|

市場調查報告書

商品編碼

2073279

移民和簽證管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Immigration and Visa Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

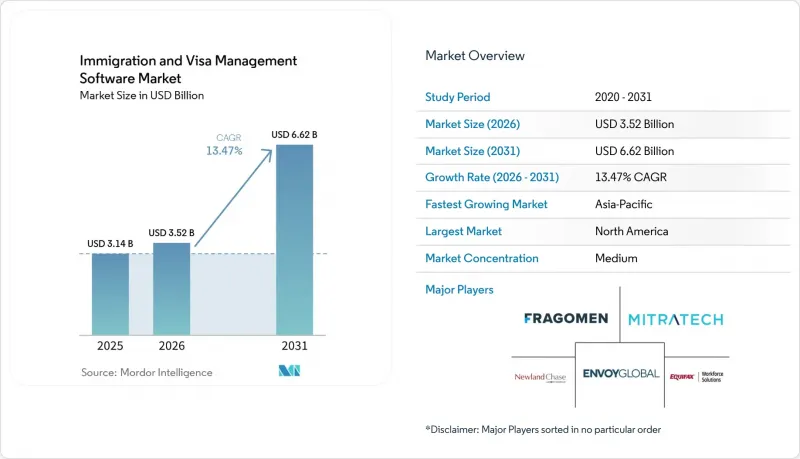

根據 Mordor Intelligence 預測,移民和簽證管理軟體市場預計將從 2025 年的 31.4 億美元成長到 2026 年的 35.2 億美元,到 2031 年達到 66.2 億美元,2026 年至 2031 年的複合年預計成長率為 13.47%。

本報告按元件(軟體和服務)、部署模式(雲端和本地部署)、應用程式(簽證和移民案件管理、合規管理等)、組織規模(大型企業和中小企業)、最終用戶(公司、律師事務所、教育機構等)以及地區進行細分。市場預測以價值(美元)表示。

全球移民和簽證管理軟體市場趨勢與洞察

雇主對簽證和工作許可自動化合規的需求日益成長。

隨著執法壓力的不斷加大,移民合規已成為跨國公司日常營運的挑戰,而非週期性的法律審查,這一轉變持續推動移民和簽證管理軟體市場的發展。 2025年1月生效的H-1B簽證現代化條例改變了擔保要求,並提高了對申請管理、文件追蹤以及雇主團隊內部協調的嚴格要求。在此背景下,人工流程成為一種風險因素,因為雇主需要完整的記錄,以便在當局要求提供證據或進行審計時能夠迅速提出。這項需求促使那些能夠在單一環境中整合案件狀態可見度、版本控制、截止日期提醒和可驗證稽核追蹤等功能的平台脫穎而出。因此,在雇主將違規不僅視為行政負擔,更視為業務中斷的領域,移民和簽證管理軟體市場正從中受益匪淺。

跨國招募和分散式勞動力的擴張

跨國招募正日益融入人才規劃,並不斷擴大移民和簽證管理軟體市場的使用者群體。跨國公司正日益整合招募、薪資核算、人才調動和移民流程,以最大限度地減少跨地域人才調配過程中的過渡環節和合規漏洞。這種需求體現在交易趨勢中,例如Payoneer於2026年1月收購Boundless,此舉將移民合規與跨國薪資核算、稅務和福利管理更直接地連結起來。 Fragomen和Papaya Global也在2026年5月採取了類似舉措,將移民相關專業知識與更廣泛的員工薪水支付工具和特定國家/地區知識工具相結合。這些發展表明,移民和簽證管理軟體市場不再局限於簽證申請,而是與更廣泛的全球僱用管理模式緊密相連。

高度敏感的移民資料的安全和隱私風險

高度敏感的移民記錄將身分資訊、國籍、法律地位以及通常的家庭狀況整合到一個系統中,這仍然是移民和簽證管理軟體市場的主要障礙。歐洲資料保護監管機構2025年針對移民管理系統管治議題的裁決,凸顯了資料保護領域對該領域的密切關注。在英國,圍繞內政部電子簽證環境的擔憂也使資料保護和資訊外洩風險在2025年受到正式關注。這種情況導致買方在簽訂合約前對資料儲存位置、身份驗證、存取控制和事件回應的成熟度提出了更高的要求。因此,無法證明其擁有強大安全管治的小規模供應商越來越難以進入移民和簽證管理軟體市場。

