|

市場調查報告書

商品編碼

2073308

持續績效管理平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Continuous Performance Management Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

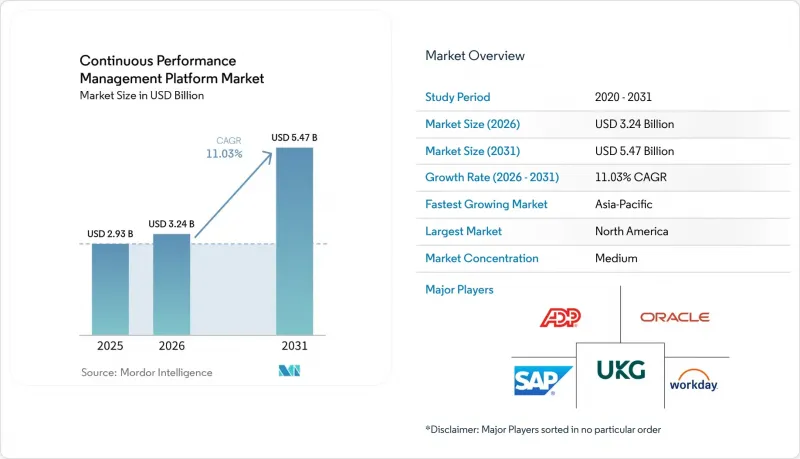

根據 Mordor Intelligence 預測,持續效能管理平台市場規模預計將在 2025 年達到 29.3 億美元,2026 年達到 32.4 億美元,到 2031 年達到 54.7 億美元,2026 年至 2031 年的複合年成長率為 11.03%。

本報告按組件(軟體和服務)、部署模式(雲端和本地部署)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、醫療保健和生命科學、零售和消費品、製造業等)以及地區進行細分。市場預測以價值(美元)表示。

全球持續性能管理平台市場趨勢與洞察

從年度評估向持續回饋體系的重大轉變。

由於間歇性評估無法捕捉角色演變和策略調整的快速變化,企業正逐漸拋棄年度績效評估。 Betterworks 的一項調查顯示,只有 16% 的公司認為人才決策是“可預測的”,而 73% 的公司意識到資訊缺口阻礙了他們的工作。將回饋整合到 Slack 和 Teams 中,無需切換上下文,即可在工作流程中擷取績效徵兆,從而更快地進行調整。 SAP 的「H1226 目標設定和目標進度代理」能夠主動辨識過時的目標,並減少考核週期結束時的意外事件。這種轉變在零售業尤為顯著,該行業高管的平均離職率高達 22%,要求不斷變化的團隊進行即時協作。採購週期正在縮短,提供夜間人力資源資訊系統 (HRIS) 同步和即時校準分析的供應商正在贏得合約。

為了追求擴充性和成本效益,基於雲端的人力資源解決方案正被廣泛採用。

雲端採用消除了以往本地部署系統所需的資本投入和長達數月的升級過程。一項2026年經同行評審的研究表明,整合分散式運算的雲端HCM平台能夠提升中小企業的數據準確性、評估可靠性和營運應對力。根據ICON Corporate Finance估計,60%的企業計劃增加對AI驅動型HCM平台的投資,而能夠每週改進功能的供應商預計將更受青睞。 Lattice的藍圖透過AI驅動的評估方案產生以及與Workday和Rippling的無縫整合,確保人才資料的完整性。諸如Workday Flex Credits之類的計量收費模式進一步減少了採購流程中的摩擦,並支援在無需重新談判合約的情況下擴展AI的使用。

對GDPR和CCPA下的資料隱私和合規性的擔憂

由於績效管理平台會收集敏感的評估、輔導筆記和情緒評分,雇主必須遵守嚴格的資料保護法規。英國資訊專員辦公室 (ICO) 在 2024 年至 2025 年間收到了約 43,000 起申訴,並且從 2026 年 6 月 19 日起,ICO 將能夠僅根據申訴提交的資料發布初步調查結果。由於人工智慧產生的摘要屬於個人資料的範疇,供應商必須提供資料最小化措施、資料保留期限和基於角色的存取控制。歐盟人工智慧法將評估演算法歸類為“高風險”,並就透明度和偏見緩解提出了額外要求。擁有 SOC 2、ISO 和 GDPR 合規認證的供應商可以獲得競爭優勢,因為買家會尋求降低合規風險。

