|

市場調查報告書

商品編碼

2073363

微出行:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Micro Mobility - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

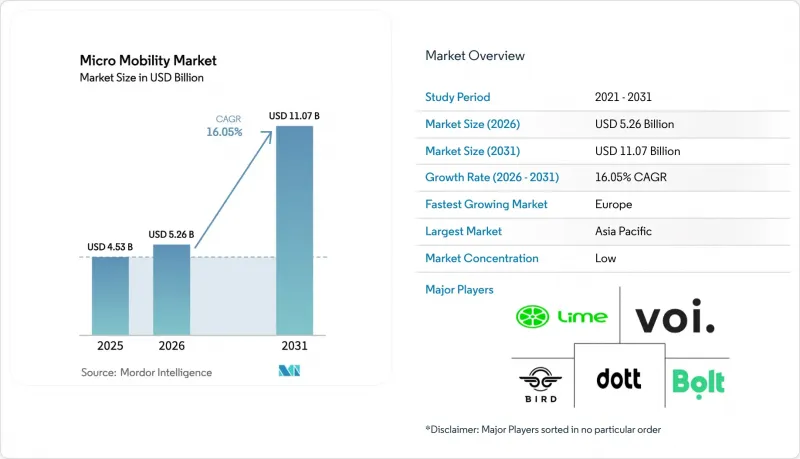

據 Mordor Intelligence 稱,2025 年全球微出行市場價值為 45.3 億美元,預計到 2031 年將達到 110.7 億美元,而 2026 年為 52.6 億美元,預測期(2026-2031 年)的複合年成長率為 16.05%。

本報告按車輛類型(電動滑板車、電動輕型機踏車、電動自行車、電動滑板等)、電池類型(密閉式鉛酸電池、鎳氫電池、鋰離子電池)、電壓(低於24V、36V、48V、高於48V)、共享模式(固定式、無樁式、訂閱式)和地區(北美等)進行細分。市場預測以價值(美元)和銷售(台)兩種形式呈現。

全球微出行市場趨勢與洞察

後疫情時代都市區交通壅塞加劇及交通方式轉變

自2024年以來,預計主要城市的交通密度將增加15%至20%,促使通勤者尋求更多能夠避免擁擠的出行方式。由於人們出於健康原因減少了搭乘公車和火車,微出行市場正在填補由此產生的服務缺口。隨著混合辦公模式的興起改變了高峰時段的交通模式,電動自行車和滑板車等靈活的門到門交通選擇正日益受到關注。混合用途區域的微出行普及率最高,因為一輛車就能滿足通勤、辦事和休閒的所有需求。城市負責人開始將專用車道和停車區域納入總體規劃,這表明當前的出行方式轉變是一種結構性重組,而非臨時應對措施。

鋰離子電池成本的降低延長了續航里程和運作。

全球電池組價格持續下降,使得製造商能夠在不提高零售價格的情況下採用更高容量的48V電池組。中國每年生產超過4500萬輛電動二輪車,形成了無與倫比的規模經濟,並惠及整個微出行市場。現代電池管理系統可將運作延長至八年,並降低整體擁有成本,使共享業者能夠制定盈利的折舊免稅額計劃。電池更換網路起源於亞洲,目前正在向歐洲擴展,它消除了充電停機時間,並為宅配業者和通勤者提供近乎不間斷的服務。

安全法規和車輛分類不一致

速度和功率限制的差異迫使營運商在不同地區部署不同的車輛,阻礙了微出行市場的發展。歐盟委員會正在考慮引入統一的「個人行動裝置」類別以簡化監管,但在美國,電機功率和頭盔要求方面仍然存在顯著差異。紐約市在2019年至2023年間,與電動出行相關的火災損失高達5.2億美元,之後訂定了「第39號地方法律」。這增加了保險的不確定性,推高了保費,並阻礙了風險規避型消費者採用這項技術。

細分市場分析

電動自行車仍是微出行市場的主力軍,預計2025年將佔35.74%的市場。目前,成長重心正轉向貨運車型,以滿足歐洲最後一公里包裹遞送的需求以及新興零排放區的要求,其複合年成長率(CAGR)達到23.65%。零售商和物流公司正轉向採用負載容量160公斤的前裝式貨箱設計,從而減少城市地區的貨車行駛里程。

