|

市場調查報告書

商品編碼

2072646

美國抗菌消毒劑市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)United States Antiseptic And Disinfectant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

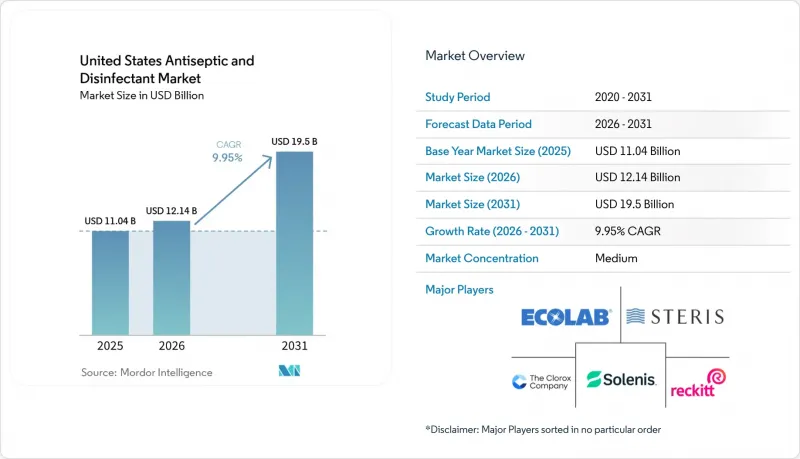

據 Mordor Intelligence 稱,2025 年美國消毒劑和抗菌劑市值為 110.4 億美元,預計到 2031 年將達到 195 億美元,而 2026 年為 121.4 億美元,預測期(2026-2031 年)的複合年成長率為 9.95%。

本報告按產品類型(季銨鹽化合物、氯化化合物、醇類和醛類、雙胍類和碘類、過氧化氫和過氧乙酸、酶清潔劑、其他)、劑型(液體、擦拭巾、噴霧劑/氣霧劑、凝膠/泡沫)、應用(表面、醫療設備高級別消毒 (HLD)、設備/酵素、皮膚預處理、其他門診手術中心(ATCL) (SNF)、檢查室、其他)進行分類。金額以美元計。

美國抗菌消毒劑市場趨勢及洞察。

院內感染(HAI)、耳念珠菌和多重抗藥性菌株(MDRO)帶來的持續壓力

醫療相關感染疾病(HAI)持續推動美國抗菌和消毒劑市場的需求。儘管美國疾病管制與預防中心(CDC)報告稱,與2023年相比,2024年大多數HAI類別的感染率將下降2%至11%,但腹部子宮切除術後傷口感染率仍上升了8%,顯示不同手術的感染控制效果存在差異。耳念珠菌感染正日益成為抗菌劑採購的重要促進因素,CDC在2024年確診了6,304例臨床病例(高於2023年的4523例)。由於耳念珠菌對多種抗真菌藥物物具有抗藥性,醫療機構正將工作重點從單純治療轉向環境消毒和更有效的孢子殺滅方案。這種壓力不再局限於急性護理醫院;長期急性護理醫院和配備人工呼吸器的專科護理機構也正在收緊採購標準,以應對定植和感染病例。這項轉變擴大了美國消毒劑和抗菌劑市場的基本客群,使其涵蓋了先前並未購買此類複雜產品的復健護理機構。

醫療保健和公共機構的永久性衛生標準

疫情後的衛生標準持續時間比許多買家最初預期的要長,這持續支撐著美國消毒劑和清潔劑市場。美國疾病管制與預防中心 (CDC) 的指導意見和醫院的感染控制措施,使得表面清潔頻率和消毒程序成為日常運作的一部分,而不僅僅是應急方案。這意味著醫療機構可以在不相應減少消毒劑用量的情況下減少床位或改變服務配置。目前更重要的需求推動要素是每個房間、治療區域和共享設備的消毒劑用量。這使得成熟醫療市場的銷售量更能抵禦醫院整合和人口成長放緩的影響。此外,能夠減少工作流程錯誤、縮短消毒時間或提高表面相容性的高級產品也受到市場青睞,因為這些特性有助於醫療機構更嚴格地遵守相關規程。

與先進醫療設備和表面的材料相容性風險

在美國,相容性風險仍然是消毒劑和抗菌劑市場面臨的一大阻礙因素,尤其是在使用複雜、可重複使用的醫療設備和聚合物含量高的設備的環境中。化學不相容性會導致環境應力開裂、光學損傷和密封件劣化,這可能會縮短設備壽命並增加維修成本。根據PDI相容性文檔,不僅活性抗菌成分,而且溶劑、表面活性劑和pH調節劑等惰性成分也可能是造成表面劣化的主要原因。這使得感染控制團隊難以標準化,因為單一產品很少能適用於各種設備配置中所有已核准的表面。資金預算緊張加劇了這項挑戰,導致機器人手術系統和先進內視鏡設備的運作延長。儘管如此,這些限制正促使供應商開發針對特定表面的化學平台,以在不增加材料應力的情況下保持有效性。