細分市場分析

隨著客戶在整合人工智慧輸出、繪製資料流程圖以及培訓管理員如何利用持續回饋方面面臨許多挑戰,業務收益正在加速成長。儘管到2025年,軟體仍將佔據持續績效管理平台市場61.45%的佔有率,但實施和整合合約的複合年成長率(CAGR)卻高達12.21%。專業服務領域持續績效管理平台市場的擴張,主要源自於對Oracle 25D功能和SAP代理版本在配置、管治和變更管理方面專業知識的需求。此外,由於人力資源部門缺乏衡量人工智慧成功指標的能力,支援合約的需求也在激增,這與SHRM的調查結果相符,即56%的公司沒有追蹤人工智慧的投資報酬率(ROI)。

第二個成長引擎是合規諮詢。當人工智慧應用於大規模監控時,資料保護影響評估和基於角色的存取控制設計仍然至關重要。能夠將諮詢服務與持續管理服務結合的供應商可以確保多年的穩定收入來源,這正推動持續效能管理平台市場擺脫以授權為中心的模式。

在預測期內,雲端採用率預計將超過本地部署解決方案,年複合成長率 (CAGR) 將達到 13.01%,這主要得益於企業對更平滑升級、更低資本支出 (CapEx) 以及高彈性人工智慧的需求。儘管到 2025 年,舊有系統仍將佔據持續績效管理平台市場 68.19% 的佔有率,但供應商藍圖顯示,雲端解決方案每週都會發布新功能,而本地部署解決方案則每年才發布一次修補程式。 Workday Flex 收費就是「按需付費」模式的典型例子,而 2026 年的學術研究也證實,雲端架構能夠提高評估週期的回應速度和資料準確性。

在嚴格監管的行業中,為了滿足資料主權法規的要求,本地部署版本仍然被廣泛應用,並維持相當可觀的部署基礎。然而,採購成本核算的趨勢正在改變。專業的SaaS供應商預計部署時間僅需4到8週,遠低於套件產品升級所需的9到18個月。這加快了價值實現的速度,並鞏固了雲端在持續效能管理平台市場的主導地位。

區域分析

預計到2025年,北美將佔全球銷售額的36.86%,並將繼續保持最大區域貢獻,這得益於北美地區密集的人力資本管理(HCM)供應商、諮詢公司和早期採用者的生態系統。儘管美國企業對試用尚不成熟的人工智慧表現出較高的接受度,但法規環境正變得日益嚴格,目前已有19個州限制雇主使用人工智慧。加拿大和墨西哥在人工智慧應用方面落後於美國,但受益於跨國公司在整個北美大陸推行的雲端部署,這些部署正在實現流程標準化。

亞太地區是成長最快的地區,複合年成長率高達11.98%,這主要得益於人力資源長(CHRO)正從勞動力規劃轉向基於技能的策略。印度的IT服務中心和澳洲成熟的服務型經濟正在複製北美地區的採用曲線,而中國則正在將績效數據與製造業的關鍵績效指標(KPI)結合。資料居住的法律法規片段化阻礙了跨境應用,但隨著在地化介面和區域資料中心的建設,這些障礙正在逐漸減少。

歐洲的情況錯綜複雜。德國和英國的雲端運算應用十分活躍,但由於GDPR的強制性要求以及與工人代表委員會的磋商,銷售週期正在延長。英國資訊專員辦公室(ICO)推出了新的申訴處理規則,合規風險日益增加;由於歐盟人工智慧法將效能演算法歸類為高風險,供應商被迫在透明度功能方面投入巨資。中東、非洲和南美洲仍在發展中,但前景可期。沙烏地阿拉伯、阿拉伯聯合大公國、巴西和阿根廷正在試點基於雲端的人力資源管理系統,作為其「數位化優先」政府計畫的一部分。基礎設施不足和外匯波動阻礙了成長,但跨國公司的子公司正在播下需求的種子,而這種需求正逐漸擴散到當地企業。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從年度評估向持續回饋體系的重大轉變。