細分市場分析

到2025年,軟體市佔率將達到71.84%,仍是移民和簽證管理軟體的主要收入來源。這是因為雇主需要一個能夠集中管理案件、文件、里程碑事件和合規報告的系統。這一主導地位反映了從律師主導的人工管理模式轉變為技術主導的營運模式的趨勢,這種模式能夠實現跨多個司法管轄區的移民業務標準化。實際上,軟體發揮著「記錄系統」的作用,如果沒有它,買家將難以有效率地管理複雜的專案。這項基礎使得軟體層成為交叉銷售分析、行動應用、合規以及更廣泛的員工工作流程的切入點。

預計到2031年,服務市場將以14.72%的複合年成長率成長,這表明移民和簽證管理軟體的採用通常與實施支援、持續的合規支援、培訓和營運管理捆綁在一起。當雇主面臨監管變化並需要外部幫助快速重組流程時,這種趨勢尤其明顯。全端供應商具有優勢,因為買家往往更傾向於能夠整合技術、流程設計和持續專案支援的單一供應商。因此,在移民和簽證管理軟體產業,能夠將軟體與全面的管理服務打包,而不是僅依賴軟體的公司,更受青睞。

到2025年,雲端技術將佔據移民和簽證管理軟體市場73.42%的佔有率,這反映出雇主對遠端存取、易於部署、持續更新以及與現代人力資源系統無縫整合的重視。雲端模式非常適合這個市場,因為移民團隊、人力資源負責人、經理和外部合作夥伴通常需要從不同地點存取相同的案例記錄。在國家法規變化迅速的市場中,雲端模式比傳統的本地部署模式更快地回應法規更新,這一點也至關重要。因此,那些提供低准入門檻和模組化雲端工作流程的供應商在移民和簽證管理軟體市場正穩步獲得青睞。

預計到2031年,雲端運算市場將以14.04%的複合年成長率成長,這意味著在整個預測期內,雲端運算市場在規模和成長方面很可能保持領先地位。本地部署系統在政府機構、部分金融機構以及其他具有嚴格內部託管法規的環境中仍扮演著重要角色。然而,隨著買家對私有雲端雲和自主雲方案(能夠解決主要安全問題)的接受度不斷提高,本地部署系統的地位正在減弱。因此,在移民和簽證管理軟體市場,重心正進一步向雲端交付轉移,而本地部署解決方案仍然重要,主要體現在一些特定用例中。

區域分析

到2025年,北美將佔據移民和簽證管理軟體市場45.92%的佔有率,並繼續保持該地區最大市場的地位。這主要歸因於北美雇主在嚴格的執法環境下運營,且工作許可要求十分詳盡。在美國,H-1B簽證現代化法規於2025年1月生效,增加了雇主行政流程的複雜性,使得能夠系統地追蹤申請狀態、截止日期、薪資水平和合格標準的軟體更有價值。此外,在美國,I-9表格和E-Verify系統的廣泛應用,不僅針對那些擁有大規模簽證專案的整體,也為移民和簽證管理軟體市場的需求奠定了堅實的基礎。在加拿大,隨著使用技術純熟勞工移民計畫的雇主受益於更完善的文件管理和狀態可見性,相關需求也在不斷成長。墨西哥市場規模仍然小規模,但由於近岸服務交付和跨境僱用模式的興起,合規軟體的重要性正在逐步提升。

歐洲是受移民和簽證管理軟體市場監管影響最大的地區,而2026年的變化速度迫使買家迅速實現工作流程現代化。 2026年4月10日,歐盟範圍內的「出入境系統(EES)」全面實施。這使得雇主、承運商和旅遊相關企業更需要將行前程序和身分驗證流程與邊境管制要求更加緊密地結合。 2026年4月,歐盟委員會也確認了EES和ETIAS的區別和實施順序,這將進一步鼓勵在旅遊和合規營運方面加大數位化準備方面的投資。同時,滿足派遣工人的需求仍然是一個至關重要的問題,歐洲勞工局2025年針對派遣計畫下第三國國民的計劃凸顯了雇主在勞動力流動和移民管制交叉領域面臨的運作複雜性。這些因素使得歐洲成為移民和簽證管理軟體市場中最依賴系統的地區之一。

預計亞太地區將以16.02%的複合年成長率成長,到2031年,該地區預計將成為移民和簽證管理軟體市場規模成長最快的地區。這項需求主要受以下因素驅動:印度科技業的人才招聘、新加坡和澳洲的勞動力流動,以及日本和韓國中型企業對更規範合規體係日益成長的需求。澳洲和紐西蘭也出現了越來越多的採用,因為雇主擔保的工作簽證需要系統化的記錄保存和持續的流程管理。在亞太地區以外,南美洲仍處於起步階段,而中東地區則吸引了許多管理大規模外籍勞工和辦理大量工作許可的雇主的注意。非洲整體市場規模仍然小規模,但南非憑藉其在跨國人才流動和雇主主導流動模式中的作用,成為移民和簽證管理軟體市場中最先進的地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雇主對簽證和工作許可合規管理自動化的需求日益成長。

