|

市場調查報告書

商品編碼

2072661

美國核心銀行軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Core Banking Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

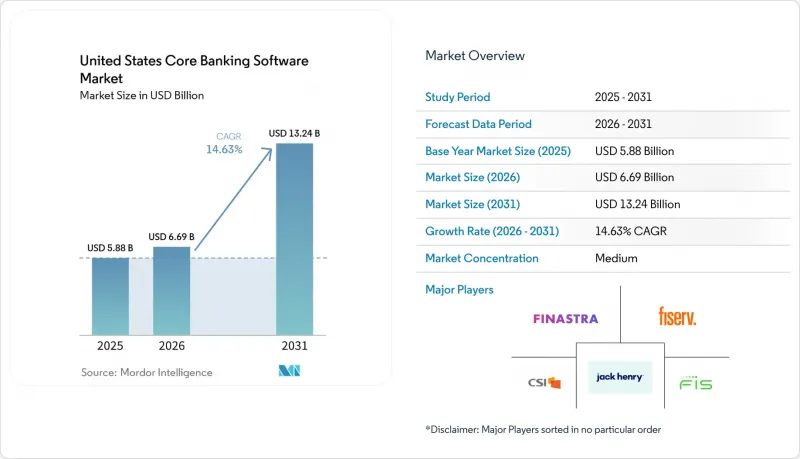

據 Mordor Intelligence 稱,2025 年美國核心銀行軟體市值為 58.8 億美元,預計到 2031 年將達到 132.4 億美元,而 2026 年為 66.9 億美元,2026 年至 2031 年預測期內的複合年成長率為 14.63%。

本報告按元件(解決方案和服務)、部署模式(雲端、本地部署、混合部署)和最終用戶(銀行、非銀行金融機構及其他(金融科技公司和支付機構))進行細分。市場預測以美元計價。

美國核心銀行軟體市場趨勢與洞察

向雲端原生架構的遷移帶來了成本節約和更短的發布週期。

雲端原生架構將發布週期從季度縮短至每週,這種速度差異正成為仍在運行單體核心系統的銀行的商業性劣勢。 2026年5月,美國銀行擴大了與AWS的合作,為其支付處理、資產管理和商業銀行應用提供支持,惠及約140萬家企業。這表明現代化不再局限於外圍系統,而是擴展到了關鍵業務工作負載。 2025年9月,Peoples Bank提前一天完成了向現代雲端原生核心系統的遷移,並允許超過19,000名客戶在24小時內重新註冊網路銀行。這為區域性金融機構提供了一個以最小營運影響完成遷移的具體範例。這些案例表明,雲端遷移不再局限於試驗計畫。國家和地區性金融機構都在利用雲端遷移來更新其營運模式和交付週期。此外,計量收費的基礎設施透過減少長期運作的大型主機環境中存在的過高固定成本,改變了成本結構。在美國核心銀行軟體市場,更快的發布速度和更高的成本可見度使得遷移時機更成為競爭策略的一部分,而不僅僅是後勤部門技術決策。

FedNow 和 RTP 的引入正在推動即時核心系統的升級。

即時支付的成長速度遠超許多系統升級預算的預期,即時交易接收和傳輸的差距暴露了以批次為中心的核心系統設計的缺陷。 FedNow在2025年將處理超過8,500億美元的交易,到2026年4月,參與該網路的金融機構數量將達到約1,700家。這顯示不同規模銀行的營運標準變化之快令人矚目。 RTP網路也在2025年2月將其交易限額從100萬美元提高到1000萬美元,拓展了商業和金融領域中需要即時帳簿可見性和快速對帳的應用場景。 2026年2月,大都會商業銀行完成了傳統ACH主機的退役,並遷移到Finzly的雲端原生、API優先的付款管道。這顯示完全退役是可行的,混合過渡方案並非唯一的出路。隨著即時結算量的成長,仍依賴批次帳簿更新的銀行在結算處理、異常處理和客戶支援方面面臨日益沉重的營運負擔。在美國核心銀行軟體市場,即時處理的準備與核心系統更換的時機密切相關,而不僅僅是獨立結算系統的升級。