- 擴大雲端人力資源解決方案的採用,以提高擴充性和成本效益。

- 遠端和混合工作模式的擴展需要即時績效視覺化。

- 整合人工智慧和分析技術,實現數據驅動的人才選拔

- 敏捷企劃團隊。

- 利用被動監聽資料流進行員工情緒分析的興起

- 市場限制因素

- GDPR 和 CCPA 下的資料隱私和合規性問題

- 組織對績效評估中文化變遷的抵制

- 人工智慧驅動的評估模型中演算法偏差的風險

- 過多的微回饋會導致管理者倦怠。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 持續回饋軟體

- 績效評估工作流程軟體

- 人力資源和技能發展追蹤軟體

- 整合和 API 管理模組

- 其他軟體

- 服務

- 實施和整合服務

- 支援和維護服務

- 軟體

- 部署模式

- 基於雲端的

- 現場

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- IT/通訊

- BFSI

- 醫療保健和生命科學

- 零售和消費品

- 製造業

- 政府/公共部門

- 教育

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP, Inc.

- UKG Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Lattice HR, Inc.

- 15Five, Inc.

- Betterworks Systems, Inc.

- Reflektive, Inc.

- Culture Amp Pty Ltd

- PerformYard LLC

- Trakstar, Inc.

- ClearCompany, Inc.

- Engagedly, Inc.

- Synergita Software Pvt. Ltd.

- Small Improvements GmbH

- WorkTango Inc.

- Paycor, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the continuous performance management platform market size is expected to be USD 2.93 billion in 2025, USD 3.24 billion in 2026, and reach USD 5.47 billion by 2031, growing at a CAGR of 11.03% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecom, Healthcare and Life Sciences, Retail and Consumer Goods, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Continuous Performance Management Platform Market Trends and Insights

Widespread Shift From Annual Reviews to Continuous Feedback Frameworks

Organizations are abandoning once-a-year appraisals because episodic reviews fail to capture the speed of role evolution and strategic pivots. Betterworks research reported that only 16% of firms view talent decisions as predictive, while 73% acknowledge intelligence gaps that derail initiatives. Embedding feedback into Slack and Teams removes context-switching, captures performance signals in flow-of-work, and delivers faster course corrections. SAP's 1H 2026 Goal Creation and Goal Progress Agents proactively flag outdated objectives, cutting end-of-cycle surprises. The shift is acute in retail, where senior-leader turnover averages 22%, forcing real-time alignment among constantly changing teams. Procurement cycles are compressing, and vendors offering nightly HRIS synchronizations alongside real-time calibration analytics are winning deals.

Rising Adoption of Cloud-Based HR Solutions for Scalability and Cost Efficiency

Cloud deployment eliminates capital expense and multi-month upgrades that hamper on-premises systems. A 2026 peer-reviewed study found that cloud HRM platforms integrating distributed computing raised data accuracy, appraisal reliability, and operational responsiveness in SMEs. ICON Corporate Finance estimated that 60% of enterprises intend to increase investment in AI-driven HCM platforms, rewarding vendors able to iterate features weekly. Lattice's roadmap delivers AI-powered review drafts and seamless Workday and Rippling integrations that keep talent data aligned. Consumption-based models such as Workday Flex Credits further reduce procurement friction and let firms scale AI usage without contract renegotiations.

