型企業、中小企業)、應用領域(行動安全、消費者安全、其他)、最終用戶產業(銀行、金融服務和保險 (BFSI)、醫療保健、零售和電子商務、其他地區進行細分、零售和電子商務區域。市場預測以美元 (USD) 為單位。

全球安全軟體市場趨勢與洞察

網路攻擊的數量和複雜性日益增加

攻擊者正利用魚叉式網路釣魚、深度造假語音和生成式人工智慧工具來自動化多態惡意軟體,迫使企業轉向更具適應性、以分析主導的防禦策略。 2024年,25.7%的工業安全事件針對製造地,迫使鋼鐵製造商紐柯公司在一次安全漏洞事件後重新評估整個檢測系統。去年,亞太地區(APAC)佔全球整體的31%,預計到2025年,該地區的網路犯罪損失將達到3.3兆美元。這些威脅趨勢正在加速安全軟體市場對整合式擴充偵測與回應(XDR)平台的採用。

遵守 GDPR、CCPA、DORA 和產業特定網路安全法規的義務

監管機構正在實施技術控制措施,而非寬泛的原則。歐盟的《數位營運韌性法案》(DORA)將於2025年1月生效,該法案強制要求金融機構維護全天候事件通報和第三方風險監控。同樣,《網路韌性法案》要求所有連網產品都必須採用「安全設計」軟體。因此,跨境營運的機構擴大採用自動化合規儀表板,這正在推動安全軟體市場平台收入的成長。

網路安全專業人才短缺推高了整體擁有成本。

全球範圍內,安全專業人員缺口高達480萬,光在美國就需要額外26.5萬名專業人員來應對日益複雜的部署。人才短缺推高了薪資水平,促使買家更傾向於選擇具備自動化功能和託管服務選項的平台。儘管供應商正在整合人工智慧驅動的編配功能以最大限度地減少人工干預,但初始整合仍然需要稀缺的工程技術人才,這在某些行業中減緩了部署速度。

細分市場分析

身分與存取管理 (IAM) 平台預計在 2025 年佔總收入的 22.65%,凸顯了其在無邊界策略中的核心地位。 IAM 安全軟體市場規模預計將從 2026 年的 171.8 億美元成長到 2031 年的 364.7 億美元,複合年成長率 (CAGR) 為 16.25%。 IAM 套件現已整合無密碼身份驗證、即時權限管理和行為分析功能,取代了傳統的 VPN。雖然防火牆和統一威脅管理 (UTM) 的升級對於檢查混合流量仍然至關重要,但支出正轉向符合零信任原則的下一代解決方案。加密軟體的需求受到量子威脅的推動,買家優先考慮提供 NIST 認證的後量子模組的供應商。增強型偵測與回應 (XDR) 套件整合了端點、網路和 SaaS 遙測數據,以減少警報疲勞,並為供應商更廣泛地採用該平台奠定基礎。

在預測期內,與競爭對手的差異化將取決於人工智慧的整合深度和可解釋性。整合硬體級信任根、API優先架構和內建合規性映射的供應商正在獲得大規模的多年期合約續約。產品藍圖正擴大納入輕量級代理、敏感運算支援和策略即程式碼功能,以滿足安全軟體市場中現代DevSecOps管線的編配需求。

到 2025 年,基於雲端的解決方案將佔總收入的 61.50%。各組織機構認為雲端解決方案具有許多優勢,例如彈性可擴展性、持續的功能更新以及不計營運成本的支出 (OPEX)。預計到 2031 年,透過雲端交付的安全軟體市場將以 17.8% 的複合年成長率成長,達到 1,006 億美元。由於混合模式對於受監管的工作負載仍然至關重要,領先的供應商正在發布本地閘道器,將日誌傳輸到雲端分析引擎以進行集中監控。

這種轉變迫使供應商將控制平面與資料平面分離,從而能夠在單一策略下,跨容器叢集、邊緣節點和 SaaS API 應用安全措施。結合了安全存取服務邊緣 (SASE)、雲端存取安全仲介(CASB) 和 Web 隔離的訂閱方案因其能夠縮短採購週期而日益普及。雖然本地部署的佔有率正在逐漸下降,但在國防、關鍵基礎設施和主權雲端環境中,由於資料本地化法規要求在國內進行處理,本地部署仍將繼續佔據一席之地。

區域分析

北美市場佔據主導地位,佔2025年銷售額的37.65%,這得益於275億美元的聯邦網路安全預算。公私資料共用舉措和充滿活力的供應商生態系統正在加速人工智慧驅動分析技術的早期應用。美國證券交易委員會(SEC)規定的高額資料揭露罰款進一步推動了積極的投資。