對於營運商而言,貨運型車輛更受歡迎,因為它們能抵消較高的初始投資成本,而且每輛車的平均日收入比標準自行車高出45%。雖然共享滑板車車隊仍在滿足休閒和出行首公里需求,但隨著營運商最佳化現有網路以提高盈利,其成長速度正在放緩。在亞洲市場,二輪車正逐漸取代汽車成為日常交通工具,而輕型機踏車則填補了出行方面的空白,凸顯了微出行市場的區域差異。

對於尋求幾乎不間斷使用的企業買家而言,電池更換相容性正逐漸成為一項新的採購標準。Yamaha的「Enyring」電動滑板車進入德國和荷蘭市場,顯示歐洲對物流的關注日益提高。相較之下,由於在公共道路上使用電動滑板車的法規核准有限,它仍然是小眾愛好。總而言之,從車輛配置來看,顯然沒有單一平台能夠滿足所有都市區需求;價值的創造來自於滿足有效負載容量、速度和續航里程等特定要求的專用設計。

到2025年,鋰離子電池將佔微出行市場82.65%的佔有率,預計到2031年將以16.62%的複合年成長率成長。這種電池化學系統的高能量密度和不斷下降的成本,使得車輛能夠在不增加重量的情況下實現長途行駛,滿足了通勤者對40-60公里實際續航里程的需求。具備預測分析功能的先進電池管理軟體可將電池組壽命延長至8年,進而降低車隊營運商的折舊免稅額成本。中國的大規模生產支撐著全球供應,而歐洲組裝則透過滿足更嚴格安全標準的強大溫度控管技術,為產品增添了價值。

密閉式鉛酸電池僅用於超低成本產品,因為這些產品的初始成本遠高於其性能,而且隨著二手鋰離子電池組湧入二手市場,其市場佔有率持續萎縮。鎳氫(NiMH)電池仍只佔少數,僅限於一些特殊的工業應用和法規遵循要求。

區域分析

預計到2025年,亞太地區將佔全球微出行市場規模的38.05%。這主要得益於中國預計在2025會計年度將部署4億輛電動二輪車,以及印度預計將售出114萬輛。在中國,平均零售價約為336美元,這為大眾提供了更多擁有電動二輪車的機會。同時,在印度,優惠的商品和服務稅(GST)稅率和國內製造業獎勵正在推動車隊規模的成長。聯合國環境規劃署(UNEP)已向亞洲和非洲的低收入國家津貼1.3億美元,顯示出口車輛和零件的未來成長潛力巨大。

歐洲是成長最快的地區,年複合成長率高達18.1%,這得益於其持續的氣候政策和法規的協調統一。在德國,儘管平均價格有所下降,但2024年電動自行車的銷量仍達205萬輛,佔國內自行車總銷量的53%。營運商正透過合併來實現規模經濟,其中價值1.5億歐元的「Tier-Dott」聯盟尤其引人注目。獲利能力的提升趨勢日益明顯,例如Voi公司累計2024年的息稅折舊攤銷前利潤(EBITDA)將達到1,720萬歐元,該公司利用這筆資金發行了5,000萬歐元的公司債進行債務再融資。隨著城市實施低排放區政策,物流公司為了獲得免稅通行權,加速採用貨運自行車。

在北美,市場正經歷17.72%的複合年成長率,這主要得益於超過5,000萬美元的地方政府採購補貼和4,455萬美元的聯邦政府積極交通津貼。 Lime已連續兩年實現正現金流,並制定了IPO計劃,展現了商業性永續性。此外,與Uber的合作將進一步推動其發展,Uber將從Lime現有的應用程式用戶群中吸引更多用戶。然而,紐約市估計火災相關損失高達5.2億美元,引發了人們對安全的擔憂,也影響了市場情緒。如果能夠推出建設性法規並擴大路邊充電基礎設施,預計市場將進一步擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 疫情後都市區交通壅塞加劇及交通途徑轉變