區域銀行轉型風險及舊有系統整合的複雜性

對於資產規模在10億美元至500億美元之間的區域性金融機構而言,遷移風險最為嚴峻。這些機構面臨高度複雜的運營,而其IT基礎設施卻仍然有限。 2025年的一項行業調查發現,35%的銀行對其核心處理器不滿意,19%的銀行可能在下次升級時更換系統。這表明,即使在充滿挑戰的情況下,轉換的需求仍然存在。挑戰通常不僅限於核心系統本身,因為銀行在切換之前通常需要重新映射30到50個甚至更多的外圍系統,這些系統涵蓋支付、財務、合規、銀行卡和數位管道等領域。此外,遺留系統會累積多年未記錄的資料轉換,而這些問題往往會在檢驗的最後階段才顯現出來,此時時間已經非常緊迫。雖然延長並行運作時間可以降低營運風險,但會增加遷移專案的成本和管理負擔,並加劇內部疲勞。在美國核心銀行軟體市場,儘管現代化帶來的長期效益已經顯而易見,但許多區域性銀行仍持謹慎態度。

細分市場分析

預計到2025年,解決方案將佔據美國核心銀行軟體市場佔有率的61.89%,軟體訂閱和平台授權仍將是供應商和買家最大的收入來源。在對美國核心銀行軟體市場規模的展望中,服務預計將在2026年至2031年間以14.98%的複合年成長率成長,使交付營運成為成長最快的收入來源。這一構成比表明,儘管銀行仍然在平臺本身投入大量預算,但它們越來越需要外部協助來安全地執行遷移、整合、測試和控制設計。需求壓力並非來自單一業務流程,因為API開放、資料映射、支付系統整合和合規準備通常在同一系統更新中並行。因此,實施能力是影響整個美國核心銀行軟體市場合約時間、供應商選擇和遷移順序的阻礙因素因素。

此外,隨著供應商和合作夥伴圍繞核心系統提供託管遷移、雲端營運和人工智慧工作流程支援等服務,服務層也逐漸成為持續的收入來源。這種轉變改善了服務交付的經濟效益,因為合作關係在平台部署完成後繼續延續,而非在上運作後就結束。此外,買家評估供應商品質的方式也在發生變化,因為交付的深度不僅影響速度,還影響營運穩定性和稽核準備。在美國核心銀行軟體產業,經認證的平台專業知識的價值日益凸顯,因為金融機構希望最大限度地減少諮詢、整合和營運等不同團隊之間的交接。因此,儘管解決方案仍然佔據支出的大部分,但服務正日益成為一個能夠滿足現代化帶來的營運需求的細分市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- FedNow 和 RTP 的部署正在推動我們即時核心系統的升級。

- 透過遷移到雲端原生架構,降低成本並縮短發布週期。

- 大型主機人才的流失正在加速核心系統的現代化。

- 開放銀行和API生態系統的擴展

- 贊助銀行專案的管理結構正在將支付環節與其核心業務緊密聯繫起來。

- 需要核心數據的事件驅動型基於代理的人工智慧程序

- 市場限制因素

- 區域銀行系統遷移風險及舊有系統整合的複雜性

- 供應商鎖定和更長的續約週期正在延緩轉換。

- 第三方和第四方的審查增加了實質審查。

- 網路韌性和大規模停電後的復原要求正在擴大轉型範圍。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 最終用戶

- 銀行

- 非銀行金融機構

- 其他終端使用者(金融科技公司、支付機構)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Fiserv, Inc.

- Jack Henry & Associates, Inc.

- Fidelity National Information Services, Inc.

- Finastra Group Holdings Limited

- Oracle Corporation

- Temenos AG

- Computer Services, Inc.

- Tata Consultancy Services Limited

- EdgeVerve Systems Limited

- Intellect Design Arena Limited

- Nymbus, Inc.

- Corelation, Inc.

- Q2 Holdings, Inc.

- nCino, Inc.

- Mambu GmbH

- Thought Machine Group Limited

- Corelation, Inc.

- ACI Worldwide, Inc.

- Finzly, Inc.

- Finxact, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states core banking software market size was valued at USD 5.88 billion in 2025 and estimated to grow from USD 6.69 billion in 2026 to reach USD 13.24 billion by 2031, at a CAGR of 14.63% during the forecast period 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), and End-User (Banks, Non-Bank Financial Institutions, and More (FinTechs and Payment Institutions)). The Market Forecasts are Provided in Terms of Value (USD).