- 跨國招募和分散式勞動力的擴張

- 遷移到基於雲端和API整合的移民平台

- 需要符合審計要求的報告和人力資源資訊系統整合

- 商務旅行、臨時工和移民合規的交會點。

- EES、ETIAS 和數位邊境合規要求

- 市場限制因素

- 敏感移民資料的安全和隱私風險

- 舊有系統和分散的資料所有權阻礙了技術的普及應用。

- 人工智慧驅動的智慧邊境和政府監控正在增加審計風險。

- 入口網站原生提交方式的改變增加了維護負擔。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 透過使用

- 簽證和移民案件管理

- 合規管理

- 員工流動管理

- 報告與分析

- 其他應用程式工作流程

- 按組織規模

- 大公司

- SME

- 最終用戶

- 公司

- 律師事務所

- 政府和公共機構

- 教育機構

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Envoy Global, Inc.

- Fragomen, Del Rey, Bernsen & Loewy, LLP

- Equifax Workforce Solutions

- Newland Chase Limited

- Jobbatical OU

- Localyze GmbH

- Equus Software, LLC

- Topia, Inc.

- xPath Global Pty Ltd

- Centuro Global Limited

- Docketwise

- Cerenade

- Boundless Immigration Inc.

- SimpleCitizen, Inc.

- Almaca, Inc.

- Sapochnick Technologies Inc.

- Imagility LLC

- Mitratech, Inc.

- CIBT Global, Inc.

- LaborLess

- US Immigration AI

- ImmiOne

- ImmiCompliance

- VisaHQ.com, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the immigration and visa management software market size is expected to increase from USD 3.14 billion in 2025 to USD 3.52 billion in 2026 and reach USD 6.62 billion by 2031, growing at a CAGR of 13.47% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, and On-Premises), Application (Visa and Immigration Case Management, Compliance Management, and More), Organization Size (Large Enterprises, and SMEs), End-User (Corporates, Law Firms, Educational Institutions, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Immigration and Visa Management Software Market Trends and Insights

Rising Employer Demand for Automated Visa and Work Authorization Compliance

Heightened enforcement pressure is making immigration compliance a routine operating issue rather than a periodic legal review for multinational employers, and that shift continues to support the immigration and visa management software market. The January 2025 H-1B modernization rule changed sponsorship requirements and increased the need for tighter filing controls, document tracking, and internal coordination across employer teams. In this setting, manual processes create risk because employers need complete records that can be produced quickly when authorities request evidence or conduct audits. That requirement favors platforms that combine case status visibility, version control, deadline alerts, and defensible audit trails in one environment. As a result, the immigration and visa management software market is benefiting most where employers view compliance failure as a business disruption rather than only an administrative burden.

Expansion of Cross-Border Hiring and Distributed Workforces

Cross-border hiring is becoming more embedded in workforce planning, and that is widening the user base for the immigration and visa management software market. Multinational employers are increasingly trying to connect hiring, payroll, mobility, and immigration steps so that talent can be deployed across locations with fewer handoff points and fewer compliance gaps. This demand is also showing up in transaction activity, including Payoneer's January 2026 acquisition of Boundless, which tied immigration compliance more directly to cross-border payroll, taxes, and benefits administration. Fragomen and Papaya Global moved in a similar direction in May 2026 by linking immigration intelligence with broader workforce payment and country knowledge tools. These moves show why the immigration and visa management software market is no longer limited to visa filing alone and is increasingly tied to broader global employment operating models.

Sensitive Immigration Data Security and Privacy Risks

Sensitive immigration records remain a major barrier in the immigration and visa management software market because they combine identity data, nationality, legal status, and often family details in a single system. The European Data Protection Supervisor highlighted governance concerns around migration management systems in 2025, which reinforces how tightly this category is being scrutinized from a data protection perspective. In the United Kingdom, concerns around the Home Office eVisa environment also drew formal attention to data protection and disclosure risks in 2025. These conditions are raising buyer expectations around data residency, certification, access controls, and incident response maturity before contracts are signed. The result is that the immigration and visa management software market is becoming harder to enter for smaller vendors that cannot demonstrate strong security governance.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Cloud-Based and API-Integrated Immigration Platforms

- Need for Audit-Ready Reporting and HRIS Integration

- Legacy Systems and Fragmented Data Ownership Slow Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 71.84% of the market in 2025 and remained the main revenue base of the immigration and visa management software market because employers need a central system for cases, documents, milestones, and compliance reporting. That leadership reflects a broader move away from attorney-led manual administration toward technology-led operating models that can standardize immigration work across multiple jurisdictions. In practice, software functions as the system of record, which makes it difficult for buyers to manage complex programs efficiently without it. This foundation also makes the software layer the entry point for cross-sell into analytics, mobility, compliance, and broader workforce workflows.

