|

市場調查報告書

商品編碼

2073351

印度計程車市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)India Taxi - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

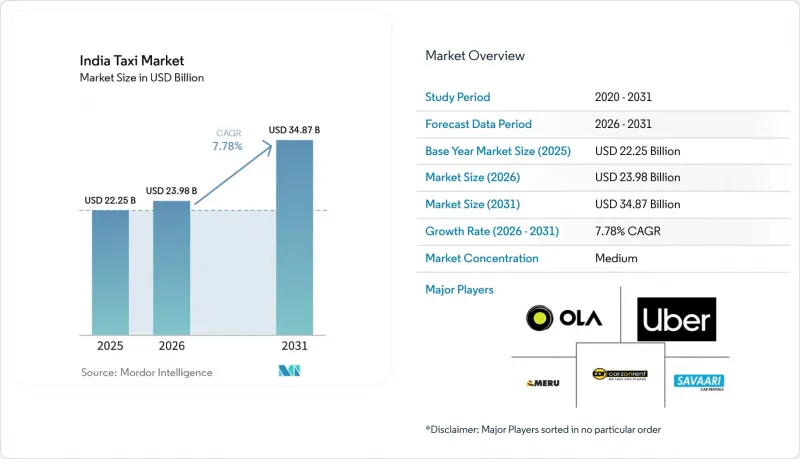

根據 Mordor Intelligence 估計,印度計程車市場在 2026 年的價值將達到 239.8 億美元,高於 2025 年的 222.5 億美元,預計到 2031 年將達到 348.7 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 7.78%。

本報告按預訂類型(線上和線下預訂)、服務類型(叫車、共乘/順風車等)、車輛類型(乘用車等)、動力類型(內燃機、電動、混合動力)、出行目的(市內點對點等)以及客戶群(個人消費者、企業/機構)進行細分。市場預測以美元計價。

印度計程車市場的趨勢和洞察

智慧型手機普及率和相容UPI的數位支付

2024年,UPI交易量大幅成長,幾乎是去年年增率的兩倍。這顯示計程車用戶的支付方式正在發生永久性的轉變。數百萬智慧型手機用戶已經開始使用叫車應用程式,這不僅減少了對現金的依賴,還擴大了二、三線城市的目標客戶群。公共交通也呈現類似的成長趨勢,例如班加羅爾城市交通公司(BMTC)在2025年3月前實現了近五分之二的票價收入透過電子方式收取。各個平台都在進行調整,例如,有的試點只接受現金支付的自動人力車服務,同時保留應用程式內的配對功能,這表明數位化接觸並不一定意味著數位化支付。生物識別和信用卡綁定的UPI等創新技術進一步提升了安全性,企業帳戶也被鼓勵在一個統一的控制面板上集中管理商務旅行費用。因此,印度計程車市場正經歷更順暢的預訂流程和更高的回頭客率。

都市區擁擠和私家車擁有率低於2%

汽車擁有率仍然很低,城市中心每天都面臨阻礙生產力的交通堵塞。二、三線城市已經創造了全國五分之三的GDP,人口密度也飆升,這凸顯了印度計程車市場對共享出行的長期依賴。 UDAN區域機場計畫開通了625條航線,運送了大量乘客,立即催生了「最後一公里」計程車需求。像Ecos Mobility這樣的輕資產企業出行服務提供商為1100家公司運營著12000輛汽車,這表明基於訂閱的車隊模式作為一種緩解交通堵塞的策略是有效的。靈活的工作安排將高峰行程時間分散到一天中,從而可以動態分配車輛,在提高車輛運轉率的同時,平衡交通負荷。

費用和額外費用上限

監管上限將佣金限制在車費的五分之一,額外費用限制在車費的兩倍,從而壓縮了尖峰時段的利潤空間。駕駛人工會認為,佣金率實際上仍維持在正常水平的近一半,這導致2025年德里爆發了大規模抗議活動,並造成服務中斷。在馬哈拉斯特拉邦,現在對司機徵收最低取消費,而乘客取消費則設定在車費的十分之一以下,地方交通管理部門正在進行審計,以遏制偷漏費行為。由於難以將不斷上漲的燃油價格轉嫁到車費上,業者正在轉向固定費率的訂閱模式,以在遵守上限規定的同時穩定司機的收入。雖然這些變化可能會減緩短期利潤率的成長,但它們很可能有助於提高客戶維繫,並促進印度計程車市場的長期成長。

