|

市場調查報告書

商品編碼

2073298

技能型招募平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Skills-Based Hiring Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

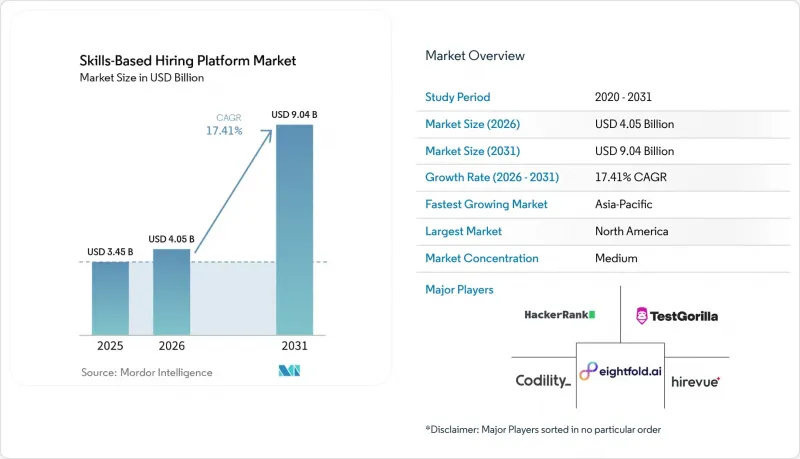

據 Mordor Intelligence 稱,2025 年基於技能的招聘平台市值為 34.5 億美元,預計到 2031 年將從 2026 年的 40.5 億美元成長到 90.4 億美元,預測期(2026-2031 年)的複合年成長率為 17.4%。

本報告按平台類型(獨立技能招募平台、整合式ATS模組、技能評估API供應商等)、部署模式(雲端、本地部署)、組織規模(中小企業、大型企業)、最終用戶產業(IT、電信等)和地區進行細分。市場預測以美元計價。

全球技能型招募平台市場趨勢與洞察

向基於能力的採納方式過渡以減少偏見

到2025年,27%的雇主將從招聘啟事中取消學士學位要求,這一比例較2020年顯著上升,表明基於學歷的選拔方式正被經過檢驗的評估所取代。華盛頓州第24-04號行政命令為公共部門基於能力的招聘制定了模板,其他州也開始採取類似措施。整合了偏見儀錶板和不利影響計算工具的平台,正在幫助企業在合規風險最高的監管行業中成功獲得合約。

透過整合人工智慧和分析技術來增強人才匹配。

紐約市第144號地區法案、伊利諾伊州眾議院第3773號法案以及即將實施的歐盟人工智慧法案均對自動化招聘流程施加了偏見審計和披露要求,迫使供應商添加即時可解釋性模組。麥肯錫2026年「組織狀況」調查發現,採用人性化的公司實現投資報酬率目標的可能性是其他公司的1.6倍,這得益於合規分析的有效性。資金雄厚的供應商正在承擔這些成本,並透過即時評估產生來打造差異化產品,進一步鞏固其競爭優勢,而小規模的競爭對手則仍在努力克服合規方面的障礙。

與傳統人力資源資訊系統和招募管理系統整合的局限性

大多數人力資源資訊系統都是圍繞著履歷文件而非標準化的技能模型建構的,這導致資料模型不一致,延長了部署時間並推高了總體擁有成本 (TCO)。採購公司被迫在投資客製化連接器或接受碎片化的工作流程之間做出選擇,這減緩了對成本敏感的中型企業的採用速度。提供承包整合和中間件的供應商可以將技能本體轉換為舊有系統欄位結構,從而緩解這些障礙並加速獲利。

細分市場分析

截至2025年,獨立系統將佔據基於技能的招聘平台市場佔有率的39.45%,但隨著雇主對更高完成率和更深入的行為洞察的需求,遊戲化評估平台正以19.34%的複合年成長率成長。 《2025年未來就業報告》指出,創造性思考、韌性和好奇心是成長最快的技能,而這些特質透過互動場景而非靜態問卷調查更能有效衡量。