細分市場分析

2025年,在美國消毒劑和滅菌劑市場中,季銨化合物(QACs)憑藉其適用於多種硬質和軟質表面的特性,以32.31%的市場佔有率保持領先地位。其廣泛的用途、低廉的使用成本以及與多種醫用塑膠的兼容性,意味著QACs在醫院和醫療機構的處方清單中仍然佔據重要地位。 QACs在美國消毒劑和滅菌劑市場的佔有率也反映了其在日常環境清潔程序中長期發揮的作用。然而,其地位並非完全穩固,因為一些感染預防團隊越來越關注有關微生物暴露於亞致死濃度QACs後產生抗藥性的報告。氯化合物仍然發揮著至關重要的作用,尤其是在與艱難梭菌和耳念珠菌消毒相關的方案中,在這些方案中,殺死孢子的性能比使用便利性更為重要。

預計從2026年到2031年,酵素性清潔劑的複合年成長率將達到11.38%,成為該領域成長最快的產品類型。推動市場需求成長的因素包括微創手術的增加、可重複使用器械日益複雜化以及無菌配製過程中對更徹底清潔程序的需求。多酶配方具有重要價值,因為它們可以在一次消毒前清潔步驟中分解蛋白質、脂質、碳水化合物和生物膜。醫療保健表面研究所的一項研究指出,即使是普通的清潔劑擦拭巾,在0.5%的應變下也會導致某些塑膠出現環境應力開裂,這解釋了為什麼醫療機構越來越重視材料的溫和性以及清潔性能。過氧化氫和過氧乙酸產品也因其兼具殺滅孢子和優異的生物分解性,在內視鏡再處理領域佔據越來越大的市場佔有率。醇類、醛類、雙胍類、碘衍生物和一些特殊化學物質在某些環境中仍然被使用,但隨著循證藥物清單的審查,低優先級產品的佔有率正在逐漸減少。

截至2025年,液體製劑將占美國抗菌消毒劑市場(按劑型分類)的52.24%,仍將是醫療機構使用最廣泛的劑型。對於需要低成本、大容量供應和靈活稀釋以實施廣泛環境衛生計畫的機構而言,液體製劑仍然是首選。美國環保署(EPA)註冊的一步式消毒清潔劑也支撐了液體製劑在美國抗菌消毒劑市場中的佔有率,這些清潔劑將清潔和消毒功能結合在一個工作流程中。噴霧劑和氣霧劑在小規模門診環境和難以觸及的表面仍然十分重要,而凝膠和泡沫劑在手部抗菌和傷口處理方面繼續發揮實用作用。

預計2026年至2031年間,擦拭巾的複合年成長率將達到10.52%,成為成長最快的劑型。其價值遠不止於便利性。由於是一次性使用,濕紙巾減少了稀釋誤差,並可在使用時精確控制活性成分濃度。醫療機構也認為擦拭巾有助於提高員工依從性,因為這種劑型易於培訓,且可在繁忙的護理區域實現標準化。藝康(Ecolab)於2024年7月推出的「消毒濕紙巾1號」(Disinfectant 1 Wipe)體現了供應商致力於將擦拭巾定位為超越普通商品的努力,它將快速消毒與可生物分解和無塑膠材料等優勢相結合。高樂氏(CloroxPro)於2025年9月推出的「螢幕+消毒濕紙巾」(Screen+Sanitizing Wipes)針對觸控螢幕、筆記型電腦和共用電子設備,進一步表明擦拭巾創新正在擴展到設備相關的護理工作流程中(但本文未引用該產品的市場調查數據)。未來隨著更多關於相容性和環境因素的可靠數據得到證實,人們對高階擦拭巾格式的傳統成本擔憂可能會減少。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 持續性醫院感染、耳念珠菌感染、多重抗藥性細菌(MDROs)所帶來的壓力

- 醫療保健和公共機構的永久性衛生標準

- 門診手術的普及增加了快速再處理的需求。

- 符合美國環保署N類清單及EVP標準的採購標準

- 修訂後的美國藥典無菌調配衛生管理標準

- 市場限制因素

- 與先進設備和表面的材料相容性風險

- 與向美國環保署/食品藥物管理局註冊、貼標籤和證明功效相關的負擔。

- 因污染導致的產品召回推高了品質保證成本和更換成本。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 季銨化合物

- 氯化合物

- 醇和醛類產品

- 雙胍類衍生物和碘類衍生物

- 過氧化氫和過氧乙酸

- 酵素性清潔劑

- 其他產品類型

- 配方

- 液體

- 擦拭巾

- 噴霧劑和氣霧劑

- 凝膠/泡沫配方

- 透過使用

- 表面消毒劑

- 醫療設備用高效消毒劑

- 設備和酵素性清潔劑

- 用於皮膚預處理的消毒劑

- 其他用途

- 最終用戶

- 醫院和診所

- 門診手術中心

- 長期照護機構及專業照護機構

- 檢查室和診斷中心

- 其他最終用戶

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Advanced Sterilization Products(ASP)

- Atlantis Consumer Healthcare Inc.

- Becton, Dickinson and Company

- Best Sanitizers, Inc.

- Cardinal Health Inc.

- Diversey, a Solenis Company

- Ecolab Inc.

- Kimberly-Clark Corporation

- Lonza LLC

- Medline Industries, LP

- Metrex Research, LLC

- PDI Healthcare

- Procter & Gamble Co.

- Reckitt Benckiser Group plc

- SC Johnson Professional USA, Inc.

- Solventum Corporation

- STERIS plc

- The Clorox Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states antiseptic and disinfectant market size was valued at USD 11.04 billion in 2025 and is estimated to grow from USD 12.14 billion in 2026 to reach USD 19.5 billion by 2031, at a CAGR of 9.95% during the forecast period (2026-2031).

This report is Segmented by Product Type (QACs, Chlorine Compounds, Alcohols & Aldehydes, Biguanides & Iodine, H2O2 & Peracetic Acid, Enzymatic Cleaners, Other), Formulation (Liquids, Wipes, Sprays & Aerosols, Gels & Foams), Application (Surface, Medical Device HLD, Instrument & Enzymatic, Skin Prep, Other), and End User (Hospitals, Ascs, LTC & SNFs, Labs, Other). Value (USD).

United States Antiseptic And Disinfectant Market Trends and Insights

Persistent HAI, Candida Auris, and MDRO Pressure

Healthcare-associated infections continue to support recurring demand across the US antiseptic and disinfectant market. CDC reporting for 2024 showed that U.S. hospitals reduced most HAI categories by 2% to 11% from 2023, but abdominal hysterectomy surgical site infections still increased by 8%, which shows that infection control performance remains uneven by procedure type. Candida auris has become a stronger procurement trigger because the CDC confirmed 6,304 clinical cases in 2024, up from 4,523 in 2023. Because C. auris is resistant across multiple antifungal classes, facilities rely more heavily on environmental disinfection and stronger sporicidal protocols than on treatment alone. This pressure no longer sits only inside acute hospitals, because long-term acute care hospitals and ventilator-capable skilled nursing facilities are also tightening purchasing standards after colonization and transmission events. That shift is widening the customer base for the US antiseptic and disinfectant market into post-acute settings that historically purchased less sophisticated products.

Permanent Hygiene Baselines Across Healthcare and Public Institutions

The post-pandemic hygiene floor has remained in place longer than many buyers first expected, which continues to support the US antiseptic and disinfectant market. CDC guidance and hospital infection prevention practices have kept more frequent surface turnover and disinfection routines embedded in day-to-day operations rather than emergency protocols. That means facilities can lower bed capacity or change service mix without producing a similar drop in disinfectant use. The more important demand driver is now disinfectant use intensity per occupied room, procedure area, and shared device. This makes volumes more resilient against hospital consolidation and slower demographic growth in mature care markets. It also creates room for premium products that reduce workflow errors, shorten kill times, or improve surface compatibility because those features help facilities hold tighter protocol compliance.

Material Compatibility Risk With Advanced Devices and Surfaces

Compatibility risk remains a practical restraint for the US antiseptic and disinfectant market, especially in settings that use complex reusable devices and polymer-heavy equipment. Incompatible chemistries can contribute to environmental stress cracking, optical damage, and seal degradation, which can shorten device life and increase repair cost. PDI's compatibility documentation states that inactive ingredients such as solvents, surfactants, and pH modifiers can be major contributors to surface degradation, not only the active antimicrobial ingredient. This makes standardization harder for infection control teams because one product rarely fits every approved surface across a mixed equipment base. The challenge becomes more severe as robotic surgery systems and advanced endoscopy assets remain in service longer under tighter capital budgets. Even so, this restraint is also pushing suppliers toward surface-aware chemistry platforms that try to protect efficacy without increasing material stress.

Other drivers and restraints analyzed in the detailed report include:

- Outpatient Surgery Migration Increasing Fast-Turn Reprocessing Demand

- EPA List N and EVP-Ready Procurement Standards

- EPA/FDA Registration, Labeling, and Claim-Substantiation Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

QACs held 32.31% of the US antiseptic and disinfectant market by product type in 2025, which kept them in the leading position because they work across many hard and soft surface use cases. Their broad utility, cost-in-use profile, and compatibility with many healthcare plastics continue to support large formulary positions across hospitals and institutional settings. The US antiseptic and disinfectant market share held by QACs also reflects their long-standing role in routine environmental cleaning programs. Even so, that position is not fully secure because some infection prevention teams are paying closer attention to documented tolerance patterns in organisms exposed to sub-lethal QAC concentrations. Chlorine compounds remain important where sporicidal performance matters more than convenience, especially in protocols tied to C. difficile and C. auris decontamination.

Enzymatic cleaners are forecast to expand at an 11.38% CAGR from 2026 to 2031, making them the fastest-growing product type in this segment. Demand is being pulled by minimally invasive surgery growth, higher reusable instrument complexity, and more intensive sterile compounding cleaning routines. Multi-enzyme formulations have value because they break down proteins, lipids, carbohydrates, and biofilm in a single cleaning step before disinfection. A Healthcare Surfaces Institute study presentation noted that even standard detergent wipes can induce environmental stress cracking in several plastics at 0.5% strain, which explains why facilities are paying more attention to material gentleness as well as cleaning performance. Hydrogen peroxide and peracetic acid products are also gaining space in endoscopy reprocessing because they combine sporicidal action with better biodegradability profiles. Alcohols, aldehydes, biguanides, iodine derivatives, and smaller niche chemistries continue to serve specific settings, but evidence-based formulary reviews are gradually compressing the tail of low-priority products.

Liquid formulations commanded 52.24% of the US antiseptic and disinfectant market by formulation in 2025, keeping them as the largest format across institutional use. Liquids remain the default choice where facilities need low cost per use, bulk dispensing, and flexible dilution for broad environmental services programs. The US antiseptic and disinfectant market size attached to liquids is also supported by one-step EPA-registered disinfectant cleaners that help sites combine cleaning and disinfection in a single workflow. Sprays and aerosols still matter in smaller outpatient settings and on hard-to-reach surfaces, while gels and foams keep a practical role in hand antisepsis and wound-related applications.

Wipes are projected to grow at a 10.52% CAGR from 2026 to 2031, which makes them the fastest-growing formulation. Their value is no longer limited to convenience because the unit-dose format also reduces dilution error and helps deliver a controlled active concentration at the point of use. Facilities also view wipes as helpful in staff compliance because the format is simpler to train and easier to standardize across fast-paced care areas. Ecolab's Disinfectant 1 Wipe launch in July 2024 showed how suppliers are pairing rapid disinfection claims with biodegradability and plastic-free positioning to move wipes beyond commodity status. CloroxPro's September 2025 Screen+ Sanitizing Wipes launch, which targeted touchscreens, laptops, and shared electronics, further showed that wipe innovation is extending into device-adjacent care workflows, although the supporting market-research citation behind that product reference is not used here. Over time, stronger compatibility data and environmental credentials are likely to narrow the historic cost objection to premium wipe formats.

Complete Report Scope:

- By Product Type

- Quaternary Ammonium Compounds

- Chlorine Compounds

- Alcohols & Aldehyde Products

- Biguanides & Iodine Derivatives

- Hydrogen Peroxide & Peracetic Acid

- Enzymatic Cleaners

- Other Product Types

- By Formulation

- Liquids

- Wipes

- Sprays & Aerosols

- Gels & Foams

- By Application

- Surface Disinfectants

- Medical Device High-Level Disinfectants

- Instrument & Enzymatic Cleaners

- Skin Preparation Antiseptics

- Other Applications

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Long-Term Care & Skilled Nursing Facilities

- Laboratories & Diagnostic Centers

- Other End Users

List of Companies Covered in this Report:

- Advanced Sterilization Products (ASP)

- Atlantis Consumer Healthcare Inc.

- Beckton Dickinson

- Best Sanitizers, Inc.

- Cardinal Health

- Diversey, a Solenis Company

- Ecolab

- Kimberly-Clark Worldwide

- Lonza LLC

- Medline Industries

- Metrex Research, LLC

- PDI Healthcare

- Procter & Gamble

- Reckitt Benckiser Group

- SC Johnson Professional USA, Inc.

- Solventum Corporation

- STERIS

- The Clorox Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Persistent HAI, Candida auris, and MDRO pressure

- 4.2.2 Permanent hygiene baselines across healthcare and public institutions

- 4.2.3 Outpatient surgery migration increasing fast-turn reprocessing demand

- 4.2.4 EPA List N and EVP-ready procurement standards

- 4.2.5 Revised USP sterile-compounding hygiene intensity

- 4.3 Market Restraints

- 4.3.1 Material compatibility risk with advanced devices and surfaces

- 4.3.2 EPA/FDA registration, labeling, and claim-substantiation burden

- 4.3.3 Product contamination recalls raising QA and switching costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Quaternary Ammonium Compounds

- 5.1.2 Chlorine Compounds

- 5.1.3 Alcohols & Aldehyde Products

- 5.1.4 Biguanides & Iodine Derivatives

- 5.1.5 Hydrogen Peroxide & Peracetic Acid

- 5.1.6 Enzymatic Cleaners

- 5.1.7 Other Product Types

- 5.2 By Formulation

- 5.2.1 Liquids

- 5.2.2 Wipes

- 5.2.3 Sprays & Aerosols

- 5.2.4 Gels & Foams

- 5.3 By Application

- 5.3.1 Surface Disinfectants

- 5.3.2 Medical Device High-Level Disinfectants

- 5.3.3 Instrument & Enzymatic Cleaners

- 5.3.4 Skin Preparation Antiseptics

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Long-Term Care & Skilled Nursing Facilities

- 5.4.4 Laboratories & Diagnostic Centers

- 5.4.5 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)}

- 6.3.1 Advanced Sterilization Products (ASP)

- 6.3.2 Atlantis Consumer Healthcare Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Best Sanitizers, Inc.

- 6.3.5 Cardinal Health Inc.

- 6.3.6 Diversey, a Solenis Company

- 6.3.7 Ecolab Inc.

- 6.3.8 Kimberly-Clark Corporation

- 6.3.9 Lonza LLC

- 6.3.10 Medline Industries, LP

- 6.3.11 Metrex Research, LLC

- 6.3.12 PDI Healthcare

- 6.3.13 Procter & Gamble Co.

- 6.3.14 Reckitt Benckiser Group plc

- 6.3.15 SC Johnson Professional USA, Inc.

- 6.3.16 Solventum Corporation

- 6.3.17 STERIS plc

- 6.3.18 The Clorox Company

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

高級消毒服務市場:全球產業規模、市場佔有率、趨勢、機會和預測(按服務、最終用戶和地區分類)、競爭格局(2021-2031 年)

高級消毒服務市場:全球產業規模、市場佔有率、趨勢、機會和預測(按服務、最終用戶和地區分類)、競爭格局(2021-2031 年) 溴硝醇市場:依劑型、應用及最終用途產業分類-2026-2032年全球市場預測防腐劑和消毒劑市場:2026-2032年全球市場預測(按產品類型、配方、作用頻譜、應用、最終用戶和銷售管道分類)

溴硝醇市場:依劑型、應用及最終用途產業分類-2026-2032年全球市場預測防腐劑和消毒劑市場:2026-2032年全球市場預測(按產品類型、配方、作用頻譜、應用、最終用戶和銷售管道分類) 消毒劑市場:按應用、劑型、最終用戶和地區分類消毒劑市場:2026-2032年全球市場預測(依產品類型、劑型、應用、最終用戶、通路及包裝類型分類)高級消毒服務市場:按服務類型、交付方式和最終用戶分類-2026-2032年全球市場預測

消毒劑市場:按應用、劑型、最終用戶和地區分類消毒劑市場:2026-2032年全球市場預測(依產品類型、劑型、應用、最終用戶、通路及包裝類型分類)高級消毒服務市場:按服務類型、交付方式和最終用戶分類-2026-2032年全球市場預測 全球抗菌消毒劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)食品級抗菌消毒劑市場:依產品類型、原料、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測十六烷基三溴甲烷化銨市場:2026-2032年全球市場預測(按應用、劑型、等級、通路和最終用戶分類)

全球抗菌消毒劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)食品級抗菌消毒劑市場:依產品類型、原料、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測十六烷基三溴甲烷化銨市場:2026-2032年全球市場預測(按應用、劑型、等級、通路和最終用戶分類) 溴硝醇市場報告:按類型、劑型、應用和地區分類,2026-2034年

溴硝醇市場報告:按類型、劑型、應用和地區分類,2026-2034年