Services are projected to expand at a 14.72% CAGR through 2031, which shows that adoption in the immigration and visa management software market is often paired with implementation help, ongoing regulatory support, training, and managed operations. This pattern is especially visible when employers face changing rules and need external support to reconfigure processes quickly. Full-stack vendors benefit because buyers often prefer one provider that can combine technology, process design, and ongoing program support. The immigration and visa management software industry is therefore rewarding companies that can package software with managed service depth rather than relying on software alone.

Cloud accounted for 73.42% of the immigration and visa management software market size in 2025, and this lead reflects the value employers place on remote access, easier deployment, continuous updates, and simpler integration with modern HR systems. The cloud model fits the market well because immigration teams, HR staff, managers, and external partners often need access to the same case record from different locations. It also supports faster regulatory updates than traditional on-premises models, which matters in a market where country requirements can shift quickly. As a result, the immigration and visa management software market is steadily favoring vendors that can deliver modular, cloud-based workflows with lower implementation friction.

Cloud is projected to grow at a 14.04% CAGR through 2031, which means it is likely to retain both scale leadership and growth leadership during the forecast period. On-premises systems still matter in government agencies, some financial institutions, and other environments with strict internal hosting rules. Even so, that position is weakening as buyers become more comfortable with private cloud and sovereign-cloud options that address core security concerns. The immigration and visa management software market is therefore seeing the center of gravity move further toward cloud delivery, while on-premises remains important mainly in specialized use cases.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- By Application

- Visa and Immigration Case Management

- Compliance Management

- Employee Mobility Management

- Reporting and Analytics

- Other Application Workflows

- By Organization Size

- Large Enterprises

- SMEs

- By End-User

- Corporates

- Law Firms

- Government and Public Sector Agencies

- Educational Institutions

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America accounted for 45.92% of the immigration and visa management software market share in 2025, and the region remained the largest geography because employers operate in a dense enforcement environment with detailed work authorization requirements. In the United States, the January 2025 H-1B modernization rule increased administrative complexity for employers and reinforced the value of software that can track filings, deadlines, wage levels, and eligibility conditions in a structured way. The United States also provides a durable demand floor for the immigration and visa management software market because I-9 and E-Verify obligations apply broadly across employers, not only to firms with large visa programs. Canada adds a related layer of demand because employers working through skilled migration streams benefit from better document management and status visibility. Mexico remains a smaller market, but nearshore service delivery and cross-border employment models are gradually making compliance software more relevant there as well.

Europe is a highly regulation-driven region for the immigration and visa management software market, and the pace of change in 2026 is pushing buyers to refresh workflows quickly. The Entry/Exit System became fully deployed across the EU on April 10, 2026, which increased the need for employers, carriers, and travel-linked operators to align pre-travel and identity processes more closely with border requirements. The European Commission also confirmed the distinction and sequencing between EES and ETIAS in April 2026, which further supports digital readiness investment across travel and compliance operations. At the same time, posted worker compliance remains an important adjacent need, and the European Labour Authority's 2025 work on third-country nationals under posting arrangements highlights the operational complexity employers face when labor mobility intersects with immigration controls. These factors are making Europe one of the most system-intensive areas of the immigration and visa management software market.

Asia-Pacific is projected to expand at a 16.02% CAGR, giving it the fastest regional growth in the immigration and visa management software market size through 2031. Demand is being supported by technology-sector hiring in India, workforce mobility flows in Singapore and Australia, and stronger interest from mid-sized employers in Japan and South Korea that now need more formal compliance systems. Australia and New Zealand also support adoption because employer-sponsored pathways require organized recordkeeping and recurring process control. Outside Asia-Pacific, South America remains earlier stage, while the Middle East is generating interest from employers that manage large expatriate workforces and high permit volumes. Africa is still a smaller market overall, but South Africa stands out as the region's clearest adoption point for the immigration and visa management software market because of its role in cross-border talent flows and employer-sponsored mobility patterns.