技能評估API供應商使企業能夠將測試整合到其入口網站中,但他們將可訪問性和本地化的責任轉移給了買家——中型人力資源團隊往往低估了這種權衡。國際貨幣基金組織的一項研究表明,尋求新經濟技能的企業通常成立時間較短,更具創新精神,這表明技術成熟度與API採用率之間存在相關性。

到2025年,本地部署將佔市場佔有率的67.14%,其中大部分將來自受監管行業,這主要是出於合規性和資料安全方面的考慮。然而,雲端訂閱正在經歷顯著成長,年成長率超過20%。這一成長主要得益於供應商建立區域資料中心以應對延遲和監管要求,以及提供自帶金鑰(BYOK)加密等進階安全功能。

自2020年以來,員工人數少於50人的公司採用雲端人力資源工具的比例不斷上升,顯示企業越來越傾向於雲端解決方案。混合模式(即在本地保留數據,同時利用供應商的雲端服務進行運算)因其在數據主權和可擴展性之間取得平衡而日益普及。然而,在成本比較方面,完整的SaaS解決方案優勢越來越明顯,傳統的本地部署供應商如果不進行創新,將面臨市場佔有率流失的風險。

區域分析

到2025年,北美將佔全球整體收入的36.76%。這主要得益於紐約市的審計法律和強大的創業投資生態系統,後者促進了產品快速迭代。針對偏見審計的區域法規正在推動平台升級。這些審計確保平台運作不存在固有偏見,從而促進營運中的公平性和包容性。同時,蓬勃創業投資環境正在推動具有全球影響力的技術進步。該生態系統不僅提供資金,還培育新創公司和成熟公司,不斷拓展創新邊界。歐洲嚴格的資料保護措施以及即將實施的人工智慧立法進一步加劇了合規挑戰。

《人工智慧法案》將為人工智慧的應用引入嚴格的指導方針,確保透明度、課責和合乎倫理的使用。然而,這些障礙也將作為基準,淘汰那些積極性不高的參與者,並創造一個以品質為導向的競爭環境。目前成長最快的亞太地區預計到2031年將以18.91%的複合年成長率成長。這一快速成長得益於印度為實現「國家技能資格框架」所做的努力,該框架旨在規範技能發展並提高勞動力的技能水平。在日本,作為應對勞動力老化政策的一部分,政府正努力將技術和技能再培訓結合,以維持生產力。

南美洲和中東/非洲地區目前仍落後於其他地區,但差距正在迅速縮小。離線評估工具和輕量級網路用戶端等創新技術正在幫助克服基礎設施方面的挑戰。離線評估工具即使在網路連線有限的地區也能正常運行,而輕量級網路用戶端則確保即使在低頻寬網路上也能可靠存取。在每個地區策略性地部署資料中心、提供支援多種語言的題庫以及符合政府標準的能力映射,將是供應商在這些快速成長的市場中取得成功的關鍵因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 過渡到擇優錄用以減少偏見

- 後疫情時代遠距招聘方式的廣泛應用

- 縮短招募時間相關指標的需求日益成長。

- 整合人工智慧和分析技術以增強人才匹配

- 政府新推出的技能分類系統促進了平台標準化。

- 利用區塊鏈技術的微憑證認證的興起

- 市場限制因素

- 與傳統人力資源資訊系統和招募管理系統的整合有限。

- 全球法規下的資料隱私和合規挑戰

- 對缺乏評估素養的負責人持懷疑態度

- 小眾領域缺乏高品質的技能評估內容

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依平台類型

- 獨立的技能型招募平台

- 整合式ATS模組

- 技能評估 API 提供者

- 遊戲化型評估平台

- 其他平台類型

- 部署模式

- 基於雲端的

- 現場

- 按組織規模

- 中小企業

- 大公司

- 產業最終用途

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售與電子商務

- 政府

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HireVue Inc.

- SHL Group Ltd.

- HackerRank Inc.

- TestGorilla BV

- Codility Ltd.

- Harver BV

- Mercer LLC(Mercer Mettl)

- iMocha

- Pymetrics Inc.

- Vervoe

- TalentSorter(Fit First Technologies Inc.)

- Arctic Shores Ltd.

- Traitify by Paradox, LLC

- Plum Inc.

- Talview Inc.