- 鋰離子電池成本的下降延長了車輛的續航里程和運作時間。

- 市政補貼和臨時基礎設施促進積極出行

- 企業微行程計畫幫助員工達成ESG目標

- 二手輕型電動車二手蓬勃發展,導致入門價格下降。

- 人工智慧驅動的車輛分析可顯著減少運作和成本。

- 市場限制因素

- 安全法規和車輛分類不一致

- 人口密集城區充電和停車位短缺。

- 電池起火事故導致保險費上漲

- 城市層級提高車輛收費和里程稅。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 車輛類型

- 電動滑板車

- 電動輕型輕型機踏車

- 電動自行車

- 電動滑板

- 電動貨運自行車

- 依電池類型

- 密閉式鉛酸電池

- NiMH

- Li-ion

- 透過電壓

- 低於24伏

- 36V

- 48V

- 48伏特或以上

- 透過共享模型

- 碼頭類型

- 無樁型

- 基於訂閱

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 土耳其

- 以色列

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Lime

- Bird Global Inc.

- Tier Mobility

- Dott

- Voi Technology

- Beam Mobility

- Yulu Bikes

- Helbiz

- Superpedestrian

- Spin

- Bolt Technologies

- Neuron Mobility

- Scooterson

- Segway-Ninebot

- NIU Technologies

- Rad Power Bikes

- Cowboy

- Zoomo

- RidePanda

第7章 市場機會與未來展望

According to Mordor Intelligence, the global micro mobility market size was valued at USD 4.53 billion in 2025 and estimated to grow from USD 5.26 billion in 2026 to reach USD 11.07 billion by 2031, at a CAGR of 16.05% during the forecast period (2026-2031).

This report is Segmented by Vehicle Type (Electric Kick Scooters, Electric Mopeds, Electric Bicycles, Electric Skateboards, and More), Battery Type (Sealed Lead Acid, Nimh, and Li-Ion), Voltage (Below 24V, 36V, 48V, and Above 48V), Sharing Model (Docked, Dockless, and Subscription-Based), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Micro Mobility Market Trends and Insights

Rapid Urban Congestion & Post-Pandemic Modal Shift

Traffic density has climbed 15-20% in major cities since 2024, prompting commuters to seek nimble alternatives that bypass gridlock. The micro mobility market now fills service gaps left when riders reduced bus and rail use for health reasons. As hybrid work alters peak-hour patterns, flexible door-to-door modes such as e-bikes and kick scooters gain traction. Mixed-use districts display the highest uptake because a single vehicle can serve commuting, errands, and leisure needs. City planners have begun incorporating protected lanes and parking corrals into master plans, confirming that the current modal shift is a structural realignment rather than a passing response.

Falling Li-ion Battery Costs Lengthening Range & Duty-Cycles

Global battery pack prices keep sliding, letting manufacturers install larger 48 V units without raising retail prices. Chinese output exceeding 45 million electric two-wheelers a year creates unmatched economies of scale that ripple across the micro mobility market. Modern battery-management systems stretch operational life to 8 years, shrinking total cost of ownership and enabling shared-fleet operators to run profitable depreciation schedules. Swapping networks pioneered in Asia and now spreading to Europe, remove charging downtime, delivering quasi-continuous service to couriers and commuters alike.

Patchwork Safety Regulations & Vehicle Classification Gaps

Divergent speed caps and power limits force operators to deploy region-specific fleets, hindering scale in the micro mobility market. The European Commission studies a unified Personal Mobility Device category to streamline rules, while U.S. state laws still vary widely on motor wattage and helmet use. New York City introduced Local Law 39 after e-mobility fire costs reached USD 520 million between 2019-2023. The resulting insurance uncertainty raises premiums and deters risk-averse consumers.

Other drivers and restraints analyzed in the detailed report include:

- Municipal Subsidies & Pop-Up Infrastructure for Active Mobility

- Corporate Micromobility Programs for Employee ESG Targets

- Insufficient Charging / Parking Bays in Dense Downtowns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric bicycles remained the anchor of the micro mobility market size, capturing 35.74% share in 2025. Growth now tilts toward cargo variants that log a 23.65% CAGR by satisfying last-mile parcel demand in Europe and emerging zero-emission zones. Retailers and logistics firms pivot to front-loading box designs capable of 160 kg payloads, cutting van mileage inside city centers.

