|

市場調查報告書

商品編碼

2073321

非洲飼料酸化劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Africa Feed Acidifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

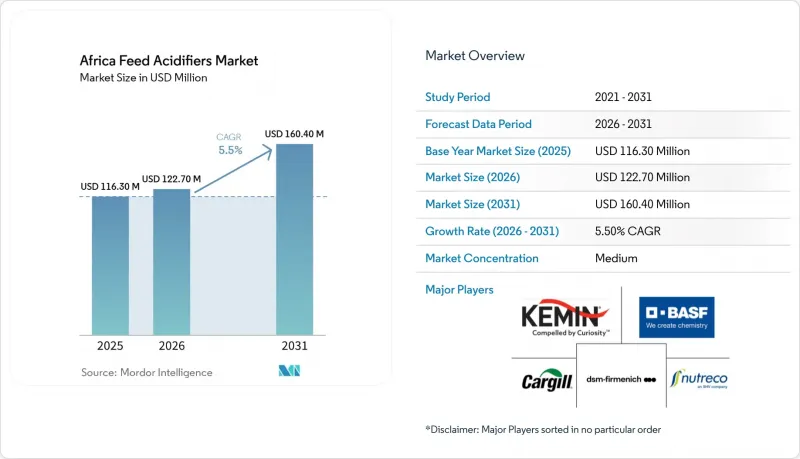

根據 Mordor Intelligence 預測,非洲飼料酸化劑市場規模將從 2025 年的 1.163 億美元成長到 2026 年的 1.227 億美元,然後在 2031 年達到 1.604 億美元,2026 年至 2031 年的複合年成長率為 5.5%。

本報告按產品類型(丙酸、甲酸、富馬酸及其他酸化劑)、目標動物(家禽、豬、反芻動物、水產養殖及其他)及地區(南非、埃及、奈及利亞、肯亞及非洲其他地區)進行細分。市場預測以價值(美元)和數量(公噸)呈現。

非洲飼料酸化劑市場趨勢與洞察。

高溫高濕儲存環境下對飼料衛生日益成長的需求。

非洲飼料酸化劑市場與氣候密切相關。非洲大陸大部分地區屬於熱帶和亞熱帶氣候,這種氣候條件有利於飼料在儲存過程中微生物的生長。高溫高濕的環境會迅速降低飼料的穩定性,尤其是在儲存管理不善和運輸時間過長的情況下。 2024年發表在《農業》(Agriculture)雜誌上的一項科學研究表明,甲酸和丙酸可以降低受污染的複合飼料中的沙門氏菌含量,這表明酸性添加劑在保鮮和病原體控制方面發揮著雙重作用。BASF SE)也針對高溫高濕環境推出了丙酸產品,例如“Lupro-Cid”,包括用於提高飼料廠操作安全性的緩衝配方。這些氣候壓力、微生物風險和產品功能共同造就了非洲飼料酸化劑市場穩定的需求基礎,與其他許多飼料添加劑類別相比,該市場對短期趨勢的依賴性較低。

非洲商業家禽生產的擴張

商業家禽生產的擴張持續支撐著非洲對飼料酸化劑的需求。這是因為大規模養殖需要穩定的飼料品質和更強的疾病控制。經濟合作暨發展組織(OECD)和聯合國糧食及農業組織(FAO)預測,非洲雞肉產量將從2020-2022年的670萬噸增加到2032年的870萬噸,這意味著飼料添加劑的需求基礎將長期擴大。據美國農業部(USDA)稱,南非已將其家禽加工能力從2023年的每週1900萬隻恢復到2024年7月的每週2260萬只,這表明商業體系的重組和飼料需求的恢復速度非常快。奈及利亞也已批准了2025年的畜牧業改革議程,將飼料和牧場發展與更廣泛的畜牧業現代化聯繫起來。隨著商業性集約化程度的提高,需求越來越受到來自一體化生產商的系統性採購的驅動,而不是小規模農場通路不規則的採購週期。