United States Core Banking Software Market Trends and Insights

Cloud-Native Migration Lowering Cost And Release Cycles

Cloud-native architectures are reducing release cycles from quarters to weeks, and that speed gap is turning into a commercial disadvantage for banks still running monolithic cores. U.S. Bank expanded its collaboration with AWS in May 2026 across payment processing, wealth management, and commercial banking applications that support approximately 1.4 million businesses, showing that modernization now spans mission-critical workloads rather than side systems. PeoplesBank completed its move to a modern cloud-native core in September 2025, finished a day ahead of schedule, and re-enrolled more than 19,000 customers in online banking within 24 hours, which gave community institutions a live example of low-disruption conversion execution. These cases show that cloud migration is no longer limited to pilot programs, because both national and community institutions are using it to reset operating models and delivery timelines. Consumption-based infrastructure also changes the cost equation by reducing the fixed overprovisioning that sat inside long-lived mainframe environments. In the United States core banking software market, that combination of faster releases and cleaner cost visibility is making migration timing part of competitive planning rather than a back-office technology decision.

FedNow And RTP Adoption Driving Real-Time Core Upgrades

Real-time payment growth is moving faster than many replacement budgets expected, and the gap between receiving transactions and sending them in real time is exposing weaknesses in batch-oriented core designs. FedNow processed more than USD 850 billion in 2025 and the network had reached around 1,700 financial institutions by April 2026, which shows how quickly the operating baseline has shifted for banks of different sizes. The RTP network also raised its transaction cap from USD 1 million to USD 10 million in February 2025, widening commercial and treasury use cases that require immediate ledger visibility and faster reconciliation. Metropolitan Commercial Bank completed the retirement of its legacy ACH mainframe in February 2026 and moved to Finzly's cloud-native, API-first payment platform, which showed that full decommission is possible and that hybrid workarounds are not the only path. As instant payment throughput rises, banks that still rely on batch-ledger updates face rising operating strain in payments, exception handling, and customer-facing service response. In the US core banking software market, the market keeps real-time readiness tied closely to core replacement timing rather than to standalone payments upgrades.

Conversion Risk And Legacy Integration Complexity At Regional Banks

Conversion risk is most acute at regional institutions in the USD 1 billion to USD 50 billion asset range, where operating complexity is high but IT scale is still limited. A 2025 industry survey found that 35% of banks were dissatisfied with their core processor and 19% were likely to convert at the next renewal date, which shows that demand to switch exists even when execution remains difficult. The challenge usually sits beyond the core itself, because banks often have to remap 30 to 50 or more ancillary systems across payments, treasury, compliance, cards, and digital channels before a cutover can happen. Legacy environments also carry years of undocumented data transformations, and those issues often appear late in validation when timelines are already tight. Longer parallel runs can reduce operational risk, but they also increase program cost, control overhead, and internal fatigue during migration. In the United States core banking software market, that keeps many regional banks cautious even when the long-term case for modernization is already clear.

Other drivers and restraints analyzed in the detailed report include:

- Agentic AI Programs Requiring Event-Driven Core Data

- Mainframe Talent Attrition Accelerating Core Renewal

- Vendor Lock-In And Long Renewal Cycles Slowing Switching

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 61.89% of the United States core banking software market share in 2025, which kept software subscriptions and platform licenses as the largest revenue base for vendors and buyers. Within the US core banking software market size outlook, services are projected to expand at a 14.98% CAGR through 2026-2031, which makes delivery work the faster-growing revenue stream. This mix shows that banks still commit large budgets to the platform itself, but they increasingly need outside help to execute conversion, integration, testing, and control design safely. The demand pressure does not come from one workstream alone, because API exposure, data mapping, payments integration, and compliance preparation often run together during the same replacement program. As a result, implementation capacity has become a constraint that shapes deal timing, vendor selection, and migration sequencing across the US core banking software market.

The services layer is also becoming more recurring as vendors and partners add managed migration, cloud operations, and AI workflow support around the core. That shift improves the economics of service delivery because the relationship continues after go-live instead of ending once the platform is installed. It also changes how buyers assess vendor quality, since delivery depth now affects not only speed but also operating stability and examination readiness. In the United States core banking software industry, certified platform expertise is becoming more valuable because institutions want fewer handoffs across separate advisory, integration, and operations teams. This leaves services positioned as the segment that absorbs the execution demands created by modernization, even while solutions remain the larger base of spending.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By End-User

- Banks

- Non-Bank Financial Institutions

- Other End-users (FinTechs, Payment Institutions)

List of Companies Covered in this Report:

- Fiserv, Inc.