在歐洲,諸如NIS2指令和網路彈性法案等協調一致的法律法規為事件回應和安全開發提供了統一的標準。提供嵌入式多語言合規工作流程的供應商越來越受歡迎,尤其是在歐盟各地的金融機構。

中東地區以14.25%的複合年成長率領先,主要得益於各國政府雄心勃勃的數位經濟計畫。沙烏地阿拉伯的網路安全市場預計到2025年將達到133億沙烏地里亞爾(約35億美元)。該國國內法規要求建立本地資料中心,並在數小時內報告資料外洩事件,這就需要快速升級軟體。同時,亞太地區各國政府正在投資建設聯合安全中心,以降低量子風險和國家主導的網路攻擊,這使得該地區成為安全軟體市場的重要成長前沿。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 網路攻擊的數量和複雜性日益增加

- 遵守 GDPR、CCPA、DORA 和產業特定網路安全法規的義務

- 雲端工作負載的快速成長需要零信任安全性

- 軟體管理措施已成為網路保險承保的強制性要求。

- OT 和 IT 的整合正在推動 ICS 專業安全領域的投資。

- 威脅行為者之間圍繞著人工智慧驅動的「進攻性安全工具」展開軍備競賽。

- 市場限制因素

- 網路安全專業人才短缺推高了整體擁有成本。

- 工具的碎片化和擴散導致了整合的複雜性。

- 開放原始碼安全協定堆疊的興起正在蠶食授權收入。

- 由於量子抗性轉變方面的不確定性,長期合約的簽署被推遲。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 價格分析

- 生態系分析

第5章 市場規模與成長預測

- 依產品類型

- 防毒/反惡意軟體

- 防火牆和統一威脅管理 (UTM)

- 加密軟體

- 身分和存取管理 (IAM)

- 端點保護平台(EPP/EDR)

- 網路安全平台

- 其他類型

- 部署模式

- 現場

- 基於雲端的

- 混合

- 按公司規模

- 大公司

- 中小企業

- 透過使用

- 行動安全

- 消費者安全套件

- 企業/資料中心安全

- 產業最終用途

- BFSI

- 衛生保健

- 零售與電子商務

- 製造業

- 能源公用事業

- 航太/國防

- 電訊

- 政府/公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Broadcom Inc.(Symantec)

- Check Point Software Technologies Ltd.

- International Business Machines Corporation(IBM)

- Trend Micro Incorporated

- CrowdStrike Holdings, Inc.

- McAfee Corp.

- Kaspersky Lab

- Sophos Group plc

- Bitdefender LLC

- Zscaler, Inc.

- Okta, Inc.

- Cloudflare, Inc.

- SentinelOne, Inc.

- Proofpoint, Inc.

- Rapid7, Inc.

- Qualys, Inc.

- Trellix(Musarubra US LLC)

第7章 市場機會與未來展望

According to Mordor Intelligence, the security software market size was valued at USD 65.25 billion in 2025 and estimated to grow from USD 72.19 billion in 2026 to reach USD 119.67 billion by 2031, at a CAGR of 10.63% during the forecast period (2026-2031).

This report is Segmented by Product Type (Antivirus/Anti-malware, Firewall & UTM, and Others), Deployment Mode (On-Premises, Cloud-Based and Others), Enterprise Size (Large Enterprises, SME), Application (Mobile Security, Consumer and Others), End-Use Industry (BFSI, Healthcare, Retail & E-Commerce and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Security Software Market Trends and Insights

Escalating Volume & Sophistication of Cyber-Attacks

Attackers are weaponizing generative AI tools that automate spear-phishing, deepfake audio, and polymorphic malware, forcing enterprises to pivot toward adaptive, analytics-driven defenses. In 2024, 25.7% of recorded industrial incidents targeted manufacturing sites, prompting steelmaker Nucor to overhaul its entire detection stack after a breach. APAC accounted for 31% of global attacks last year, and regional cybercrime costs are forecast to reach USD 3.3 trillion by 2025. These threat dynamics accelerate adoption of unified extended detection and response (XDR) platforms within the security software market.

Mandatory Compliance with GDPR, CCPA, DORA & Sectoral Cyber-Rules

Regulators are prescribing technical controls rather than high-level principles. The EU Digital Operational Resilience Act, effective January 2025, compels financial firms to maintain 24-hour incident reporting and third-party risk oversight. Parallel mandates in the Cyber Resilience Act demand secure-by-design software across all connected products. Cross-border organizations therefore favor automated compliance dashboards, boosting platform revenue inside the security software market.