中小飼料生產商的價格容忍度極限

除了飼料體系最發達的地區外,非洲飼料酸化劑市場仍面臨巨大的價格障礙。南非和埃及以外的許多飼料廠小規模,服務於對價格敏感的農民網路,幾乎沒有空間將額外成本轉嫁給客戶。根據《衛報奈及利亞版》(2026年2月)報道,在奈及利亞,蛋飼料的交易價格為每25公斤15,000至17,000奈拉(約合10至11美元),奈及利亞家禽協會敦促飼料廠根據穀物價格的下降來降低價格,而不是增加新的成本因素。鑑於買家仍將酸性添加劑視為可有可無而非必需品,這些價格壓力使得酸性添加劑的推廣更加困難。從長遠來看,像烏干達2024年《動物飼料法》這樣的正式品質標準有助於將非洲飼料酸化劑市場從“自願購買模式”轉變為“最低合規模式”,但這種轉變在許多國家仍然不均衡。

細分市場分析

丙酸是最大的產品類型,預計到2025年將佔非洲飼料酸化劑市場39.2%的佔有率。其主導地位源自於其在穀物儲存、複合飼料保藏以及溫貯條件下青貯飼料應用中強大的抗真菌和抗菌性能。在非洲飼料酸化劑市場,這種化學物質長期以來一直是南非商業家禽養殖系統的首選。在南非,供應商提供緩衝型且易於操作的配方,供飼料廠日常使用。BASF公司透過「Luprosil」和「Lupro-Cid」等產品鞏固了這一地位,這些產品也包含丙酸和甲酸的混合物,專為高溫環境下的儲存和實際操作而設計。甲酸仍然是第二大產品類別,而乳酸、乙酸、山梨酸、檸檬酸和客製化的多元酸混合物則發揮更專業的作用,例如控制腸道pH值、飲用水處理、保藏和螯合支持。

富馬酸是成長最快的飼料酸化劑產品類型,預計2026年至2031年間,其在非洲飼料酸化劑市場的複合年成長率將達到7.8%。這一趨勢對肯亞的酪農系統和南非的育肥場運作具有重大意義,因為這些地區的生產者正面臨著透過提高投入效率來提升生產力的壓力。非洲飼料酸化劑市場也正在經歷從單一酸產品向多酸體系的廣泛轉變,後者旨在透過單一配方實現飼料衛生、腸道健康和操作安全性。 Perstorp Holding AB正透過提供酯化和熱穩定性解決方案的技術指導來強調這一方向,這將推動市場向更複雜的混合物轉型,以應對日益嚴苛的營運條件。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高溫高濕儲存環境下對飼料衛生日益成長的需求。

- 非洲商業家禽生產的擴張

- 在飼料成本飆升的壓力下,人們越來越關注飼料轉換效率。

- 擴大畜禽飼料中非抗生素飼料添加劑的使用

- 對飼料和飲用水系統中病原體控制的需求日益成長

- 擴大酸性添加劑的使用範圍,以提高本地食材的消化率

- 市場限制因素

- 中小飼料生產商的價格容忍範圍較窄

- 對內容和產品選擇的技術理解有差異

- 部分市場存在分銷通路分散和倉儲管理不善的問題。

- 進口原料供應狀況和成本的波動

- 技術展望

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 甲酸

- 丙酸

- 乳酸

- 其他有機酸化劑

- 動物

- 水產養殖

- 魚

- 蝦

- 其他養殖物種

- 家禽

- 肉雞

- 產蛋母雞

- 其他家禽

- 反芻動物

- 牛

- 牛

- 其他反芻動物

- 豬

- 其他動物

- 水產養殖

- 國家

- 南非

- 埃及

- 奈及利亞

- 肯亞

- 其他非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Cargill, Incorporated

- DSM-Firmenich

- Kemin Industries, Inc.

- Adisseo Group

- Nutreco(SHV Holdings)

- Novus International, Inc.

- Archer Daniel Midland Company

- Perstorp Holding AB

- Alltech, Inc.

- Impextraco NV

- Lallemand Inc.

- Vetagro SpA

- CID LINES

- Phibro Animal Health Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the africa feed acidifiers market size is projected to grow from USD 116.3 million in 2025 to USD 122.7 million in 2026 and is forecasted to reach USD 160.4 million by 2031 at 5.5% CAGR over 2026-2031.