- Applied Ltd.

- SkillSurvey Inc.

- AssessFirst SA

- Bryq PC

- Eightfold AI Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the skills-based hiring platform market size was valued at USD 3.45 billion in 2025 and estimated to grow from USD 4.05 billion in 2026 to reach USD 9.04 billion by 2031, at a CAGR of 17.4% during the forecast period (2026-2031).

This report is Segmented by Platform Type (Standalone Skills-Based Hiring Platforms, Integrated ATS Modules, Skill Assessment API Providers, and More), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Small and Medium Enterprises [SMEs], and Large Enterprises), End-Use Industry (IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Skills-Based Hiring Platform Market Trends and Insights

Shift Toward Competency-Based Recruitment to Reduce Bias

Twenty-seven percent of employers removed bachelor's-degree requirements from job postings in 2025, up sharply from 2020, confirming that credential screens are being replaced by validated assessments. Washington State's Executive Order 24-04 created a public-sector template for competency hiring and has already been echoed by other U.S. states. Platforms embedding bias dashboards and adverse-impact calculators now win regulated-sector contracts where compliance risk is greatest.

Integration of AI And Analytics to Enhance Talent Matching

New York City Local Law 144, Illinois HB 3773, and the soon-to-be-enforced EU AI Act impose bias-audit and disclosure mandates on automated hiring, driving vendors to add real-time explainability modules.McKinsey's 2026 "State of Organizations" survey shows firms using human-centric AI are 1.6 times more likely to hit ROI targets, reinforcing the payoff from compliant analytics. Well-capitalized providers absorb these costs and widen product gaps via real-time assessment generation, reinforcing competitive moats even as smaller peers struggle to clear compliance hurdles.

Limited Integration with Legacy HRIS and ATS Systems

Most human-resource information systems were built around resume files, not normalized skill profiles, so data-model misalignment inflates implementation timelines and pushes total cost of ownership higher. Buyers either fund bespoke connectors or accept fragmented workflows, delaying adoption among cost-sensitive mid-market firms. Vendors offering turnkey integrations and middleware that translate skills ontologies into legacy field structures mitigate this drag and accelerate revenue conversion.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Remote Hiring Practices Post-Pandemic

- Increasing Demand for Faster Time-to-Hire Metrics

- Data Privacy and Compliance Challenges Under Global Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standalone systems accounted for 39.45% of the skills-based hiring platform market share in 2025, yet gamified assessment platforms are growing at a 19.34% CAGR as employers seek higher completion rates and richer behavioral insight. The Future of Jobs 2025 report ranks creative thinking, resilience, and curiosity among the fastest-rising skills, traits better measured through interactive scenarios than static surveys.

Skill-assessment API vendors let enterprises embed tests into proprietary portals, but they off-load accessibility and localization burdens onto buyers, a trade-off some mid-market HR teams underestimate. IMF research shows that firms advertising new-economy skills tend to be younger and more innovative, implying a correlation between technical maturity and API adoption.

In 2025, on-premises deployments commanded a 67.14% market share, predominantly in regulated sectors where compliance and data security concerns drive adoption. However, cloud subscriptions are experiencing significant growth, with an annual increase exceeding 20%. This growth is fueled by vendors establishing regional data centers to address latency and regulatory requirements, as well as offering advanced security features like bring-your-own-key encryption.

Cloud HR tool adoption among firms with fewer than 50 employees rose from 2020, showcasing the growing preference for cloud-based solutions. Hybrid models, which retain data locally while leveraging vendor clouds for computation, are gaining traction due to their ability to balance data sovereignty with scalability. However, cost comparisons increasingly favor full SaaS solutions, putting pressure on traditional on-premises providers to innovate or risk losing market share.

