|

市場調查報告書

商品編碼

2072696

美國醫療保健管理系統:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)United States Practice Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

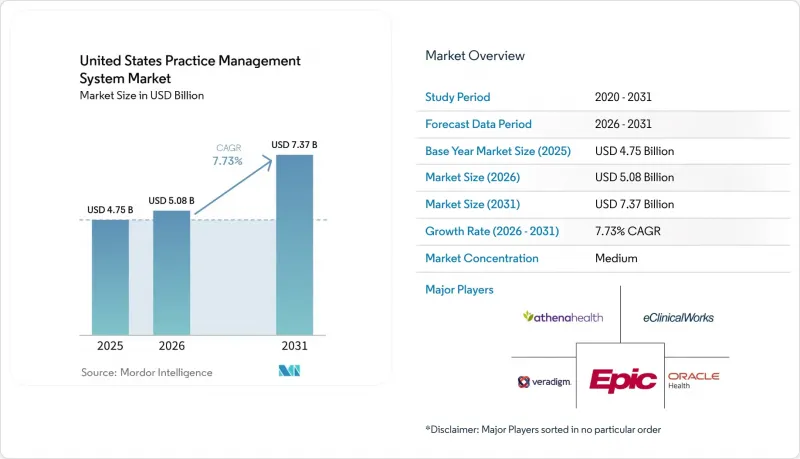

根據 Mordor Intelligence 預測,美國醫療保健管理系統市場規模將從 2025 年的 47.5 億美元和 2026 年的 50.8 億美元成長到 2031 年的 73.7 億美元,2026 年至 2031 年的複合年成長率為 7.73%。

本報告按產品(整合式、獨立式)、組件(軟體、服務)、交付模式(基於Web、基於雲端/SaaS、本地部署)、功能(日程安排、計費、預核准、醫療記錄、分析、病人參與、遠端醫療、電子處方)和最終用戶(診所、醫院、實驗室、藥房、門診部)進行細分。市場預測以美元計價。

美國醫療保健管理系統市場趨勢及洞察

管理成本和保險索賠被拒使得維持現狀變得困難。

美國醫療保健管理系統市場受到計費環境的影響,醫療服務提供者使用分散的工具管理計費變得更加困難。根據 Kodiak Solutions 的一份報告,到 2025 年,美國醫院因最終帳單被拒和壞帳造成的收入淨額損失將達到 484 億美元,高於 2024 年的 386 億美元。同時,最終帳單被拒率的中位數預計將從 2.5% 上升至 2.7%。此外,Premier 的報告顯示,醫療機構的帳單審核成本高達 257 億美元,其中 180 億美元可能是不必要的支出。這表明支付週期中仍然存在大量可避免的返工。因此,醫療機構更加重視資格驗證、提交前資料審核、編碼輔助和拒付預防等功能,這些功能能夠直接促進收款。這就是為什麼計費、編碼和計費管理仍然是美國醫療保健管理系統市場中最大的功能模組,也是為什麼供應商越來越重視可衡量的收入恢復,並將其作為核心價值提案。

整合的 EHR-PM-RCM 套件重新定義了平台的購買單位。

美國醫療保健管理系統市場正朝向整合式管理和臨床平台轉型。這是因為醫療服務提供者希望減少從預約、病歷到收入週期等整個營運過程中資料交接和核對的延遲。到了2025年,整合式醫療保健管理系統將佔總收入的61.9%,這證實買家已經更傾向於功能更全面的套件,而不是孤立的單一功能產品。 Epic在2026年HIMSS大會上展示了這一發展方向,其「Penny」用於計費和避免拒付,並將代理驅動的工作流程工具整合到主平台而非外部。 athenahealth也在2026年春季發布了“athenaOne”,進一步強化了向協調工作流程和定期平台級升級的轉變,並擴展了其嵌入式的收入週期改進功能。從實際角度來看,這種整合模式減少了重複資料輸入,將患者和計費資料匯總到單一的操作層,並使採購過程中的互通性準備工作更容易評估。

遷移成本和工作流程中斷給系統更新周期帶來了沉重負擔。

加速系統升級的主要障礙在於將運作中管理任務從一個系統遷移到另一個系統所需的時間和營運中斷。目前,實施過程遠不止於簡單的軟體安裝。醫療機構通常需要在完全切換之前進行資料清理、工作流程重新設計、員工再培訓、與保險公司規則協調以及並行運作。對於缺乏內部企劃團隊或無力在運作期間處理計費的獨立醫療機構和社區營運商而言,這一負擔尤其沉重。預計到2031年,醫療服務將以每年9.3%的速度快速成長,這表明許多買家正在投資外部實施支援、培訓和收入週期管理支持,而不是僅依賴內部團隊。雖然這可能會在短期內減緩採購速度,但它將支撐美國醫療管理系統市場供應商的持續收入成長。