Data Privacy and Compliance Concerns Under GDPR And CCPA

Performance platforms capture sensitive ratings, coaching notes, and sentiment scores, exposing employers to strict data-protection rules. The UK ICO logged nearly 43,000 complaints in 2024-2025, and from 19 June 2026 it can issue preliminary findings based solely on complainant submissions. AI-generated summaries fall under personal-data definitions, forcing vendors to offer minimization controls, retention schedules, and role-based access. The EU AI Act classifies evaluation algorithms as high risk, layering extra transparency and bias-mitigation requirements. Providers sporting SOC 2, ISO, and GDPR-ready attestations gain an edge as buyers de-risk compliance exposure.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote and Hybrid Work Models Requiring Real-Time Performance Visibility

- Integration of AI And Analytics for Data-Driven Talent Decisions

- Organizational Resistance to Cultural Change in Performance Evaluation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is accelerating as customers struggle to integrate AI outputs, map data flows, and train managers on continuous feedback. In 2025 software still commanded 61.45% of the continuous performance management platform market, yet implementation and integration engagements are expanding at a 12.21% CAGR. The continuous performance management platform market size for professional services grows because Oracle's 25D features and SAP's agent releases demand configuration, governance, and change-management expertise. Support contracts also balloon as HR teams lack the capacity to measure AI success metrics, corroborating SHRM's finding that 56% of firms never track AI ROI.

A second growth engine is compliance consulting: data-protection impact assessments and role-based access design remain mandatory when AI qualifies as large-scale monitoring. Vendors able to bundle consultancy with recurring managed services lock in multi-year revenue, pushing the continuous performance management platform market beyond a license-centric model.

Cloud adoption is set to eclipse on-premises during the forecast, expanding at a 13.01% CAGR as enterprises seek frictionless upgrades, lower CapEx, and elastic AI consumption. Although legacy installations retained 68.19% of the continuous performance management platform market share in 2025, vendor roadmaps reveal weekly cloud feature drops versus annual on-premises patches. Workday Flex Credits exemplify the pay-as-you-grow model, and a 2026 academic study confirmed cloud architectures improve appraisal-cycle responsiveness and data accuracy.

Highly regulated sectors still deploy on-premises versions to satisfy data-sovereignty rules, preserving a sizable installed base. Yet procurement math is shifting: specialized SaaS vendors quote four-to-eight-week implementations, well below the nine-to-eighteen-month timelines of suite upgrades, accelerating time-to-value and solidifying cloud's ascendancy within the continuous performance management platform market.

Complete Report Scope:

- By Component

- Software

- Continuous Feedback Software

- Performance Review Workflow Software

- Talent and Skill Development Tracking Software

- Integration and API Management Modules

- Other Software

- Services

- Implementation and Integration Services

- Support and Maintenance Services

- Software

- By Deployment Mode

- Cloud-Based

- On-Premises

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Retail and Consumer Goods

- Manufacturing

- Government and Public Sector

- Education

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.86% of 2025 revenue and remains the largest regional contributor, buoyed by dense ecosystems of HCM vendors, consultants, and early adopters. U.S. firms show a high tolerance for piloting unfinished AI, but the regulatory backdrop is tightening as 19 states now regulate employer AI. Canada and Mexico trail in adoption yet benefit from multinational cloud rollouts that standardize processes across the continent.

Asia-Pacific is the fastest-growing region at an 11.98% CAGR, underpinned by CHRO mandates to shift from headcount planning to skills-based strategies. India's IT services clusters and Australia's mature services economy mirror North American adoption curves, while China blends performance data with manufacturing KPIs. Data-residency laws and fragmented regulations complicate cross-border implementations, but local-language interfaces and regional data centers are lowering barriers.

Europe presents a mixed picture: cloud uptake is strong in Germany and the UK, but GDPR obligations and works-council consultations elongate sales cycles. The UK ICO's new complaint rules elevate compliance risk, and the EU AI Act classifies performance algorithms as high risk, forcing vendors to invest heavily in transparency features. Middle East and Africa plus South America are nascent yet promising, with Saudi Arabia, the United Arab Emirates, Brazil, and Argentina piloting cloud HR stacks under digital-first government programs. Infrastructure gaps and currency volatility temper growth, but multinational subsidiaries are seeding demand that gradually radiates to local firms.

