|

市場調查報告書

商品編碼

2073104

政府和公共部門綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)Government and Public Sector Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

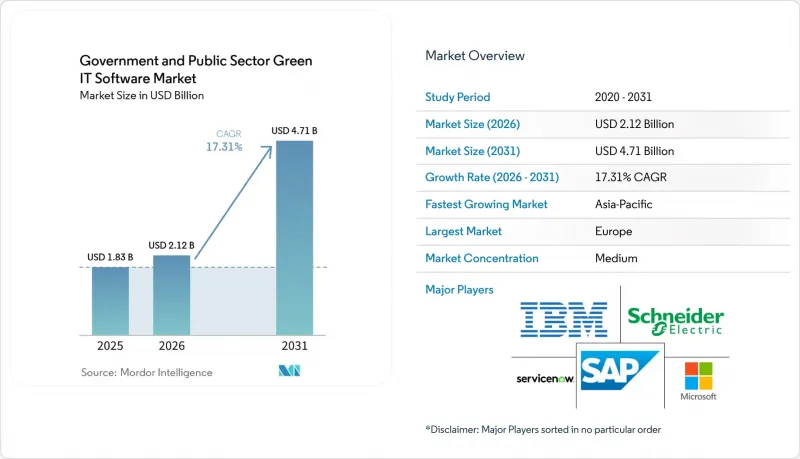

據 Mordor Intelligence 稱,政府和公共部門的綠色 IT 軟體市場預計將從 2025 年的 18.3 億美元成長到 2026 年的 21.2 億美元,到 2031 年達到 47.1 億美元,預計 2026 年至 2031 年的複合成長率為 17.31%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、最終用戶(中央和聯邦政府、州和地方政府、公共產業機構及其他)、應用領域(碳資料收集和揭露及其他)以及地區進行細分。市場預測以美元計價。

全球綠色IT軟體市場趨勢及對政府和公共部門的洞察

公共部門淨零排放採購要求重組合約標準

公共採購法規正推動政府和公共部門綠色IT軟體市場從自願報告轉向具有合約約束力的排放報告。在英國,PPN 006適用於2025年2月24日之後公佈的大型政府契約,要求契約金額超過500萬英鎊(659萬美元)的供應商提交碳減排計劃,作為參與契約的條件。這項要求正在改變對軟體的需求,因為各機構需要能夠讓採購團隊以檢驗格式收集、儲存和呈現供應商營運排放資料的系統。這也意味著採購、法律、財務和永續發展團隊將在同一工作流程中協作,凸顯了集中式報告和審計追蹤在政府和公共部門綠色IT軟體市場中的價值。因此,在各機構評估競標時,已經符合正式公共採購流程的供應商將獲得競爭優勢,這與功能豐富性同等重要。

政府推行的數位現代化政策正在加速平台整合。

隨著永續性要求融入更廣泛的技術現代化挑戰,政府和公共部門綠色IT軟體市場的數位現代化專案預算範圍正在擴大。英國環境、食品和農村事務部 (Defra) 的《2025-2030年數位永續發展策略》設定了到2030年將IT相關碳排放減少16%的目標,要求年合約金額超過100萬英鎊(132萬美元)的數位提供服務業者提交檢驗的碳足跡和淨零排放計畫。根據該策略,Defra集團的IT營運將在2024年產生1萬噸二氧化碳當量排放,佔該部門總排放的13%。這表明,軟體驅動的追蹤和管理在IT管理中變得越來越重要。在美國,GSA(美國總務署)與SAP於2025年12月簽署的「OneGov」協議將為聯邦政府機構提供資料庫、整合、分析和雲端工具高達80%的整體,預計可節省1.65億美元。此舉有利於已納入已批准採購和企業技術體系的供應商,從而推動政府和公共部門整個綠色IT軟體市場的平台整合。

預算和採購週期的分割會延緩酌情執行。

年度預算結構持續阻礙政府和公共部門綠色IT軟體市場的成長。這是因為永續發展工具往往與同一資金籌措週期內的高優先IT專案存在競爭。在許多機構中,網路安全、人力資源系統和舊有系統現代化改造在預算審查期間仍然優先於碳管理平台,導致即使指令明確,實施也會出現延誤。美國總務管理局 (GSA) 與 SAP 簽訂的「OneGov」合約原本有望透過大幅折扣降低實施成本,節省1.65億美元,但該合約也表明,較短的採購週期會影響實施進度和續約風險。地方政府層級也存在類似的挑戰。市、縣和州的預算時間表通常與國家報告要求不一致,導致政策要求在預算批准前就已生效。能夠提供分階段部署、試點範圍和模組化定價的供應商非常適合幫助政府和公共部門應對綠色IT軟體市場中的這些限制。

細分市場分析

到2025年,碳會計和報告軟體將佔據政府和公共部門綠色IT軟體市場28.74%的佔有率,成為預測期初最大的解決方案類型。這一領先地位反映了公共機構實際的營運流程,因為它們必須先建立可衡量和可審計的排放基準,然後才能設定減排目標、比較供應商或證明與津貼相關的資訊揭露的合理性。此外,隨著合規義務的擴大,審計可追溯性和結構化記錄的重要性與使用者功能不相上下,因此,政府採購負責人對系統的評估方式也對此類別有所好處。 SAP在2026年5月宣布其碳計量解決方案再次接受了IDC MarketScape的評估,這凸顯了ERP原生架構的吸引力,這種架構能夠更緊密地將排放記錄與財務管理實踐相結合。

能源和電力管理軟體也正與這個主要類別一起受到關注。這是因為各組織比以往任何時候都更迫切地需要將永續發展工作與營運效率和資料中心效能目標連結起來。綠色採購和供應商永續性管理軟體預計到2031年將以18.12%的複合年成長率成長,成為此解決方案類別中成長最快的領域。 EcoVadis和Workiva於2026年5月建立的合作夥伴關係,充分說明了為何該類別如此快速成長。供應商碳排放數據不再局限於單一採購系統,而是與可審計的報告更直接關聯起來。此外,隨著政府機構需要一個統一的環境來集中管理會計、採購和營運訊息,而無需重複進行人工匯總,永續性資料管理平台的重要性也日益凸顯。

到2025年,雲端採用將佔政府和公共部門綠色IT軟體市場收入的65.41%,顯著超越其他部署模式。政府機構傾向於盡可能採用雲端技術,因為訂閱模式可以縮短合規時間,並允許他們將規則更新、維護和發布管理工作外包給供應商。這對公共部門至關重要,因為公共部門的內部IT團隊通常面臨資源限制,需要能夠維持最新狀態而無需大規模重新配置的軟體。此外,雲端技術也符合政府現代化計畫的更廣泛趨勢,這些計畫透過利用協商採購管道和已通過核准的平台來加速雲端技術的採用。

預計2026年至2031年間,混合部署的複合年成長率將達到17.95%,並有望成為成長最快的模式,因為買家需要在快速合規和敏感資料管理之間取得平衡。歐盟委員會的「主權雲端框架」和法國2026年旨在減少歐洲對外部資源依賴的指令,透過提高公共部門資料儲存和處理的標準,正在推動這種穩健的模式。因此,即使本地部署不再是成長的主要驅動力,但對於擁有國防、國家安全和嚴格運營資料法規的機構而言,它仍然是一個至關重要的選擇。由於主權要求依然存在,能夠無縫地在本地環境和合規雲層之間遷移資料的供應商,預計將在政府和公共部門綠色IT軟體市場中獲得更大的佔有率。

區域分析

到2025年,歐洲將繼續保持在區域市場的領先地位,佔據政府和公共部門綠色IT軟體市場34.56%的佔有率。這一地位得益於其完善的政策環境,在該環境中,環境合規、採購管理和數位管治不再是各自獨立的問題,而是相互整合。歐盟委員會的「主權雲端框架」將環境永續性作為公共雲端採購的評估標準之一,同時繼續將主權保障置於採用決策的核心。英國透過其《公共採購和數位永續性條例》進一步推動了這一趨勢,該條例對供應商和政府部門的IT營運提出了正式要求。因此,歐洲既擁有廣泛的合規壓力,也具備能夠引導支出流向已做好接受公共部門審查準備的供應商的採購系統。

預計到2025年,北美將成為政府和公共部門綠色IT軟體的第二大區域市場。在美國,集中採購模式對軟體的普及應用有著顯著的影響,使得主要供應商能夠比與各機構單獨達成協議更快地進入聯邦政府的系統環境。美國總務管理局(GSA)與SAP之間的「OneGov」協議表明,聯邦機構可以透過協商折扣和通用的採購條款來擴展其對分析、整合和雲端功能的存取。雖然這種機制支援大規模部署,但也為專業工具留出了空間,這些工具可以在主平台之外,為供應商、資產或資訊揭露提供更高級的功能。

預計亞太地區在2026年至2031年間將以18.45%的複合年成長率成長,成為政府和公共部門綠色IT軟體市場成長最快的區域市場。該地區正從政策規劃轉向實施,推動了對碳計量、生命週期追蹤和採購導向報告工具的需求成長。 NTT集團於2026年3月發布的軟體生命週期二氧化碳運算標準,反映了亞太地區已開發市場軟體相關排放標準化的趨勢。儘管南美洲和中東及非洲目前的市場規模較小,但Khazna、Agility和阿拉伯聯合大公國能源與基礎設施部聯合宣布的阿拉伯聯合大公國試點計畫表明,政府能源管理正在這兩個最大的地區之外積極實施。這預示著未來在歐洲和北美以外地區的擴張很可能首先從有針對性的公共計畫開始,然後隨著各機構內部能力的提升和對採購理解的加深而逐步擴展。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府強制推行數位化現代化

- 公共部門淨零排放採購要求

- 資料中心面臨電力價格和能源成本上漲的壓力

- 各機構向自動化永續發展報告轉型

- 公共機構傳統IT碳排放視覺化的不足

- 津貼計畫中可審計碳數據的需求

- 市場限制因素

- 分段式傳統採購與預算週期

- 資料主權和公共雲端授權方面的限制

- 軟體檢驗和變更管理所需時間很長。

- 我公司在ESG和碳計量。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按解決方案類型

- 碳核算和報告軟體

- 能源和發電管理軟體

- IT資產生命週期管理軟體

- 永續性資料管理平台

- 綠色採購和供應商永續管理軟體

- 按實現類型

- 雲

- 現場

- 混合

- 最終用戶

- 中央和聯邦政府

- 州/地方政府

- 公共產業及公共機構

- 公立教育機構及公立醫療機構

- 透過使用

- 碳數據的收集和披露

- 能源最佳化和工作負載調度

- 利用IT資產並最佳化其生命週期

- 公共採購和供應商排放追蹤

- 合規、稽核和ESG工作流程的自動化

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Persefoni AI Inc.

- Cority Software Inc.

- Dakota Software Corporation

- Enablon SA

- Enviance, Inc.

- IBM Corporation

- Johnson Controls International plc

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Schneider Electric SE

- ServiceNow, Inc.

- Siemens AG

- Sphera Solutions, Inc.

- Sustainability Software Group, Inc.

- UL Solutions Inc.

- Workiva Inc.

- Wolters Kluwer NV

- Honeywell International Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the government and public sector green IT software market size is expected to increase from USD 1.83 billion in 2025 to USD 2.12 billion in 2026 and reach USD 4.71 billion by 2031, growing at a CAGR of 17.31% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), End User (Central and Federal Government, State and Local Government, Public Utilities and Public Agencies, and More), Application (Carbon Data Collection and Disclosure, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Government and Public Sector Green IT Software Market Trends and Insights

Public Sector Net-Zero Procurement Requirements Reshape Contract Standards

Public procurement rules are pushing the government and public sector green IT software market away from voluntary reporting and toward contract-bound emissions documentation. The United Kingdom applied PPN 006 to major government contracts advertised from February 24, 2025, and the rule requires suppliers on contracts above GBP 5 million (USD 6.59 million) to submit carbon reduction plans as a condition of participation. That requirement changes software demand because agencies need systems that can collect, retain, and present supplier and operational emissions data in a form procurement teams can verify. It also brings together procurement, legal, finance, and sustainability teams on a single workflow, underscoring the value of centralized reporting and audit trails in the government and public sector green IT software market. Vendors that already fit formal public buying processes therefore gain an access advantage that can matter as much as feature depth when agencies evaluate bids.

Government Digital Modernization Mandates Accelerate Platform Consolidation

Digital modernization programs are widening the budgetary path for the government and public sector green IT software markets, as sustainability requirements are being built into broader technology renewal agendas. The United Kingdom's Defra Digital Sustainability Strategy 2025-2030 set a target to reduce IT carbon emissions by 16% by 2030 and required digital service suppliers with an annual contract value above GBP 1 million (USD 1.32 million) to hold externally verified carbon footprints and net-zero plans. The same strategy stated that Defra group IT operations generated 10,000 tonnes of CO2 equivalent in 2024, equal to 13% of the department's total emissions, which shows why software-backed tracking is moving closer to core IT governance. In the United States, the GSA's OneGov agreement with SAP in December 2025 offered federal agencies discounts of up to 80% across database, integration, analytics, and cloud tools, with projected savings of USD 165 million. These moves favor vendors that already sit within approved procurement and enterprise technology stacks, which support platform consolidation across the government and public-sector green IT software markets.

Fragmented Budget and Procurement Cycles Slow Discretionary Uptake

Annual budgeting structures continue to slow the government and public sector green IT software market, as sustainability tools often compete with higher-priority IT projects within the same funding cycle. In many agencies, cybersecurity, workforce systems, and legacy modernization still rank ahead of carbon management platforms in appropriations reviews, which delays rollouts even when mandates are clear. The GSA's OneGov agreement with SAP lowered entry costs through deep discounts and projected USD 165 million in savings, but the arrangement also showed that short-term procurement windows can shape adoption timing and renewal risk. The same challenge arises at the subnational level, where city, county, and state budget calendars often do not align with national reporting expectations so that the policy requirement can arrive before the budget authority. Vendors that offer phased deployment, pilot scopes, and modular pricing are better suited to move through this constraint in the government and public sector green IT software market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Data Center Energy Costs Shift the Software ROI Case

- Sustainability Reporting Automation Replaces Spreadsheet Workflows

- Data Sovereignty Requirements Create Competing Architecture Demands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbon accounting and reporting software held 28.74% of the government and public sector green IT software market share in 2025, which made it the largest solution type at the start of the forecast period. That lead reflects the practical order of agency work, because public bodies first need a measured and auditable emissions baseline before they can set reduction targets, compare suppliers, or defend grant-linked disclosures. The category also benefits from how government buyers evaluate systems, since audit traceability and structured records matter as much as user features as compliance obligations expand. SAP's May 2026 announcement that its carbon accounting offering was recognized again in the IDC MarketScape reinforces the appeal of ERP-native architectures that align emissions records more closely with financial control practices.

Energy and power management software is gaining traction alongside the leading category, as agencies now face a stronger need to tie sustainability actions to operating efficiency and data center performance targets. Green procurement and supplier sustainability software is projected to expand at 18.12% CAGR through 2031, the fastest pace within the solution mix. EcoVadis and Workiva's May 2026 partnership shows why this category is moving quickly: supplier carbon data is being linked more directly into audit-ready reporting rather than staying in separate procurement systems. Sustainability data management platforms are also becoming increasingly important because agencies need a single environment to bring together accounting, procurement, and operational information without the need for repeated manual consolidation.

Cloud deployment accounted for 65.41% of revenue in 2025, which kept it well ahead of other deployment models in the government and public sector green IT software market. Agencies favor the cloud where possible because subscription delivery can shorten time to compliance and shift rule updates, maintenance, and release management toward the vendor. That matters in public settings, where internal IT teams often face limited capacity and need software that can stay current without extensive reconfiguration. Cloud also fits the wider pattern of government modernization programs that use negotiated procurement channels and approved platforms to accelerate adoption.

Hybrid deployment is projected to grow at 17.95% CAGR during 2026-2031, making it the fastest-rising model as buyers balance compliance speed with control over sensitive data. The European Commission's Sovereign Cloud Framework and France's 2026 directive on reducing extra-European dependencies both support this middle path by raising the bar for where and how public-sector data can be stored and processed. On-premises deployment, therefore, remains relevant for defense, national security, and agencies with strict operational data rules, even if it no longer sets the pace of growth. Vendors that can move data cleanly between local environments and compliant cloud layers are likely to capture a larger share of the government and public sector green IT software market as sovereignty requirements remain in place.

Complete Report Scope:

- By Solution Type

- Carbon Accounting and Reporting Software

- Energy and Power Management Software

- IT Asset Lifecycle Management Software

- Sustainability Data Management Platforms

- Green Procurement and Supplier Sustainability Software

- By Deployment

- Cloud

- On-Premises

- Hybrid

- By End User

- Central and Federal Government

- State and Local Government

- Public Utilities and Public Agencies

- Public Education and Public Healthcare Institutions

- By Application

- Carbon Data Collection and Disclosure

- Energy Optimization and Workload Scheduling

- IT Asset Utilization and Lifecycle Optimization

- Public Procurement and Supplier Emissions Tracking

- Compliance, Audit, and ESG Workflow Automation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe accounted for a 34.56% share of the government and public sector green IT software market in 2025, maintaining its lead among regional markets. The region's position is supported by a dense policy landscape in which environmental compliance, procurement controls, and digital governance are advancing together rather than as separate agendas. The European Commission's Sovereign Cloud Framework made environmental sustainability one of the scored dimensions for public cloud procurement while also keeping sovereignty assurance central to adoption decisions. The United Kingdom added further momentum through public procurement and digital sustainability rules that place formal expectations on suppliers and departmental IT operations. As a result, Europe combines broad compliance pressure with procurement systems that can channel spending toward vendors already prepared for public-sector review.

North America was the second-largest regional market for government and public sector green IT software in 2025. In the United States, adoption is being shaped heavily by centralized procurement vehicles, which give large software vendors a faster route into federal estates than one-by-one agency sales. The GSA's OneGov agreement with SAP showed how federal bodies can scale access to analytics, integration, and cloud capabilities through negotiated discounts and common procurement terms. This structure supports volume deployment but also leaves room for specialist tools that provide deeper supplier, asset, or disclosure functionality alongside the main platform.

Asia-Pacific is projected to expand at a 18.45% CAGR during 2026-2031, making it the fastest-growing regional segment in the government and public sector green IT software market. The region is moving from policy planning to implementation, which is broadening demand for carbon accounting, lifecycle tracking, and procurement-oriented reporting tools. NTT Group's March 2026 release of a lifecycle CO2 calculation standard for software reflects a more formal treatment of software-related emissions in advanced Asia-Pacific markets. South America, the Middle East, and Africa are smaller bases today, yet the UAE pilot announced with Khazna, Agility, and the Ministry of Energy and Infrastructure shows that government energy management deployments are moving into active execution outside the two largest regions. This means future expansion outside Europe and North America is likely to begin with targeted public projects and then widen as agencies build internal capacity and procurement familiarity.

- Accenture plc

- Persefoni AI Inc.

- Cority Software Inc.

- Dakota Software Corporation

- Enablon SA

- Enviance, Inc.

- IBM Corporation

- Johnson Controls International plc

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Schneider Electric SE

- ServiceNow, Inc.

- Siemens AG

- Sphera Solutions, Inc.

- Sustainability Software Group, Inc.

- UL Solutions Inc.

- Workiva Inc.

- Wolters Kluwer N.V.

- Honeywell International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Digital Modernization Mandates

- 4.2.2 Public Sector Net-Zero Procurement Requirements

- 4.2.3 Rising Utility and Data Center Energy Cost Pressure

- 4.2.4 Shift Toward Sustainability Reporting Automation in Agencies

- 4.2.5 Legacy IT Carbon Visibility Gaps Across Public Institutions

- 4.2.6 Demand for Audit-Ready Carbon Data in Grant-Funded Programs

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy Procurement and Budget Cycles

- 4.3.2 Data Sovereignty and Public Cloud Approval Constraints

- 4.3.3 Long Software Validation and Change-Management Timelines

- 4.3.4 Limited Internal ESG and Carbon Accounting Skill Depth

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Buyers

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Carbon Accounting and Reporting Software

- 5.1.2 Energy and Power Management Software

- 5.1.3 IT Asset Lifecycle Management Software

- 5.1.4 Sustainability Data Management Platforms

- 5.1.5 Green Procurement and Supplier Sustainability Software

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User

- 5.3.1 Central and Federal Government

- 5.3.2 State and Local Government

- 5.3.3 Public Utilities and Public Agencies

- 5.3.4 Public Education and Public Healthcare Institutions

- 5.4 By Application

- 5.4.1 Carbon Data Collection and Disclosure

- 5.4.2 Energy Optimization and Workload Scheduling

- 5.4.3 IT Asset Utilization and Lifecycle Optimization

- 5.4.4 Public Procurement and Supplier Emissions Tracking

- 5.4.5 Compliance, Audit, and ESG Workflow Automation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Persefoni AI Inc.

- 6.4.3 Cority Software Inc.

- 6.4.4 Dakota Software Corporation

- 6.4.5 Enablon SA

- 6.4.6 Enviance, Inc.

- 6.4.7 IBM Corporation

- 6.4.8 Johnson Controls International plc

- 6.4.9 Microsoft Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 SAP SE

- 6.4.12 Schneider Electric SE

- 6.4.13 ServiceNow, Inc.

- 6.4.14 Siemens AG

- 6.4.15 Sphera Solutions, Inc.

- 6.4.16 Sustainability Software Group, Inc.

- 6.4.17 UL Solutions Inc.

- 6.4.18 Workiva Inc.

- 6.4.19 Wolters Kluwer N.V.

- 6.4.20 Honeywell International Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業管治、風險與合規市場:依產品、組件、部署模式、組織規模與產業分類-全球預測,2026-2032年

企業管治、風險與合規市場:依產品、組件、部署模式、組織規模與產業分類-全球預測,2026-2032年 2026年全球鏈上企業管治市場報告

2026年全球鏈上企業管治市場報告 企業管治、風險和合規 (EGRC) 市場規模、佔有率和趨勢分析報告:按組件、軟體、服務、應用、組織規模、行業、地區和細分市場預測 (2026–2033)2026年全球企業管治、風險與合規(eGRC)市場報告2026年全球環境、社會與管治(ESG)報告軟體市場報告

企業管治、風險和合規 (EGRC) 市場規模、佔有率和趨勢分析報告:按組件、軟體、服務、應用、組織規模、行業、地區和細分市場預測 (2026–2033)2026年全球企業管治、風險與合規(eGRC)市場報告2026年全球環境、社會與管治(ESG)報告軟體市場報告 企業管治、風險與合規市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測2026年全球空中管治市場報告2026年全球企業管治服務市場報告

企業管治、風險與合規市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測2026年全球空中管治市場報告2026年全球企業管治服務市場報告 企業管治、風險與合規市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、流程、部署、最終用戶與功能分類

企業管治、風險與合規市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、流程、部署、最終用戶與功能分類 企業管治、風險與合規市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、組織規模、最終用戶、地區和競爭對手分類,2021-2031年

企業管治、風險與合規市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、組織規模、最終用戶、地區和競爭對手分類,2021-2031年