細分市場分析

到2025年,線上預訂將佔印度計程車市場70.84%的佔有率,預計到2031年將以7.80%的複合年成長率成長。線下叫車仍佔約30%的佔有率,但隨著智慧型手機在二線城市普及率的提高,其佔有率持續下降。由於乘客和司機使用UPI支付均免手續費,預計印度計程車市場在線預訂的市場規模將逐年成長。

開放數位商務網路 (ONDC) 的夥伴關係使 Namma Yatri 等平台能夠轉型為訂閱模式,將車費直接委託給乘客和駕駛人,從而在保持應用可見性的同時降低聚合平台費用。新的 Sahkar Taxi 計畫下的合作社進一步降低了中階的利潤,但仍依賴於市場定義的「數位預訂」應用程式介面。儘管監管指南尚未統一數據共用協議,但普及數位化的趨勢正在鞏固。

預計到 2025 年,叫車將佔印度計程車市場收入的 65.10%,而到 2031 年,共乘和順風車的複合年成長率預計將達到 7.98%。對價格敏感的通勤者在尖峰時段時段會選擇共用,因為車費上限降低了共乘與單程乘車的價格差異。

馬哈拉斯特拉邦拉邦的法規正式製定了共乘安全標準,這增強了女性用戶的安全感,並有助於維持共享平台的用戶忠誠度。對於需要在混合辦公模式下提供「最後一公里」接駁服務的雇主而言,企業租賃和訂閱式車隊可以提供可預測的月度成本。在交通堵塞持續加劇的情況下,公共政策鼓勵增加每輛車的載客量,而共乘在印度計程車市場的成長速度也開始超過叫車。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧型手機普及率和相容UPI的數位支付

- 都市區交通擁擠和私家車擁有率低於2%

- 政府促進電動車發展的政策(FAME II、各州電動車政策)

- 機場客流量激增帶動了預訂共乘服務的發展。

- 三級艦隊模式的合作/擴展

- 人工智慧驅動的交通行動服務(MaaS) 整合

- 市場限制因素

- 費用和額外費用上限(2020 年 MV 聚合器規則)

- 電動車總擁有成本高以及資金籌措缺口

- 乘客安全問題和司機離崗

- 印度各邦法規存在差異

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按預訂類型

- 線上預訂

- 線下預訂

- 按服務類型

- 叫車

- 共乘/順風車

- 訂閱和企業租賃

- 車輛類型

- 搭乘用車

- 摩托車

- 三輪自動人力車

- 廂型車和多用途汽車

- 依推進類型

- 內燃機(汽油/柴油/壓縮天然氣)

- 電的

- 混合

- 按運動目的

- 城市點對點

- 機場接送

- 長途旅行/城際旅行

- 商務流動性

- 按客戶細分

- 個人消費者

- 公司和組織

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ANI Technologies Pvt Ltd(Ola Cabs)

- Uber Technologies Inc.

- Rapido

- Meru Mobility Tech Pvt Ltd

- BluSmart Mobility Pvt Ltd

- Carzonrent India Pvt Ltd

- NTL FastTrack Taxi

- Savaari Car Rentals

- inDrive

- Spice Cabs

- Mega Cabs

- BlaBlaCar

- Evera Cabs

- Jugnoo

- Zoomcar India Pvt Ltd

- TaxiForSure

- Bounce Infinity

- Yulu Bikes

- Sahkar Taxi(Co-operative)

第7章 市場機會與未來展望

According to Mordor Intelligence, india taxi market size in 2026 is estimated at USD 23.98 billion, growing from 2025 value of USD 22.25 billion with 2031 projections showing USD 34.87 billion, growing at 7.78% CAGR over 2026-2031.

This report is Segmented by Booking Type (Online Booking and Offline Booking), Service Type (Ride-Hailing, Ride-Sharing/Car-Pooling, and More), Vehicle Type (Passenger Cars and More), Propulsion Type (ICE, Electric, and Hybrid), Trip Purpose (Intra-City Point-To-Point and More), and Customer Segment (Individual Consumers, Corporate/Institutional). The Market Forecasts are Provided in Terms of Value (USD).

India Taxi Market Trends and Insights

Smartphone Penetration & UPI-Enabled Digital Payments

UPI transaction volume grew exponentially in 2024, almost double the previous year's annual rise, which signals a permanent behavioral change in how riders pay for taxis. Millions of smartphone users already access ride apps, lowering cash dependence and enlarging target customer pools in tier-2 and tier-3 cities. Public transport systems mirror the adoption curve, as shown by Bangalore Metropolitan Transport Corporation collecting almost two-fifth of ticket revenue digitally in March 2025. Platforms adapt by piloting cash-only auto-rickshaw services that still employ in-app matching, confirming that digital contact does not always equal digital settlement. Biometric authentication and credit-linked UPI innovations further tighten security, encouraging corporate accounts to centralize travel spend under a single dashboard. As a result, the Indian taxi market leverages smoother booking funnels and better repeat ride conversion.