Shortage of Skilled Cyber Personnel Inflates Total Cost of Ownership

A global talent gap of 4.8 million security professionals persists, with the United States alone needing another 265,000 specialists to keep pace with deployment complexity. Scarcity pushes salaries higher, compelling buyers to favour platforms with automation and managed service options. While vendors embed AI-driven orchestration to minimize manual triage, the upfront integration effort still requires scarce engineering skill, slowing rollouts in some verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cloud Workload Expansion Demanding Zero-Trust Security

- Cyber-Insurance Underwriting Now Mandating Software Controls

- Fragmented Tool Sprawl Drives Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Identity and Access Management platforms generated 22.65% of 2025 revenue, underlining their central role in perimeter-less strategies. The security software market size for IAM is forecast to grow from USD 17.18 billion in 2026 to USD 36.47 billion by 2031, expanding at 16.25% CAGR. IAM suites now bundle password-less authentication, just-in-time privilege, and behavioural analytics, displacing legacy VPNs. Firewall and UTM upgrades remain essential for hybrid traffic inspection, yet spending is shifting toward next-gen offerings aligned to zero-trust principles. Encryption software demand is bolstered by looming quantum threats, with buyers prioritizing vendors offering NIST-validated post-quantum modules. Extended detection and response (XDR) suites unify endpoint, network, and SaaS telemetry, reducing alert fatigue and positioning vendors for wider platform adoption.

Over the forecast period, competitive differentiation will depend on integration depth and AI explainability. Vendors integrating hardware-level root-of-trust, API-first architecture, and built-in compliance mapping are securing larger multiyear renewals. Product roadmaps increasingly feature lightweight agents, confidential computing support, and policy-as-code functions, meeting the orchestration needs of modern DevSecOps pipelines within the security software market.

Cloud-based deployments captured 61.50% revenue in 2025. Organizations cite elastic scalability, continuous feature updates, and opex budgeting benefits. The security software market size for cloud-delivered solutions is projected to climb at an 17.8% CAGR, reaching USD 100.6 billion by 2031. Hybrid models remain vital for regulated workloads; hence leading vendors release on-premises gateways that forward logs to cloud analytics engines for central oversight.

The shift pushes vendors to decouple control planes from data planes, enabling enforcement across container clusters, edge nodes, and SaaS APIs under one policy set. Subscription bundles combining secure access service edge (SASE), cloud access security broker (CASB), and web isolation are resonating, as they cut procurement cycles. On-premises share will gradually decline yet persist in defence, critical infrastructure, and sovereign cloud environments where data-locality rules require in-country processing.

Complete Report Scope:

- By Product Type

- Antivirus / Anti-malware

- Firewall and UTM

- Encryption Software

- Identity and Access Management (IAM)

- Endpoint-protection Platform (EPP / EDR)

- Network Security Platforms

- Other Types

- By Deployment Mode

- On-premise

- Cloud-based

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SME)

- By Application

- Mobile Security

- Consumer Security Suites

- Enterprise / Data-centre Security

- By End-use Industry

- BFSI

- Healthcare

- Retail and e-Commerce

- Manufacturing

- Energy and Utilities

- Aerospace and Defence

- Telecommunications

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America dominated with 37.65% revenue in 2025, supported by the USD 27.5 billion 2025 federal cybersecurity budget. Public-private data-sharing initiatives and a vibrant vendor ecosystem accelerate early adoption of AI-driven analytics. High breach disclosure penalties under U.S. SEC rules further encourage proactive investment.

Europe benefits from harmonized legislation such as the NIS2 Directive and Cyber Resilience Act, providing unified benchmarks for incident response and secure development. Vendors offering built-in multilingual compliance workflows gain traction, especially among pan-EU financial institutions.

The Middle East posts the fastest 14.25% CAGR, spurred by sovereign digital-economy ambitions. Saudi Arabia's cybersecurity market reached SAR 13.3 billion (USD 3.5 billion) in 2025. National regulations mandate local data centers and breach notification within hours, compelling rapid software upgrades. Meanwhile, Asia-Pacific governments invest in joint security centers to mitigate quantum risks and state-sponsored attacks, positioning the region as a significant growth frontier for the security software market.

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Broadcom Inc. (Symantec)

- Check Point Software Technologies Ltd.

- International Business Machines Corporation (IBM)

- Trend Micro Incorporated

- CrowdStrike Holdings, Inc.

- McAfee Corp.