This report is Segmented by Product Type (Propionic, Formic, Fumaric, and Other Acidifiers), by Animal (Poultry, Swine, Ruminants, Aquaculture, and Others), and by Geography (South Africa, Egypt, Nigeria, Kenya, and the Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Africa Feed Acidifiers Market Trends and Insights

Rising Need for Feed Hygiene in Hot and Humid Storage Conditions

The African feed acidifiers market is closely tied to climate, as much of the continent operates under tropical and subtropical conditions that accelerate microbial growth in stored feed. High ambient temperatures and elevated humidity can quickly reduce feed stability, especially when storage discipline is weak and transport times are long. Scientific work published in 2024 in Agriculture showed that formic acid and propionic acid can reduce Salmonella load in contaminated compound feed, giving acidifiers a dual role in preservation and pathogen management. BASF SE also positions propionic acids, such as Lupro-Cid, for high-temperature and high-moisture conditions, including buffered formats that improve handling safety for feed mills. This combination of climate stress, microbial risk, and product functionality gives the Africa feed acidifiers market a stable demand base that is less dependent on short-term producer sentiment than many other feed additive categories.

Expansion of Commercial Poultry Production Across Africa

Commercial poultry expansion continues to support demand for feed acidifiers across Africa, as larger flocks require consistent feed quality and stronger disease control. The Organization for Economic Co-operation and Development and the Food and Agriculture Organization of the United Nations (OECD-FAO) projected African poultry meat output to rise from 6.7 million metric tons in 2020-2022 to 8.7 million metric tons by 2032, suggesting a larger long-term feed base for additive use. According to the United States Department of Agriculture (USDA), South Africa had already restored weekly poultry processing capacity to 22.6 million birds by July 2024, up from 19 million in 2023, demonstrating how quickly commercial systems can rebuild and resume feed demand. Nigeria also endorsed a livestock reform agenda in 2025 and linked feed and fodder development to broader sector modernization. As commercial density rises, demand becomes increasingly influenced by structured procurement from integrated producers rather than by irregular buying cycles in smallholder channels.

Limited Price Tolerance Among Small and Mid-Sized Feed Manufacturers

The Africa feed acidifiers market still faces a clear affordability barrier outside the most developed feed systems. Many mills outside South Africa and Egypt operate on a smaller scale, serve price-sensitive farmer networks, and have little room to pass additional costs through to customers. In Nigeria, layer feed trades at NGN 15,000 to NGN 17,000 per 25 kg bag, equivalent to approximately USD 10 to USD 11, according to The Guardian Nigeria (February 2026), and the Poultry Association of Nigeria is urging millers to lower prices in line with softer grain costs rather than add new cost layers. That kind of pricing pressure makes it harder to adopt acidifiers when buyers still view these products as optional rather than essential. Over time, formal quality rules such as Uganda's Animal Feeds Act 2024 can help shift the Africa feed acidifiers market from a discretionary purchase model toward a minimum compliance model, but that transition is still uneven across many countries.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Non-Antibiotic Feed Additives in Livestock Nutrition

- Rising Demand for Pathogen Control in Feed and Drinking Water Systems

- Volatile Availability and Cost of Imported Raw Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Propionic acid was the largest product type, accounted for 39.2% of the Africa feed acidifiers market share in 2025. Its leading position reflects strong antifungal and antibacterial performance in grain storage, compound feed preservation, and silage use under warm storage conditions. The Africa feed acidifiers market has long favored this chemistry in South Africa's commercial poultry systems, where suppliers offer buffered and easier-to-handle formulations for routine mill use. BASF SE supports this position through products such as Luprosil and Lupro-Cid, including combinations of propionic acid and formic acid designed for high-ambient-temperature storage and practical handling. Formic acid remained the next major product group, while lactic acid, acetic acid, sorbic acid, citric acid, and custom multi-acid blends served more specialized roles in gut pH control, drinking water treatment, preservation, and chelation support.

Fumaric acid was the fastest product type, with a projected 7.8% CAGR during 2026-2031 in the Africa feed acidifiers market. That profile is relevant for Kenya's dairy systems and for South Africa's feedlot operations, where producers are under pressure to improve performance with better input efficiency. The Africa feed acidifiers market is also seeing a wider shift from single-acid products to multi-acid systems that aim to combine feed hygiene, gut health, and handling safety in one formulation. Perstorp Holding AB highlighted this direction through technical guidance on esterified and heat-stable solutions, which supports the move toward more advanced blends in markets with tougher operating conditions.