- Jack Henry & Associates, Inc.

- Fidelity National Information Services, Inc.

- Finastra Group Holdings Limited

- Oracle Corporation

- Temenos AG

- Computer Services, Inc.

- Tata Consultancy Services Limited

- EdgeVerve Systems Limited

- Intellect Design Arena Limited

- Nymbus, Inc.

- Corelation, Inc.

- Q2 Holdings, Inc.

- nCino, Inc.

- Mambu GmbH

- Thought Machine Group Limited

- Corelation, Inc.

- ACI Worldwide, Inc.

- Finzly, Inc.

- Finxact, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 FedNow and RTP Adoption Driving Real-Time Core Upgrades

- 4.2.2 Cloud-Native Migration Lowering Cost and Release Cycles

- 4.2.3 Mainframe Talent Attrition Accelerating Core Renewal

- 4.2.4 Open Banking and API Ecosystem Expansion

- 4.2.5 Sponsor-Bank Program Controls Pulling Payments Closer to the Core

- 4.2.6 Agentic AI Programs Requiring Event-Driven Core Data

- 4.3 Market Restraints

- 4.3.1 Conversion Risk and Legacy Integration Complexity at Regional Banks

- 4.3.2 Vendor Lock-In and Long Renewal Cycles Slowing Switching

- 4.3.3 Third-Party and Fourth-Party Scrutiny Raising Due-Diligence Burden

- 4.3.4 Cyber-Resilience and Severe-Outage Recovery Requirements Increasing Migration Scope

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End-User

- 5.3.1 Banks

- 5.3.2 Non-Bank Financial Institutions

- 5.3.3 Other End-users (FinTechs, Payment Institutions)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Fiserv, Inc.

- 6.4.2 Jack Henry & Associates, Inc.

- 6.4.3 Fidelity National Information Services, Inc.

- 6.4.4 Finastra Group Holdings Limited

- 6.4.5 Oracle Corporation

- 6.4.6 Temenos AG

- 6.4.7 Computer Services, Inc.

- 6.4.8 Tata Consultancy Services Limited

- 6.4.9 EdgeVerve Systems Limited

- 6.4.10 Intellect Design Arena Limited

- 6.4.11 Nymbus, Inc.

- 6.4.12 Corelation, Inc.

- 6.4.13 Q2 Holdings, Inc.

- 6.4.14 nCino, Inc.

- 6.4.15 Mambu GmbH

- 6.4.16 Thought Machine Group Limited

- 6.4.17 Corelation, Inc.

- 6.4.18 ACI Worldwide, Inc.

- 6.4.19 Finzly, Inc.

- 6.4.20 Finxact, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

核心銀行軟體市場預測至2034年-按銀行功能、架構、整合層、部署模式和最終用戶分類的全球分析

核心銀行軟體市場預測至2034年-按銀行功能、架構、整合層、部署模式和最終用戶分類的全球分析 核心銀行軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、最終用途、地區和細分市場預測(2026-2033 年)

核心銀行軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、最終用途、地區和細分市場預測(2026-2033 年) 全球核心銀行軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球核心銀行軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球核心銀行軟體市場

2026-2030年全球核心銀行軟體市場 2026年全球核心銀行軟體市場報告

2026年全球核心銀行軟體市場報告 核心銀行軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及模組分類核心銀行軟體市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

核心銀行軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及模組分類核心銀行軟體市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 核心銀行軟體市場規模、佔有率和成長分析(按組件、部署類型、最終用途和地區分類)-2026-2033年產業預測基於 SaaS 的核心銀行軟體市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及 2024-2032 年預測

核心銀行軟體市場規模、佔有率和成長分析(按組件、部署類型、最終用途和地區分類)-2026-2033年產業預測基於 SaaS 的核心銀行軟體市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及 2024-2032 年預測 核心銀行軟體市場(按產品、服務交付模式、銀行類型、部署模式和最終用戶分類)—2025-2030 年全球預測

核心銀行軟體市場(按產品、服務交付模式、銀行類型、部署模式和最終用戶分類)—2025-2030 年全球預測