- Kaspersky Lab

- Sophos Group plc

- Bitdefender LLC

- Zscaler, Inc.

- Okta, Inc.

- Cloudflare, Inc.

- SentinelOne, Inc.

- Proofpoint, Inc.

- Rapid7, Inc.

- Qualys, Inc.

- Trellix (Musarubra US LLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating volume and sophistication of cyber-attacks

- 4.2.2 Mandatory compliance with GDPR, CCPA, DORA and sectoral cyber-rules

- 4.2.3 Rapid cloud workload expansion demanding zero-trust security

- 4.2.4 Cyber-insurance underwriting now mandating software controls

- 4.2.5 Convergence of OT and IT triggering spend on specialised ICS security

- 4.2.6 AI-powered "offensive security tooling" arms-race among threat actors

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled cyber personnel inflates total cost of ownership

- 4.3.2 Fragmented tool sprawl drives integration complexity

- 4.3.3 Rising open-source security stack cannibalises licence revenue

- 4.3.4 Quantum-safe migration uncertainty delaying long-term contracts

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Ecosystem Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Antivirus / Anti-malware

- 5.1.2 Firewall and UTM

- 5.1.3 Encryption Software

- 5.1.4 Identity and Access Management (IAM)

- 5.1.5 Endpoint-protection Platform (EPP / EDR)

- 5.1.6 Network Security Platforms

- 5.1.7 Other Types

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SME)

- 5.4 By Application

- 5.4.1 Mobile Security

- 5.4.2 Consumer Security Suites

- 5.4.3 Enterprise / Data-centre Security

- 5.5 By End-use Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 Retail and e-Commerce

- 5.5.4 Manufacturing

- 5.5.5 Energy and Utilities

- 5.5.6 Aerospace and Defence

- 5.5.7 Telecommunications

- 5.5.8 Government and Public Sector

- 5.5.9 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 Palo Alto Networks, Inc.

- 6.4.4 Fortinet, Inc.

- 6.4.5 Broadcom Inc. (Symantec)

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 International Business Machines Corporation (IBM)

- 6.4.8 Trend Micro Incorporated

- 6.4.9 CrowdStrike Holdings, Inc.

- 6.4.10 McAfee Corp.

- 6.4.11 Kaspersky Lab

- 6.4.12 Sophos Group plc

- 6.4.13 Bitdefender LLC

- 6.4.14 Zscaler, Inc.

- 6.4.15 Okta, Inc.

- 6.4.16 Cloudflare, Inc.

- 6.4.17 SentinelOne, Inc.

- 6.4.18 Proofpoint, Inc.

- 6.4.19 Rapid7, Inc.

- 6.4.20 Qualys, Inc.

- 6.4.21 Trellix (Musarubra US LLC)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

網路風險管理市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

網路風險管理市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 安全軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署模式、服務、類型、企業規模、地區和競爭對手分類,2021-2031 年

安全軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署模式、服務、類型、企業規模、地區和競爭對手分類,2021-2031 年 託管網路安全服務市場:按服務類型、部署模式、產業和組織規模分類-2026-2032年全球市場預測網路安全軟體市場:按組件、部署類型、組織規模和行業分類 - 全球市場預測(2026-2032 年)

託管網路安全服務市場:按服務類型、部署模式、產業和組織規模分類-2026-2032年全球市場預測網路安全軟體市場:按組件、部署類型、組織規模和行業分類 - 全球市場預測(2026-2032 年) 2026年全球安全套件市場報告

2026年全球安全套件市場報告 燈塔網路市場:按組件、技術、應用和地區分類

燈塔網路市場:按組件、技術、應用和地區分類 防毒軟體套裝市場規模、佔有率、趨勢和預測:按設備、作業系統、最終用戶和地區分類,2026-2034 年雲端網路安全市場:按組件、部署模型、服務模型、組織規模和產業分類-2026-2032年全球市場預測防毒軟體市場:2026-2032年全球市場預測(按平台、服務類型、保全服務、組織規模、部署模式、銷售管道和最終用戶分類)2026年全球3D(3D)監控軟體市場報告

防毒軟體套裝市場規模、佔有率、趨勢和預測:按設備、作業系統、最終用戶和地區分類,2026-2034 年雲端網路安全市場:按組件、部署模型、服務模型、組織規模和產業分類-2026-2032年全球市場預測防毒軟體市場:2026-2032年全球市場預測(按平台、服務類型、保全服務、組織規模、部署模式、銷售管道和最終用戶分類)2026年全球3D(3D)監控軟體市場報告