Complete Report Scope:

- By Product Type

- Formic Acid

- Propionic Acid

- Lactic Acid

- Other Organic Acidifiers

- By Animal

- Aquaculture

- Fish

- Shrimp

- Other Aquaculture Species

- Poultry

- Broiler

- Layer

- Other Poultry Birds

- Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- Swine

- Other Animals

- Aquaculture

- By Country

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

List of Companies Covered in this Report:

- BASF SE

- Cargill, Incorporated

- DSM-Firmenich

- Kemin Industries, Inc.

- Adisseo Group

- Nutreco (SHV Holdings)

- Novus International, Inc.

- Archer Daniel Midland Company

- Perstorp Holding AB

- Alltech, Inc.

- Impextraco NV

- Lallemand Inc.

- Vetagro S.p.A.

- CID LINES

- Phibro Animal Health Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Feed Hygiene in Hot and Humid Storage Conditions

- 4.2.2 Expansion of Commercial Poultry Production Across Africa

- 4.2.3 Greater Focus on Feed Conversion Efficiency Under High Feed Cost Pressure

- 4.2.4 Increasing Adoption of Non-Antibiotic Feed Additives in Livestock Nutrition

- 4.2.5 Rising Demand for Pathogen Control in Feed and Drinking Water Systems

- 4.2.6 Growing Use of Acidifiers to Improve Local Ingredient Digestibility

- 4.3 Market Restraints

- 4.3.1 Limited Price Tolerance Among Small and Mid-Sized Feed Manufacturers

- 4.3.2 Uneven Technical Awareness of Inclusion Rates and Product Selection

- 4.3.3 Fragmented Distribution and Limited Storage Discipline in Some Markets

- 4.3.4 Volatile Availability and Cost of Imported Raw Materials

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Formic Acid

- 5.1.2 Propionic Acid

- 5.1.3 Lactic Acid

- 5.1.4 Other Organic Acidifiers

- 5.2 By Animal

- 5.2.1 Aquaculture

- 5.2.1.1 Fish

- 5.2.1.2 Shrimp

- 5.2.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 Broiler

- 5.2.2.2 Layer

- 5.2.2.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 Beef Cattle

- 5.2.3.2 Dairy Cattle

- 5.2.3.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 By Country

- 5.3.1 South Africa

- 5.3.2 Egypt

- 5.3.3 Nigeria

- 5.3.4 Kenya

- 5.3.5 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Cargill, Incorporated

- 6.4.3 DSM-Firmenich

- 6.4.4 Kemin Industries, Inc.

- 6.4.5 Adisseo Group

- 6.4.6 Nutreco (SHV Holdings)

- 6.4.7 Novus International, Inc.

- 6.4.8 Archer Daniel Midland Company

- 6.4.9 Perstorp Holding AB

- 6.4.10 Alltech, Inc.

- 6.4.11 Impextraco NV

- 6.4.12 Lallemand Inc.

- 6.4.13 Vetagro S.p.A.

- 6.4.14 CID LINES

- 6.4.15 Phibro Animal Health Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

飼料酸添加劑市場:按類型、牲畜類型、劑型、應用和分銷管道分類-2026-2032年全球市場預測

飼料酸添加劑市場:按類型、牲畜類型、劑型、應用和分銷管道分類-2026-2032年全球市場預測 2026-2034年全球飼料酸添加劑市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球飼料酸添加劑市場規模、佔有率、趨勢和成長分析報告 2026年全球飼料酸化劑市場報告

2026年全球飼料酸化劑市場報告 飼料酸化劑市場規模、佔有率和成長分析(按類型、劑型、化合物、畜種和地區分類)-2026-2033年產業預測

飼料酸化劑市場規模、佔有率和成長分析(按類型、劑型、化合物、畜種和地區分類)-2026-2033年產業預測 飼料酸化劑市場-全球產業規模、佔有率、趨勢、機會和預測,按添加劑(富馬酸、乳酸、丙酸)、動物(水產養殖、家禽、反芻動物、豬)、地區和競爭細分,2020-2030 年預測

飼料酸化劑市場-全球產業規模、佔有率、趨勢、機會和預測,按添加劑(富馬酸、乳酸、丙酸)、動物(水產養殖、家禽、反芻動物、豬)、地區和競爭細分,2020-2030 年預測 亞太地區酸味劑市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美飼料酸味劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲飼料酸味劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)飼料酸味劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)飼料酸味劑市場:未來預測(2025-2030)

亞太地區酸味劑市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美飼料酸味劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲飼料酸味劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)飼料酸味劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)飼料酸味劑市場:未來預測(2025-2030)