Urban Congestion & Less than 2% Private Car Ownership

Private car penetration remains minimal, and urban cores face daily congestion that stifles productivity. Tier-2 and tier-3 cities already generate three-fifths of GDP, see population densities soar, underpinning long-run dependence on shared mobility in the India taxi market. The UDAN regional airport scheme activated 625 routes serving multiple passengers, creating immediate last-mile taxi needs. Asset-light corporate mobility providers such as Ecos Mobility run 12,000 vehicles for 1,100 enterprises, validating subscription fleets as congestion countermeasures. Flexible work setups widen travel peaks across the day, so dynamic fleet allocation helps operators lift utilization while smoothing traffic loads

Commission & Surge-Price Caps

Regulatory ceilings restrict commissions to one-fifth of fare and limit surge multipliers to 2X, trimming peak-hour revenue potential. Driver associations claim that take rates nearly half persist in practice, leading to protests across Delhi in 2025 that disrupted service availability. Maharashtra now enforces minimal cancellation penalties on drivers and less than one-tenth on riders, applying Regional Transport Authority audits to contain side payments. With lower elasticity to pass through fuel spikes, operators pivot toward fixed-fee subscriptions that comply with caps yet stabilize driver income. Such shifts may blunt near-term margin expansion but could lift retention and support long-term growth in the India taxi market over time.

Other drivers and restraints analyzed in the detailed report include:

- Government EV Push (FAME-II and State Policies)

- Airport Traffic Boom Powering Pre-Scheduled Rides

- Rider Safety Issues & Driver Attrition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online reservations accounted for 70.84% of the Indian taxi market in 2025 and are projected to expand at a 7.80% CAGR through 2031. Offline hail retains almost three-tenth, but its share keeps falling as smartphone literacy spreads in tier-2 corridors. The Taxi market in india size associated with online booking is poised to widen yearly because payments over UPI remain fee-free for riders and drivers.

The Open Network for Digital Commerce partnership lets platforms like Namma Yatri migrate toward subscription models that directly leave fare collections to riders and drivers, cutting aggregator commissions while preserving app visibility. Cooperatives under the new Sahkar Taxi program further shrink the middle-layer margin, though they still rely on app interfaces classified as digital booking in market definitions. Regulatory guidance is yet to harmonize data-sharing protocols, but the trajectory toward universal digital engagement appears locked in.

Ride-hailing produced 65.10% of the Indian taxi market revenue in 2025, while ride-sharing and car-pooling are expected to clock an 7.98% CAGR to 2031. Price-sensitive commuters choose shared trips during peak pricing windows because caps narrow the differential to solo rides.

State rules in Maharashtra formalize car-pool safety norms that boost female ridership confidence, helping share platforms retain loyalty. Corporate leasing and subscription fleets supply predictable monthly spend for employers that need last-mile shuttles in hybrid work models. As congestion continues, public policy encourages higher occupancy per vehicle, positioning ride-sharing to edge ride-hailing growth in the Indian taxi market.

Complete Report Scope:

- By Booking Type

- Online Booking

- Offline Booking

- By Service Type

- Ride-Hailing

- Ride-Sharing / Car-Pooling

- Subscription & Corporate Leasing

- By Vehicle Type

- Passenger Cars

- Two-Wheelers

- Three-Wheeler Auto-Rickshaws

- Vans & MPVs

- By Propulsion Type

- ICE (Petrol/Diesel/CNG)

- Electric

- Hybrid

- By Trip Purpose

- Intra-city Point-to-Point

- Airport Transfers

- Outstation / Inter-city

- Corporate Mobility

- By Customer Segment

- Individual Consumers

- Corporate / Institutional

List of Companies Covered in this Report:

- ANI Technologies Pvt Ltd (Ola Cabs)

- Uber Technologies Inc.

