|

市場調查報告書

商品編碼

2073160

食品加工與處理設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Food Processing and Handling Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

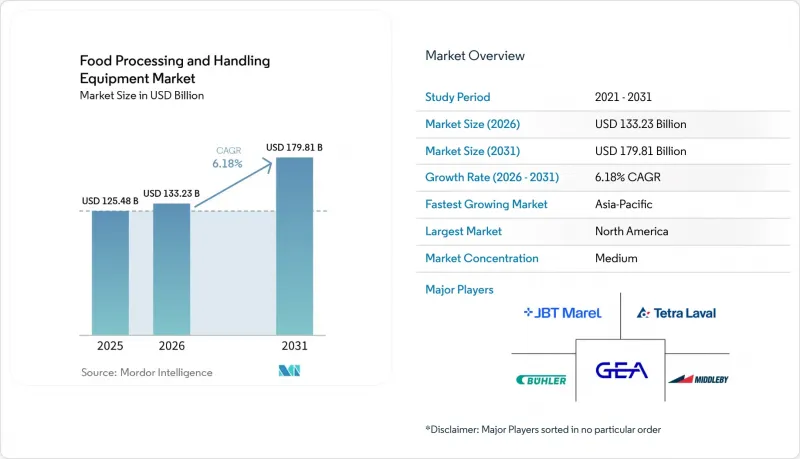

根據 Mordor Intelligence 預測,食品加工和處理設備市場規模預計將從 2025 年的 1,254.8 億美元成長到 2026 年的 1,332.3 億美元,到 2031 年將達到 1,798.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按設備類型(食品加工設備、食品包裝設備)、最終產品形態(固體、液體、半固體)、應用領域(肉類和家禽、烘焙和糖果甜點、乳製品、飲料及其他)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球食品加工及處理設備市場趨勢及洞察

對加工食品、包裝食品和加值食品的需求不斷成長

受已開發市場和新興市場對包裝食品和增值食品需求不斷成長的推動,食品加工和處理設備市場持續成長。預計到2025年,全球包裝食品市場將持續成長,其中亞太地區將佔據顯著佔有率。這反映出該地區生產能力的擴張和設備需求的增加。如今,人們的關注點已不再局限於單純的產量,機能性食品、植物來源蛋白和高階調理食品等品類需要更複雜的系統來進行處理、混合、熱處理和填充。雖然老舊的生產線仍能正常運轉,但其性能正在下降,導致市場更新換代週期縮短。目前,投資重點集中在能夠在同一工廠內應對頻繁的生產切換、更嚴格的品管和複雜產品要求的靈活平台。

食品製造中自動化和機器人技術的融合

食品製造商如今將提高勞動效率和生產線一致性視為首要任務,不僅作為改進目標,更將其視為必要的營運要求,從而推動了食品加工和處理設備市場的成長。 PMMI 和 FPSA 預測,到 2026 年,人工智慧驅動的檢測、基於人機介面 (HMI) 的知識轉移以及數位化工具的應用將成為美國食品飲料加工商的主要投資領域。加工商不再將機器人技術視為獨立的採購項目,而是將其整合到連接偵測、資料收集、機器回應和產品品質的系統中。這種方法縮短了自動化專案的投資回收期,尤其是在人手不足和熟練操作人員有限的地區。隨著投資回收期的縮短,對食品加工和處理設備的需求不斷成長,如今也包括了中型加工商。

嚴格的食品安全法規和合規成本

食品加工和處理設備市場正受益於更嚴格的標準,但滿足這些標準的成本仍然是小規模加工商面臨的阻礙因素。合規通常需要重新設計設備、進行額外的檢驗、更系統化的變更管理以及更詳盡的文件記錄,這延長了採購週期,並限制了用於性能改進的可自由支配支出。大型加工商可以透過增加產量來分攤這些成本,而中小企業在決定升級食品加工和處理設備時,則面臨利潤率較低的挑戰。這導致原始設備製造商 (OEM) 的訂單模式出現波動,因為一些客戶正在快速升級其生產線,而另一些客戶則推遲採購,專注於最小限度的維修。因此,市場出現了這樣一種局面:法規支持長期升級需求,但在短期內,它們可能會延遲將意圖轉化為最終訂單。

細分市場分析

至2025年,食品加工設備將佔食品加工和處理設備市場48.21%的佔有率。這一主導地位凸顯了產品加工關鍵製程的重要性,例如切割、研磨、混合和熱處理。與其他設備類別相比,這些製程的設備安裝數量更多,更換需求也更大。此外,提高衛生、自動化和生產效率的努力通常始於初級製作流程,然後擴展到工廠的其他環節。

從2026年到2031年,食品包裝設備產業預計將以6.7%的複合年成長率成長。這一成長主要得益於製造商採用可回收材料、產品形式多樣化以及生產批量縮小等舉措,從而帶動了對軟性灌裝、封口、貼標和生產線末端系統需求的成長。克朗斯股份公司(Krones AG)公佈,2025年銷售額為56.638億歐元,較2024年的52.936億歐元成長7.0%,反映出市場對包裝技術的強勁需求。根據德國機械設備製造業聯合會(VDMA)的報告,到2025年,包裝器材將佔德國食品機械出口總額的近70%,凸顯了其在全球市場的重要性。因此,包裝生產線正逐漸成為戰略資產,有助於加快新產品推出速度、提高材料適應性並提升勞動效率。

區域分析

至2025年,北美將佔全球食品加工和處理設備市場32.11%的佔有率。美國將在該地區發揮主導作用,食品和飲料機械出貨收益將達到62億美元,比2024年成長3.2%。市場重心正從新建工廠轉向現有設備的升級改造,從而推動了對自動化、可追溯性和更高加工能力的需求。專注於現有生產線維修、增強數位化可追溯性和提高勞動效率的供應商將從中受益。營運壓力帶來的升級需求正在支撐北美市場的成長。

歐洲仍是全球第二大食品加工和包裝器材市場,也是重要的出口樞紐。預計到2025年,德國食品和包裝器材產業的市場規模將達到170億歐元,其中110億歐元(84%)將用於出口。歐洲供應商與全球資本投資趨勢緊密相連。 「綠色新政」和「EXQUISHEAT」等政策正在推動對節能系統和最佳化製程佈局的需求。市場青睞具備應對力、衛生和持續合規性的高階系統,因此其較高的初始成本也物有所值。

亞太地區是成長最快的地區,預計2026年至2031年複合年成長率將達到8.34%。這一成長主要集中在中國、印度和東南亞,其驅動力包括加工食品產量增加、出口活動擴大以及對低溫運輸的投資。印度食品加工工業部已根據總理食品加工支援計畫(PMKSY)撥款65.2億印度盧比(約7.85億美元)用於低溫運輸和價值鏈基礎設施建設,該計畫的有效期至2026年3月。 JBT Marel位於浦那的全球生產中心將於2025年9月開業,顯示該地區製造業的重要性日益凸顯。儘管南美洲和中東及非洲的佔有率較小,但拉丁美洲佔全球食品出口的25%。 2026年5月簽署的阿布達比食品中心3.7萬平方公尺低溫運輸基礎設施合約表明,食品加工和處理設備的市場潛力正在不斷擴大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對加工食品、包裝食品和加值食品的需求不斷成長

- 食品製造中自動化和機器人技術的融合

- 人們越來越關注食品安全和衛生法規。

- 重視食品加工的永續性和能源效率

- 低溫運輸基礎設施和冷藏物流的擴張

- 加工和包裝設備的技術創新

- 市場限制因素

- 嚴格的食品安全法規和合規成本

- 設備維護的複雜性

- 高昂的維護和營運成本

- 供應鏈中斷與原物料價格波動

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依設備類型

- 食品加工設備

- 切割和切片設備

- 研磨和銑削設備

- 混合攪拌設備

- 均質機

- 擠出機

- 烹飪/加熱設備

- 巴氏殺菌和滅菌設備

- 乾燥/脫水設備

- 蒸發器和濃縮裝置

- 發酵裝置

- 食品包裝設備

- 食品加工設備

- 最終產品形式

- 固體的

- 液體

- 半固體

- 透過使用

- 麵包糖果甜點

- 肉類/家禽

- 魚貝類

- 乳製品

- 酒精飲料

- 不含酒精的飲料

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 波蘭

- 比利時

- 瑞典

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 韓國

- 泰國

- 新加坡

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 摩洛哥

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BAADER Group

- JBT Marel

- Buhler AG

- GEA Group Aktiengesellschaft

- Tetra Laval International SA

- The Middleby Corporation

- Krones AG

- Alfa Laval AB

- SPX Flow, Inc.

- The Huppmann Group

- Marel hf.

- Heat and Control, Inc.

- FENCO Food Machinery Srl

- Bigtem Makine AS

- TNA Australia Pty Limited

- Foodmate BV

- LEHUI Equipamientos Carnicos, SL

- Provisur Technologies, Inc.

- JBT Corporation

- Paul Mueller Company, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the food processing and handling equipment market is projected to grow from USD 125.48 billion in 2025 to USD 133.23 billion in 2026 and reach USD 179.81 billion by 2031, with a CAGR of 6.2% during 2026-2031.

This report is Segmented by Equipment Type (Food Processing Equipment, Food Packaging Equipment), End-Product Form (Solid, Liquid, Semi-Solid), Application (Meat and Poultry, Bakery and Confectionery, Dairy Products, Beverages, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Food Processing and Handling Equipment Market Trends and Insights

Rising Demand for Processed, Packaged, and Value-Added Food Products

The food processing and handling equipment market is growing alongside the rising demand for packaged and value-added foods in developed and emerging markets. In 2025, the global packaged food market experienced growth, with the Asia-Pacific region holding a significant share. This reflects the regions expanding manufacturing capacities and increasing equipment demand. The focus is shifting beyond volume, as categories like functional foods, plant-based proteins, and premium ready meals require advanced systems for handling, mixing, thermal treatment, and filling. Older production lines, though mechanically functional, are becoming less suitable, shortening replacement cycles in the market. Investments are now directed toward flexible platforms that support frequent changeovers, stricter quality controls, and complex product requirements within the same plant footprint.

Integration of Automation and Robotics in Food Manufacturing

Food manufacturers now prioritize labor efficiency and line consistency as essential operational needs rather than improvement goals, driving growth in the food processing and handling equipment market. By 2026, PMMI and FPSA identified AI-assisted inspection, HMI knowledge transfer, and digital tool adoption as key investment areas for U.S. food and beverage processors. Processors no longer view robotics as standalone purchases but integrate automation into systems connecting inspection, data capture, machine response, and output quality. This approach shortens the return window on automation projects, especially in regions with labor shortages and limited skilled operators. As payback periods shrink, demand for food processing and handling equipment is expanding, now including more mid-sized processors.

Stringent Food Safety Regulations and Compliance Costs

The food processing and handling equipment market benefits from stricter standards, but the cost of meeting them still acts as a restraint for smaller processors. Compliance work often requires equipment redesign, additional validation, more structured change control, and broader documentation, which stretches procurement cycles and limits discretionary spending on performance upgrades. Large processors can spread those costs across higher output volumes, while small and mid-sized operators face a narrower margin for replacement decisions in the food processing and handling equipment market. This creates uneven order patterns for OEMs because some customers move quickly to replace lines, while others delay purchases and focus on minimum viable retrofits. The result is a market where regulation supports long-term replacement demand but can also slow short-term conversion of interest into finalized orders.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Focus on Food Safety and Hygiene Regulations

- Emphasis on Sustainability and Energy Efficiency in Food Processing

- Supply Chain Disruptions and Raw Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, food processing equipment held a 48.21% share of the food processing and handling equipment market. This dominance highlights essential operations like cutting, grinding, mixing, and thermal treatment, which are crucial for product transformation. These processes result in a larger installed base and higher replacement needs compared to other equipment categories. Additionally, hygiene, automation, and productivity upgrades often start in primary processing before extending to other plant functions.

Between 2026 and 2031, the food packaging equipment segment is expected to grow at a 6.7% CAGR. This growth is driven by rising demand for flexible filling, sealing, labeling, and end-of-line systems as manufacturers adopt recyclable materials, diversify formats, and shorten production runs. Krones AG reported EUR 5,663.8 million in revenue in 2025, a 7.0% increase from EUR 5,293.6 million in 2024, reflecting strong demand for packaging technology. VDMA reported that packaging machines accounted for nearly 70% of Germany's food machinery exports in 2025, emphasizing their global importance. As a result, packaging lines are evolving into strategic assets, improving launch speeds, material adaptability, and labor efficiency.

Complete Report Scope:

- By Equipment Type

- Food Processing Equipment

- Cutting and slicing equipment

- Grinding and milling equipment

- Mixing and blending equipment

- Homogenizers

- Extruders

- Cooking and heating equipment

- Pasteurization and sterilization equipment

- Drying and dehydration equipment

- Evaporators and concentrators

- Fermentation equipment

- Food Packaging Equipement

- Food Processing Equipment

- By End-Product Form

- Solid

- Liquid

- Semi-solid

- By Application

- Bakery and Confectionery

- Meat and Poultry

- Fish and Seafood

- Dairy Products

- Alcoholic Beverages

- Non-alcoholic Beverages

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

In 2025, North America accounted for 32.11% of the food processing and handling equipment market. The U.S. led the region, with food and beverage machinery shipments reaching USD 6.2 billion, a 3.2% increase from 2024. The focus has shifted to brownfield upgrades over new plant construction, driving demand for automation, traceability, and throughput improvements. Suppliers specializing in retrofitting existing lines, enhancing digital traceability, and improving labor efficiency are benefiting. Replacement demand, driven by operational pressures, sustains North America's market growth.

Europe remains the second-largest market and a key export hub for food processing and packaging machinery. Germany's food and packaging machinery sector reached EUR 17 billion in 2025, with 84% exported, totaling EUR 11 billion. European suppliers are closely tied to global capital spending trends. Policies like the Green Deal and EXQUISHEAT program are boosting demand for energy-efficient systems and optimized process layouts. The market leans toward premium systems offering energy savings, hygiene readiness, and compliance durability, justifying higher upfront costs.

Asia-Pacific is the fastest-growing region, projected to grow at an 8.34% CAGR from 2026 to 2031. Growth is concentrated in China, India, and Southeast Asia, driven by rising processed food production, export activities, and cold chain investments. India's Ministry of Food Processing Industries allocated INR 6,520 crore (USD 785 million) for cold chain and value addition infrastructure under PMKSY through March 2026. JBT Marel's Global Production Center, launched in Pune in September 2025, highlights the region's growing manufacturing importance. While South America and the Middle East & Africa hold smaller shares, Latin America contributes 25% to global food exports. Abu Dhabi Food Hub's 37,000 sqm cold chain infrastructure deal in May 2026 signals expanding market potential for food processing and handling equipment.

- BAADER Group

- JBT Marel

- Buhler AG

- GEA Group Aktiengesellschaft

- Tetra Laval International S.A.

- The Middleby Corporation

- Krones AG

- Alfa Laval AB

- SPX Flow, Inc.

- The Huppmann Group

- Marel hf.

- Heat and Control, Inc.

- FENCO Food Machinery S.r.l.

- Bigtem Makine A.S.

- TNA Australia Pty Limited

- Foodmate B.V.

- LEHUI Equipamientos Carnicos, S.L.

- Provisur Technologies, Inc.

- JBT Corporation

- Paul Mueller Company, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for processed, packaged, and value-added food products

- 4.2.2 Integration of automation and robotics in food manufacturing

- 4.2.3 Increasing focus on food safety and hygiene regulations

- 4.2.4 Emphasis on sustainability and energy efficiency in food processing

- 4.2.5 Expansion of cold chain infrastructure and refrigerated logistics

- 4.2.6 Technological innovation in processing and packaging equipment

- 4.3 Market Restraints

- 4.3.1 Stringent food safety regulations and compliance costs

- 4.3.2 Equipment maintenance complexities

- 4.3.3 High maintenance and operational costs

- 4.3.4 Supply chain disruptions and raw material price volatility

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Food Processing Equipment

- 5.1.1.1 Cutting and slicing equipment

- 5.1.1.2 Grinding and milling equipment

- 5.1.1.3 Mixing and blending equipment

- 5.1.1.4 Homogenizers

- 5.1.1.5 Extruders

- 5.1.1.6 Cooking and heating equipment

- 5.1.1.7 Pasteurization and sterilization equipment

- 5.1.1.8 Drying and dehydration equipment

- 5.1.1.9 Evaporators and concentrators

- 5.1.1.10 Fermentation equipment

- 5.1.2 Food Packaging Equipement

- 5.1.1 Food Processing Equipment

- 5.2 By End-Product Form

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.2.3 Semi-solid

- 5.3 By Application

- 5.3.1 Bakery and Confectionery

- 5.3.2 Meat and Poultry

- 5.3.3 Fish and Seafood

- 5.3.4 Dairy Products

- 5.3.5 Alcoholic Beverages

- 5.3.6 Non-alcoholic Beverages

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Products, Recent Developments)

- 6.4.1 BAADER Group

- 6.4.2 JBT Marel

- 6.4.3 Buhler AG

- 6.4.4 GEA Group Aktiengesellschaft

- 6.4.5 Tetra Laval International S.A.

- 6.4.6 The Middleby Corporation

- 6.4.7 Krones AG

- 6.4.8 Alfa Laval AB

- 6.4.9 SPX Flow, Inc.

- 6.4.10 The Huppmann Group

- 6.4.11 Marel hf.

- 6.4.12 Heat and Control, Inc.

- 6.4.13 FENCO Food Machinery S.r.l.

- 6.4.14 Bigtem Makine A.S.

- 6.4.15 TNA Australia Pty Limited

- 6.4.16 Foodmate B.V.

- 6.4.17 LEHUI Equipamientos Carnicos, S.L.

- 6.4.18 Provisur Technologies, Inc.

- 6.4.19 JBT Corporation

- 6.4.20 Paul Mueller Company, Inc.