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP, Inc.

- UKG Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Lattice HR, Inc.

- 15Five, Inc.

- Betterworks Systems, Inc.

- Reflektive, Inc.

- Culture Amp Pty Ltd

- PerformYard LLC

- Trakstar, Inc.

- ClearCompany, Inc.

- Engagedly, Inc.

- Synergita Software Pvt. Ltd.

- Small Improvements GmbH

- WorkTango Inc.

- Paycor, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread Shift from Annual Reviews to Continuous Feedback Frameworks

- 4.2.2 Rising Adoption of Cloud-Based HR Solutions for Scalability and Cost Efficiency

- 4.2.3 Expansion of Remote and Hybrid Work Models Requiring Real-Time Performance Visibility

- 4.2.4 Integration of AI and Analytics for Data-Driven Talent Decisions

- 4.2.5 Growing Demand for Objective and Key Results Alignment Within Agile Project Teams

- 4.2.6 Emergence of Employee Sentiment Analysis Using Passive Listening Data Streams

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Compliance Concerns Under GDPR and CCPA

- 4.3.2 Organizational Resistance to Cultural Change in Performance Evaluation

- 4.3.3 Algorithmic Bias Risks in AI-Powered Evaluation Models

- 4.3.4 Overload of Micro-Feedback Leading to Manager Burnout

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Continuous Feedback Software

- 5.1.1.2 Performance Review Workflow Software

- 5.1.1.3 Talent and Skill Development Tracking Software

- 5.1.1.4 Integration and API Management Modules

- 5.1.1.5 Other Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Support and Maintenance Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and Consumer Goods

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday Inc.

- 6.4.4 ADP, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Cornerstone OnDemand, Inc.

- 6.4.7 BambooHR LLC

- 6.4.8 Lattice HR, Inc.

- 6.4.9 15Five, Inc.

- 6.4.10 Betterworks Systems, Inc.

- 6.4.11 Reflektive, Inc.

- 6.4.12 Culture Amp Pty Ltd

- 6.4.13 PerformYard LLC

- 6.4.14 Trakstar, Inc.

- 6.4.15 ClearCompany, Inc.

- 6.4.16 Engagedly, Inc.

- 6.4.17 Synergita Software Pvt. Ltd.

- 6.4.18 Small Improvements GmbH

- 6.4.19 WorkTango Inc.

- 6.4.20 Paycor, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球數位許可證頒發平台市場報告

2026年全球數位許可證頒發平台市場報告 聯絡人管理軟體市場:2026-2032年全球市場預測(依產品類型、平台、應用、組織規模、部署模式及最終用戶產業分類)2026年全球雲端列印服務市場報告

聯絡人管理軟體市場:2026-2032年全球市場預測(依產品類型、平台、應用、組織規模、部署模式及最終用戶產業分類)2026年全球雲端列印服務市場報告 銷售培訓和入職軟體市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組和功能分類招募CRM軟體市場:功能、定價模式、部署模式、組織規模、產業垂直領域、全球預測(2026-2032年)按營運商類型、公司規模、倉庫類型、服務類型、儲存類型和最終用戶產業分類的全球海關倉儲市場預測(2026-2032 年)

銷售培訓和入職軟體市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組和功能分類招募CRM軟體市場:功能、定價模式、部署模式、組織規模、產業垂直領域、全球預測(2026-2032年)按營運商類型、公司規模、倉庫類型、服務類型、儲存類型和最終用戶產業分類的全球海關倉儲市場預測(2026-2032 年) Salesforce AppExchange 工具市場規模(全球),依工具類型、部署類型、垂直產業、區域覆蓋範圍和預測

Salesforce AppExchange 工具市場規模(全球),依工具類型、部署類型、垂直產業、區域覆蓋範圍和預測 全球雲端列印服務市場:截至 2031 年

全球雲端列印服務市場:截至 2031 年 P2P 租賃應用市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

P2P 租賃應用市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測