Complete Report Scope:

- By Platform Type

- Standalone Skills-Based Hiring Platforms

- Integrated ATS Modules

- Skill Assessment API Providers

- Gamified Assessment Platforms

- Other Platform Types

- By Deployment Mode

- Cloud-Based

- On-Premises

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-Use Industry

- IT and Telecom

- BFSI

- Healthcare

- Manufacturing

- Retail and E-Commerce

- Government

- Other End-Use Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America delivered 36.76% of global revenue in 2025, propelled by New York City's audit law and a dense venture-capital ecosystem driving rapid product cycles. Local mandates on bias audits are prompting upgrades across platforms. These audits ensure that platforms operate without inherent biases, fostering fairness and inclusivity in their operations. Simultaneously, a robust venture-capital landscape is fueling technological advancements with global repercussions. This ecosystem not only provides funding but also nurtures startups and established firms to push the boundaries of innovation. Europe's rigorous data protection measures, alongside the impending AI Act, elevate compliance challenges.

The AI Act introduces stringent guidelines for AI deployment, ensuring transparency, accountability, and ethical usage. However, these hurdles also establish a benchmark, filtering out less-invested players and promoting a competitive environment focused on quality. Asia-Pacific, charting the fastest growth trajectory, is set to expand at an 18.91% CAGR through 2031. This surge is driven by India's alignment with the National Skills Qualifications Framework, which standardizes skill development and enhances workforce readiness. Japan's policies addressing its aging workforce aim to integrate technology and reskilling initiatives to maintain productivity.

While South America, the Middle East, and Africa lag behind, they're rapidly closing the gap. Innovations like offline-capable assessments and streamlined web clients are helping them navigate infrastructural challenges. Offline-capable assessments enable functionality in areas with limited internet access, while lighter web clients ensure accessibility on low-bandwidth networks. The strategic placement of regional data centers, diverse language item banks, and adherence to government-standard competency mapping will play pivotal roles in determining vendor success across these burgeoning markets.

- HireVue Inc.

- SHL Group Ltd.

- HackerRank Inc.

- TestGorilla B.V.

- Codility Ltd.

- Harver B.V.

- Mercer LLC (Mercer Mettl)

- iMocha

- Pymetrics Inc.

- Vervoe

- TalentSorter (Fit First Technologies Inc.)

- Arctic Shores Ltd.

- Traitify by Paradox, LLC

- Plum Inc.

- Talview Inc.

- Applied Ltd.

- SkillSurvey Inc.

- AssessFirst SA

- Bryq P.C.

- Eightfold AI Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Competency-Based Recruitment to Reduce Bias

- 4.2.2 Growing Adoption of Remote Hiring Practices Post-Pandemic

- 4.2.3 Increasing Demand for Faster Time-to-Hire Metrics

- 4.2.4 Integration of AI and Analytics to Enhance Talent Matching

- 4.2.5 Emerging Government Skills Taxonomies Driving Platform Standardization

- 4.2.6 Rise of Micro-credential Verification via Blockchain

- 4.3 Market Restraints

- 4.3.1 Limited Integration With Legacy HRIS and ATS Systems

- 4.3.2 Data Privacy and Compliance Challenges Under Global Regulations

- 4.3.3 Skepticism From Hiring Managers Lacking Assessment Literacy

- 4.3.4 Shortage of High-Quality Skill Assessment Content in Niche Domains

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Standalone Skills-Based Hiring Platforms

- 5.1.2 Integrated ATS Modules

- 5.1.3 Skill Assessment API Providers

- 5.1.4 Gamified Assessment Platforms

- 5.1.5 Other Platform Types

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-Use Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government

- 5.4.7 Other End-Use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HireVue Inc.

- 6.4.2 SHL Group Ltd.

- 6.4.3 HackerRank Inc.

- 6.4.4 TestGorilla B.V.

- 6.4.5 Codility Ltd.

- 6.4.6 Harver B.V.

- 6.4.7 Mercer LLC (Mercer Mettl)

- 6.4.8 iMocha

- 6.4.9 Pymetrics Inc.

- 6.4.10 Vervoe

- 6.4.11 TalentSorter (Fit First Technologies Inc.)

- 6.4.12 Arctic Shores Ltd.

- 6.4.13 Traitify by Paradox, LLC

- 6.4.14 Plum Inc.

- 6.4.15 Talview Inc.

- 6.4.16 Applied Ltd.

- 6.4.17 SkillSurvey Inc.

- 6.4.18 AssessFirst SA

- 6.4.19 Bryq P.C.

- 6.4.20 Eightfold AI Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment