|

市場調查報告書

商品編碼

2073281

預支薪資(EWA)平台:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Earned Wage Access (EWA) Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

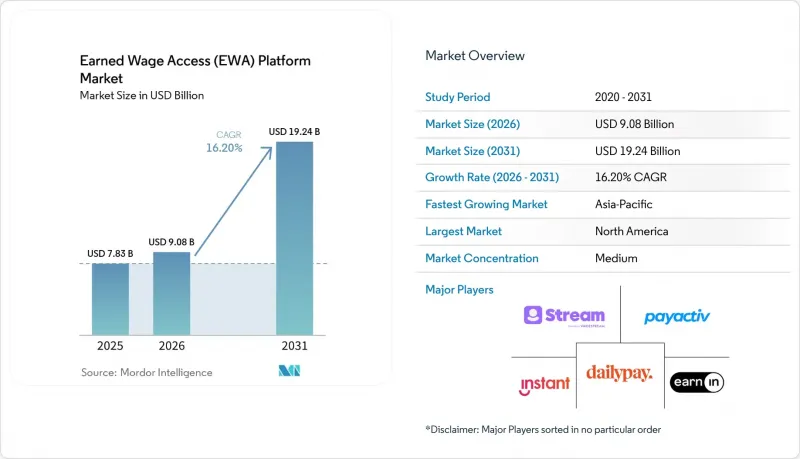

根據 Mordor Intelligence 預測,薪資預支 (EWA) 平台市場規模預計將在 2025 年達到 78.3 億美元,2026 年達到 90.8 億美元,到 2031 年達到 192.4 億美元,2026 年至 2031 年的複合成長率為 16.2%。

本報告依交付模式(雇主整合預支薪資服務 [EWA]、消費者直接預支薪資服務 [EWA] 等)、部署模式(雲端部署、本地部署)、組織規模(大型企業和中小企業 [SME])、最終用戶產業(零售/電子商務及其他)和地區進行細分。市場預測以美元 (USD) 為單位。

全球預繳薪資(EWA)平台市場趨勢與洞察

將「預支薪資服務 (EWA)」作為財務健康福利的採用率正在迅速提高。

研究表明,超過一半的第一線醫護人員將財務壓力與工作表現聯繫起來,因此,雇主已將按需支付從一項附加福利轉變為其財務健康戰略的核心要素。護理師自願離職率的降低,使得每位留任員工都能節省數萬美元的成本,這也使得預支工資服務的評估標準從人力資源預算轉向了首席財務官層面的成本節約指標。儘管絕大多數小時工都表示可以選擇每週或即時支付,但雇主的接受度仍然較低,這表明該領域仍有巨大的成長空間。隨著 SOC 2 和 GDPR 等審計標準成為基本要求,頂級供應商正透過透明的收費系統和防篡改的審計追蹤脫穎而出。這些因素共同鞏固了私人和公共部門雇主對按需支付的需求。

已開發國家市場即時支付基礎建設的擴展

預計到2025年,即時支付系統(例如美國的FedNow、歐洲的RTP和澳洲的新支付平台)將迎來大幅規模化發展,交易限額將大幅提高,金融機構的參與度也將進一步擴大。當日結算將減少或消除資金籌措造成的資金滯留問題(先前預付款一直是服務提供者的負擔),從而使免手續費的薪資預支在經濟上永續。更高的交易限額將涵蓋中等規模的工資發放批次,使雇主能夠使用單一支付管道進行工資預支和常規薪水支付。因此,供應商現在可以承諾向員工即時支付工資,而無需依賴儲值卡,從而解決了用戶體驗調查中指出的最大挑戰之一。由此,單位層級的規模經濟效益將得到結構性提升,因此能夠涵蓋更廣泛的地理區域。

貸款和非貸款分類方面的監管模糊不清。

儘管美國聯邦指南豁免了免手續費的綜合性「工資預支服務」的貸款監管,但各州和許多國際司法管轄區仍保留將其作為匯款或小額貸款業務進行許可的自由裁量權。加州的揭露要求和康乃狄克州的註冊要求增加了合規成本,給新興供應商帶來了特別沉重的負擔。在亞太地區,印度將服務提供者視為非銀行金融機構,從而提供了清晰的監管框架,而印尼和其他國家仍在就費用上限和許可分類進行辯論。由此產生的監管不一致迫使平台要么尋求分散的許可,要么遊說制定統一的規則,這減緩了跨州擴張的速度並增加了法律成本。這種持續存在的不確定性仍然是短期業務擴張的一大障礙,因為廣泛的地域覆蓋對於成長至關重要。

細分市場分析

到2025年,雇主整合系統將佔據工資預支(EWA)平台市場54.77%的最大佔有率。這反映了大型企業優先考慮免手續費福利以規避貸款合規要求的趨勢。結合了兩種功能的混合平台正以18.34%的複合年成長率快速成長,成為成長最快的細分市場。然而,對於零工人員和沒有企業支援計畫的公司員工而言,直接面對消費者的應用程式仍然至關重要。這些解決方案將預算管理儀表板、儲蓄加速功能和提前支付功能整合到單一工作流程中,滿足了尋求全面財務管理的員工的需求。近期白牌API的出現使薪資核算供應商能夠將這些服務整合到其現有套件中,從而將部署時間縮短至數週。這種整合預示著未來單一用途服務將逐漸減少,而整合式健康套件將成為主流,這將進一步強化網路效應,使那些在雇主、薪資核算和消費者之間擁有最廣泛接觸點的平台受益。

混合模式透過收集雇主工資數據並直接向員工結算資金,降低了監管風險,並允許根據不同司法管轄區進行動態合規設定。領先的服務提供者報告稱,混合模式的用戶在三個月內至少會使用兩項輔助服務,例如預算管理或基於目標的儲蓄,這有助於提高用戶留存率和交叉銷售收入。隨著企業尋求既能滿足合規要求又能兼顧員工偏好的可配置方案,預計到2031年,分配給混合平台的預支工資市場規模將成長一倍以上。

儘管預計到 2025 年,本地部署仍將佔總收入的 66.67%,但隨著中型企業對更快運作速度和更低資本支出的需求,雲端採用率正以 18.71% 的複合年成長率快速成長。 Workday 的策略投資已將 DailyPay 直接整合到其雲端 HCM 套件中,從而消除了中間件帶來的延遲。此雲端平台每週更新功能,提供多區域冗餘,並能以遠低於本地部署所需的時間與即時支付系統整合。領先的人力資源軟體供應商的策略性投資正在將基於雲端的預支薪資功能直接整合到核心人才管理套件中,這些架構正逐漸成為新部署的預設選擇。

儘管在受嚴格資料主權法規約束的行業中,本地部署環境仍然被廣泛使用,但除了與頂級企業客戶的合約外,幾乎所有新契約都明確規定了雲端採用。在薪資平台市場,由於安全升級可以在租戶之間統一進行,而無需供應商提供客製化補丁,因此效率得到了顯著提升。此外,API優先的雲端系統有助於開放開發者生態系統,從而不斷附加元件,進一步增強了其核心價值提案。

區域分析

預計到2025年,北美將佔全球銷售額的36.54%。這得歸功於成熟的薪資核算軟體生態系統、資金雄厚的供應商以及FedNow Rail的推出(該平台處理了7,400萬筆交易)。聯邦法規的明確進一步降低了企業的猶豫,並加速了財富500強企業對該軟體的採用。在加拿大和墨西哥,人們對該軟體的興趣日益濃厚,這主要得益於零工經濟平台採用的直接面對消費者的模式,這種模式無需雇主擔保。

亞太地區是成長的主要驅動力,預計到2031年將以17.92%的複合年成長率成長。在印度,將服務提供者歸類為非銀行金融公司,為其開闢了債務資金籌措管道,零工經濟從業人員人數已超過770萬人。區域企業正利用這項監管利好,透過採用即時支付基礎設施(例如澳洲的「新支付平台」和新加坡的「FAST」系統)來拓展企業發展。在中國、日本和韓國,即時支付的普及正在穩步推進,主要集中在電子商務和製造業領域。

在歐洲,隨著參與SEPA Instant成為強制性要求,即時支付在成員國之間實現標準化,即時支付正保持穩定成長的勢頭。雖然遵守GDPR增加了初始安全成本並延長了採購週期,但一旦完成整合,企業報告說扣回爭議帳款降低,員工滿意度提高。在南美洲,阿根廷關於基於電子錢包的薪水支付的監管討論正在促進平台間的合作,並展現出強勁的發展勢頭。同時,巴西和哥倫比亞也開始製定開放金融指南,以鼓勵更多地使用預支工資。在中東,大規模的外籍勞工群體正在推動即時支付的普及,其中數額達數千萬美元的合資企業就是一個典型的例子。然而,由於即時支付基礎設施不足以及消費者金融素養水準參差不齊,非洲的即時支付仍處於發展初期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 將「預支薪資服務」作為一種財務福利手段正迅速普及。

- 已開發國家市場即時支付基礎建設的擴展

- 亞太地區零工經濟勞動力的成長

- 零售和餐飲業對時薪員工的競爭日益激烈。

- 擴大金融科技公司與傳統薪資核算服務供應商之間的策略夥伴關係

- 嵌入式金融 API 的出現,使得白牌EWA 成為可能。

- 市場限制因素

- 關於「貸款」和「非貸款」分類的監管規定存在模糊之處。

- 大型企業的資料安全與隱私問題

- 非洲用戶金融素養不足,導致用戶接受新事物的速度放緩。

- 交換費的降低給單位盈利帶來了壓力。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按型號提供

- 雇主關聯工資預支服務 (EWA)

- 消費者預支薪資服務 (EWA)

- 混合模式

- 部署模式

- 基於雲端的

- 現場

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- 零售與電子商務

- 衛生保健

- 製造業

- 飯店餐飲業

- 運輸/物流

- 銀行、金融服務和保險(BFSI)

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Payactiv Inc.

- Earnin, Inc.

- DailyPay Inc.

- Wagestream Holdings Limited

- Instant Financial USA Inc.

- FlexWage Solutions LLC

- Even Responsible Finance, Inc.

- Branch Technologies Inc.

- Rain Technologies Inc.

- ZayZoon Inc.

- Clair Inc.

- Hastee Technologies Limited

- SalaryFinance Limited

- Refyne Tech Private Limited

- Tapcheck Inc.

- FinFit Ops LLC

- Immediate Solutions, Inc.

- Payflow SL

- Line Financial PBC

- Instapay Technologies Pty Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the earned wage access (EWA) platform market size is expected to be USD 7.83 billion in 2025, USD 9.08 billion in 2026, and reach USD 19.24 billion by 2031, growing at a CAGR of 16.2% from 2026 to 2031.

This report is Segmented by Delivery Model (Employer-Integrated Earned Wage Access [EWA], Direct-To-Consumer Earned Wage Access [EWA], and More), Deployment Mode (Cloud-Based, and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises [SMEs]), End-User Industry (Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Earned Wage Access (EWA) Platform Market Trends and Insights

Surging Adoption of Earned Wage Access as a Financial-Wellness Benefit

Employers have repositioned on-demand pay from a fringe perk to a central component of financial-wellness strategies, driven by survey evidence showing more than half of frontline healthcare staff link money stress to job performance. Lower voluntary turnover among nurses translated into five-figure savings per departure prevented, shifting evaluation of earned wage access from HR budgets to CFO-level cost-avoidance metrics. Hourly workers overwhelmingly state a preference for weekly or instant pay, yet employer adoption still lags, signaling significant headroom for growth. As audit standards such as SOC 2 and GDPR become baseline requirements, best-in-class vendors differentiate through transparent fee structures and immutable audit trails. Taken together, these factors anchor demand across both commercial and public-sector employers.

Expansion of Real-Time Payments Infrastructure in Developed Markets

Instant-settlement systems, FedNow in the United States, RTP in Europe, and the New Payments Platform in Australia, scaled dramatically during 2025, lifting transaction ceilings and widening financial-institution participation. Same-day clearing lowers or eliminates the pre-funding float previously carried by providers, making zero-fee wage advances economically sustainable. Higher transaction limits now cover mid-sized payroll batches, enabling employers to use a single rail for both advances and regular salary. In turn, vendors can promise workers immediate disbursement without relying on prepaid cards, addressing one of the largest pain points cited in user-experience surveys. The result is a structural improvement in unit economics that supports broader geographic rollouts.