細分市場分析

預計到2025年,整合醫療管理系統(EHR)將佔銷售額的61.87%,並將在2031年之前以8.25%的複合年成長率成長,在所有產品選項中擁有最大的市場規模和最強勁的成長勢頭。從產品角度來看,該細分市場目前是美國醫療管理系統市場最明確的關注點,因為醫療服務提供者希望在一個系統中處理預約管理、與醫療記錄整合、計費流程以及患者溝通。 EHR和EMR整合系統繼續佔據該細分市場的最大佔有率,因為醫療系統和大規模醫生組織仍然傾向於單一供應商的營運環境。隨著醫療服務提供者希望將計費資訊的檢索、編輯和拒付管理與前端接待和後端收款作業更緊密地整合,收入週期整合產品也正在蓬勃發展。隨著數位化病患登記、費用估算和自助服務工作流程從可選功能轉變為標準管理任務,病人參與整合工具的重要性日益凸顯。此外,隨著整個醫療保健系統對互通性的期望不斷提高,電子處方箋的整合也正朝著標準功能的方向發展。

這一趨勢印證了美國醫療管理系統產業對分散式軟體架構的容忍度正在降低的觀點。 Epic、athenahealth、eClinicalWorks 和 Veradigm 等公司都在致力於擴展工作流程接受度。這是因為醫療機構越來越傾向於以平台減少營運交接和商機來衡量平台的價值,而不是衡量其可購買的獨立模組的數量。獨立系統仍然佔據相當大的市場佔有率,預計到 2025 年將佔產品收入的近 38%。這是因為小規模診所和專科診所通常需要更簡單的預約和計費管理工具,而無需大規模套件的複雜性。這些買家仍然重視低進入門檻、易於設定和低營運負擔,尤其是在臨床系統已經部署到位或診所希望避免完全遷移平台的情況下。隨著時間的推移,模型化的 SaaS 軟體套件正在縮小差距,因此,美國醫療管理系統市場正逐漸轉向整合解決方案,即使在小規模臨床環境中也是如此。

到2025年,軟體收入將佔組件收入的63.83%,這反映出許可、訂閱和核心應用程式存取在各種規模的醫療機構中扮演著至關重要的角色。這種已部署的軟體基礎仍然是美國醫療管理系統市場的商業基石,因為任何醫療機構都離不開記錄管理系統和工作流程控制層來運行其排班、接待、計費和報告流程。隨著買家選擇在平台內部而非透過外部工具添加人工智慧驅動的編碼、工作流程最佳化、分析和患者溝通功能,軟體銷售仍然強勁。隨著商業性在其套件中整合更多功能,單獨替換軟體模組變得越來越困難,這提高了客戶留存率並提升了客戶價值。這也是領先的供應商儘管買家表達了對更簡單技術環境的渴望,但仍在不斷擴展其產品線的原因之一。

服務業正以更快的速度成長,預計到2031年複合年成長率將達到9.34%。這種成長反映的是實施難度增加,而非軟體需求下降。隨著許多醫療機構尋求的是計費工作流程、拒付管理、應收帳款催收和營運改革方面的直接支持,而不僅僅是技術交接,管理式收入週期服務正在不斷擴展。培訓和支援的角色也在不斷增強,因為新的人工智慧和自動化功能正在改變接待員、計費負責人和管理人員的日常工作流程,而不僅僅是在系統中添加螢幕。 AdvancedMD、Veradigm和CareCloud都強調2026年將發布新版本以增強工作流程,這表明實施的成功在很大程度上取決於營運支援和技術可用性。事實上,在美國醫療管理系統產業,許多醫療機構的業務收益正在成長,因為平台的複雜性已經超過了內部管理能力的提升速度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 降低行政成本和保險理賠拒賠率所面臨的挑戰。

- 遷移到整合的 EHR-PM-RCM 套件

- 多站點和混合工作流程中的雲端遷移

- 基於FHIR的互通性和電子預核准合規性

- TEFCA/QHIN 連線正逐漸成為一項採購標準。

- 基於人工智慧的拒付預防和員工能力提升

- 市場限制因素

- 與遷移和實施相關的成本,以及對工作流程的干擾。

- 雲端連線環境中的網路安全和 HIPAA 風險

- 支付機構的資料品質與API支援狀況之間的差距。

- 供應商整合以及傳統平台的不確定性

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品

- 綜合醫療管理系統

- 電子健康記錄/電子病歷整合系統

- 整合計費和收入周期系統

- 病人參與整合系統

- 電子處方箋整合系統

- 獨立醫療管理系統

- 綜合醫療管理系統

- 按組件

- 軟體

- 服務

- 安裝和設定服務

- 培訓和支援服務

- 管理收入周期服務

- 透過串流媒體模式

- 基於網路的

- 基於雲端/SaaS

- 現場

- 功能性別

- 預訂/登記

- 計費、編碼和保險索賠管理

- 保險合格和預核准流程

- 病患記錄追蹤和文件管理

- 報告、分析、儀錶板

- 患者參與和溝通

- 遠端醫療協調

- 電子處方箋和轉診管理

- 最終用戶

- 醫生後勤部門/診所

- 醫院和醫療系統

- 診斷檢查室

- 藥局

- 門診及其他門診設施

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- AdvancedMD

- athenahealth

- Azalea Health

- CareCloud

- CollaborateMD

- CureMD

- DrChrono

- Elation Health

- eClinicalWorks

- Epic Systems Corporation

- Greenway Health

- Henry Schein One/MicroMD

- Meditab

- ModMed

- NextGen Healthcare

- Office Ally

- Oracle Health

- PracticeSuite

- RXNT

- Tebra

- Veradigm

- WRS Health

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states practice management system market size is projected to expand from USD 4.75 billion in 2025 and USD 5.08 billion in 2026 to USD 7.37 billion by 2031, registering a CAGR of 7.73% between 2026 to 2031.

This report is Segmented by Product (Integrated, Standalone), Component (Software, Services), Delivery Mode (Web-Based, Cloud-Based/SaaS, On-Premise), Functionality (Scheduling, Billing, Prior Auth, Records, Analytics, Patient Engagement, Telehealth, E-Prescribing), and End User (Physician Offices, Hospitals, Labs, Pharmacies, Ambulatory). Market Forecasts are Provided in Value (USD).

United States Practice Management System Market Trends and Insights

Administrative Costs and Claim Denials Make Status Quo Unsustainable

The United States practice management system market is being shaped by a billing environment that has become materially harder for providers to manage with fragmented tools. Kodiak Solutions reported that net revenue leakage from final denials and bad debt reached USD 48.4 billion across U.S. hospitals in 2025, up from USD 38.6 billion in 2024, while the median final denial rate rose from 2.5% to 2.7%. Premier also reported that claims adjudication costs providers USD 25.7 billion and that USD 18 billion of that spend is potentially unnecessary expense, which shows how much avoidable rework remains in the payment cycle. As a result, practices are giving higher priority to eligibility checks, pre-submission claim scrubbing, coding support, and denial prevention functions that can be tied directly to cash collection. This is why billing, coding, and claims management remain the largest functionality block in the United States practice management system market and why vendors are increasingly positioning measurable revenue recovery as the central value proposition.

Integrated EHR-PM-RCM Suites Redefine the Platform Buying Unit

The United States practice management system market is moving toward unified administrative and clinical platforms because providers now want fewer data handoffs and fewer reconciliation delays across scheduling, documentation, and revenue cycle activity. Integrated practice management systems controlled 61.9% of revenue in 2025, which confirms that buyers are already favoring broader suites over isolated point products. Epic showed the direction of travel at HIMSS 2026 with Penny for billing and denial avoidance, alongside agent-driven workflow tools that sit inside the main platform rather than outside it. athenahealth also expanded embedded revenue cycle improvements in its Spring 2026 athenaOne release, reinforcing the same shift toward connected workflows and regular platform-level upgrades. In practical terms, the integrated model reduces duplicate entry, keeps patient and billing data in one operating layer, and makes interoperability readiness easier to evaluate during procurement.

Migration Costs and Workflow Disruption Weigh on Replacement Cycles

The main brake on faster replacement remains the time and disruption involved in moving live administrative operations from one system to another. Implementation now goes beyond software installation because practices often need data cleansing, workflow redesign, staff retraining, payer rule alignment, and a parallel operating period before a full switch can happen. That burden is especially difficult for independent practices and community operators that do not have internal project teams or spare billing capacity during go-live periods. The rapid expansion of services, which is projected to grow at 9.3% through 2031, shows that many buyers are paying for outside implementation, training, and managed revenue cycle support instead of relying only on internal teams. This slows purchasing in the short run, even as it supports recurring vendor revenue inside the United States practice management system market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration Extends Beyond Cost Savings Into Operational Resilience

- FHIR-Based Interoperability Moves From Optional to Contractually Mandated

- Cybersecurity Exposure Reshapes Cloud Vendor Selection Criteria

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated practice management systems held 61.87% of revenue in 2025 and are projected to expand at 8.25% CAGR through 2031, which gives them both the largest base and the strongest momentum among product options. In product terms, this segment now represents the clearest center of gravity in the United States practice management system market because providers want one system to handle scheduling, documentation links, billing flow, and patient communication. EHR and EMR integrated systems remain the largest volume layer inside this group because health systems and larger physician organizations still favor single-vendor operating environments. Revenue-cycle integrated products are also gaining ground because providers want charge capture, edits, and denial management connected more tightly to front-end registration and back-end collections. Patient engagement integrated tools are becoming more relevant as digital intake, payment estimation, and self-service workflows move from optional features to normal administrative practice. E-prescribing integration is also shifting toward baseline functionality as broader interoperability expectations continue to rise across provider settings.

This direction supports the view that the United States practice management system industry is becoming less tolerant of disconnected software stacks. Epic, athenahealth, eClinicalWorks, and Veradigm are all leaning into broader workflow coverage because providers increasingly judge value by whether a platform reduces handoffs and missed revenue opportunities, not by how many separate modules can be purchased. Standalone systems still retain a meaningful share of demand, at near 38% of product revenue in 2025, because smaller physician offices and specialty clinics often want simpler scheduling and billing tools without the full complexity of a larger suite. Those buyers still value lower switching friction, easier configuration, and lower perceived operating burden, especially when clinical systems are already in place or when the office wants to avoid a full platform conversion. Over time, modular SaaS packaging is narrowing that gap, and that is gradually shifting more of the United States practice management system market toward integrated offers even in smaller practice settings.

Software accounted for 63.83% of component revenue in 2025, which reflects the central role of licensing, subscriptions, and core application access across provider organizations of every size. That installed software base remains the commercial foundation of the United States practice management system market because no practice can operate its scheduling, registration, billing, and reporting processes without a system of record and workflow control layer. Software revenue also stays elevated because buyers are adding AI-assisted coding, workflow orchestration, analytics, and patient communication capabilities inside the platform rather than through outside tools. As vendors bundle more functions into unified suites, software becomes harder to replace module by module, which supports retention and deeper account value. This is one reason the leading vendors continue to widen their product scope even when buyers say they want simpler technology estates.

Services are growing faster, at 9.34% CAGR through 2031, and that growth says more about implementation difficulty than about a reduced need for software. Managed revenue cycle services are expanding because many providers want direct support with claims workflows, denial management, collections, and operational change rather than a technology-only handoff. Training and support are also taking on a larger role because new AI and automation features alter work routines for front-desk staff, billers, and managers instead of merely adding another screen to the system. AdvancedMD, Veradigm, and CareCloud have all emphasized workflow-enhancing releases in 2026, which shows that successful deployment now depends on operating support as much as on technical availability. In effect, the United States practice management system industry is generating more service revenue because platform sophistication is rising faster than internal administrative capacity in many provider organizations.

Complete Report Scope:

- By Product

- Integrated Practice Management Systems

- EHR / EMR-Integrated Systems

- Billing and Revenue-Cycle-Integrated Systems

- Patient Engagement-Integrated Systems

- E-Prescribing-Integrated Systems

- Standalone Practice Management Systems

- Integrated Practice Management Systems

- By Component

- Software

- Services

- Implementation and Configuration Services

- Training and Support Services

- Managed Revenue Cycle Services

- By Delivery Mode

- Web-Based

- Cloud-Based / SaaS

- On-Premise

- By Functionality

- Appointment Scheduling and Registration

- Billing, Coding and Claims Management

- Insurance Eligibility and Prior Authorization Workflow

- Patient Record Tracking and Document Management

- Reporting, Analytics and Dashboarding

- Patient Engagement and Communication

- Telehealth Coordination

- E-Prescribing and Referral Management

- By End User

- Physician Back Offices / Physician Offices

- Hospitals and Health Systems

- Diagnostic Laboratories

- Pharmacies

- Ambulatory and Other Outpatient Settings

List of Companies Covered in this Report:

- AdvancedMD

- athenahealth

- Azalea Health

- CareCloud

- CollaborateMD

- Curemd Healthcare

- DrChrono

- Elation Health

- eClinicalWorks

- Epic Systems

- Greenway Health

- Henry Schein One / MicroMD

- Meditab

- ModMed

- NextGen Healthcare

- Office Ally

- Oracle Health

- PracticeSuite

- RXNT

- Tebra

- Veradigm

- WRS Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Administrative Cost and Claim-Denial Reduction Imperative

- 4.2.2 Shift To Integrated EHR-PM-RCM Suites

- 4.2.3 Cloud Migration for Multi-Site and Hybrid Workflows

- 4.2.4 FHIR-Based Interoperability and E-Prior-Authorization Compliance

- 4.2.5 TEFCA / QHIN Connectivity Becoming a Buying Criterion

- 4.2.6 AI-Native Denial Prevention and Staff-Capacity Extension

- 4.3 Market Restraints

- 4.3.1 Costly Migration, Onboarding, and Workflow Disruption

- 4.3.2 Cybersecurity and HIPAA Exposure in Cloud-Connected Environments

- 4.3.3 Payer Data Quality and API-Readiness Gaps

- 4.3.4 Vendor Consolidation and Legacy-Platform Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Integrated Practice Management Systems

- 5.1.1.1 EHR / EMR-Integrated Systems

- 5.1.1.2 Billing and Revenue-Cycle-Integrated Systems

- 5.1.1.3 Patient Engagement-Integrated Systems

- 5.1.1.4 E-Prescribing-Integrated Systems

- 5.1.2 Standalone Practice Management Systems

- 5.1.1 Integrated Practice Management Systems

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.2.2.1 Implementation and Configuration Services

- 5.2.2.2 Training and Support Services

- 5.2.2.3 Managed Revenue Cycle Services

- 5.3 By Delivery Mode

- 5.3.1 Web-Based

- 5.3.2 Cloud-Based / SaaS

- 5.3.3 On-Premise

- 5.4 By Functionality

- 5.4.1 Appointment Scheduling and Registration

- 5.4.2 Billing, Coding and Claims Management

- 5.4.3 Insurance Eligibility and Prior Authorization Workflow

- 5.4.4 Patient Record Tracking and Document Management

- 5.4.5 Reporting, Analytics and Dashboarding

- 5.4.6 Patient Engagement and Communication

- 5.4.7 Telehealth Coordination

- 5.4.8 E-Prescribing and Referral Management

- 5.5 By End User

- 5.5.1 Physician Back Offices / Physician Offices

- 5.5.2 Hospitals and Health Systems

- 5.5.3 Diagnostic Laboratories

- 5.5.4 Pharmacies

- 5.5.5 Ambulatory and Other Outpatient Settings

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AdvancedMD

- 6.3.2 athenahealth

- 6.3.3 Azalea Health

- 6.3.4 CareCloud

- 6.3.5 CollaborateMD

- 6.3.6 CureMD

- 6.3.7 DrChrono

- 6.3.8 Elation Health

- 6.3.9 eClinicalWorks

- 6.3.10 Epic Systems Corporation

- 6.3.11 Greenway Health

- 6.3.12 Henry Schein One / MicroMD

- 6.3.13 Meditab

- 6.3.14 ModMed

- 6.3.15 NextGen Healthcare

- 6.3.16 Office Ally

- 6.3.17 Oracle Health

- 6.3.18 PracticeSuite

- 6.3.19 RXNT

- 6.3.20 Tebra

- 6.3.21 Veradigm

- 6.3.22 WRS Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

醫療管理系統市場報告:按組件、產品、部署模式、最終用戶和地區分類(2026-2034 年)

醫療管理系統市場報告:按組件、產品、部署模式、最終用戶和地區分類(2026-2034 年) 全球診所管理系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)實踐管理系統市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,2026-2034 年

全球診所管理系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)實踐管理系統市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,2026-2034 年 實踐管理系統市場規模、佔有率和成長分析(按產品、組件、交付模式、最終用戶和地區分類)—產業預測,2026-2033年

實踐管理系統市場規模、佔有率和成長分析(按產品、組件、交付模式、最終用戶和地區分類)—產業預測,2026-2033年 實踐管理系統市場

實踐管理系統市場 2025年全球實踐管理系統市場報告全球實踐管理系統市場:2025 年至 2030 年預測

2025年全球實踐管理系統市場報告全球實踐管理系統市場:2025 年至 2030 年預測 美國實踐管理系統市場規模、佔有率和趨勢分析報告:按產品、組件、交付類型、最終用途和細分市場預測,2025 年至 2033 年實踐管理系統市場規模、佔有率、趨勢分析報告:按產品、組件、交付模式、最終用途、地區和細分市場預測,2025 年至 2030 年

美國實踐管理系統市場規模、佔有率和趨勢分析報告:按產品、組件、交付類型、最終用途和細分市場預測,2025 年至 2033 年實踐管理系統市場規模、佔有率、趨勢分析報告:按產品、組件、交付模式、最終用途、地區和細分市場預測,2025 年至 2030 年