|

市場調查報告書

商品編碼

2073111

印度油脂化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Oleochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

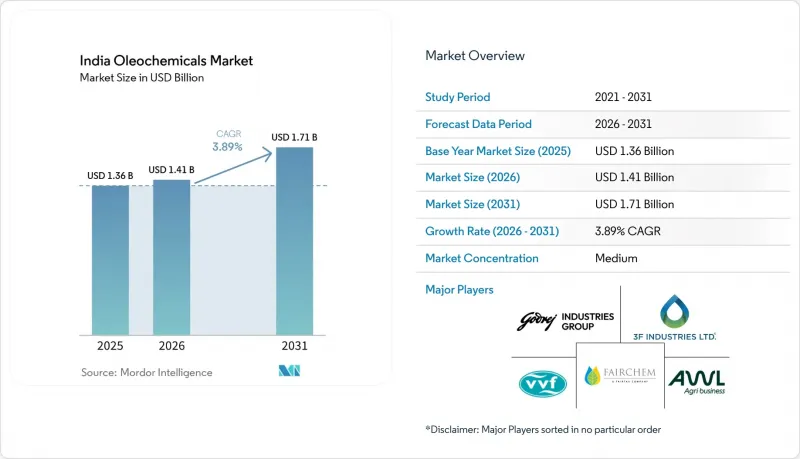

據 Mordor Intelligence 稱,2025 年印度油脂化學品市場價值為 13.6 億美元,預計到 2031 年將從 2026 年的 14.1 億美元成長至 17.1 億美元,預測期(2026-2031 年)複合年成長率為 3.89%。

本報告按產品類型(脂肪酸甲酯、脂醇類、甘油、脂肪酸及其他)、應用領域(醫藥及個人護理、肥皂及清潔劑、食品飲料、聚合物及其他)和原料(棕櫚油基、大豆油及其衍生物、蓖麻油基、動物脂肪)進行分類。市場預測以美元計價。

印度油脂化學品市場趨勢與洞察

個人護理需求激增

隨著個人護理市場的擴張,配方研發人員擴大用其他成分取代硫酸鹽類成分以滿足潔淨標示的要求,從而催生了對C12-C14脂醇類的新需求。印度標準局(BIS)於2025年修訂了IS 4707標準,對重金屬含量設定了限制並收緊了pH值範圍。這迫使一些規模較小的品牌採用符合RSPO標準的原料。黑田印度公司位於達赫傑的工廠於2026年3月投產,供應經EXCiPACT認證的酯類產品,售價比一般產品高出15-20%。這顯示市場對高品質原料的需求持續旺盛。二、三線城市居民可支配收入的成長推動了人均消費,而國際品牌則利用印度的成本優勢出口經認證的油脂化學品。因此,隨著符合規範的等級產品取代通用原料,印度油脂化學品市場不僅在數量上擴張,而且在價值上也擴張,這促成了中期複合年成長率達到 0.8 個百分點。

關於生物柴油和可再生化學品的強制性規定

2026年4月,E20乙醇混合燃料將開始投入生產。這將使脂肪酸甲酯從界面活性劑領域轉向生物柴油領域。 Universal Biofuels公司在卡基納達運作一座年產能8,000萬加侖的工廠,並已獲得價值1.03億美元的訂單,將於2024年向石油分銷商交付。預計2025-2026年將增加訂單。生質柴油使用量每增加1個百分點,市場將吸收約5萬至6萬噸的脂肪酸甲酯,所產生的價格差異將促使清潔劑領域以脂醇類。這種短期供應短缺將使印度油脂化學品市場的複合年成長率提高1.2個百分點,這將使能夠靈活切換脂肪酸甲酯和脂肪酸生產的綜合煉油廠受益。

棕櫚油價格波動

2025年,棕櫚油基油脂佔原料佔有率的56.41%,但由於馬來西亞和印尼將部分供應轉向國內生質柴油生產,進口量降至710萬噸,為15年來最低水準。依賴棕櫚油衍生原料的肥皂和清潔劑生產商在2025年至2026年價格飆升期間,其息稅折舊攤銷EBITDA獲利率)下降了200-300個基點(bps)。以大豆油取代棕櫚油可以起到一定的風險對沖作用,但阿根廷的出口政策和南美洲的氣候是新的影響因素。這種負面影響將使印度油脂化學品市場的複合年成長率(CAGR)下降0.3個百分點。

細分市場分析

截至2025年,脂肪酸甲酯佔印度油脂化學品市場規模的34.76%,但隨著清潔劑生產商將中檔配方提高10%,預計脂醇類市場在預測期(2026-2031年)內將以4.66%的複合年成長率更快成長。 Godrage公司投資750印度盧比(約9000萬美元)的擴建項目將使脂醇類產量翻番,特種產品產能翻兩番,目標是溢價15-20%的無硫酸鹽洗髮精。 VVF公司位於塔羅賈的工廠(亞洲最大的工廠)正透過向90個國家出口產品,持續擴大其在印度油脂化學品市場的佔有率。

由於中國產甘油以每噸620至680美元的價格大量湧入市場,而通用甘油又面臨供應過剩,戈德瑞公司正轉向使用USP級產品,這些產品仍然具有顯著的價格優勢。費爾凱姆公司利用酸性油脂廢棄物加工的特殊脂肪酸,例如二聚體和異硬脂酸,售價比普通甘油高出50%至100%,從而保護了利潤率免受棕櫚油價格波動的影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 個人護理需求激增

- 強制使用生質柴油和可再生化學品

- 包裝食品加工的擴張

- 日本植物油綜合精煉

- 將採購轉移到印度,作為「中國+1」策略的一部分

- 市場限制因素

- 棕櫚油價格波動

- 具成本競爭力的石油化學產品替代品

- 對高純度特種酯的進口依賴

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品

- 脂肪酸甲酯

- 脂醇類

- 甘油

- 脂肪酸

- 其他

- 透過使用

- 藥物和個人護理

- 肥皂和清潔劑

- 食品/飲料

- 聚合物

- 其他

- 按原料

- 棕櫚油和脂肪

- 大豆油及其衍生物

- 蓖麻油基油

- 動物油脂

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- South India Krishna Oil & Fats Pvt. Ltd.(SIKOF)

- 3F Industries LTD

- AAK

- Adani Wilmar Ltd(AWL)

- Croda India Ltd.

- Emery Oleochemicals

- Fairchem Organics Limited

- Fine Organic Industries Limited.

- Godrej Industries Limited

- India Glycols Ltd(IGL)

- Jocil Limited.

- KLK OLEO

- Muez Hest

- Oleon NV

- Pan Oleo

- Patanjali Foods Ltd

- SPIC

- Universal Biofuels Private Limited

- VVF Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india oleochemicals market size was valued at USD 1.36 billion in 2025 and is estimated to grow from USD 1.41 billion in 2026 to reach USD 1.71 billion by 2031, at a CAGR of 3.89% during the forecast period (2026-2031).

This report is Segmented by Product (Fatty Acid Methyl Esters, Fatty Alcohol, Glycerin, Fatty Acid, and Others), Application (Pharmaceuticals and Personal Care, Soap and Detergents, Food and Beverages, Polymers, and Others), and Feedstock (Palm-Based Oils, Soybean Oil and Derivatives, Castor-Based Oils, and Animal Tallow). The Market Forecasts are Provided in Terms of Value (USD).

India Oleochemicals Market Trends and Insights

Personal-Care Demand Surge

The personal-care upswing channels new volumes into C12-C14 fatty alcohols as formulators replace sulfates to meet clean-label claims. The Bureau of Indian Standards updated IS 4707 in 2025, capping heavy metals and tightening pH ranges, which forces smaller brands to qualify RSPO-compliant inputs. Croda India's Dahej facility, opened in March 2026, supplies EXCiPACT-certified esters that sell at 15-20% premiums, signaling sustained appetite for high-grade inputs. Rising disposable income in tier-2 and tier-3 cities lifts per-capita consumption, while international brands leverage India's cost base to export certified oleochemicals. The India oleochemicals market, therefore, expands not only in volume but in value as compliant grades displace commodity inputs, reinforcing a medium-term CAGR lift of 0.8 percentage points.

Biodiesel and Renewable-Chemicals Mandates

April 2026 marks the operational start of E20 ethanol blending, which diverts fatty acid methyl esters away from surfactant pools into biodiesel. Universal Biofuels already runs an 80-million-gallon-per-year plant at Kakinada and has booked USD 103 million in 2024 deliveries to oil marketing companies, with higher volumes scheduled for 2025-2026. Each 1-percentage-point rise in biodiesel use removes roughly 50,000-60,000 tons of methyl esters, prompting price spreads that encourage fatty alcohol substitution in detergents. The short-term squeeze adds 1.2 percentage points to the India oleochemicals market CAGR, rewarding integrated refiners that can swing between methyl esters and fatty acids.

Palm-Oil Price Volatility

Palm-based oils held 56.41% feedstock share in 2025, yet imports fell to a 7.1 million-ton, 15-year low as Malaysia and Indonesia diverted supply to domestic biodiesel. Soap and detergent makers reliant on palm derivatives saw EBITDA margins compress 200-300 basis points (bps) during 2025-2026 spikes. Substituting soybean oil provides some hedge, but Argentine export policies and South American weather add fresh volatility. The net drag slices 0.3 percentage points from the India oleochemicals market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Packaged-Food Processing

- Integrated Domestic Vegetable-Oil Refining

- Cost-Competitive Petrochemical Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fatty acid methyl esters commanded 34.76% share of India oleochemicals market size in 2025, yet fatty alcohol value will rise faster at a 4.66% CAGR during the forecast period (2026-2031) as detergent makers increase mid-cut loading by 10%. Godrej's INR 750 crore (approximately USD 90 million) expansion doubles fatty alcohol output and quadruples specialty capacity, targeting sulfate-free shampoos priced at 15-20% premiums. VVF's Taloja plant, Asia's largest, strengthens India oleochemicals market share in exports across 90 countries.

Commodity glycerin faces oversupply as Chinese cargoes land at USD 620-680/ton, so Godrej pivots to USP-grade units where price spreads remain strong. Specialty fatty acids such as dimer and isostearic, processed by Fairchem from acid-oil waste, earn 50-100% premiums and insulate margins from palm volatility.

Complete Report Scope:

- By Product

- Fatty Acid Methyl Esters

- Fatty Alcohol

- Glycerin

- Fatty Acid

- Others

- By Application

- Pharmaceuticals and Personal Care

- Soap and Detergents

- Food and Beverages

- Polymers

- Others

- By Feedstock

- Palm-based Oils

- Soybean Oil and Derivatives

- Castor-based Oils

- Animal Tallow

List of Companies Covered in this Report:

- South India Krishna Oil & Fats Pvt. Ltd. (SIKOF)

- 3F Industries LTD

- AAK

- Adani Wilmar Ltd (AWL)

- Croda India Ltd.

- Emery Oleochemicals

- Fairchem Organics Limited

- Fine Organic Industries Limited.

- Godrej Industries Limited

- India Glycols Ltd (IGL)

- Jocil Limited.

- KLK OLEO

- Muez Hest

- Oleon NV

- Pan Oleo

- Patanjali Foods Ltd

- SPIC

- Universal Biofuels Private Limited

- VVF Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Personal-care demand surge

- 4.2.2 Biodiesel and renewable-chemicals mandates

- 4.2.3 Expanding packaged-food processing

- 4.2.4 Integrated domestic vegetable-oil refining

- 4.2.5 China-plus-one sourcing shift into India

- 4.3 Market Restraints

- 4.3.1 Palm-oil price volatility

- 4.3.2 Cost-competitive petrochemical substitutes

- 4.3.3 Import dependence on high-purity specialty esters

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Fatty Acid Methyl Esters

- 5.1.2 Fatty Alcohol

- 5.1.3 Glycerin

- 5.1.4 Fatty Acid

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Pharmaceuticals and Personal Care

- 5.2.2 Soap and Detergents

- 5.2.3 Food and Beverages

- 5.2.4 Polymers

- 5.2.5 Others

- 5.3 By Feedstock

- 5.3.1 Palm-based Oils

- 5.3.2 Soybean Oil and Derivatives

- 5.3.3 Castor-based Oils

- 5.3.4 Animal Tallow

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 South India Krishna Oil & Fats Pvt. Ltd. (SIKOF)

- 6.4.2 3F Industries LTD

- 6.4.3 AAK

- 6.4.4 Adani Wilmar Ltd (AWL)

- 6.4.5 Croda India Ltd.

- 6.4.6 Emery Oleochemicals

- 6.4.7 Fairchem Organics Limited

- 6.4.8 Fine Organic Industries Limited.

- 6.4.9 Godrej Industries Limited

- 6.4.10 India Glycols Ltd (IGL)

- 6.4.11 Jocil Limited.

- 6.4.12 KLK OLEO

- 6.4.13 Muez Hest

- 6.4.14 Oleon NV

- 6.4.15 Pan Oleo

- 6.4.16 Patanjali Foods Ltd

- 6.4.17 SPIC

- 6.4.18 Universal Biofuels Private Limited

- 6.4.19 VVF Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球特種油脂及化學品市場

全球特種油脂及化學品市場 油脂化學品市場:按產品、應用和地區分類

油脂化學品市場:按產品、應用和地區分類 油脂化學品市場:2026-2032年全球市場預測(依產品類型、原料、通路、形態及最終用途產業分類)

油脂化學品市場:2026-2032年全球市場預測(依產品類型、原料、通路、形態及最終用途產業分類) 全球油脂化學品市場的規模、佔有率、成長和產業分析:按類型、應用和地區的洞察,2026-2034年的預測

全球油脂化學品市場的規模、佔有率、成長和產業分析:按類型、應用和地區的洞察,2026-2034年的預測 油脂化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

油脂化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 油脂化學品市場報告:按類型、形態、應用、原料和地區分類(2026-2034年)全球油脂化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

油脂化學品市場報告:按類型、形態、應用、原料和地區分類(2026-2034年)全球油脂化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026 年全球油脂化學品市場報告2026年全球特種油脂化學品市場報告

2026 年全球油脂化學品市場報告2026年全球特種油脂化學品市場報告 全球油脂化學品市場,2026-2030

全球油脂化學品市場,2026-2030