Regulatory Ambiguity Around Lending Versus Non-Lending Classification

Federal guidance in the United States excludes fee-free, employer-integrated earned wage access from lending statutes, yet each state, and many foreign jurisdictions, retains discretion to impose money-transmitter or small-loan licensing. California's disclosure mandates and Connecticut's registration thresholds raise compliance costs that weigh heaviest on emerging vendors. In Asia-Pacific, India offers clarity by treating providers as non-banking financial companies, whereas Indonesia and others still debate fee caps and license categories. The resulting patchwork forces platforms into either piecemeal licensing or lobbying for harmonized rules, slowing multi-state rollouts and inflating legal overhead. Because growth requires wide geographic reach, persistent ambiguity remains a significant drag on near-term expansion.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Gig-Economy Workforce Across Asia-Pacific

- Intensifying Competition for Hourly Talent in Retail and Hospitality

- Data-Security and Privacy Concerns Among Large Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Employer-integrated systems commanded the largest slice of the Earned Wage Access (EWA) Platform market with 54.77% in 2025, a reflection of large organizations prioritizing zero-fee benefits that sidestep lending compliance. The blend of both hybrid platforms is the fastest-growing segment, expanding at an 18.34% CAGR. Direct-to-consumer apps, however, remain essential for gig workers and employees at firms without sponsored programs. These solutions weave budgeting dashboards, savings nudges, and early-deposit features into one workflow, addressing worker demand for holistic money management. Recent white-label API launches let payroll vendors bolt such services onto existing suites, shortening deployment to weeks. This convergence points to a future where single-purpose advances fade, and bundled wellness suites dominate, reinforcing network effects that reward platforms with the broadest employer, payroll, and consumer touchpoints.

Hybrid models also temper regulatory risk because they collect employer payroll data yet settle funds directly to workers, allowing dynamic compliance configurations by jurisdiction. Major providers report that hybrid users engage with at least two ancillary services, budgeting or goal-based savings, within three months, improving stickiness and cross-sell revenue. The earned wage access market size allocated to hybrid platforms is on track to more than double by 2031 as enterprises seek configurable options that satisfy both compliance and worker preference.

On-premise installs represented 66.67% of revenue in 2025, yet cloud deployments advance at an 18.71% CAGR, as mid-market firms look for faster go-lives and lower capital expenditure. Workday's strategic investment embedded DailyPay directly into its cloud HCM suite, eliminating middleware latency. Cloud platforms push weekly feature updates, provide multi-region redundancy, and integrate with real-time payment rails in a fraction of the time required for on-prem installs. Strategic investments from leading HR software vendors baked cloud earned wage access directly into core human-capital suites, cementing these architectures as default for greenfield implementations.

While on-premise will persist in industries subject to stringent data-sovereignty rules, practically every new contract below the top-tier enterprise category now specifies cloud deployment. The earned wage access platform market experiences tangible efficiency gains because vendors can unify security upgrades across tenants, rather than delivering custom patches. Moreover, API-first cloud systems make it straightforward to open developer ecosystems, spawning add-ons such as earned-asset trading or automated savings that amplify the core proposition.

Complete Report Scope:

- By Delivery Model

- Employer-Integrated Earned Wage Access (EWA)

- Direct-to-Consumer Earned Wage Access (EWA)

- Hybrid Models

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- Retail and E-Commerce

- Healthcare

- Manufacturing

- Hospitality and Food Service

- Transportation and Logistics

- Banking, Financial Services and Insurance (BFSI)

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.54% revenue share in 2025, underpinned by a mature payroll-software ecosystem, well-capitalized providers, and the operational debut of the FedNow rail that processed 74 million transactions. Federal regulatory clarity further thawed enterprise hesitancy, accelerating adoption among Fortune 500 employers. Canada and Mexico show rising interest, driven by gig-economy platforms embedding direct-to-consumer models that bypass employer sponsorship.

Asia-Pacific is the growth engine, advancing at a 17.92% CAGR through 2031. India's classification of providers as non-banking financial companies unlocked debt funding pathways, while the gig workforce vaulted beyond 7.7 million. Regional players use this regulatory runway to scale pan-Asian footprints, leveraging real-time payment infrastructure such as Australia's New Payments Platform and Singapore's FAST system. China, Japan, and South Korea report mid-tier uptake, anchored by the e-commerce and manufacturing sectors.

Europe maintains a steady trajectory as SEPA Instant participation becomes mandatory, standardizing immediate settlement across member states. GDPR compliance inflates upfront security costs, elongating procurement cycles, but once integrated, enterprises report fewer chargebacks and higher employee satisfaction. South America records solid momentum as regulatory discussions in Argentina about wallet-based payroll catalyze platform partnerships, while Brazil and Colombia start to craft open-finance guidelines conducive to earned wage access expansion. In the Middle East, large expatriate workforces underpin adoption, exemplified by eight-figure joint ventures, whereas Africa remains nascent due to patchy instant-payment rails and varying consumer financial literacy.