- Rapido

- Meru Mobility Tech Pvt Ltd

- BlUSmart Mobility Pvt Ltd

- Carzonrent India Pvt Ltd

- NTL FastTrack Taxi

- Savaari Car Rentals

- inDrive

- Spice Cabs

- Mega Cabs

- BlaBlaCar

- Evera Cabs

- Jugnoo

- Zoomcar India Pvt Ltd

- TaxiForSure

- Bounce Infinity

- Yulu Bikes

- Sahkar Taxi (Co-operative)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone Penetration & UPI-Enabled Digital Payments

- 4.2.2 Urban Congestion & Less than 2 % Private Car Ownership

- 4.2.3 Government EV Push (Fame-Ii, State EV Policies)

- 4.2.4 Airport Traffic Boom Powering Pre-Scheduled Rides

- 4.2.5 Cooperative/Tier-III Fleet Model Expansion

- 4.2.6 AI-Based Mobility-As-A-Service (Maas) Integrations

- 4.3 Market Restraints

- 4.3.1 Commission & Surge-Price Caps (MV Aggregator Rules 2020)

- 4.3.2 High EV Total-Cost-of-Ownership & Financing Gaps

- 4.3.3 Rider-Safety Issues & Driver Attrition

- 4.3.4 Regulatory Fragmentation Across Indian States

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Type

- 5.1.1 Online Booking

- 5.1.2 Offline Booking

- 5.2 By Service Type

- 5.2.1 Ride-Hailing

- 5.2.2 Ride-Sharing / Car-Pooling

- 5.2.3 Subscription & Corporate Leasing

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Two-Wheelers

- 5.3.3 Three-Wheeler Auto-Rickshaws

- 5.3.4 Vans & MPVs

- 5.4 By Propulsion Type

- 5.4.1 ICE (Petrol/Diesel/CNG)

- 5.4.2 Electric

- 5.4.3 Hybrid

- 5.5 By Trip Purpose

- 5.5.1 Intra-city Point-to-Point

- 5.5.2 Airport Transfers

- 5.5.3 Outstation / Inter-city

- 5.5.4 Corporate Mobility

- 5.6 By Customer Segment

- 5.6.1 Individual Consumers

- 5.6.2 Corporate / Institutional

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 ANI Technologies Pvt Ltd (Ola Cabs)

- 6.4.2 Uber Technologies Inc.

- 6.4.3 Rapido

- 6.4.4 Meru Mobility Tech Pvt Ltd

- 6.4.5 BluSmart Mobility Pvt Ltd

- 6.4.6 Carzonrent India Pvt Ltd

- 6.4.7 NTL FastTrack Taxi

- 6.4.8 Savaari Car Rentals

- 6.4.9 inDrive

- 6.4.10 Spice Cabs

- 6.4.11 Mega Cabs

- 6.4.12 BlaBlaCar

- 6.4.13 Evera Cabs

- 6.4.14 Jugnoo

- 6.4.15 Zoomcar India Pvt Ltd

- 6.4.16 TaxiForSure

- 6.4.17 Bounce Infinity

- 6.4.18 Yulu Bikes

- 6.4.19 Sahkar Taxi (Co-operative)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

摩托計程車市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、按應用類型、按地區和競爭對手分類,2021-2031年

摩托計程車市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、按應用類型、按地區和競爭對手分類,2021-2031年 新能源計程車市場:2026-2032年全球市場預測(依動力傳動系統、充電方式、電池容量及續航里程分類)計程車服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、行駛里程、預約平台及客戶群分類)摩托車計程車服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、使用時間、客戶群和應用程式分類)摩托車計程車服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、服務時長、車款及使用者類型分類)

新能源計程車市場:2026-2032年全球市場預測(依動力傳動系統、充電方式、電池容量及續航里程分類)計程車服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、行駛里程、預約平台及客戶群分類)摩托車計程車服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、使用時間、客戶群和應用程式分類)摩托車計程車服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、服務時長、車款及使用者類型分類) 2026年全球線上計程車服務市場報告2026年全球計程車和豪華轎車服務市場報告2026年全球計程車服務市場報告豪華轎車服務市場:2026-2032年全球市場預測(依服務類型、時間長度、車輛燃料類型、車輛類型、最終用戶和預訂方式分類)計程車和豪華轎車服務市場:按類型、服務時間、服務模式、距離和車輛類型分類-2026-2032年全球市場預測

2026年全球線上計程車服務市場報告2026年全球計程車和豪華轎車服務市場報告2026年全球計程車服務市場報告豪華轎車服務市場:2026-2032年全球市場預測(依服務類型、時間長度、車輛燃料類型、車輛類型、最終用戶和預訂方式分類)計程車和豪華轎車服務市場:按類型、服務時間、服務模式、距離和車輛類型分類-2026-2032年全球市場預測