Operators favor cargo units because average daily revenue per vehicle runs 45% higher than for standard bikes, offsetting their higher capital cost. Shared scooter fleets continue to serve leisure and first-mile needs, yet expansion cools as operators optimize existing networks for profitability. Mopeds fill the mobility gap in Asian markets where two-wheelers replace cars for everyday travel, underscoring regional diversity within the micro mobility market.

Battery-swap compatibility is emerging as a purchase criterion for commercial buyers who target near-continuous utilization. Yamaha's Enyring push into Germany and the Netherlands highlights Europe's growing logistics focus. In contrast, electric skateboards remain a niche pastime with limited regulatory acceptance for street use. Overall, the vehicle mix shows that one platform cannot satisfy every urban task; instead, specialized designs unlock value by matching payload, speed, and range requirements.

Li-ion held 82.65% of the micro mobility market size in 2025 and is on track for a 16.62% CAGR to 2031. The chemistry's high energy density and falling price enable longer trips without weight penalties, aligning with commuter expectations for 40-60 km real-world range. Advanced battery-management software featuring predictive analytics now extends pack life to 8 years, lowering per-ride depreciation for fleet operators. Manufacturing scale in China supports global supply, while European assemblers add value with robust thermal management to meet stricter safety codes.

Sealed lead-acid persists only in ultra-budget offerings where upfront price outweighs performance, yet its share continues to erode as second-hand Li-ion packs enter the resale market. NiMH remains marginal, restricted to specialized industrial carts or compliance-driven procurement.

Complete Report Scope:

- By Vehicle Type

- Electric Kick Scooters

- Electric Mopeds

- Electric Bicycles

- Electric Skateboards

- Electric Cargo Bikes

- By Battery Type

- Sealed Lead Acid

- NiMH

- Li-ion

- By Voltage

- Below 24V

- 36V

- 48V

- Above 48V

- By Sharing Model

- Docked

- Dockless

- Subscription-based

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East & Africa

- Middle East

- United Arab Emirates

- Turkey

- Israel

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific accounted for 38.05% of the micro mobility market size in 2025, buoyed by China's installed base of 400 million electric two-wheelers and India's 1.14 million unit sales in FY2025. Average retail prices near USD 336 in China open ownership to mass segments, while India's fleet scales on favorable GST rates and domestic manufacturing incentives. The United Nations Environment Programme directs USD 130 million in grants to lower-income Asian and African nations, signaling future upside for exported vehicles and components.

Europe, the fastest-growing region at 18.1% CAGR, benefits from cohesive climate policy and advancing regulatory harmonization. Germany sold 2.05 million e-bikes in 2024, representing 53% of domestic bicycle volume even as average prices dipped. Operators amalgamate to chase scale economies, most notably the Tier-Dott union worth EUR 150 million. Profit focus intensifies, illustrated by Voi's EUR 17.2 million EBITDA in 2024 and debt refinancing via a EUR 50 million bond. As cities enforce low-emission zones, cargo bikes accelerate adoption by logistics firms seeking tariff-free access.

North America posts a 17.72% CAGR on the back of more than USD 50 million in local purchase subsidies and USD 44.55 million in federal active-transport grants. Lime shows commercial viability with two straight years of positive cash flow and an IPO roadmap, backed by an Uber partnership that funnels riders from an established app user base. Yet safety fears weigh on sentiment after New York City quantified USD 520 million in fire-related costs. Pending constructive rules and expanding curbside charging stand to unlock further market depth.

- Lime

- Bird Global Inc.