- Payactiv Inc.

- Earnin, Inc.

- DailyPay Inc.

- Wagestream Holdings Limited

- Instant Financial USA Inc.

- FlexWage Solutions LLC

- Even Responsible Finance, Inc.

- Branch Technologies Inc.

- Rain Technologies Inc.

- ZayZoon Inc.

- Clair Inc.

- Hastee Technologies Limited

- SalaryFinance Limited

- Refyne Tech Private Limited

- Tapcheck Inc.

- FinFit Ops LLC

- Immediate Solutions, Inc.

- Payflow S.L.

- Line Financial PBC

- Instapay Technologies Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Earned Wage Access as a Financial-Wellness Benefit

- 4.2.2 Expansion of Real-Time Payments Infrastructure in Developed Markets

- 4.2.3 Increasing Gig-Economy Workforce Across Asia-Pacific

- 4.2.4 Intensifying Competition for Hourly Talent in Retail and Hospitality

- 4.2.5 Growing Strategic Partnerships Between FinTechs and Traditional Payroll Vendors

- 4.2.6 Emergence of Embedded-Finance APIs Enabling White-Label EWA

- 4.3 Market Restraints

- 4.3.1 Regulatory Ambiguity Around Lending vs. Non-Lending Classification

- 4.3.2 Data-Security and Privacy Concerns Among Large Enterprises

- 4.3.3 Limited Financial Literacy Slowing User Uptake in Africa

- 4.3.4 Interchange-Fee Compression Pressuring Unit Economics

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Delivery Model

- 5.1.1 Employer-Integrated Earned Wage Access (EWA)

- 5.1.2 Direct-to-Consumer Earned Wage Access (EWA)

- 5.1.3 Hybrid Models

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Retail and E-Commerce

- 5.4.2 Healthcare

- 5.4.3 Manufacturing

- 5.4.4 Hospitality and Food Service

- 5.4.5 Transportation and Logistics

- 5.4.6 Banking, Financial Services and Insurance (BFSI)

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Payactiv Inc.

- 6.4.2 Earnin, Inc.

- 6.4.3 DailyPay Inc.

- 6.4.4 Wagestream Holdings Limited

- 6.4.5 Instant Financial USA Inc.

- 6.4.6 FlexWage Solutions LLC

- 6.4.7 Even Responsible Finance, Inc.

- 6.4.8 Branch Technologies Inc.

- 6.4.9 Rain Technologies Inc.

- 6.4.10 ZayZoon Inc.

- 6.4.11 Clair Inc.

- 6.4.12 Hastee Technologies Limited

- 6.4.13 SalaryFinance Limited

- 6.4.14 Refyne Tech Private Limited

- 6.4.15 Tapcheck Inc.

- 6.4.16 FinFit Ops LLC

- 6.4.17 Immediate Solutions, Inc.

- 6.4.18 Payflow S.L.

- 6.4.19 Line Financial PBC

- 6.4.20 Instapay Technologies Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

嵌入式薪資核算和預支薪資服務市場預測至2034年-按解決方案類型、存取模式、交付管道、技術、應用、最終用戶和地區分類的全球分析

嵌入式薪資核算和預支薪資服務市場預測至2034年-按解決方案類型、存取模式、交付管道、技術、應用、最終用戶和地區分類的全球分析 2026年全球即時薪資取得市場報告2026年全球即時薪資存取(EWA)服務供應商市場報告2026年全球直接面對消費者的薪資預支(EWA)市場報告2026年全球行動工資取得應用市場報告2026年全球雇主提供薪資取得已賺收入市場報告

2026年全球即時薪資取得市場報告2026年全球即時薪資存取(EWA)服務供應商市場報告2026年全球直接面對消費者的薪資預支(EWA)市場報告2026年全球行動工資取得應用市場報告2026年全球雇主提供薪資取得已賺收入市場報告 薪資預支市場規模、佔有率、成長和全球產業分析:按類型、應用和地區分類的洞察,以及 2026-2034 年的預測。全球預支薪資軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

薪資預支市場規模、佔有率、成長和全球產業分析:按類型、應用和地區分類的洞察,以及 2026-2034 年的預測。全球預支薪資軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)