- Envoy Global, Inc.

- Fragomen, Del Rey, Bernsen & Loewy, LLP

- Equifax Workforce Solutions

- Newland Chase Limited

- Jobbatical OU

- Localyze GmbH

- Equus Software, LLC

- Topia, Inc.

- xPath Global Pty Ltd

- Centuro Global Limited

- Docketwise

- Cerenade

- Boundless Immigration Inc.

- SimpleCitizen, Inc.

- Almaca, Inc.

- Sapochnick Technologies Inc.

- Imagility LLC

- Mitratech, Inc.

- CIBT Global, Inc.

- LaborLess

- US Immigration AI

- ImmiOne

- ImmiCompliance

- VisaHQ.com, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Employer Demand for Automated Visa and Work Authorization Compliance

- 4.2.2 Expansion of Cross-Border Hiring and Distributed Workforces

- 4.2.3 Shift to Cloud-Based and API-Integrated Immigration Platforms

- 4.2.4 Need for Audit-Ready Reporting and HRIS Integration

- 4.2.5 Convergence of Business Travel, Posted Worker, and Immigration Compliance

- 4.2.6 EES, ETIAS, and Digital Border Readiness Requirements

- 4.3 Market Restraints

- 4.3.1 Sensitive Immigration Data Security and Privacy Risks

- 4.3.2 Legacy Systems and Fragmented Data Ownership Slow Adoption

- 4.3.3 Smart-Border and AI-Driven Government Scrutiny Raising Audit Exposure

- 4.3.4 Portal-Native Filing Changes Increase Maintenance Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.3 By Application

- 5.3.1 Visa and Immigration Case Management

- 5.3.2 Compliance Management

- 5.3.3 Employee Mobility Management

- 5.3.4 Reporting and Analytics

- 5.3.5 Other Application Workflows

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 SMEs

- 5.5 By End-User

- 5.5.1 Corporates

- 5.5.2 Law Firms

- 5.5.3 Government and Public Sector Agencies

- 5.5.4 Educational Institutions

- 5.5.5 Other End-Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Envoy Global, Inc.

- 6.4.2 Fragomen, Del Rey, Bernsen & Loewy, LLP

- 6.4.3 Equifax Workforce Solutions

- 6.4.4 Newland Chase Limited

- 6.4.5 Jobbatical OU

- 6.4.6 Localyze GmbH

- 6.4.7 Equus Software, LLC

- 6.4.8 Topia, Inc.

- 6.4.9 xPath Global Pty Ltd

- 6.4.10 Centuro Global Limited

- 6.4.11 Docketwise

- 6.4.12 Cerenade

- 6.4.13 Boundless Immigration Inc.

- 6.4.14 SimpleCitizen, Inc.

- 6.4.15 Almaca, Inc.

- 6.4.16 Sapochnick Technologies Inc.

- 6.4.17 Imagility LLC

- 6.4.18 Mitratech, Inc.

- 6.4.19 CIBT Global, Inc.

- 6.4.20 LaborLess

- 6.4.21 US Immigration AI

- 6.4.22 ImmiOne

- 6.4.23 ImmiCompliance

- 6.4.24 VisaHQ.com, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

智慧數位推理市場預測-全球分析(按組件、部署模式、技術、應用、最終用戶和地區分類)——2034年

智慧數位推理市場預測-全球分析(按組件、部署模式、技術、應用、最終用戶和地區分類)——2034年 2026年全球企業內部網路與企業外部網路市場報告2026年全球協作套件市場報告全球群組軟體市場報告(2026 年)

2026年全球企業內部網路與企業外部網路市場報告2026年全球協作套件市場報告全球群組軟體市場報告(2026 年) 工作空間交付網路市場規模、佔有率和成長分析:按組件類型、部署模式、組織規模、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測

工作空間交付網路市場規模、佔有率和成長分析:按組件類型、部署模式、組織規模、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測 工作空間交付網路市場報告:按類型、應用和地區分類 2026-2034 年

工作空間交付網路市場報告:按類型、應用和地區分類 2026-2034 年 全球會議室解決方案市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球會議室解決方案市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 會議室解決方案市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、安裝類型和解決方案分類案例管理軟體 (CMS) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類下一代行動安全演算法市場,全球預測至2032年-按演算法類型、組件、車輛類型、技術、應用、最終用戶和地區分類

會議室解決方案市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、安裝類型和解決方案分類案例管理軟體 (CMS) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類下一代行動安全演算法市場,全球預測至2032年-按演算法類型、組件、車輛類型、技術、應用、最終用戶和地區分類