- Tier Mobility

- Dott

- Voi Technology

- Beam Mobility

- Yulu Bikes

- Helbiz

- Superpedestrian

- Spin

- Bolt Technologies

- Neuron Mobility

- Scooterson

- Segway-Ninebot

- NIU Technologies

- Rad Power Bikes

- Cowboy

- Zoomo

- RidePanda

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urban congestion & post-pandemic modal shift

- 4.2.2 Falling Li-ion battery costs lengthening range & duty-cycles

- 4.2.3 Municipal subsidies & pop-up infrastructure for active mobility

- 4.2.4 Corporate micromobility programs for employee ESG targets

- 4.2.5 Booming secondary market for used LEVs lowering entry price

- 4.2.6 AI-driven fleet analytics slashing operating downtime & cost

- 4.3 Market Restraints

- 4.3.1 Patchwork safety regulations & vehicle classification gaps

- 4.3.2 Insufficient charging / parking bays in dense downtowns

- 4.3.3 Rising insurance premiums following battery-fire incidents

- 4.3.4 Escalating city-level per-vehicle fees & trip taxes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Electric Kick Scooters

- 5.1.2 Electric Mopeds

- 5.1.3 Electric Bicycles

- 5.1.4 Electric Skateboards

- 5.1.5 Electric Cargo Bikes

- 5.2 By Battery Type

- 5.2.1 Sealed Lead Acid

- 5.2.2 NiMH

- 5.2.3 Li-ion

- 5.3 By Voltage

- 5.3.1 Below 24V

- 5.3.2 36V

- 5.3.3 48V

- 5.3.4 Above 48V

- 5.4 By Sharing Model

- 5.4.1 Docked

- 5.4.2 Dockless

- 5.4.3 Subscription-based

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Saudi Arabia

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Lime

- 6.4.2 Bird Global Inc.

- 6.4.3 Tier Mobility

- 6.4.4 Dott

- 6.4.5 Voi Technology

- 6.4.6 Beam Mobility

- 6.4.7 Yulu Bikes

- 6.4.8 Helbiz

- 6.4.9 Superpedestrian

- 6.4.10 Spin

- 6.4.11 Bolt Technologies

- 6.4.12 Neuron Mobility

- 6.4.13 Scooterson

- 6.4.14 Segway-Ninebot

- 6.4.15 NIU Technologies

- 6.4.16 Rad Power Bikes

- 6.4.17 Cowboy

- 6.4.18 Zoomo

- 6.4.19 RidePanda

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球微出行市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球微出行市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 微出行充電基礎設施市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、安裝模式、解決方案

微出行充電基礎設施市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、安裝模式、解決方案 城市自行車共享和微出行租賃市場預測—全球車輛類型、驅動系統、共享模式、服務類型、應用、最終用戶和地區分析—2034年

城市自行車共享和微出行租賃市場預測—全球車輛類型、驅動系統、共享模式、服務類型、應用、最終用戶和地區分析—2034年 微出行市場規模、佔有率和趨勢分析報告:按車輛類型、電池類型、電壓、地區和細分市場分類的預測(2026-2033 年)

微出行市場規模、佔有率和趨勢分析報告:按車輛類型、電池類型、電壓、地區和細分市場分類的預測(2026-2033 年) 微出行市場規模、佔有率、趨勢和預測:按類型、推進類型、共享類型、速度、年齡層、所有權類型和地區分類,2026-2034 年

微出行市場規模、佔有率、趨勢和預測:按類型、推進類型、共享類型、速度、年齡層、所有權類型和地區分類,2026-2034 年 2026年全球微出行充電基礎設施市場報告2026年全球微行程市場報告

2026年全球微出行充電基礎設施市場報告2026年全球微行程市場報告 微出行充電基礎設施市場:按組件、車輛類型、充電器類型、功率容量、整合類型、應用和最終用戶分類-2026-2032年全球市場預測微出行市場:2026-2030年全球市場預測(按車輛類型、推進系統、引擎排氣量、內燃機類型、所有權狀態、銷售管道和最終用戶分類)微行程市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、最終使用者、模式、部署類型及解決方案分類

微出行充電基礎設施市場:按組件、車輛類型、充電器類型、功率容量、整合類型、應用和最終用戶分類-2026-2032年全球市場預測微出行市場:2026-2030年全球市場預測(按車輛類型、推進系統、引擎排氣量、內燃機類型、所有權狀態、銷售管道和最終用戶分類)微行程市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、最終使用者、模式、部署類型及解決方案分類